The Optimal Inflation Rate

A consensus seemed to exist until a few years ago that monetary transactions costs are relatively small at zero inflation and that implementing low and stable inflation is the proper policy.[35] Optimal monetary policy analyses (Khan, King and Wolman 2003; Schmitt-Grohe and Uribe 2004) identify two key frictions driving the optimal level of long-run (or trend) inflation.

The first is the adjustment cost of goods prices, which invariably drives the optimal inflation rate to zero. The second is monetary transaction costs that arise unless the central bank implements the Friedman rule, i.e. a zero nominal interest rate implying a negative inflation rate in steady state. On balance, i.e. considering these two frictions together, the optimal inflation rate should be negative, but close to zero.In their survey of the literature, Schmitt-Grohe and Uribe (2011) argue that the optimality of zero inflation is robust to other frictions, such as nominal wage adjustment costs, downward wage rigidity, hedonic prices, the existence of an untaxed informal sector and the zero bound on the nominal interest rate. This result is broadly confirmed by Coibion, Gorodnichenko and Wieland (2012), who find that the optimal inflation rate is low, typically less than 2 per cent, but is in sharp contrast both with empirical evidence and widespread central bank practice of adopting inflation targets between 2 and 4 per cent.

Some contributions (e.g. Rogoff 2010; Blanchard, Dell'Ariccia and Mauro 2010; Aizenman and Marion 2011; Ball 2014) in some ways evoked the well-known Phelps (1973) argument that to alleviate the burden of distortionary taxation, it might be optimal for governments to resort to monetary financing, driving a wedge between the private and social costs of money. This argument has been neglected for about four decades, possibly also because the New Keynesian models widely adopted since the 1990s offer what has been called the ‘divine coincidence' between low inflation and zero output gap (Blanchard, Dell'Ariccia and Mauro 2010).

After a few voices had risen after 2010 in favour of a higher long-run inflation target, the importance of the Phelps effect was reconsidered only recently, in a DSGE model (Di Bartolomeo, Tirelli and Acocella 2015; Tirelli, Di Bartolomeo and Acocella 2015). This leads to results that challenge the optimality of near-zero inflation rates when the tax system is incomplete. A non-negligible - but moderate - inflation rate can indeed be optimal, and inflation (and tax rate) volatility should be exploited in order to get rid of the debt accumulated after 2008 as well as to stabilise debt/gross domestic product (GDP) ratio in the long run. This is obtained simply by allowing for a plausible parameterisation of public consumption and transfers. As a matter of fact, public consumption accounts for a limited component of overall public expenditures in some Organisation for

Table 3.1 Public consumption, other public expenditures and total revenues,0 selected OECD countries (1998-2008)

| Public consumption | Other public expenditures | Total revenues | |

| Sweden | 26.67 | 29.03 | 57.21 |

| Switzerland | 11.4 | 23.48 | 34.40 |

| United Kingdom | 19.83 | 22.28 | 40.38 |

| United States | 15.26 | 20.51 | 33.47 |

| Euro area | 20.17 | 27.11 | 45.39 |

a Average ratios to GDP.

Source: OECD 2012.

Economic Co-operation and Development (OECD) countries, and transfers are relatively large (Table 3.1).

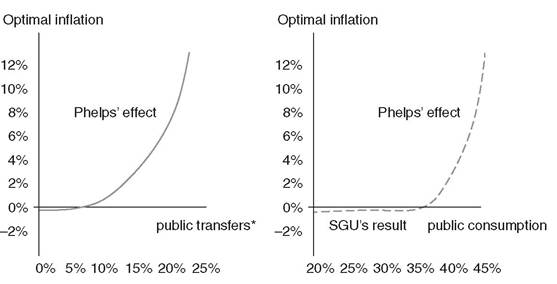

Contrary to Schmitt-Grohe and Uribe (2004), the optimal inflation rate monotonically increases from 2 to 12 per cent as the transfers-to-GDP ratio goes from 10 to 20 per cent, a result their model can obtain only with very large public- consumption-to-GDP ratios, in an order of magnitude ranging from 40 to 47 per cent.

The rationale of this result is related to the different effects of public consumption and transfers on tax and inflation revenues and thus to the different incentives to use taxes or inflation to finance them. An increase in public consumption reduces private consumption and money holdings while potentially raising the labour supply (depending on the effects of public expenditure on output). Reductions in private consumption and money holdings erode the inflation tax base. The rising labour supply increases the tax base, making an increase in the distortionary tax rate unnecessary. In other words, increases in public consumption make it more likely that taxes can finance it compared with inflation. By contrast, transfers have no impact on overall

100

Re-establishing the First Pillar

(*) Additional to 20% of expenditure in public consumption.

Figure 3.1 Optimal inflation rates with and without fiscal transfers.

(Source: Di Bartolomeo, Tirelli and Acocella 2015)

consumption and labour supply and thus do not favour ordinary tax financing of public expenditure vis-a-vis an inflation tax (see Figure 3.1).

In advocating a higher inflation rate, one should consider that it has both benefits and shortcomings. From the former point of view, while being useful as a way of paying down the value of outstanding public debt and reducing future taxes, it has other advantages. In fact, it also reduces the value of extant private debt, thus possibly stimulating investment and discriminating between types of assets in favour of mobilisation of capital.

In addition, it can get rid of the ‘zero-lower- bound’ (ZLB) constraint by lowering real interest rates. Finally, contrary to other results (e.g. Albanesi 2007), it can reduce inequality if implemented in combination with lower income taxes (Menna and Tirelli 2017).Some costs and risks of permanently raising target inflation rates exist. These can refer to the increase in long-term nominal interest rates that would follow as an effect of higher interest rates, but this is usually lower than the increase in the inflation target. Some authors also fear the ensuing loss in

the credibility of central banks deriving from expectations of further increases in the target. However, this appears as well established, and a simultaneous increase in advanced countries’ target inflation rate should do no damage.

As for dissent on the opportunity to raise the inflation rate, Mishkin (2011) argues that very deep recessions such as the one begun in 2007-8 are very rare, and then the risk of easily reaching a constraining ZLB is not very relevant. Then the benefits from a higher inflation target would not be very large.[36] Instead, a higher inflation rate would cause distortions in cash holdings and greater uncertainty about relative prices and possibly undesired redistribution of wealth. As a matter of fact, however, most empirical estimates find limited effects of this kind (Ball 2014). As to the effects on expectations, Mishkin fears that people’s expectations on future inflation will keep on rising. Piketty (2013) holds that the initial positive effect can partly disappear over time because people’s expectations can change. Bernanke (2010), Mishkin (2011) and Woodford (2009), in their papers cited by Ball (2014), are sceptical about targeting a higher inflation rate, say, at 4 per cent, since people would think that going to 4 per cent is only a first step to going to 6 per cent or more, and it would be very difficult to tie down expectations at 4 per cent.

However, in Ball’s opinion, the ‘central bank should determine its optimal policy, explain this policy to the public, and carry it out. We have learned from recent experience that 4 per cent inflation is better than 2 per cent, because of the zero bound problem. Why can’t policymakers explain this, raise inflation to 4 per cent, and keep it there?’ (Ball 2014: 14), which seems to us a very reasonable argument. Along a similar line of reasoning, Blanchard, Dell’Ariccia and Mauro (2010: 11) provocatively ask ‘is it more difficult to anchor expectations at 4 percent than at 2 percent?' This issue of expectations must be dealt with carefully. In fact, what matters is obtaining a stable pattern of higher inflation expectations. This can be very useful from another point of view, i.e. in lowering the expected real interest rate in a way that counteracts secular stagnation (see Section 5.7).Another possible shortcoming of a higher inflation rate target can derive from the possibility that the inappropriate timing to implement this policy might generate or feed bubbles in the asset markets (Wolff 2014). This is really a relevant point, and we underline it later (see Chapter 5), but it should not be overemphasised. The true problem is that policymakers should be well aware of this possibility and introduce additional tools to counteract the risk, such as macro-prudential policies. Finally, there are the effects of distortions arising from a higher inflation. These are of two kinds at least. The first kind has to do with distortions on money holdings. Another argument in favour of a low inflation rate target is that a strong anti-inflationary policy mitigates the adverse effects of uncertainty on aggregate demand, as hiring decisions play a significant role in transmitting uncertainty (Guglielminetti 2016). Both distortions cannot be denied. The real issue is to compare them with those from higher taxation. In all probability, the costs of an inflation target of 4 per cent rather than 2 per cent are not significantly higher.[37]

3.6