Estonia

Caught in protracted recession

| GDP | USD38.1bn (World ranking 100) |

| Population | 1.3mn (World ranking 155) |

| Form of state | Parliamentary Republic |

| Head of government | Kaja Kallas (PM) |

| Next elections | 2026, Presidential |

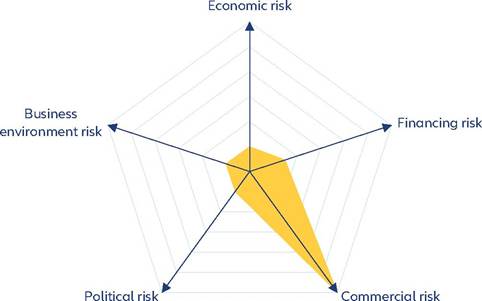

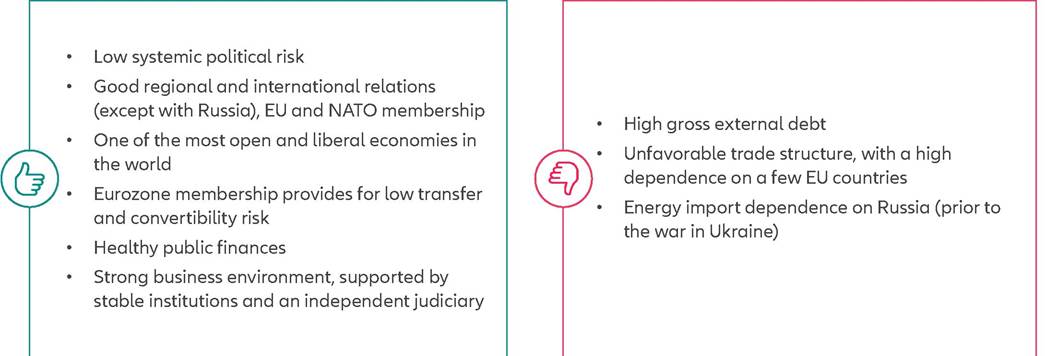

Strengths & weaknesses

Economic overview

Slow recovery in 2024-2025

Estonia's economic outlook has sharply deteriorated as a result of the war in Ukraine.

This is mainly due to the country's geographic proximity to Russia and its significant (pre-war) trade relations (accounting for 8% of Estonia's exports, 10% of its imports and, notably, 46% of its natural gas imports). Following a strong post-Covid-19 rebound with +7.2% real GDP growth in 2021, economic activity in Estonia cooled rapidly in 2022 amid surging inflation, rising interest rates, weakening external demand and deteriorating business confidence. In q/q terms, real GDP has contracted for seven consecutive quarters from Q1 2022 until Q3 2023, taking the economy into full-year recession in 2022 (-0.5%) and 2023 (-3.4% in the first three quarters). Looking ahead, we expect Estonia to exit recession in the course of 2024, in part due to base effects and in part thanks to an eventual modest recovery of trade with Western Europe. Government fiscal stimulus and EU fund inflows should also help. We forecast full-year real GDP to expand by around +1% in 2024 and +2.5% in 2025.Inflationary pressures will remain elevated in 2024.

Consumer price inflation rose to double digits at end-2021 and remained there until mid-2023 (with a peak of 25% y/y in August 2022), driven by surging energy and food prices as well as interrupted supply chains. In the meantime, it has come down to 4% at end-2023 thanks to base effects, moderated energy prices and weak domestic demand. As these effects will gradually wane in 2024, we forecast inflation to remain in the range of 3-4% in 2024. Meanwhile, Eurozone membership provides for moderate transfer and convertibility risk in Estonia.Public and external finances have weakened but remain unproblematic

Estonia's public finances will remain manageable despite strong fiscal stimulus measures taken in 2020-2021 to mitigate the economic impact of the Covid-19 crisis and renewed, albeit more moderate, stimulus to mitigate the impact of the recession in 2022-2023. The government posted fiscal deficits of -5.4% of GDP in 2020, -2.5% in 2021 and -1.0% in 2022. We forecast the annual shortfalls to increase to the range of -2.5% to -3.0% in 2023-2025, driven by rising wages and pensions as well as new permanent spending for defense, education and child benefits. At the same time, fiscal revenues have deteriorated due to the lasting recession. As a result, public debt increased from just 8.5% of GDP in 2019 to slightly more than 20% and is projected to remain above that threshold in the next years. However, this will still be very low compared to peers or the Eurozone average and in fact means that Estonia should have more room for fiscal leeway if needed.

Estonia's external finances should remain manageable as well. Following seven years of annual surpluses from 2013 to 2019, the current account posted moderate deficits equivalent to -1.0% of GDP in 2020 and -1.8% in 2021, mainly due to a relative strong import performance in the context of a domestic investment boom. The annual shortfalls widened to almost -3.0% of GDP in 2022-2023 owing to sharply increased prices for energy and food imports.

Going forward, we forecast the annual deficits to narrow somewhat in 20242025 as global energy prices have moderated.Gross external debt is elevated in Estonia, having risen from 76% of GDP in 2019 to around 90% in 2023 in the wake of the Covid-19 crisis and the impact of the war in Ukraine. We forecast the ratio to remain close to 90% in the next few years amid weak economic growth potential. Meanwhile, shortterm external debt as a share of gross debt has fallen to 34% as of September 2023, after it had increased from just 28% in 2018 to around 40% in mid-2022. Overall, any concern about the gross external debt position is mitigated by the fact that Estonia remains a net external creditor and has actually enlarged that position in recent years. At end-2023, net external assets accounted for around 31% of GDP.

Strong business environment and moderate political risk

The business environment for corporates in Estonia is very strong. The World Bank's annual Worldwide Governance Indicators surveys suggest that the regulatory and legal frameworks are business-friendly and the level of corruption is low. Likewise, the Heritage Foundation's annual Index of Economic Freedom surveys have put Estonia in the top ten out of around 180 economies in recent years (rank 6 in 2023), reflecting very strong scores with regard to property rights, judicial effectiveness, government integrity, tax burden, trade freedom and investment freedom; only labor freedom is scored below average. With regard to environmental sustainability, Estonia scores somewhat less favorably, owing to a low level of renewable electricity output and a moderate recycling rate. However, the country does well with regard to energy intensity, water stress and overall vulnerability to climate change and has significantly improved in terms of CO2 emissions in recent years. In all, Estonia has climbed to rank 57 out of 210 economies in our proprietary Environmental Sustainability Index, up from rank 70 a year ago.

Overall systemic political risk has deteriorated somewhat from a previously low level because geopolitical risk in the region has increased with the war in Ukraine. Estonia is a well-established democracy and has good international relations - except with Russia - reflected in its EU, OECD and NATO membership. However, there is a risk that social tensions are emerging from the sizeable Russian-speaking minority in Estonia.