Business Cycle and Fiscal Policy

If the fact that Samuelson was working closely with Hansen was only hinted at in the summary of his talk to the American Economic Association, it was explicit in the article he published in May 1939, presumably written in late 1938 or very early in 1939, “Interactions Between the Multiplier Analysis and the Principle of Acceleration.”17 On the first page he acknowledged Hansen's help, saying that the paper had been written at his suggestion and that “Professor Hansen has developed a new model sequence which ingeniously combines the multiplier analysis with that of the acceleration principle or relation.”18

Hansen produced a model in which the multiplier was ½ and the accelerator was 2, and to his surprise found that income went into decline.

He thought that perhaps this could explain the 1937 recession and discussed it with Samuelson.19 Samuelson recognized Hansen's system as a difference equation that would produce repeated oscillations Hansen would have discovered had he solved it for more periods. Samuelson formulated the model algebraically, allowing the values of the multiplier and accelerator to take any meaningful values, and he found a general solution, working out combinations of multiplier and accelerator, that would produce stability, instability, or periodic fluctuations.aHowever, though Samuelson could readily understand such algebra, it was unfamiliar to most economists, which explains the way he chose to describe the theory. He started with an austere numerical example: initially government spending, investment, and consumption are zero. In the first period, government spending rises to ι and stays at that level. Samuelson then worked out, period by period, the new levels of consumption and investment, assuming that the marginal propensity to consume was ½ and the accelerator was ι.

These results were chosen so that the result was a cycle, with total income converging to its new equilibrium only after fourteen periods? Then, to show that the problem was too complicated for such reasoning, he went through the same calculation for four more sets of values for the multiplier and accelerator, demonstrating that they generated completely different results.a. The multiplier could be anywhere in the range zero to ι, and the accelerator had to be positive.

b. The new equilibrium is approached asymptotically; this calculation assumes very small discrepancies are ignored.

The only way to analyze the problem, Samuelson concluded, was to turn to algebra. Formulating the model as two difference equations, in which consumption depended on income in the previous period, and investment depended on the change in consumption from one period to the next, he was able to construct a diagram that showed how the system would behave for any combination of feasible values for the multiplier and accelerator. This led him to a methodological conclusion: “Contrary to the impression commonly held, mathematical methods properly employed, far from making economic theory more abstract, actually serve as a powerful liberating device enabling the entertainment and analysis of ever more realistic and complicated hypotheses.”20 The paper was used to argue the case for mathematical reasoning. Unlike some of his earlier papers, in this one he augmented his mathematics with verbal and diagrammatic explanations that made clear both the importance of the problem he was tackling and the usefulness of the mathematics. Perhaps this was because Hansen needed this type of explanation.

The paper is also interesting because of the way he framed the problem. His first sentence conceded that the new “multiplier” analysis had thrown light on the problem of government spending. He then went on to express the fear that “this extremely simplified mechanism” might be hardening into a dogma, “hindering progress and obscuring important subsidiary relations and processes.”21 This was precisely the situation with the multiplier that he had discussed in his presentation to the American Economic Association.

What his analysis showed was that “the conventional multiplier sequences [were] special cases of the more general Hansen analysis.”22 A page later he reiterated this point by saying that “the Keynes-Kahn-Clark formula” was “subsumed under the more general Hansen analysis.” In a footnote, he minimized the originality of his own work by claiming that his model was formally identical to the model sequences investigated by the Swedish economist Erik Lundberg and the Dutch econometrician Jan Tinbergen.This makes clear that when he wrote this paper, Samuelson was following Hansen in fitting ideas that were coming to be associated with Keynes into the older framework of American business cycle theory, and that these ideas were widely held. This was made even clearer in his second article on the subject, published in the Journal of Political Economy in December.23 Whereas his previous paper had used the accelerator to complicate the theory of the multiplier, this one used the multiplier to add a missing element to business cycle theories based on the accelerator. The idea behind the multiplier was not new—the idea that “actual movements of consumer demand depend on the movements of purchasing power; and these in turn are governed by the rate of production in general” was well established—but the mechanism and the mode of its interaction with the accelerator were not understood.24

Samuelson related his theory to debates that took place in 1931—32 concerning the role of consumer spending in the cycle and involving Charles Hardy, Ragnar Frisch, and John Maurice Clark. These writers, he claimed, realized that to explain fluctuations it was necessary to explain both investment and saving, but while they formulated the acceleration principle very clearly, they were less clear on what determined consumption. This is where Keynes came in, providing a clear statement of the multiplier that could be placed alongside the accelerator to make a fully specified theory.25 The General Theory had been followed by work by Roy Harrod, Gottfried Haberler, and Hansen, who brought the two concepts together into a theory that could explain turning points, and hence the cycle.

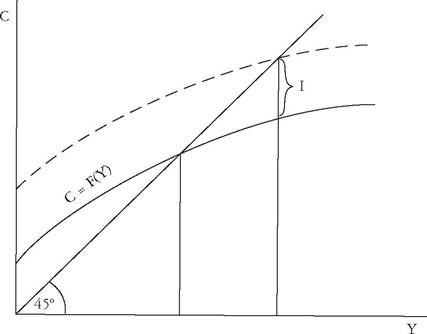

The problem with this literature was that there was no overall agreement on how to formulate the theory, and their work contained many flaws. There was, for example, confusion over the roles of net and gross investment, and about what caused the downturn at the top of the cycle.After this brief review of the literature, Samuelson proceeded to cut though the confusion. His starting point was the consumption function. If consumption depended on current income, as shown in figure 13.1— and given the level of net investment—only one level of income was consistent with business not making losses, for only at this level of income would the amount business received from consumers equal the amount they paid out to factors of production. Significantly, the diagram was labeled “Determination of the Level of National Income.” However, although the multiplier could be used to determine the level of income, the acceleration principle was needed to explain fluctuations in the level of income.26

This was one of the points at which the importance of mathematical analysis became clear. If the model was to generate cycles, it was necessary not only to introduce the acceleration principle but also to assume that consumption in any period depended on the previous period's income.c This was something that would have been difficult to establish without the mathematics. Having performed this analysis, though, Samuelson could then sort out issues that Harrod had been unable to settle. For the first time, he defended Keynes against the claims found in American business

c. Adding this lag turned what would otherwise have been a first-order difference equation into a second-order difference equation; a first-order difference equation cannot generate cycles, whereas a second-order one will do so for appropriate parameter values.

Figure 13.1 Income determination—consumption and investment.

Source: Samuelson 1939e, p. 790.

cycle theory: “From the long-run point of view Keynes was partially justified in ignoring the acceleration principle completely. The average level of the system is independent of its operation, depending rather upon the level of investment outlets.”27 However, though he was defending the Keynesian apparatus as relevant for explaining the long-run level of national income, his argument was grounded on a theory of investment that was very different from that found in the General Theory, where the analysis of investment had focused on short-run fluctuations in the stock market. Samuelson’s reference to “investment outlets” as the determinants of investment echoed Hansen, not Keynes.

This diagram (figure 13.ι), known also as “the 45-degree diagram,” is important because it is the first use of what was to become, through Samuelson’s textbook, the standard method of explaining the central argument in Keynesian economics.d Not only was the determination of national income central to Samuelson’s exposition of economics, but it also adorned the book’s cover.e After that, it became synonymous, if not with Keynesian economics then with “simple” Keynesianism, being used almost universally in teaching introductory economics. However, though the diagram clearly

d. See chapter 27 this volume. Note that there are two versions of the diagram. Figure 13.1 illustrates the condition that consumption plus investment equals income (C + I = Y); the other, shown in figure 18.1 later in this volume, illustrates the condition that saving equals investment (S = I), where saving is the difference between income and consumption.

e. See chapter 25 this volume.

drew on the General Theory, it arose naturally in the course of Samuelson’s development and analysis of a theory that Hansen had developed.

The tone of Samuelson’s conclusions was different in this paper. Instead of overtly praising the mathematics for opening up the analysis of more complex models, he pointed out that the assumptions were simplifications, and that “[o]bvious qualifications must be made before the results can be applied to the real world.”28 This reflects the different role played by diagrams in the two papers: in the first paper, a diagram was used to explain a complex situation; in the second paper, the diagram was used to illustrate a fundamental principle.

However, despite this difference, Samuelson remained the mathematical theorist settling disputes. He did not praise the use of mathematics explicitly, but he criticized those who believe that economic problems can be solved by disputes over terminology. It is not definitions of saving and investment but, rather, “the numerical relations of the acceleration principle and the multiplier” that explain the cycle.f For Samuelson, quantifiable relationships were what mattered, and mathematics offered a useful way to analyze them.Samuelson’s continuing engagement with Keynesian ideas through 1939 is illustrated by his review of Gunnar Myrdal’s Monetary Equilibrium (1939) for the American Economic Review.29 The book had been translated from German by two of his friends, Bryce and Stolper. Samuelson showed that he had accepted some ideas from the General Theory when he criticized Myrdal for placing too much emphasis on price changes rather than changes in output and employment, and for not recognizing that monetary equilibrium might occur at high rates of unemployment. Having started from Hansen, Samuelson approved of Myrdal’s more dynamic approach. In particular, he praised Myrdal’s introduction of the terms ex ante and ex post, which were to become standard fare in macroeconomics teaching.g He described the Swedish school as “virile” and he recommended the chapter where Myrdal tackled saving and investment using the concepts ex ante and ex post, thereby clarifying points on which Keynes had been confused. Given that the book had been translated by his friends, that Myrdal had visited the Fiscal Policy Seminar, and that he had heard Samuelson present his paper at the American

f. He illustrated this point with reference to the dispute between Keynes and Dennis Robertson over whether saving and investment were equal.

g. Given the expectations and plans prevailing at the beginning of a period (ex ante), which would not necessarily be consistent with each other, the problem for the economist was to work out how differences between saving and investment were resolved by the end of the period (ex post).

Economic Association meeting, Samuelson would have engaged with Myrdal’s ideas before reading the book for review. He might even have read the German version.

The way in which Samuelson’s work was developing is shown in the manner he expanded the paper that he had presented to the American Economic Association to ready it for publication in the American Economic Review.30 Though his title, “The Theory of Pump-Priming Reexamined,” may have suggested a narrower topic, the paper was wide-ranging. He began by explaining the pre-suppositions underlying his arguments: the economic system was not frictionless, under-utilization of resources was possible, and there might be cumulative movements away from equilibrium. Given the desire to save, full employment required a high level of net investment, and there was no reason to believe that this would be achieved automatically, even with a perfect capital market. Indeed, this was very unlikely.

The amount of net investment must be regarded as dependent on dynamic factors of economic progress such as the amount of as yet undeveloped innovations, trend of population, past net investment, as well as upon the shifting state of confidence and expectations.... This means that in any community there exists a possibility of insufficient net investment, and, perhaps in a wealthy community a likelihood of such an insufficiency.31

Despite citing confidence and expectations, two factors to which Keynes attached importance, this was a non-Keynesian analysis that could have been taken straight from Hansen. Samuelson made it clear that he did not consider Keynes to be his starting point when he included a footnote crediting Keynes with having made a similar point. That is, there was no need to adopt Keynes’s theory of liquidity preference in order to explain why there might be insufficient net investment. His argument was that it was an advantage for there to be investment in capital that did not immediately increase production of consumer goods, applying a similar argument to government spending.

[T]he present emphasis upon self-liquidating public investment may be misplaced. Aside from the fact that it is a poor social economy to saddle overhead charges upon the use of governmental services (as is done in the case of a toll bridge), it may be equally undesirable for government activity to ape the business practices of private enterprise. If the government employs the same calculations with respect to action as a private business, it may soon find itself in the same dilemma as confronts a purely individualistic economy.32

In a footnote to this observation, Samuelson criticized the application of commercial practices such as amortizing deficits over fixed periods or a separate capital budget (an idea supported by Keynes).

The paper was less explicitly critical of Keynes than his earlier presentation, in that the comment on Keynes's theory being a “backward step” was removed, but he still presented the instantaneous multiplier used by Keynes as a special case of a more dynamic model. In writing that the doctrine of the multiplier was “nothing more than a recognition of the strategic importance of investment in determining the level of the national income,”33 Samuelson placed himself squarely in the tradition of American business cycle theory as represented by Clark and Hansen. The need for a more dynamic model was not simply a theoretical nicety, for dynamic multipliers, such as used by Clark, were needed to work out the time for which changes in government spending would affect the time path of national income. This was central to the problem of pump-priming, and to the issue of whether government spending should be increased when the economy began to turn down or when the bottom of the depression had been reached. The argument for the latter was that the downturn produced changes in the structure of prices and costs that were important for the long-run health of the economy.h Samuelson questioned this, arguing that the downturn brought maladjustments of its own that might even be “far worse than those of the boom,” and that he doubted there was much downward flexibility in modern economies.34

This paper is important because, in contrast to his more much more widely cited papers on multiplier-accelerator interaction, most of the claims he made in it were not derived from mathematical models. The multiplier was an inherently mathematical concept and was the basis for the claim that a rise in government spending must necessarily generate a larger government deficit because increased tax revenue would not be sufficient to cover the extra government spending. Mathematical reasoning also lay behind his argument that national income would be maximized if taxation were such as to equalize different households' marginal propensities to consume.35 However, Samuelson's statement that the multiplier was useful “to examine various mechanical aspects of the impact of government expenditures” implied that there were other aspects that could not be analyzed that way.36 He drew upon

h. This was a point associated with Friedrich Hayek, though at the time Sumner Slichter was making it.

the multiplier—accelerator model to take account of changes in investment that would occur in response to changes in other types of spending, but this was a minor point in his argument.

Most of his claims involved arguments that were not derived from mathematical models: he argued against waiting until the bottom of the depression before turning to expansionary fiscal policy on the grounds that it was perverse to let business become bad merely to improve it; and he challenged Hansen's interpretation of the 1935—37 recovery by arguing that Hansen's distinction between recoveries initiated by government spending and ones initiated by private investment did not make sense. Furthermore, when it came to determining the desirable long-term level of government spending, it was necessary to bring in political and ethical judgments. Using fiscal policy to reduce unemployment would raise the deficit, and this might have costs in the long term. His view was, while fiscal expansion to counter depression might have long-term costs, these costs, which were very uncertain, were less important than the benefits that could be obtained. “If the real national income can be increased by five or ten percent over a long period of years only at the cost of incurring a debt of some tens of billions of dollars,” he wrote, “I for one should consider the price not exorbitant.”37

Even by the summer of 1940, Samuelson had not been converted to Keynesianism. He used some Keynesian concepts and accepted ideas that came to be associated with Keynes, but he made it very clear that he considered Keynes to be one of many significant contributors to business cycle theory.[30] His writing gave no hint of the status to which he and others would later elevate Keynes, repeatedly being critical of Keynes for being insufficiently dynamic and for ignoring important factors. He was following Hansen, not Keynes. Samuelson's analysis of what had happened in the early 1930s—that new industries had grown to maturity, requiring no more than replacement investment, and “no new outlets appear on the horizon”—was pure Hansen.38 Even where he challenged Hansen, he added the rider that Hansen's views on long-term stagnation were very interesting. His work with Marion on population growth supported Hansen's views on why the American economy was stagnating.’

Keynes's General Theory had caused excitement in Harvard, and many of the younger generation were converted, but Samuelson's response, like that of his mentor, was not to accept Keynes's claim to be offering a more general theory but, instead, to integrate Keynesian ideas into the existing theory of the business cycle he had learned from Schumpeter, Haberler, and above all, Hansen himself. Consistent with this, the business cycle remained, in a way not true of Keynes, the context in which issues of fiscal policy were addressed. It is possible to discern hints of a changed focus toward income determination as the central problem, but they were no more than hints. Thus, when the thought arose that Samuelson should write a textbook, it is hardly surprising that its subject was to be business cycles.39

In August 1940, still expecting to remain at Harvard for at least another year, he signed a contract with Prentice-Hall to write a textbook for delivery on April i, 1941.40 It was to be co-authored with Erich Roll (1907-2005), who had arrived at Harvard as a visitor in 1939.41 Born in the Austrian Empire, near Czernowitz, the city in modern-day Romania where Schumpeter had his first teaching position, Roll had come to Britain as a student in 1925, in the School of Oil Engineering and the Faculty of Commerce at the University of Birmingham. He was persuaded to stay on to do a PhD on the partnership between Boulton and Watt, two of the pioneers of steam power in eighteenthcentury Britain. Roll obtained a teaching position at the University of Hull, and published two textbooks, one on money and the other on the history of economic thought.

Roll came to the United States in November 1939, on a Rockefeller scholarship. War had broken out in Europe, but he was encouraged to take up his fellowship because the authorities believed it would be useful to have young British scholars at American universities. Most of his time was spent at Harvard and Princeton, with many shorter visits to other universities. During his time at Harvard, Roll and his wife, Freda, were introduced by Svend and Nita Laursen (Svend was another Rockefeller Fellow who had arrived a few months earlier) to Samuelson and Marion, with whom they struck up a close friendship.42 Freda later provided an account of time they spent together on a summer trip to Berkeley, California.

Together with the Samuelsons we sampled the pleasures of the neighbourhood. We sipped through straws exotic drinks in coconut shells at Trader Vic's in Oakland. We often drove over the Oakland Bay Bridge to San Francisco where we were greeted by the most delicious aroma of roasting coffee; we saw Alcatraz, a former penal settlement; we visited the Sally Rand nude ranch where scantily-clad girls lack-a-daisically lobbed ping-pong balls to each other; we ate excellent French meals at a little French restaurant for $1.95 including wine; we went to Chinatown; we gazed in wonder at the Golden Gate Bridge. We also visited Stanford University and lunched with the Haberlers, Machlups and other economists. We then said au revoir sadly to the Samuelsons as they set off for Harvard.43

Their friendship will have been a major factor leading Paul and Erich to decide to commit to writing a book together. Perhaps the opportunity to work together was one justification for their seemingly idyllic stay in California. However, there were good reasons for Samuelson’s choice of co-author. Roll was eight years older, with a decade of teaching experience and two textbooks behind him, on the basis of which he could recommend Prentice-Hall as a publisher. He was also an applied economist: in his time at Princeton he worked on interwar balance-of-payments problems, and he had helped construct the first American index of industrial production.44 At the same time, he was interested in economic theory and in using that to tackle empirical problems. Roll brought to the project skills that were complementary to Samuelson’s.

The book was never completed. After the war, Samuelson wrote to Prentice-Hall to explain that it would never be finished.45 In his letter he blamed their failure to complete the book on the war: they “never properly started” on the book because Roll moved to Washington and after that he moved to MIT; Samuelson had increasingly heavy teaching responsibilities and became involved in government service. Samuelson sought to save face by saying that they would have abandoned the book anyway because, almost immediately after issuing them a contract, Prentice-Hall had published another book, Estey’s Business Cycles (1941), covering much the same ground at the same level of difficulty as their proposed book.46

Given Samuelson’s later remarks, it is useful to see what the Estey book covered and to see the points Roll made when reviewing the book early in 1941. Almost a third of Estey’s book was on data—distinguishing cycles from trends and seasonal fluctuations, the history of cycles including the Great Depression, and measurement problems. This was followed by a review of theories, including a chapter on Keynes’s theories, and a lengthy section (almost 40 percent of the book) on stabilization, covering monetary policy, public works, stabilizing consumption, and policies directed toward wages and prices. Roll praised the book, contending that it was better than previous textbooks, all of which gave an old-fashioned picture of the field.47 His main criticism, apart from the omission of a significant number of important theories, presumably to keep the book simple, was that the book paid insufficient attention to the change that had taken place in business cycle theory since the 1920s. “The most striking feature of recent cycle theory,” he wrote, “is the way in which it has changed its character to become a study of the determinants of the level of economic activity through time.”48 The debates stimulated by Keynes had made it both more important and more possible to link business cycle theory with general economic theory, to the extent that business cycle theory “in the old sense” was rapidly disappearing. Even if Roll had not discussed these ideas with him, Samuelson would surely have read very closely a review by his erstwhile co-author of a book that he believed to be similar to one they were planning to write.

What Samuelson did not tell Prentice-Hall when he wrote about canceling his contract was that he had by then embarked on a textbook for another publisher—one that would take a very different approach to the problem of economic fluctuations. However, in 1940, that was a long way ahead, for he was still a student at Harvard who needed to secure his future. The first stage was writing a thesis, and the second was securing a more permanent and remunerative academic position. Moreover, though war had broken out in Europe, and though the U.S. government was preparing for war, it was not obvious what form American involvement would take and, a fortiori, it was not clear that this would have enormous implications for Samuelson himself.