MichalKalecki

7.3.1. The level of income and its distribution

Michal Kalecki (1899-1970) is considered by many as a minor Keynesian and a popularizer of the Keynesian revolution. Sometimes he is recognized as being a forerunner, but not much more.

On the contrary, his work is important for the history of modern economic thought, not only because he was the first to formulate the theory of effective demand, nor so much for the fact that the Kaleckian version of that theory was more realistic than the Keynesian one, but because of the centrality Kalecki assigned to the problem of the distribution of income and to the non-competitive context in which he assumed prices to be determined. His work is important, above all, because Kalecki, given his non-academic origin and his Marxist background, was almost completely immune to those doctrinal restraints that on more than one occasion had confused Keynes’s thought. And it has been quite rightly pointed out that, precisely for this reason, Kalecki was more Keynesian than Keynes himself. So much so that, after the Second World War, some of Keynes’s most coherent Cambridge followers, in the attempt to purify their master’s work of every anti-Keynesian residue, did nothing but develop a Kaleckian version of the theory of effective demand and construct a theoretical system that could be defined as neo-Kaleckian.We find the first formulation of the principle of effective demand in a paper published in Warsaw in 1933 entitled ‘Proba teorji Konjunktury', and later published in a shorter version in Econometrica (1935), entitled ‘A Macroeconomic Theory of Business Cycle’. In the following five years, various articles came out which were collected together in 1939 in a book entitled Essays in the Theory of Economic Fluctuations. Other papers and anthologies were published in the following years. Here we will limit ourselves to the Selected Essays on the Dynamics of the Capitalist Economy 1933-1970, published in 1971, a collection of the best of Kalecki’s scientific work.

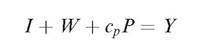

To explain Kalecki’s theory of effective demand in the simplest way, we will begin with an equation which defines the national income as the sum of consumption and investment, Y = C +1. We will separate the workers’ consumption from that of the capitalists. The former, under the assumption that the workers’ propensity to consume is equal to 1, coincides with the wage bill, W. The latter is equal to cpP, where cp is the capitalists’ propensity to consume and P is the level of profits. Then:

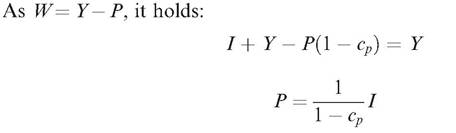

The last equation incorporates the Kaleckian version of the theorem of the ‘widow’s cruse’: ‘the capitalists may decide to consume and invest more in a given period than in the preceding one, but they cannot decide to earn more. It is, therefore, their investment and consumption decisions which determine profits, and not vice versa’ (pp. 78-9). In this way profits are determined by investment decisions through a process similar to the Keynesian multiplier. In the Kaleckian version, however, the role played by the multiplier in the creation of the savings necessary to finance investments is even more clear. Since, in this model, only the capitalists save, the increase in profits generated by a given increase in investments will continue up to the point at which all the necessary funds have been created to repay the debts with which those investments were financed.

The problem now is: which level of income and employment is generated by given investment decisions? After a not very convincing first attempt, based on the hypothesis that the rate of profit, the profit margin, and the level of utilization of productive capacity vary in the same direction, Kalecki finally managed to solve the problem by making use of ‘Bowley’s Law’—an empirical law, discovered in 1937, according to which the wage share in the national income is constant through time.

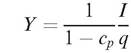

In this case also we will simplify as much as possible. If q = P/Y is the profit share, then we can transform the profit equation in the following way:

Given the investment level and the profit share, the lower the propensity to save of the capitalists the higher the income necessary to supply the savings required to finance investments.

One final problem remains: the determination of the profit share. Kalecki assumed three hypotheses to solve this problem:

(1) Perfect competition does not exist.

(2) Average variable costs of the firms are constant up to the point of full utilization of the plant and/or full employment.

(3) Prices are set by the firms in relation to the average variable costs and the average price prevailing in the industry in which they operate.

The basic idea is this: because of phenomena such as industrial concentration, vertical integration, productive diversification, and oligopolistic co-ordination of the markets, modern large-scale firms possess a discretionary market power; and they use this power to fix prices. Therefore, neither variations in demand nor conditions of scarcity play an important role in explaining the movements of prices of manufactured goods. From this point of view, prices depend on variable costs, especially on the cost of labour, and on the ‘degree of monopoly’ existing in the various industries. The intersectoral diversity of the degrees of monopoly is due to the diverse degrees of industrial concentration prevailing in the various productive sectors, while the degree of monopoly in force in each sector depends on the distribution of market power among the firms of the sector.

Thus, given the degree of monopoly of the various firms, their cost curves, and their relative contributions to the output of the industry, the average profit margin of the industry depends on the average degree of monopoly and does not vary with changes in the level of output.

This reasoning can be extended to the whole economy (which, for simplicity, we assume closed). Given the average profit margin of the whole economy, the profit—wage ratio is known. An increase in investment raises aggregate demand. If there is not full employment or full utilization of plant, the firms can satisfy the increased demand by expanding production without modifying prices. Therefore, the level of income can increase with no changes in income distribution. This depends on the structure of the markets. The lower the competition, the higher, on average, are the prices with respect to variable costs, and the higher are the profits with respect to wages. Later Kalecki reinterpreted the ‘degree of monopoly’ in such a way as to take into account class conflict and, in particular, the role played by wage bargaining in the determination of the distribution of income. In this way the theory became more realistic, but its analytical structure remained basically the same.7.3.2. The trade cycle

Unlike Keynes, Kalecki used the principle of effective demand, not within a theory of the level of output, but within a theory of the business cycle. Once he had determined the output level starting from the level of investment decisions, Keynes had accomplished his task, but Kalecki’s had only just begun, as he had to solve the problem of determining the level of investments. The problem of the business cycle is that of explaining fluctuations in the level of investments.

Kalecki believed that investments depend on profit expectations and the interest rate. The latter affects investment in that it represents the cost of finance. However, in all analytical formulations of the investment function Kalecki ignored the interest rate—a simplification justified by a particular theory of the term structure of the interest rate and its changes. This theory seems to be based on a mixture of Marxian and Fisherian doctrines, even if Kalecki mentioned neither Marx nor Fisher in regard to this matter.

The short-run interest rate varies pro-cyclically, as it is drawn along by real profitability. Therefore, if the profit expectations depend on the current rate of profit and the variations of the latter are stronger than the variations in the interest rate, the influence of the cost of finance on investment can be ignored, at least to the degree to which the investments are financed by shortrun credit. This is Marx pure and simple. If instead investments are financed by the issue of long-run liabilities, the long-run interest rate must be taken into account. However, according to a theory already put forward by Fisher, the long-run interest rate is no more than an average of the expected shortterm rates within the time of maturity of the loan. Therefore, the variations in the long-run rate are always smaller than those of the short-term rates; and, to the extent to which investments are financed with long-term debt, the influence of the variations of the cost of finance can be ignored even more legitimately.A problem does arise here, however: if there is a permanent gap between the rate of profit and the interest rate, what prevents investments from growing indefinitely? Keynes’s solution to this problem consisted of the assumption of a decreasing marginal efficiency of capital, an assumption basically justified by the hypothesis of increasing costs in the capital-goods industry. Kalecki rejected this explanation, substituting one based on the hypothesis of ‘increasing risk’—a hypothesis for which he drew inspiration from work by Marek Breit, a Polish economist with whom he had collaborated in Warsaw. This hypothesis implies that the risk of bankruptcy increases with the ratio of investments to total wealth and with the ratio of debt to investment.

In one of the first versions of his model of the business cycle, Kalecki made investments depend on the national income (considered as a proxy for the amount of profits) and on the existing capital stock. The level of investments is an increasing function of national income and a decreasing function of capital stock.

This is nothing more than a special version of the principle of adjustment of the capital stock. The cyclical movement of investments is explained by coupling this principle with some hypotheses relating to the structure of time lags. An increase in investments raises the capital stock; this at a certain point will be judged too high to justify a further increase in investments, which then begin to decrease; when the capital stock is again considered too low, the cycle starts again. A similar model, but one applied to shipyard production, was formulated by J. Tinbergen in an article of 1913. It is worth mentioning this, as Kalecki drew some inspiration from this work.In a later version of his model Kalecki modified the investment function, making it depend not only on the level of income (by means of the savings function) but also on its variations and on the variations of capital stock. The new model turned out to be a generalization of the old, as well as of various other models of the multiplier-accelerator type.

It seems that, from the beginning of the 1940s, Kalecki grew increasingly dissatisfied with this kind of model, even though he continued to work on them until the 1950s. In fact, in a 1943 article on the political business cycle he took a completely different direction, opening a new research field that proved to be much more promising than that of the mechanistic models of the multiplier-accelerator type. The article in question is ‘Political Aspects of Full Employment’, published in the Political Quarterly and then republished in the Selected Essays. In it Kalecki focused his attention on the possibility of stimulating an increase in output by means of public spending. However, he argued, such a policy would meet with opposition from ‘business leaders’. This opposition could be explained both by ideological factors and by more specific political-economic factors. The point is that the maintenance of full employment would bolster workers’ self assurance, reawaken their class consciousness, weaken the disciplinary function of the fear of unemployment, stimulate strike activity, undermine the authority of the factory bosses, and, in the final analysis, could cause social and political changes judged dangerous by the dominant classes.

Class conflict encouraged by full employment would not necessarily cause a reduction in profits, given the ability of firms to immediately transfer the cost increases onto prices. ‘But “discipline in the factories’’ and ‘‘political stability’’ are more appreciated by the business leaders than profits. Their class instinct tells them that lasting full employment is unsound from their point of view and that unemployment is an integral part of the normal capitalist system’ (p. 141). Thus, sooner or later the government would be forced to abandon full employment policies. The consequent depression would, however, induce the resumption of expansionist policies and the cycle would begin again.

7.3.