John Maynard Keynes

7.2.1. English debates on economic policy

During the inter-war period, as had already occurred about a century before at the time of Ricardo and Malthus, England became once again an experimental laboratory for economic theory.

In this particular time and in this particular place, the interaction between theory and practical problems was uniquely strong. The public debate on economic policy concerned two principal issues: the return to the Gold Standard, and the problem of unemployment.By around 1875 the Gold Standard had been pretty well accepted by all the main capitalist countries; and it continued to rule until the First World War. The war destroyed the system, but immediately afterwards there were attempts to rebuild it, especially in England, where strong efforts were made to restore sterling to its pre-war parity. From 1920 to 1925, when the English authorities were still working on preparations for the return to the Gold Standard, prices in that country fell by 40 per cent. In 1925 sterling was again linked to the pre-war gold parity, but the system only lasted six years. English prices were still too high and the export industries too weak. Meanwhile the United States and France were experiencing strong surpluses on their balance of payments. The United States masked them with a policy of long-run foreign loans, whereas France accumulated gold and sterling reserves. The final blow to the English Gold Standard came immediately after the 1929 crash. American loans dried up, while the Bank of France decided to convert its sterling reserves into gold. Then, in 1931, a wave of panic, caused by the collapse of the ‘Credit Anstalt', spread throughout Europe. When several countries began to convert sterling reserves into gold, the Bank of England was unable to resist and the Gold Standard was abandoned. The 1930s were years of international monetary chaos, with competitive devaluations, protectionist trade policies, and deflationary monetary policies.

The main problem with the Gold Standard was that the ‘automatic' adjustment processes it is assumed to entail require price flexibility, otherwise the price-specie-flow mechanism does not work. But by the last quarter of the nineteenth century, prices and wages had already become fairly rigid; and, in fact, the adjustments, effected by careful interest rate manoeuvres, mainly acted on capital movements. They also led, however, to deflationary processes which affected production, the levels of real output, and employment.

In theory, the adjustment should be made in the following way: a deficit in the balance of payments would cause an outflow of gold and a reduction in gold reserves. The domestic money supply would therefore diminish. This would lead to a reduction in the level of prices and a consequent increase in the competitiveness of national goods. Exports would grow, imports would decrease, the balance of trade would improve and the external deficit would be eliminated. This automatic adjustment can be accelerated by manoeuvring interest rates. The central bank raises the rate as soon as it ascertains the existence of a deficit in the balance of payments. In this way, it stimulates the inflow of capital from abroad and deters the outflow of internal capital. The ensuing improvement in the surplus (or reduction in the deficit) of the capital movement account would contribute to reduce the overall deficit.

However, if prices and wages are rigid, the adjustment does not work this way. When the supply of domestic money is reduced following an outflow of gold, the aggregate demand for goods declines. Since prices do not diminish, the quantities produced will be reduced. Real deflation will hit employment and the wage bill. As a consequence, consumption will be reduced. Imports of consumer and intermediate goods will fall and the balance of payments will improve. If the monetary authorities then raise the interest rate, they will succeed in accelerating the adjustment, chiefly because they exacerbate the recession, by discouraging investments.

This kind of adjustment had become socially intolerable and politically dangerous, given the rates of unemployment experienced in all capitalist countries in the inter-war years. In England, for example, in the 1920s unemployment averaged 10 per cent and reached 22 per cent in 1931. In the United States it even touched 27 per cent in 1933.What could be done? Nothing at all, maintained the British Government. The line prevailing in government circles was derived from that liberal orthodoxy which preached the necessity of balancing State accounts by spending as little as possible and, for the rest, laissez-faire the private economy. Trying to alleviate unemployment by public works would only cause trouble. The main argument of the Treasury was that, as public expenditure had in any case to be financed from private sources, by taxation or debt, it subtracted capital from private enterprise and therefore reduced employment in the private sector by the same amount as it raised that provided by the State. This is the famous ‘Treasury view’. It was put into practice by the Treasury in the second half of the 1920s and presented in Parliament by Churchill in 1929. But as early as 1913 it had received scientific backing from Hawtrey, who, in Good and Bad Trade, had put forward the argument according to which ‘the government by the very fact of borrowing for [public] expenditure is withdrawing from the investment market savings which would otherwise be applied to the creation of capital’ (p. 260). Most of the economists, though, were against this view. Robertson criticized Hawtrey’s arguments in 1915. Pigou had already criticized a view similar to that of the Treasury as early as 1908. The problem was: how was it possible to demonstrate scientifically that the Treasury view was mistaken? We do not believe we are exaggerating when we say that this was one of the main subjects of the economic-policy debate from which the Keynesian revolution arose.

Before considering Keynes, however, it is necessary to return to the theories of the business cycle, so as to show the climate and tenor of the scientific debate from which the General Theory finally emerged.

Let us, for a moment, accept Hawtrey’s version of the Treasury view: the government cannot increase the level of employment if it finances the additional expenditure by taxation and/or public debt. This, however, still leaves open the possibility of financing the deficit with a monetary expansion. Nothing more dangerous, argued Hawtrey. On the contrary, it is precisely in this way that the economic fluctuations responsible for unemployment would be amplified. An expansion in bank credit increases expenditure, aggregate demand, and incomes, fuelling inflation, profit expectations, and investment activity. In this way expectations become self-fulfilling and the economic boom proceeds at a sustained pace, but the demand for credit (for money in general) increases beyond the capacity of the financial sector. When the bank reserves fall ‘too’ much, the banks increase the interest rate and reduce the supply of money. The ensuing contraction of expenditure is further amplified by the wholesaler’s policy of reducing their inventories, as they work on a high debt/ turnover ratio and are therefore severely hit by increases in the interest rate. The monetary contraction does not immediately or completely lead to a reduction in prices, as these are sticky. Wages are also rigid. Therefore the deflation leads to a reduction in the level of output.Hawtrey’s is a ‘purely monetary’ theory of economic fluctuations; however, the hypothesis concerning price and wage rigidity plays an essential role in accounting for the process of the transmission of the monetary impulses to the real variables. Notice that it was precisely to this hypothesis that, some years later, attempts were made to reduce the Keynesian ‘special case’. Keynes, however, was a critic of this theoretical approach. We will limit ourselves to noting this strange fact but will return to it in more detail later on.

In the 1920s, Hawtrey found himself somewhat isolated in English academic circles. In the 1930s, however, Robbins and Hayek arrived to give him a hand.

Of particular importance were two works by Friederich August von Hayek of 1929 and 1931. Hayek’s cycle theory endeavoured to blend a monetary theory of fluctuations similar to that of Hawtrey with Bohm- Bawerk’s theory of capital and Wicksell’s theory of the cumulative process. A credit expansion initially produces two effects: it lowers the interest rate and creates forced savings, increasing the purchasing power in the hands of the investors to the detriment of that available to consumers. With investment, the prices of capital goods increase too and, therefore, their production rises. Thus the length of the production period and the capital intensity of the system increase. In phases of monetary contraction the opposite processes occur, so that the labour force must be dislocated from one sector to the other. In fact, deflation reduces the period of production, increasing consumption and reducing investment.This transformation process, however, requires time, as capital goods cannot actually be transferred from one sector to another but must be substituted by new capital goods. During this technical substitution process, temporary unemployment is created.

On the opposing theoretical front to that of Hawtrey and Hayek were Robertson, Pigou, and Keynes. Denis Holme Robertson emphasized the real factors of the economic fluctuations, by combining an over-investment theory with a theory of the effects of technological innovations similar to that of Schumpeter. Successively he concentrated instead on the monetary aspects of the cycle, supporting the theory of forced savings. One important argument, which differentiates Robertson’s theory from those of Hawtrey and Hayek, concerns the definition of the role of the banking system. Robertson argued that, besides its traditional objective of price stability, the financial sector, given its ability to influence the level of investments by means of forced savings, should also be governed with the aim of guaranteeing the level of desired savings.

Pigou was another fervent critic of the Treasury view. From his vast and complex theory it is worth underlining three elements above all. First is the argument that variations in the level of employment are generated by variations in the aggregate demand and, in particular, by variations in investment, by means of a propagation process based on the multiplier, even if the multiplier principle is not formally expressed. Second is the typically post- Marshallian, or rather pre-Keynesian, argument that fluctuations of investments basically depend on the profit expectations of the entrepreneur.

Finally, it is important to recall that, according to Pigou, the possibility of increasing the level of employment depends on the occurrence of two institutional conditions: high elasticity of the credit supply and high flexibility of prices and wages.

7.2.2. How Keynes became Keynesian

In regard to the two fundamental problems of English economic policy of the 1920s and the 1930s, the Gold Standard and unemployment, Keynes took up a precise position right from the mid-1920s, and there is no doubt that, to a large degree, his theoretical work in the following years was motivated by the need to give scientific respectability to his political stances. Keynes began to oppose a return to the Gold Standard as early as 1923, when, in the Tract on Monetary Reform, he pointed out the deflationary danger inherent in the return to gold. Two years later, when the Gold Standard had been re-established, Keynes argued that the pound was still too overvalued with respect to the dollar, and that consequently a return to the Gold Standard, in the presence of rigid wages, would have required adjustments in levels of production which would have been very damaging to the English export industries. In regard to the problem of unemployment, Keynes was a supporter of public investment programmes, at least from 1924 onwards, when, in the article ‘Does Unemployment need a Drastic Remedy?’, he backed the programme of employment put forward by Lloyd George and the Liberal Party. The philosophy underpinning his political attitude was put forward in The End of Laissez Faire (1926), in which he argued the necessity of abandoning rigid free-trade orthodoxy, whose economic effects he feared just as much as ‘State socialism’.

Keynes observed that there are spheres of activity in which private initiative carries out an essential economic role and in which the State should not interfere, while there are also spheres of activity in which the State operates in a better way than the private sector. He did not go very far forward in identifying the latter types of economic activity, which, basically he reduced to two: credit control and the regulation of the process of formation and allocation of savings. He put forward the idea that the State should take on the role of ‘concerted and deliberate management’ of the economy, albeit by means of a limited number of political instruments.

Such an emphasis on public management was also motivated by the fact that the Gold Standard, against which, realistically, he no longer fought after its re-establishment, created additional problems of stability for the national economy, problems that, he argued, could be resolved by a prudent macroeconomic policy. This view might seem paradoxical, if one considers the fact that the Gold Standard was supported by liberal thinkers precisely for its supposed ability to produce automatic adjustments. However, Keynes considered the basic political and philosophical problem to be different: are these ‘automatic’ adjustments, given their effects on unemployment, not worse than the illness they wish to cure?

The crucial years for the maturation of Keynes’s thought were those immediately after the publication of A Treatise on Money (1930). In 1931 the Macmillan Report came out, the product of a Commission on Finance and Industry of which Keynes was a member. The report supported a philosophy of economic policy similar to the one put forward in The End of Laissez Faire. Furthermore, it proposed a reflationary monetary policy that seemed to have been inspired by the theory advanced by Keynes in the Treatise. The basic idea was that monetary expansion would stimulate profits and investments, thus pushing the economy out of the troughs of depression.

In the Treatise on Money Keynes had reached this theoretical conclusion by means of a rather complicated and extremely ambitious model with which he tried to integrate the results of two streams of research: on the one hand, the neoclassical theories of the cycle as a phenomenon of monetary disequilibrium, in particular Marshall’s and, above all, Wicksell’s theories; on the other, the theories of the production/expenditure disequilibrium which had been formulated in the heterodox ‘underworlds’ of Tugan-Baranovskij, Hobson, etc.

From the latter type of model Keynes took the idea of disaggregation in two productive sectors, consumer goods and investment goods, and, above all, the idea of studying the dynamics of the economy as a disequilibrium phenomenon. As investment decisions are not savings decisions, nor decisions to produce investment goods, the investment share in the aggregate expenditure may be higher than the share of investment goods. In a disequilibrium situation such as this, the prices of investment goods will rise over and above the costs (inclusive of normal profits). Thus (extraordinary) profits will increase. If this rise in profits fuels the confidence of the capitalists, they will increase both their consumption and investment expenditure. Thus the expansive stimulus is self-sustaining; on the one hand it spreads from the capital-goods sector to the whole economy, on the other it produces the strange and miraculous effect of the ‘widow’s cruse’: as the expenditure of each agent is the profit of another, the higher the aggregate expenditure of the capitalists, the higher their earnings will be.

The Marshallian element of the model resides in the theory of money demand, which Keynes, by using the Cambridge equation, formulated in terms of the quantity of liquid assets the public wishes to hold. Developing an argument of Robertson, however, he took a step forward, by distinguishing between a demand for cash deposits motivated by the needs of transactions and a demand for saving deposits dependent on psychological factors such as the state of confidence and the level of bearishness of the public. The bank interest rate depends on the forces of supply and demand for money. At this point Wicksell’s cumulative process enters the scene. The monetary authorities can lower the interest rate. In this way they will encourage investment and cause both prices and profits to rise, which, in turn, will make the entrepreneurs more confident and lead them to increase production. Here is the gist of the monetary management policy Keynes supported in the 1920s. The authorities should not be concerned solely with price stability, but also, and above all, with the creation of savings and investments. The treatise was heavily criticized. Here we will limit ourselves to outlining the most important criticism, the one raised both by Hawtrey and by the members of the circle of young Cambridge economists who met periodically to discuss Keynes’s theories, especially Kahn. Basically this criticism refers to the fact that the ‘fundamental equations’ by means of which Keynes formulated his model are only valid under the hypothesis of full employment; thus the implications in regard to the ability of the cumulative process and the monetary policy to reflate the economy in real terms were a non sequitur. It was a simple and devastating criticism. Keynes felt the punch and, undoubtedly, this was the beginning of the theoretical travail which was to lead him to publish, six years later, The General Theory.

The rethinking process, however, had begun as early as 1931. For example, while the Macmillan Report adopted the theories Keynes had put forward in The End of Laissez Faire and in the Treatise, a minority of the commission, including Keynes himself, were sceptical about the possibility of curing unemployment with monetary policy. Furthermore, and still in 1931, Keynes gave some Harris Lectures in Chicago in which, for the first time, he tackled the problem of unemployment in terms of the equilibrium level of production determined by a given level of investment. In so doing he admitted, even if only in passing, that an unemployment situation can be an equilibrium.

7.2.3. The General Theory: effective demand and employment

The decisive theoretical leap with which Keynes achieved his revolution consisted in the abandonment of the disequilibrium analysis typical of the Treatise and the adoption of a macroeconomic-equilibrium approach. In order to understand this change it is necessary to begin with Say’s Law. Most pre-Keynesian critics had rejected this law because of its implications for the equilibrium between production and expenditure. A criticism of this type underlies all those savings-investment disequilibrium models which were to culminate in the ‘fundamental equations’ of the Treatise. In The General Theory of Employment Interest and Money (1936), Keynes criticized Say’s Law for a different reason from the traditional one—for its implications in regard to the direction of the causal link connecting production and expenditure. In contrast with Say’s law, Keynes argued that it is not production which generates expenditure and demand, but the expenditure decisions which generate demand; then production adjusts to demand. This argument has three important theoretical implications. The first is that there is no longer any reason to waste time analysing the disequilibrium dynamic processes by which production adjusts to demand; it is sufficient to assume they are rapid so as to be able to take them for granted; then the analysis becomes an equilibrium analysis. The second is that it is no longer necessary to focus on the dynamics of the inter-sectoral composition of production; as production quickly adjusts to demand, the changes in its structure can be ignored in the study of the factors determining its level, and this is the main justification of Keynesian macroeconomic analysis. The third is that, in order to identify the causes that determine the employment level, it is necessary to study the factors on which expenditure decisions depend.

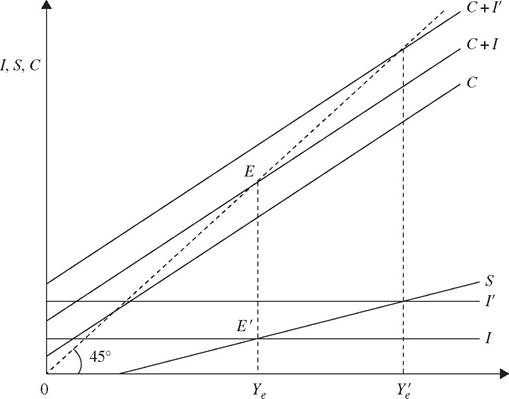

To present the theory of effective demand in the simplest way we will use an expository device invented by Hansen. Aggregate demand is subdivided into an autonomous component, investment, I, and an induced component, consumption, C. Consumption varies with income according to function C = C0 + cY. Investments are assumed to be given at level I. Therefore the aggregate expenditure is I + C = I + C0 + cY. The three functions, I, C, C +1 are shown in Fig. 7. The horizontal axis represents produced and distributed income and the vertical axis represents expenditure. On the 45o line are all the points in which aggregate expenditure equals income. The equilibrium point therefore will be E, at which the C +1 line meets the 45o line. At this point, the expenditure generates exactly the amount of demand and production which will distribute the income, Ye, necessary to finance the expenditure itself. As C depends on the level of income, while I is autonomous, the

Fig. 7 latter variable will determine the level of activity. The level of production determined in this way does not necessarily mean there will be full employment. However, it is an equilibrium point, in that it guarantees equality between aggregate supply and demand.

The problem is: in what sense is it possible to speak of investments as autonomous expenditure if they are, in any case, financed by the savings created by the equilibrium income? The answer on which the Keynesian revolution is based is this: it is investments that generate the necessary saving for financing, not vice versa. In fact, investment decisions are independent of the amount of available savings. A part of investments, for instance, can be financed through credit. Given the propensity to consume of the collectivity, a certain amount of investment will determine, by means of the multiplier, a certain level of income. The savings stemming from that level of income will be exactly sufficient to finance those investments. This can be seen from Fig. 7, where point E' represents the equality between savings and investment. The savings function is S = Y — C0 — cY =— C0 + sY. Let us assume that, starting from an equilibrium situation, investments increase by $100 bn. and that the propensity to consume is 80 per cent. The multiplier will be 1∕(1-c) = 1/0.2 = 5. Therefore, income will increase by $500 bn. The propensity to save is 20 per cent, so that the saving created by the $500 bn. will be $100 bn., which is exactly the value of the additional investment. Fig. 7 shows that an increase in the investments from I to I' will raise the income from Ye to Y'e, while the savings will adjust to the new investment level.

The idea that the levels of output and employment depend on investment decisions has two important theoretical implications. The first is that, if the level of employment depends on the level of investment, rather than on its composition, the neoclassical view that full employment is reached by means of the changes in relative factor prices, and the consequent changes in relative demand, is deprived of any theoretical relevance.

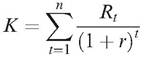

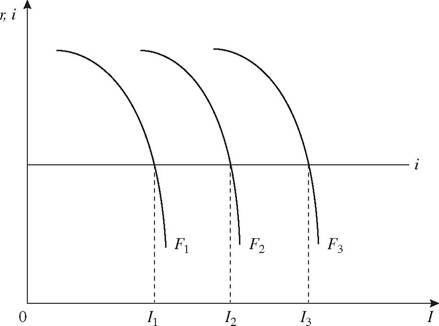

The second implication concerned the explanation of the instability of capitalism. Keynes focused on the problem of why investments did not normally settle at the level that guarantees full employment. Investments depend on the marginal efficiency of capital, which is a synthetic estimate of the future returns of investments, Rt (t = 0, 1,... n). The marginal efficiency of capital, r, is calculated as the discount rate that makes the present value of those returns equal to the cost of the capital goods:

The higher the expected returns from a given investment, the higher the marginal efficiency of capital. Keynes added that, for a given state of expectations, the marginal efficiency of capital decreases as investments increase. In order to determine the level of investments, therefore, it is sufficient to know

Fig. 8

the interest rate, i, which is taken as an indicator of the cost of finance. The problem is that the investment returns, on the basis of which the marginal efficiency of capital is calculated, are not concrete elements, but psychological variables which depend on entrepreneurs’ expectations about the future trends of the economy. However, the future is uncertain and expectations are volatile. Moods, the state of confidence, and the ‘animal spirits’ of the entrepreneurs play a key role in the formation of their expectations and, therefore, in investment decisions. The levels of activity and employment depend on imponderable, uncontrollable, and extremely unstable psychological factors. Fig. 8 shows various schedules of the marginal efficiency of capital, one for each state of confidence, Fi; those which are further to the right represent the most optimistic expectations. Investments are determined in the point where the marginal efficiency of capital equals the interest rate, r = i. It is easy to see that, on a given schedule, investments increase as the interest rate decreases. However, taking interest as given, investments decrease as entrepreneurs’ confidence falls. This should be enough to allow us to understand the profound difference between the notion of ‘marginal efficiency of capital’ and that of marginal productivity of capital: the marginal efficiency of capital depends more on psychological factors than on technology.

7.2.4. The General Theory: liquidity preference

The neoclassical economists consider the interest rate as a real variable, and determine it as the price of savings. In equilibrium it is supposed to equate savings and investments. We have seen that, in Keynes, savings adjust to investments through the variations in income generated by the investments themselves. In this adjustment process the interest rate plays no relevant role. Thus the double problem arises of what the rate of interest is and how it should be determined in a theory of effective demand. Keynes’s solution was to consider it as a monetary rather than a real variable, and to determine it by the forces of supply and demand for money.

In the ‘Cambridge equation’ the quantity theory was formulated in terms of the quantity of liquid balances which individuals wish to keep in relation to the income they earn. From this point of view, money is mainly demanded for its services in the purchasing of real goods. Purchases cannot be completely planned, as they depend on unpredictable factors; therefore liquid reserves are also demanded for precautionary motives. And this is the origin of the liquidity preference theory. Individuals wish to hold liquid assets because the future is uncertain. Money, the liquid asset par excellence, is purchasing power that can be used at any moment to face unexpected eventualities. Therefore, individuals prefer to hold their wealth as money rather than as any other form of asset. But money is also necessary to finance investment. The entrepreneurs who invest more than they earn must in some way obtain the liquidity necessary to finance the investment expenditure. In order to do this they issue forms of liabilities such as bonds, bills of exchange, and bank debts, which they try to ‘sell’ in exchange for money. But why should the economic agents agree to hold their own wealth in the form of non-liquid assets? If liquidity preference exists, the economic agents who renounce holding liquid assets must be rewarded. Here is the liquidity premium: the difference between the returns on non-liquid and liquid assets. In the simplified case which Keynes dealt with, there is no return on money, and the liquidity premium is the same as the interest paid on a non-liquid asset called ‘security’.

In this way, the demand for money depends, not only on the level of transactions, as was suggested by the Cambridge equation with its emphasis on the precautionary and transaction motives, but also on the level of the interest rate. Given liquidity preference, the quantity of money that the economic agents decide to hold increases as the interest rate decreases. So, if the monetary authorities manage to control the money supply, they will also be able to determine the interest rate. If they have this ability they will possess an easily manageable policy instrument. We will soon see what great importance is attached to the two conditions we have emphasized above.

Monetary policy could act on the real economy by means of an ‘indirect transmission mechanism’ which is now called ‘Keynesian’ in most macroeconomic textbooks. An expansion in the money supply lowers the interest rate; then, given the schedule of marginal efficiency of capital, investments are stimulated; finally, by virtue of the multiplier, incomes and employment also increase. No doubt, in Keynes there are many arguments that justify this theory of monetary policy. But it is also true that, in the 1930s, abandoning the views he had held in the previous decade, Keynes became rather sceptical about the effectiveness of monetary policy. The reasons for this scepticism can be found in three factors.

First of all, it is not certain that the monetary authorities are able effectively to control the money supply. Even if in the General Theory Keynes assumed (although rather for explanatory convenience than for any other reason) a quantity of money fixed exogenously by the monetary authorities, on several other occasions he put forward the opinion that the money supply may adapt in a fairly elastic way to the demand and that, in fact, it is quite endogenous. Keynes was not able to exploit all the advantages that a theory of the endogenous money supply offered for his point of view. Instead, as we will see in more detail in Chapter 9, these advantages were fully exploited in more recent times by modern post-Keynesian thinkers.

A second group of doubts were derived from Keynes’s consideration of the role of speculation in the determination of the interest rate. Money is demanded, not only to finance productive activity, but also to finance speculation. The liabilities issued by firms receive a price which depends solely on the forces of supply and demand. In ‘normal’ times, speculators behave more or less like any other economic agent. When the prices of securities increase and the interest rate decreases, speculators expect that, in the future, prices and the interest rate will return to their fundamental values. Therefore they will sell securities with the intention of buying them back in the future. In this way they contribute to stabilizing the stock market. In ‘abnormal’ times, however—and one has the impression that Keynes believed that times are quite often abnormal on the stock market—speculators do not take into consideration the fundamental values, but try to make capital gains by speculating with a very short-run perspective. For example, they buy stocks when their prices are rising, contributing in this way to making their prices rise still more. In an epoch of crisis and pessimism the prices of stocks tend to decrease and the interest rate to rise. Then speculators sell stocks in the expectation of further price contractions. But in this way they contribute to the contraction. The rate of interest will go on increasing. This kind of speculation destabilizes the market and condemns to ineffectiveness the monetary policies which aim at setting the interest rate in a discretionary way. The objectives of monetary policy can be frustrated by speculators’ expectations.

Finally, the third set of doubts concerns the possibility of influencing, to a relevant degree, investment decisions by means of monetary policy. Even if we admit that the monetary authorities are able discretionally to set the interest rate, in what degree would a variation in the latter influence the level of investment? In a minimal way, Keynes argued. It is true that investment decisions depend on the marginal efficiency of capital and on the cost of finance. But profit expectations basically depend on the moods of the entrepreneurs, and these are very unstable. When pessimism predominates, investments will be postponed until better times, and a reduction in the interest rate will not persuade entrepreneurs to change their minds. On the contrary, in phases of optimism the profit expectations are high and selfsustaining, so that it is unlikely that an increase in the interest rate will discourage investment decisions in any significant way. In other words, investments are inelastic with respect to the interest rate. The curves of marginal efficiency of capital are almost vertical in the relevant points. This means that investments are influenced much more by the state of confidence than by the rate of interest.

So, even if we accept that the first two sets of difficulties can be overcome and that the monetary authorities are able discretionally to modify the interest rate without destabilizing the financial markets, this does not mean that such a policy will be effective in influencing the real variables. It is easy to understand why the monetary policies upheld by Keynes’s followers after the Second World War, and adopted by the main industrial nations up to the 1960s, had the simple goal of stabilizing the interest rate.

Keynes’s revolutionary book concludes with an important chapter on the ‘social philosophy towards which the General Theory might lead’. In it he took up again the subjects he had dealt with ten years before in The End of Laissez Faire, but came to a more extreme anti-laissez-faire position, conceding a vast area to the exercise of State intervention in the economy. More sceptical about monetary policy than he had been ten years before, Keynes had by that time convinced himself that the right of the State to intervene in the private sector should no longer be limited to credit management and, by means of it, the savings-formation process. Instead, it should be extended to two fields in which laissez-faire had most clearly shown its deficiencies: the determination of the level of output and of income distribution.

On the first subject, Keynes even reached the point of preaching some form of ‘socialization of investments’. Given that the level of investments normally tend, in a laissez-faire regime, to lead the economy to underemployment equilibria, the State had the right, or rather the duty, to intervene in order to ensure full employment. In regard to the distribution of income, Keynes pointed out that the natural tendency of a laissez-faire regime is towards the determination of arbitrary and unjust distributive patterns; and he believed that the large amount of savings generated by very unequal distribution of income would only serve to keep the level of expenditure and aggregate demand at a low level, rather than supporting the capital accumulation process. The State should also intervene in this case.

It should intervene, however, without damaging the fundamental tenets on which the capitalist economy was built: individualism and private ownership of the means of production. He had become an anti-laissez-faire economist but he was still a liberal. He believed that State intervention should not abolish the ‘invisible hand’ but help it to manifest itself and, in a certain sense, render it visible. This is the origin of the new philosophy of the ‘administered market’, a philosophy that is aptly summed up by Keynes’ telling statement: ‘Economists are guardians not of civilization, but of the possibility of civilization’ (quoted in Skidelsky, Keynes, p. 19).

7.3.