The Balanced-Budget Multiplier

At some point between March and June 1942, Samuelson wrote a chapter, “Full Employment After the War,” for a volume that Seymour Harris was editing on Postwar Economic Problems.1 Whereas elsewhere Samuelson’s concern was the need to take action, in this chapter he focused on economic theory.

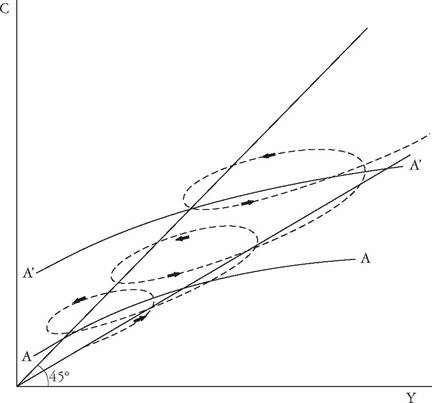

Sensitive to the political implications, Samuelson emphasized repeatedly that he was talking about a technique of analysis that was “neutral on policy questions,” and that, though the framework being used to analyze the problem of unemployment was usually named after Keynes, it had roots in earlier thinking.2 As he had done consistently since his first encounters with the problem of fiscal policy, he distanced himself from Keynes.The existence of a stable relationship between consumption and income was central to the theory of employment. Samuelson explained this stability by talking about the stability of the proportions of household budgets spent on different commodities, something he was becoming very familiar with through his work at the NRPB. Over short periods of time, Samuelson argued, the fraction of income saved rose with income. There was a level of income at which people saved nothing, but as income rose, so did the proportion of income saved. This was shown by the consumption function, AA, in figure 20.1. Over time, the consumption function shifted upward, indicated

Figure 20.1 Consumption and income.

Source: Samuelson 1943d, p. 35.

by the move from curve AA to A,A,. Because income fluctuated over the business cycle, the time path followed by consumption and income was like that indicated by the dotted line in figure 20.1.a

The reason why Samuelson emphasized the relationship between consumption and income was that he believed it to be central to all business cycle analysis: interest rates and stocks of wealth were less important than income as determinants of how incomes were divided between consumption and saving.

The relationship between consumption and income had historically been very stable, but it could be altered by “deliberate social action.”3 The reason why this was mattered was that savings had to be “offset” by spending, either business investment or government spending. If there were to be full employment, there must be sufficient spending to offset the amount that people wished to save. If not, there would be a downward spiral of income and employment until saving was reduced accordingly.He countered the argument that flexible wages would be sufficient to maintain full employment by causing prices to fall, hence lowering interest

a. The diagram is reproduced here to make it clear that this chapter contained a view on the behavior of consumption function that is commonly, but incorrectly, thought to have surfaced only later. The diagram is very similar to ones that were later used to justify the permanent income and lifecycle theories of consumption. rates and stimulating investment. The problems with this argument were that low interest rates—cheap money—did not work: the argument relied on continuously falling prices, but this would have “adverse psychological effects.” It was thus possible that ever-falling prices would make unemployment worse, not better. There was, likewise, no reason to believe that the economic system would automatically generate full employment. By the same token, there was no reason to believe that there would necessarily be unemployment. It was an empirical question. Samuelson did not point out that the same argument was to be found in Keynes's General Theory.

This chapter is also the first publication in which Samuelson referred to the saving and investment diagram he had used in “The Modern Theory of Income” (see figure 18.1), as “analogous to the ‘Marshallian cross' of supply and demand.”4 This diagram and its equivalent showing consumption, investment, and a 45-degree line (figure 13.1) came to be associated so closely with Keynesian economics and Samuelson's textbook that it is important to note he remained skeptical of it.

The reason was that it oversimplified the factors behind investment:However valid this [the S and I diagram] may be formally, it is necessary to insist that investment in anything but the shortest run cannot be related to income in the way that savings can. Even in the shortest run it is not the statical level of income, but its time pattern of change taken in conjunction with the existing stock of capital equipment, which determines investment. In the present writer's opinion, this cannot be emphasized too much.5

Once again, he was stressing the importance of dynamics. Perhaps this was the reason he was in no hurry to publish his earlier paper, despite Hansen's urging him to do so.

Reviewing the “offsets” to saving that might contribute to full employment, Samuelson covered various possibilities, including business investment, government spending to redistribute income, foreign investment, the development of new wants to stimulate consumption, deficit-financed government spending, and “government spending matched by equivalent taxes.”6 The last of these was a recent discovery.

Only recently have I become convinced that item 6 [the last factor in this list] does provide a genuine offset to saving—that a balanced budget at a high level, with “nonprogressive” taxes and expenditure, is nevertheless employment- and income-creating. A proof cannot be attempted here. However, if valid, this form may provide an important method by which our economy can hope to maintain the level of effective demand.[40]

This was what came to be known as the “balanced-budget multiplier:” the idea that an increase in government spending matched by an equivalent rise in taxation is expansionary. The political significance of this is hard to exaggerate, given the extent to which opposition to Keynesian ideas focused on the danger of perpetual government deficits.

Shortly after discovering the balanced-budget multiplier, Samuelson had a conversation with Bill Salant, one of two brothers whom Samuelson had known as a student in Harvard, discovering that the two of them had worked out essentially the same result.[41] Samuelson was confident that the result had not been published, at least in the English-language literature, and suggested they write it up together.

In July 1942, Salant, who was then a member of Lauchlin Currie's staff in the White House, wrote up the idea as “Taxes, the Multiplier and the Inflationary Gap.”[42]Salant's starting point was the claim that the government deficit had an effect on national income that was the same as an equivalent increase in investment. This led economists to deduce that, provided the deficit remained unchanged, alterations in government spending would have no effect. He then proceeded to explain why this was incorrect. The key was in considering changes in government spending separately: government spending would raise national income directly, and it would also do so through inducing rises in consumption. If taxes rose to fund the rise in government spending, they would reduce consumption and exactly offset the rise in consumption induced by the rise in government spending, leaving just the rise in government spending? The balanced budget multiplier would be precisely one.

Another way to think about this is that the balanced-budget multiplier arises because the only difference between government spending and taxation is that the former is a component of national income, whereas taxation is not (taxes are treated as a transfer payment, like Social Security payments or gifts from one person to another that are not associated with the production of any commodity or service). The balanced-budget multiplier thus depended on the way the national accounts were constructed, which provided one reason the idea had not been discovered sooner.c The earliest national accounts defined national income so as to include only the part of government spending that was financed by taxes, a procedure that, even if it made sense during the Depression, certainly made no sense during the war, when the deficit increased to an unprecedented fraction of national income. Similarly, when Currie had used multiplier analysis to work out the cause of the 1937 recession, he had used the deficit—the net contribution of the government to income generation.d Samuelson added another explanation of the failure to see the balanced-budget multiplier that applied specifically to him and Salant—they were both concerned with foreign trade multipliers, where it makes sense to see the stimulus as being the trade balance, or exports minus imports.

Samuelson was right to be surprised that the result had not been discovered earlier. Looking at the algebra alone, it is hard to understand why Samuelson did not see the idea when he was analyzing the difference between public works and relief expenditure in the paper he wrote the previous summer.[43],' Had he asked how much income would have been generated by transferring money from the public works budget to the Social Security budget, he would have gotten the same answer. Those who were concerned with war finance, such as Salant at the White House and his brother Walter at the Office of Price Administration, were using the concept of the inflationary gap, and it was in this context that Keynes had implicitly employed the idea of the balanced-budget multiplier when writing a statement for the 1940 budget in the United Kingdom.[44] However, perhaps the most telling interpretation is that their failure to see the idea illustrates the way in which theorizing about the multiplier was driven by policy issues rather than theoretical questions internal to the discipline. Neither of Samuelson’s two papers on the multiplier had the theoretical precision and focus that he achieved in papers in which the goals were purely theoretical.

Samuelson and Salant continued to correspond about publication. In October, Samuelson wrote with suggestions for how that paper could begin, saying that material Salant had already written could follow this. Samuelson also suggested adding an alternative explanation of the result.

Originally the community is in equilibrium at that level of income where savings and investment[,] in the schedule sense, are just equal. After the proposed change the national income produced for the civilian population can only be in equilibrium at the same level on the assumption that private investment is unchanging and that savings depend only upon disposable income. Any other result would lead to a contradiction. Hence the total of government employment is superimposed upon the old level of employment so that there is a dollar increase in employment for each spent dollar increase in taxes.[45]

This makes it clear that, although the mathematics behind the result was very simple, they were still struggling with the conceptual issues, deriving the theorem in different ways.

The reference to national income produced for the civilian population shows that their work was rooted in wartime discussions, a point reinforced by reference not to an abstract concept of national income but to specific income series developed in government agencies. Even the correct concept of national income to be used was unsettled. Samuelson closed by insisting that their names appear in alphabetical order, and that he hoped they could meet a week later when he was in Washington. However, the paper was not finished, because Salant moved to London, working for the Office of Strategic Services, to analyze bombing targets.[46]