Tunisia

Stalling without falling (for now)

| GDP | USD46.7bn (World ranking 90) |

| Population | 12.4mn (World ranking 78) |

| Form of state | Republic |

| Head of government | KaTs SaTed (President) |

| Next elections | 2024, Presidential |

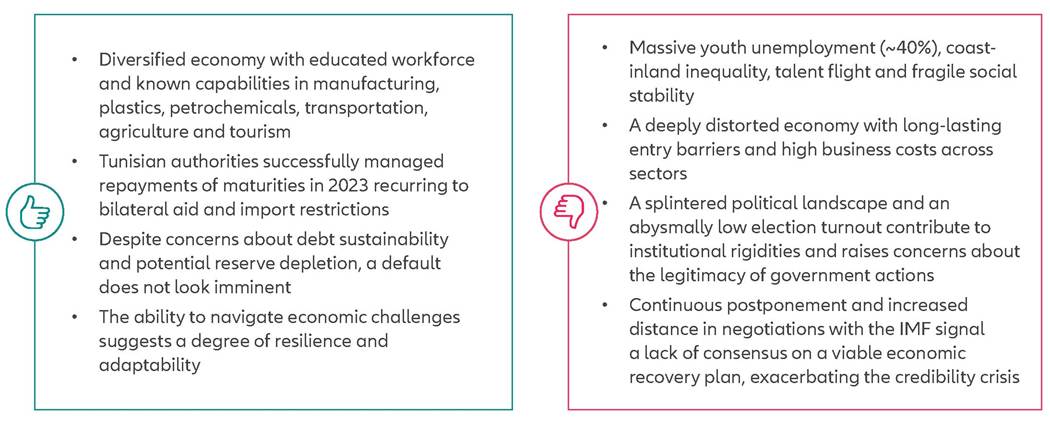

Strengths & weaknesses

Economic overview

Debt sustainability concerns will persist until 2026

Economic stagnation in 2023 with an estimated +0.9% GDP growth is forecast to be followed by +1.8% growth in 2024 as a result of stalling negotiations with the IMF, political turmoil, sluggish growth in Europe (Tunisia's main export partner) and a prolonged tightening cycle across advanced economies.

Concerns about debt sustainability will accompany Tunisia at least until 2026, since around 52% of the Tunisian public debt comes to maturity between 2024 and that year. The sum of the current account deficit and external debt repayments maturing in the next 12 months is forecast at around USD5bn, with international reserves standing at USD8.1bn as of October 2023 (equivalent to eight months of 2023 imports). This means that a depletion of reserves throughout the year is likely should negotiations with international lenders keep stalling, but a default should not materialize even without rapid IMF support. Tunisian authorities managed to repay Eurobond maturities in 2023 (USD166mn in yen- denominated guaranteed bonds in August and EUR500mn in euro-denominated bonds in October) as repayments were stipulated in the 2023 Budget Law.

A EUR850mn Eurobond is maturing in February 2024, representing almost half of the total amount of sovereign debt maturing in the year. Therefore, the balance of payments will remain under pressure as long as external financing remains limited and the current account posts a deficit even under persistent import restrictions.A deeply distorted economy, with long-lasting entry barriers and elevated costs for businesses

Negotiations with the IMF have been continuously postponed through 2023 and seem to remain the only way out of the economic and credibility crisis that has enveloped the country since 2022. The board of the International Monetary Fund (IMF) has yet to approve a bailout package for Tunisia originally discussed for USD1.9bn. The package, which may help restore external and fiscal stability as well as provide social protection, was tentatively agreed upon with Tunisian authorities in October 2022 and widely seen as a multiplier of much-needed international financial assistance for an amount of around USD5bn, equivalent to 4% of Tunisia's GDP. The distance between the two sides has increased and it is now unlikely that a staff-level agreement on a financing deal with Tunisia will be signed in the short term. In addition, Tunisia's performance under previous IMF programs has been poor. The last IMF agreement was terminated in March 2020, earlier than intended, due to the protracted parliamentary and presidential election cycle at the time and with just five out of eight reviews completed.

The economy remains deeply distorted, with elevated entry barriers because of market concentration and inflated costs of doing business across sectors due to factors such as onerous regulations on investment, trade and permits, limited access to capital and expanding government bureaucracy. Redundancies in the public sector, difficult conditions for agricultural workers and still-subdued demand from tourists weigh on long-term economic prospects. Tensions between the government and trade unions, including the Nobel Peace Prize winner UGTT (Tunisian General Labor Union), remain latent and led to the arrest of political opponents amid concerns over spending cuts affecting the public sector, with public salaries totaling 15% of GDP.

The agricultural sector employs about 15% of the country's workforce and remains particularly vulnerable to climate change and water management in the absence of foreign investment. Tourist receipts dropped to USD1.3bn in 2022 (2.9% of GDP) and are estimated at USD2bn for 2023, still far from USD3.5bn recorded in 2010 (7.5% of GDP), the year before the Arab Spring unfolded from Tunisia across Northern Africa and the Middle East. In contrast, regional peers such as Morocco and Egypt were able to return to 2010 levels already in 2016-2017.A splintered political landscape exacerbates Tunisia's institutional rigidities

The economic and social turmoil in Tunisia, the cradle of the Arab Spring pro-democracy movement more than a decade ago, has only increased since President Kais Saied seized power, began cracking down on his opponents and suspended the Parliament in July 2021. In July 2022, a new constitution came in, which gave almost absolute power to the president. In March 2023, the first session of Parliament took place after legislative elections highlighted record- high abstention rates on both rounds on the back of calls for a boycott from opposition parties. Elections to the new second chamber of parliament were held on 24 December 2023. Opposition parties boycotted the poll and turnout was once again minimal. Official participation numbers in the referendum to accept his new constitution (30%), a new parliament with reduced powers (11.2%) and the December municipal elections (11.6%) have all been gravely low. Under the new constitution introduced by President Saied, the latter election serves to put in motion a parliamentary chamber that will aid in government spending and regional development initiatives. The poor turnout is clearly frustrating President Saied's efforts to legitimize his authority.

Moreover, public statements by President Saied against Black communities raised tensions across the country as well as with Sub-Saharan partners and multilateral lenders. An increasing flow of migrants from Tunisia has also accompanied the government's quest for a normalization of diplomatic relationships with Europe and negotiations for further financial assistance. The arrest of former parliamentary speaker and opposition leader Rached Ghannouchi in April 2023 confirmed that the clampdown on civil liberties is far from over and this is likely to alienate donors and multilateral institutions for a long time, as well as increase reputational risk for companies dealing with Tunisian entities associated with the regime.