Dominican Republic

Robust growth prospects, persistent structural weakness

| GDP | USD 113.64bn (World ranking 65) |

| Population | 11.23mn (World ranking 83) |

| Form of state | Presidential republic |

| Head of government | Luis Abinader (President) |

| Next elections | 2024, Presidential |

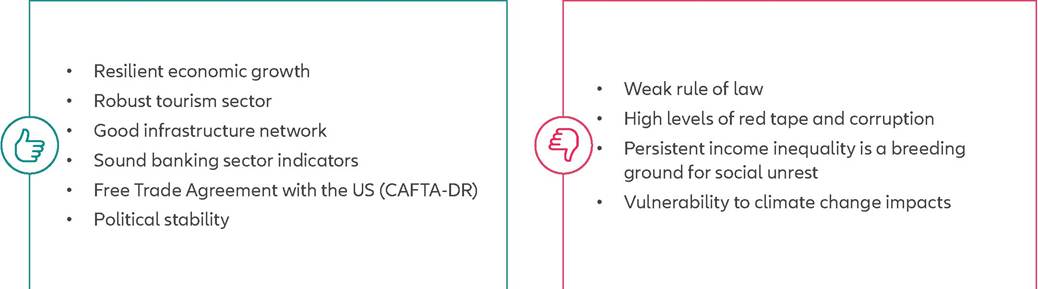

Strengths & weaknesses

Economic overview

Steady amid storms

Over the past decade, the Dominican Republic has emerged as one of Latin America and the Caribbean's fastest growing economies, boasting an average growth rate of around +5% per annum.

Although the country was not insulated from the impact of the pandemic, it has since made a full recovery, with +12.3% real GDP growth in 2021 and +4.9% in 2022. The latter was largely fueled by its services sector (which accounts for approximately 55% of GDP), along with expansionary fiscal policies. In 2023, the pace of growth slowed to an estimated +3.5%, affected by a global economic slowdown that took a toll on exports, even in the face of record-breaking tourism numbers. Looking ahead to 2024, while a deceleration in tourism numbers is anticipated, a more relaxed monetary policy and a normalizing external environment are expected to push growth to +4.3%, offsetting a predicted slowdown in the agriculture (an important employment sector) as a consequence of El Nino-related droughts. Over the longer term, the implementation of a planned tax reform in 2025 is likely to constrain domestic demand, resulting in a slightly lower average GDP growth of +4.2% between 2025 and 2028.Like many other Latin American countries, the Dominican Republic is highly dependent on oil imports. This vulnerability was exposed by supply chain disruptions arising from the Russia-Ukraine conflict which culminated in the Dominican Republic experiencing 8.8% y/y inflation in 2022. However, inflationary pressures have started to wane, dropping to around 4.3% in late 2023. They are projected to decline further to 4.2% by the end of 2024, partly due to falling commodity prices as well as the expected extension of existing fuel and electricity subsidies. This being said, a sluggish US recovery could curb tourism and suppress inflation more than anticipated, while higher than anticipated tourism could have the opposite effect. Additionally, an earlier-than-expected withdrawal of fuel and electricity subsidies or a weaker peso could exert upward pressure on prices.

Amidst a backdrop of easing inflation, the Central Bank of the Dominican Republic (BCRD) has shifted towards a more accommodative monetary stance, moving away from the tighter policies previously enacted. The benchmark interest rates, which had peaked at 8.5% early in 2023 to counter the effects of global supply disruptions, have been revised to 7.5% as of August 2023. It is projected that the policy rate will undergo a methodical decline to an estimated 6% by early 2024 and reach a terminal rate of 5.5% later the same year. Accompanying these rate adjustments, the BCRD has also relaxed legal reserve requirements for banks and increased liquidity through open-market operations

All's well, mostly...

Part of the story behind the Dominican Republic's region leading growth over the past two decades has been prudent fiscal and monetary policy which have supported macroeconomic stability. However, unlike its economy, the country's fiscal position has yet to fully recover from pandemic disruptions. Public debt in 2023 is estimated to be around 56% of GDP, higher than the 52% pre-pandemic. This slower recovery of public finances can be attributed to government efforts to mitigate the impact of price increases on the population through increased subsidies for fuel and energy. Although, these inflationary pressures have begun to ease, the fiscal deficit is expected to remain broad in 2024, influenced by spending related to upcoming May 2024 general elections.

However, projections indicate the deficit may begin to narrow again in 2025, contingent on the likely re-election of the current Abinader administration and its anticipated focus on restrained spending and long-overdue tax reforms.After widening to 5.6% of GDP in 2022 amid softer exports and higher commodity prices, the current-account deficit is on a path of contraction. It's projected to decrease from 4.3% in 2023 to 3.7% in 2024, led by robust exports and global economic recovery. Although the deficit is anticipated to linger between 2024 and 2028, it should progressively narrow, supported by increasing remittances and tourism revenue. While BCRD's loosening monetary policy may curb capital inflows due to a smaller US interest-rate gap, FDI is still expected to rise, boosted by nearshoring activities by USbased firms. While short-term risks such as tightening global financial conditions and sluggish global growth persist, they're more balanced in the medium term, suggesting a sustainable external position.

Surface Political Stability, Deep-Rooted Challenges

In the short term, political risks appear limited as President Luis Abinader of the Partido Revolucionario Moderno holds a strong congressional majority and enjoys high approval ratings. While his re-election in the upcoming May 2024 general election is widely expected, the president's marketfriendly agenda is likely to stall until then. If re-elected, the landscape of low governability risks should continue, despite lingering issues with weak public institutions and poor accountability. While government efforts to enhance the rule of law are likely to prevent large-scale disturbances, sporadic protests ignited by corruption scandals could still occur. Further fueling public unease are persistent social issues, such as high unemployment, income inequality, escalating crime and unreliable electricity. External political risks largely stem from the Abinader administration's contentious policies towards Haitian migrants, including closure of the border and deportations of undocumented migrants.

These actions have strained its largely amicable relationship with the US, its main trade partner and largest source of foreign investment. Although the probability is low, there exists the risk that the US may intensify existing sanctions should it perceive a deterioration in the treatment of Haitians.Despite its market-oriented economic policies and advantageous geographical proximity to the US, the country's business environment remains below its full potential. Principal shortcomings include unstable governance systems and gaps in vital areas such as educational facilities and its electrical network. The government has a strong commitment to electricity sector reform which points to a long-term vision, but quick fixes are unlikely. This same long-term perspective applies to a shortage of human capital, which remains a bottleneck for business sector growth. Weak intellectual property protections add another layer of complexity, undermining an otherwise robust entrepreneurial environment. This weakens R&D investment and translates into sparse patent activity, ultimately hindering the generation of quality jobs.

In spite of these challenges, the Dominican Republic's long-term economic outlook is cautiously optimistic. Yet its 23rd ranking (out of 191 countries) in the 2023 Inform Risk Index underscores the urgent need for climate resilience strategies. Increased frequency and severity of natural disasters, exacerbated by climate change, put both economic growth and vulnerable communities at risk. Addressing this issue is crucial for sustaining progress and mitigating social inequalities.