Consumption and Investment and the Multiplier

The unsettled status of the theory of income determination is illustrated by correspondence Samuelson had with his friend Abram Bergson early in 1942. Bergson was writing a paper in which he analyzed the role of price changes in income determination.24 His method was to argue that, whether companies operated in competitive markets or had monopoly power, it was possible to argue in terms of a function in which price depended on both output and the marginal cost of labor.j Different authors, including Keynes, Hicks, and Pigou, reached different results, Bergson claimed, because they made different assumptions about the responsiveness of price to these two variables.

This required rethinking the theory of saving and investment to take account of price changes that went along with changes in output.While working on this paper, Bergson contacted Samuelson to ask whether stability required that the marginal propensity to save in terms of money had to be greater than the marginal propensity to invest in terms of money (Samuelson's analysis had all been in real terms). This led Samuelson to explain the position he had taken. He justified leaving out price changes “as a first approximation in conditions of deep depression.” The wage rate was given “for institutional reasons,” and it was assumed that prices were proportional to wage rates because of constant returns to scale. These were admittedly “drastic assumptions,” but they were “necessary for the validity

j. This is a simplification, for Bergson allowed for other inputs that might need to be used alongside labor, but it does not affect the argument. of the more rudimentary multiplier models involving wage units, etc.”25 He then went on to explain that the only way to understand how stability conditions would change when a more realistic model was assumed would be to specify a dynamic model.

For example, one might assume that the change in output equaled the difference between saving and investment, both of which depended on real income and other variables. In the published version of the paper, Bergson followed this approach, producing an equation similar to one Samuelson had used in an earlier article, but modified to incorporate the prices of consumption and investment goods.26 A month later he acted as a referee on Bergson's paper, recommending that Dickson Leavens accept it for Econometrica, saying that it was a contribution on a very difficult subject, and suggesting that Bergson be asked to insert the full set of equations from which it was derived, so as to clarify the assumptions on which it was based.27Samuelson made further progress toward providing a systematic treatment of the theory of income determination when, at the end of 1941 or early in 1942, he wrote a long paper, initially titled “Consumption, Investment, and Income” but changed at some point to “The Modern Theory of Income.”28 Its main purpose was expository: to present a simplified version of the modern theory of income determination and to draw conclusions about the relative importance of consumption and investment in stimulating output. However, when the argument moved into dynamics, the exposition became much less simple. The paper shows the direction in which Samuelson was taking Keynesian theory, and it shows him writing about fellow economists in what was to become a characteristic style. He resorted to irony in discussing the work of his contemporaries.

While wise economists have undoubtedly always been in perfect agreement as to what constitutes the correct theory of output as a whole, just what that theory is, until recently, no wise economist would ever tell. But in the last half-dozen years [since 1936, when Keynes's General Theory was published] the secret has slipped out, although its full implications are only gradually becoming familiar.29

Though the effects of the secrets having slipped out had generally been salutary, an unfortunate effect of recent developments had, Samuelson claimed, been “the glorification of the expansionary stimulus of real investment as compared to consumption.” His aim, therefore, was to correct the misunderstandings that lay behind this view.

Irony was even more evident in a footnote discussing economists at the University of Cambridge (UK), with which Keynes was associated. He saw the lack of continuity between Keynes's two major books as “worthy of a doctor's dissertation” and that clues to when ideas in Cambridge (UK) changed were to be found in articles by Joan Robinson, “who holds among other offices that of public relations expert between the ‘Cambridge school' and the rest of the world.”30Samuelson wrote explicitly in terms of different schools of thought— classical, neoclassical (and even neo-neoclassical), and Keynesian. Though he clearly approved of Keynes's main arguments, he did not identify with any single school, implying he stood above them all. His tone was that of someone who understood the mathematics and was able to point out error by virtue of getting the mathematics right, something other economists had not managed to do. Thus at one point he remarked, “I should like to make it clear that I am not accusing any one school of thought, such as the antiKeynesians, of being more confused than their opponents. The Keynesians too have sinned, including the Master.” In a footnote to this passage, he pointed out errors in four “mathematical versions of the Keynesian system some of which have received the apostolic benediction.”31 He patronizingly accused Robinson of being confused and having “corrupted” the Polish economist Michal Kalecki.k

An illustration of the importance of understanding the mathematics occurred in the opening section in which he explained that one reason economists believed investment to be the driving force was that the output of investment goods industries, such as pig iron, was known to fluctuate much more than the output in consumption goods industries. Because fluctuations in investment seemed to come before changes in consumption, it had been assumed that causation must run from investment to consumption. Against this, Samuelson, drawing on his mathematical experience, could easily see that if investment was compared with changes in consumption (as implied by the accelerator), the timing was reversed, immediately undermining any presumption about causality.

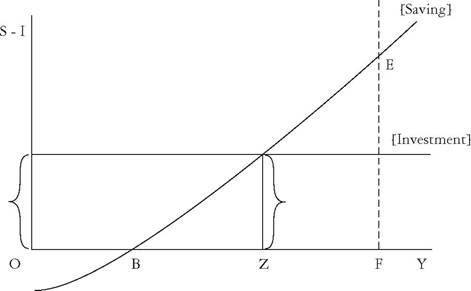

The paper is also significant for being the first place where Samuelson used the diagram that was later to adorn not only the pages of his bestselling introductory textbook but also its cover; it showed the level of income as being determined by the intersection of an upward sloping saving function with a horizontal investment function. This diagram, figure 18.1, was a variation on the diagram he and Hansen had

k. Kalecki, who had left Poland for Cambridge, had developed a theory that had much in common with that of Keynes, but with Marxist elements. Robinson was, in 1942, discovering Marx.

Figure i8.i Income determination—saving and investment.

previously used (figure 13.1), but instead of plotting consumption against income, he plotted the difference between them (saving) against income? Equilibrium output is Z, at which ex ante (planned) saving and investment are equal (he was using what was coming to be the accepted terminology, despite his own preference for the term “virtual saving”).32 If Z is less than full-employment output, F, then F cannot be an equilibrium. Samuelson claimed that, though this account of income determination was oversimplified, it was based on “firm empirical patterns which every theory must take into account”—notably the stability and broad shape of the consumption function that he had estimated in his previous work— and it was sufficient to correct misunderstandings.33 He compared his diagram with the Marshallian “cross,” the well-known supply and demand diagram, using Marshall’s analogy of the two blades of a pair of scissors to explain that it was neither saving nor investment but the relationship between them that determined income. The diagram therefore came to be known as “the Keynesian cross.”

However, while such diagrams could do much to explicate the relation between saving and investment, they needed to be used in conjunction with other arguments, for a crucial role was played by the rate of interest, which brought in the money supply and central bank policy.

More complicated was the role of time. One of the additions made to the earliest draft was an eight- page section on the dynamics behind these static diagrams. This requiredl. If saving is defined as the difference between income and consumption, the gap between expenditure (consumption plus investment) and income must be identical to the gap between investment and saving.

that Samuelson make assumptions about the lags involved. One possibility was to assume that current consumption depends on income in the previous period. Another was to assume that it takes time for production to respond to changes in sales, with any difference between the two being met from inventories. The relationship between saving and investment out of equilibrium would be different in each case. It was here that he made the remark, cited earlier, that both Keynesians and anti-Keynesians had made mistakes in equal measure.

Samuelson argued that it was optimal to have a propensity to consume that was sufficiently high to produce full employment, for if there were unemployment, consumption and investment could both increase. However, once full employment was reached, consumption and investment became competitive, which meant that “optimal behavior then involves deliberate social decision and cannot be decided upon mechanical behavioristic grounds.”34 Probably, he argued, “societies desire neither the largest possible rate of capital accumulation per unit time nor the smallest.” The paper ended with a review of what Samuelson called the “under-consumptionist school,” going back to Malthus, which had argued that unemployment could result from the level of consumption being too low.m They had consistently been dismissed, even by writers such as Hansen, and yet modern thought was, Samuelson noted, moving in their direction. How was this possible?

His answer was that the analysis of effective demand was “one of the most difficult problems of economic analysis,” to which advances in value theory (the theory of how individual prices are determined) could contribute little.35 Whereas the theory of value was well developed and could be reduced to a few basic principles (as he had shown in his thesis), he contended that “It would be too much to expect...

that any one writer should have developed a beautiful, logical, and complete theory [of effective demand].” Quoting Keynes's General Theory, he observed that “the underconsumptionists ‘saw truth obscurely,' and they often combined with it naive, cranky, and refutable points of analysis.”36 He was no doubtm. It was widely held, at least since the time of Adam Smith, that saving (refraining from consumption) was beneficial. High saving would lower interest rates, raise investment, and stimulate economic growth. Malthus argued that there was an optimal propensity to consume (conceptually equivalent to assuming an optimal propensity to save) because, after a certain point, saving was harmful because spending would be insufficient to buy all the goods that could be produced. The result would be unemployment. This idea, the basis for under-consumptionism, was considered heretical, for it challenged the idea that saving was always a virtue.

addressing his teachers when he claimed that such errors were not a reason for rejecting the theory.n

The concluding message of the paper was that, though differences over economic policy were real, there was great agreement on economic analysis. His remark that “[i]t is particularly important to emphasize the great consensus of analysis which has been reached by almost all present day economists” implicitly gave authority to his own arguments, in a paper in which he had found fault with the writings of his many of his most eminent contemporaries.37

One of Samuelson’s main targets in this paper—certainly if judged by the number of pages devoted to it—was an article in which Oskar Lange (1938) had taken up the idea, made in the early nineteenth century by Malthus, that there was an “optimum” propensity to consume. This idea was important because it challenged an orthodoxy that was deeply entrenched in economic thinking. Using a model similar to Samuelson’s, but also having an equation in which supply and demand for money determined the rate of interest, and in which the rate of interest affected investment, Lange had shown that there would be some propensity to consume at which investment was maximized. If consumption were lower than this, the rate of interest would be lowered and investment would rise; if consumption were higher, the rate of interest would rise, thereby lowering investment. This vindicated, so Lange claimed, the under-consumptionists, who claimed that an economy could be held back by a lack of consumption, thereby contradicting the orthodoxy according to which saving was always beneficial. However, Samuelson believed his argument to be mistaken on several counts, and that Lange’s claim that there might be an optimal propensity to consume that resulted in less than full employment was completely wrong.

Samuelson had corresponded with Lange about his earlier work on consumer and welfare economics, and naturally sent Lange a copy of this paper. Lange replied that he had read it with great interest.38 He offered many suggestions for improving the paper, as he had done on a previous occasion when Samuelson had criticized him and he had conceded that Samuelson was right to find fault with his algebra, but he claimed that Samuelson’s own algebra was not right either, and that if the mistakes were corrected, his own conclusions were justified. Lange said he was “inclined to be more charitable

n. He criticized Slichter, whose textbook he had used as an undergraduate (see chapter 3 this volume), and Williams, who had taught him money and banking at Harvard, and ran the Fiscal Policy Seminar with Hansen (see chapter 12 this volume) for objecting to under-consumption on grounds that were merely verbal. to the neo-classical theory than I was before or than you appear to be.” His reason was that neoclassical writers assumed all prices were completely flexible, which meant that if the propensity to consume fell, prices as well as output would fall, reducing the demand for money. Moreover, if people did find themselves with excess cash balances, this would have a direct effect on both demand for durable consumption goods and investment.o The theory presumed that the supply of money did not fall as fast as demand, which would certainly be true if, as did most neoclassical economists, the money supply were assumed constant. Lange concluded by saying that in a month's time he hoped to have the draft of a booklet, “Price Flexibility, Employment and Economic Stability,” that would explain the neoclassical theory. Aside from a footnote, the notion of the “optimum” propensity to consume did not appear. Lange said that he might send it to Samuelson if he was not too busy.

Not surprisingly, Samuelson found this letter helpful. He wrote Lange that he was particularly grateful for spotting his mathematical error, for “it would have been embarrassing for this to have occurred in print,” implying that Lange should be embarrassed about his own mistake.39 He went on to say that, on rereading, he had come to realize that his wording had not made sufficiently clear the complete generality of Lange's case. He had implicitly taken Lange to be talking about a world in which there was unemployment. In such a world, wages may be taken as constant. It was only as full employment was approached that wages would rise. In contrast, he presumed that Lange had intended to encompass the full-employment case in his equations.

Samuelson then explained why he was not convinced by Lange's argument about real cash balances. This effect presumed imperfect capital markets, for in a perfect capital market, in which companies could borrow and lend unlimited amounts at the market rate of interest, cash balances should not matter. However, though he accepted that capital markets were imperfect, he thought that the effects Lange discussed would be “completely overshadowed” by the effects of a falling price level on the marginal efficiency of capital.

Under realistic conditions, therefore, I think that the neo-classical position is utterly fallacious, despite the fact that it is possible to construct models in which the curves do not have the flatnesses and steepnesses of the real world and in which wage reductions would temporarily increase employment.40

o. The investment function would take the form I = F(i, C, M), where i is the rate of interest, C is consumption, and M is cash balances.

He then made his objections to the neoclassical theory clear, explaining why he hoped that the manuscript Lange had promised him would not compromise on the crucial questions.

In contrast to this for our world, the armament period included, a real thorough-going application of their [the neo-classical economists’] plans would lead to the introduction of hyper-deflation with disastrous consequences to our economic and political system. I shall be very sorry, therefore, if in your monograph you give way on these points. The optimum propensity to consume should occupy much more than a footnote.41

In a postscript to his letter, Samuelson explained that though he was not anxious to publish his paper quickly, Hansen wanted him to get it out as soon as possible, suggesting that this would be easier if it were divided into two parts. To avoid this, he wondered whether Lange thought that the Journal of Political Economy might be willing to take it at its current length. However, the paper was submitted, unfinished, to the American Economic Review, asking for advice on what was needed to make it publishable. The editor wrote that he would be happy to accept it when Samuelson was satisfied it was ready for publication, though without waiving his “editorial prerogative to suggest improvements.”42 However, he confirmed Samuelson’s view that he should take plenty of time to revise the paper thoroughly.

If I were you, I should not be in too great a hurry with it. In other words, the manuscript will bear careful reworking. In particular, I suggest you try to put your positive analysis into a more orderly relation to your commentary on Hansen and Lange. The two strands get a little in each other’s way. Could some of the critical comment be reduced to footnotes? In the last section you devote too much space to commenting on Slichter and not enough to bringing your paper to a good end.43

The letter ended with an invitation to lunch when Samuelson was next in Washington. However, despite everyone Samuelson consulted thinking the paper was sufficiently important to publish, it was never published, and the ideas were to come out in other ways. The explanation is no doubt that Samuelson was becoming increasingly busy with teaching in MIT and with fortnightly visits to Washington.p

p. See chapter 19 this volume.