The New Keynesian Macroeconomics

9.6.1. A distant Hicksian background

Perhaps this is the right place to say something about the ideas developed by John Hicks after his ‘conversion’ around the middle of the 1960s—a conversion which requires a more in-depth reinterpretation by historians than is possible in an outline such as ours.

However, it is already possible to see that it must have been much more drastic than it seemed at first sight, a conversion that induced the great neoclassical economist to judge as ‘a piece of rubbish’ the theses on the functional distribution of income which he had himself formulated in 1932 in the Theory of Wages (theses which are still today taught in the orthodox economic textbooks). That same conversion led him to reconsider the general theoretical significance of methodological individualism and the hypothesis of individual maximizing behaviour, besides inducing him to criticize the interpretation of Keynes based on his old IS-LM model. The model was rejected basically for two reasons: first, because the role played by liquidity preference, as Keynes intended it, in the determination of the dynamics of employment cannot be adequately understood in a static temporary equilibrium model, such as the IS-LM; second, because it makes no sense to determine the macroeconomic equilibrium by means of two curves, one of which, the IS, expresses a condition of flow equilibrium and the other, the LM, a condition of stock equilibrium. And if all this is not enough to justify the classification of the ‘second Hicks’ within the post-Keynesian approach, there are also some other skilful and courageous changes of attitude: his prompt acceptance of the Cambridge criticism of the neoclassical theory of capital (in Capital and Growth, 1965); his use of the method of vertically integrated sectors and his formulation of non-steady-state growth models (in Capital and Time, 1973); and, finally, his most recent revision of the theory of money (in A Market Theory of Money, 1989).But this ‘later’ Hicks is important especially because, with his fix-price model, he laid down the theoretical bases of the new Keynesian macroeconomics of the 1980s. The fix-price approach, proposed in Capital and Growth and taken up again in The Crisis in Keynesian Economics (1974), goes well beyond the traditional neoclassical argument that the results obtained by Keynes depend on the abandonment of the hypothesis of perfect competition, and also goes beyond the observation that most Keynesian macroeconomic modelling, beginning from the theory of the multiplier, presupposes an implicit hypothesis of fixed prices. Hicks’s objective was much more ambitious, since he rejected en bloc the neoclassical theory of price formation in a competitive regime, a theory which, assuming that economic agents are all price-takers, needed to invent an imaginary auctioneer to account for the process of price-setting. According to the later Hicks, it is only in particular markets, speculative ones, that the traditional flex-price hypotheses make sense. In industrial goods markets, on the contrary, prices are set by the agents themselves, who modify them by responding to economic signals such as variations in wages and other prices. This does not mean that these prices are ‘rigid’, but only that they do not change so fast (i.e. ‘instantaneously’) as the neoclassical microeconomic textbooks would lead us to believe. The main consequence is that it is necessary to reject the widespread prejudice of Marshallian origin (even though Marshall was not a theorist of the auctioneer), according to which price variations predominate in short-run adjustments and quantity variations in long-run adjustments.

The fix-price approach enjoyed wide success in the 1970s and 1980s. Besides the non-Walrasian equilibrium models, which were, at least in part, inspired by it, or the post-Keynesian models, which adopted the fix-price hypothesis long before Hicks had reproposed it, in the last twenty years a stream of thought has developed which has placed this hypothesis at the centre of macroeconomic analysis, pushing it further along the road opened by Hicks, especially in the search for microeconomic justifications.

It is still difficult to say whether studies moving in this direction will lead to the construction of a homogeneous theoretical system. Certainly, they cannot all be assimilated into the post-Keynesian approaches, especially on account of the presence of various marginalist theoretical residues. On the other hand, all these authors have, in common with the post-Keynesians, a critical attitude towards monetarism and neomonetarism, as well as the desire to reconstruct macroeconomics on Keynesian bases. Lacking a better option, and well aware of the danger of misrepresenting particular authors by using a label, we shall accept the now widespread use of uniting them in what has been defined the ‘new Keynesian macroeconomics’, even though it seems to be more of a bricolage of models than a homogeneous approach.To be precise, various aspects of this approach differ from the postKeynesian one. While the latter was formed in contrast with the neoclassical synthesis and monetarist counter-revolution, the development of new Keynesian macroeconomics was stimulated by the need to oppose the neo-monetarism of the new classical macroeconomists. On the other hand, while post-Keynesians rejected monetarism and neomonetarism en bloc, the new Keynesians accepted some of their hypotheses and fundamental penchants, in particular the following:

(1) a theoretical preference for monetary rather than fiscal policies;

(2) a greater analytical attention to the rigidities from the supply side, rather than from that of demand;

(3) the attempt to micro-found macroeconomics on the basis of an hypothesis of rational or quasi-rational behaviour of agents;

(4) the widespread (although not complete) acceptance of the rational expectations hypothesis;

(5) the adoption of the neoclassic conceptual apparatus, especially with regard to the relationship between the remuneration of productive factors and their level of utilization; employment, for example, is almost invariably assumed as determined by the marginal productivity of labour and the latter as equivalent to the real wage.

With these premisses, it is no wonder that many people have begun to doubt the truly Keynesian nature of this approach. In effect, only two points substantially differentiate new ‘Keynesian’ macroeconomists from new ‘classical’ macroeconomists: rejection of the flex-price hypothesis and/or the complete information hypothesis. It must, however, be acknowledged that the new Keynesians have gone even further than the post-Keynesians in studying the microeconomic conditions of real and nominal rigidity and in analysing the macroeconomic effects of the various information asymmetries.

9.6.2. Nominal rigidities

An ambitious attempt at explaining price and wage rigidities has been made by Okun in ‘Inflation: its Mechanics and Welfare Costs’ (1975) and in Prices and Quantities (1982). Okun developed Hicks’s distinction between ‘flex-price’ and ‘fix-price’, transforming it into that between ‘auction’ and ‘customer’ markets. In the former, prices are determined by supply and demand. In the latter, they are fixed by the sellers and kept stable for as long as possible with the aim of preserving a particular clientele of the firm. ‘Customer’ markets allow firms to economize both on the use of plant and on the cost of acquiring and supplying information about their own product markets (market research, advertising etc.).

But they also enable customers to save on research costs. Because of the costs involved, buyers do not push their research to the point of finding the best possible seller, i.e. the one who sells at the lowest price. Moreover, after finding a seller who has quoted a convenient price, the buyer is unlikely to take the trouble to carry out further research as long as the price remains stable.

Buyers’ reactions to price increases and reductions are asymmetrical. A seller who increases his price will lose many customers since they will immediately notice the price increase without shouldering the cost of new research. A firm that lowers its prices, on the other hand, will acquire few new customers, since the customers of competitor firms will have to meet the costs of research before the reduction is noticed.

In addition, as Stiglitz pointed out, in the presence of incomplete information on product quality, buyers often look to price as a quality indicator: goods that cost a lot are thought to be worth a lot. This provides sellers with a further reason for not lowering prices during a recession: avoid giving customers information that may be interpreted as a sign of deterioration in quality. All this induces firms to keep their prices stable. It should be noted that this is not only nominal but also real rigidity, since relative prices are involved. Because of it, a negative shock in aggregate demand will give rise to real recessive effects.Okun made a similar distinction to that between ‘auction’ and ‘customer markets’ with regard to the labour market, extending the theory of ‘dual labour markets’ already put forward by P. B. Doeringer and M. J. Piore. There exist both competitive labour markets and labour markets internal to the firm (‘career markets’). In the latter, firms offer workers long-term wage contracts which are slightly higher and more stable with respect to those prevailing in the markets external to the firm. In this way the firm aims, on the one hand, to encourage the workers to be more efficient and, on the other, to keep workers’ abilities within the firm. When the economy enters into a period of recession, the firms do not reduce wages, but dismiss the most inefficient and least skilled workers.

Other economists have investigated the theoretical implications of a fact which is obvious and yet disregarded by the neomonetarists: that labour contracts are defined on a nominal basis and are, in any case, long-term contracts. Workers and firms would both rationally choose long-term contracts: because negotiations imply substantial research and transaction costs; because even more costly are industrial actions with which the parties show off and build up their bargaining strength; because firms are frightened of losing their market shares when they adjust monetary wages before their competitors.

Of the economists who contributed to this line of research we will only recall the work by J. Gray and S. Fischer. Their most interesting result is that, contrary to what the neomonetarists asserted, particular monetary policy measures can be effective, even if perfectly predicted by the economic agents, simply because the duration of the labour contract and/or the level of indexation can hinder a quick and full adjustment of wages to the expected effects of the policy. An expansion of money supply creates inflation. If nominal wages do not adjust soon, the real ones decrease so that companies are induced to raise production.This line of thought was further developed in the theory of ‘staggered’ labour contracts, recently put forward by J. B. Taylor. In this approach contracts are long-term, but not all expire on the same date. The fact that expiration dates are not synchronized turns out to be useful to companies and workers since it enables them to collect information by observing the contracts stipulated by others. Furthermore, it is assumed that the worker does not exclusively aim at maximizing his own wage, but also endeavours to maintain certain ‘relativities’ with other workers. Let us suppose that an exogenous shock leads to a reduction in the aggregate demand at time t. The workers who renew their contracts in t, having rational expectations, know that, say, at time t + d the economic policy will become expansive again. If they accept a reduction in their nominal wage in t, this will allow for a reduction in prices. But in this way their real wages will diminish with respect to those workers who will renew their contracts in time t + d. Therefore they will refuse a reduction in their nominal wage, so as to avoid a change in their relative position; they will rather accept a temporary increase in unemployment, a problem that can be faced in fact by an expansive monetary policy. In this way it is possible to understand why monetary policy is able to produce real effects even in the presence of rational expectations.

The problem with the theories of nominal wage rigidity is that they assume real wages have an anti-cyclical trend, implying that they should increase during recessions, when employment drops and marginal labour productivity grows, and decrease in phases of expansion. In reality, as Keynes had already realized in 1939, real wages tend to be pro-cyclical. Those theories therefore appear disproved by empirical data. For this reason, many economists have tried to explain nominal rigidities starting from price policies rather than wage policies.

A group of economists of this kind, among which we will recall N. G. Mankiw, G. Akerlof, and J. Yellen, developed the analysis of costs for the adjustment of prices, or the ‘small-menu costs’ approach. These are costs that a firm must bear in order to modify the prices of its own products when conditions of demand or production vary. There are various types of such cost, for example those connected with the updating of payrolls and price lists, those undergone in changing labels of products, and those caused by loss of confidence on the part of customers who face continuous price changes and over-complicated renegotiations of contracts. Firms try to avoid these costs, even if they are small in relation to product prices: it is sufficient that they are higher than the profit increases that would follow these price cuts. Then the decision not to cut prices would be rational. But often companies avoid changing price even in the absence of menu costs, provided the expected profit increases are small. This kind of behaviour is quite widespread, and is considered ‘quasi-rational’. In short, companies tend to fix their prices and to hold them stable for as long as possible. So, when facing temporary changes in demand, they modify production levels, utilization of plant, and levels of inventories, rather than product prices. It is this phenomenon which gives real efficacy to short-term monetary policies.

It can generally be said that theories of nominal rigidities explain unemployment and under-utilization of resources as a consequence of a co-ordination failure. This kind of failure derives from the fact that no one agent is motivated to co-operate with the others to achieve results that would be optimal for all. For instance, no firm is induced to lower its prices when there is a fall in demand, because any profit increases obtained in this way would be small and probably lower than menu costs. If all the firms do the same, production, employment, and aggregate profits will all diminish. If, on the other hand, there were co-ordination among the firms, they would all reduce their prices. In this way production costs would also fall. Furthermore, positive wealth effects will be prompted which would increase aggregate demand. Thus a new equilibrium would be achieved with lower prices but without reducing production, employment and profits. ‘Keynesian’ type policy interventions, such as monetary expansion during a recession, would therefore serve to avoid the harmful effects of co-ordination failures.

An underlying doubt has been put forward on the Keynesian nature of the theories of nominal rigidities. It should not be forgotten that Keynes expressly rejected this kind of explanation for unemployment. Indeed, in chapter 19 of his General Theory he argued that nominal rigidities are an element of stability since they prevent the triggering of those vicious recession and deflation circles which drive the economy towards depression.

9.6.3. Real rigidities

According to neoclassical theory, the rigidity of nominal wages is not sufficient to cause unemployment. An inflationary process can always compensate for an increase in the monetary wage so as to make the real wage coincide with marginal labour productivity. If the real wage is made flexible in this way, it will always be possible to reach the rate at which the supply and demand for labour are equal. Involuntary unemployment is impossible. However, few economists in the eighties were prepared to accept the neomonetarist provocation that stable unemployment is always voluntary. When the unemployment rate stays riveted for long at 7-10 per cent, as occurred in the major capitalist countries in the eighties and in Europe still today, economic theory must account for it in a credible manner. The new Keynesian macroeconomists endeavoured to do so by elaborating models that explained the rigidity of real wages.

A first type of model is based on the theory of implicit contracts. Contributions to it were made by economists such as M. N. Baily, D. F. Gordon, C. Azariadis. According to this approach, workers are more risk-averse than entrepreneurs. The latter therefore tend to take on the responsibility for that part of the risk which workers would encounter in a perfectly competitive market, where wages would change sharply. Thus they offer workers implicit contracts according to which wages are maintained stable through time. A consequence of this is that, in periods of recession, the entrepreneurs, rather than reducing wage-levels, tend to cut labour hours or dismiss some of employees.

One of the most interesting of the recent microeconomic approaches to the problem of unemployment is that of efficiency wages. The basic idea here is that labour productivity increases with wages. An early theory of efficiency wages in the developing countries was put forward in 1957 by J. Leibenstein in Economic Backwardness and Economic Growth. The argument was that, given the subsistence levels of the wages prevailing in the developing countries, an increase in them would improve the standard of living and the health of the workers and therefore would increase their work performance. In the 1970s various attempts were made to generalize this theory and extend it to industrial countries, for example by Salop and Solow. Finally, in the early 1980s, a comprehensive formulation was reached in works by Akerlof, Weiss, Shapiro and Stiglitz.

The theory of efficiency wages is based on three principal ideas. The first is that the intensity of the work effort of each employee, and therefore the marginal productivity of labour, increases with an increase in wages. The second is that the workers’ effort is also influenced by the level of unemployment, in that the fear of being dismissed for inefficiency increases with an increase in the probability of not immediately finding another job with the same pay—a probability that rises with the level of unemployment. The third hypothesis is that there is a type of asymmetric information, as firms are not able directly to ascertain the intensity of effort of hired worker or the ability of those to be hired. In these conditions it is in the interest of firms to pay high wages to encourage workers’ effort. Wages, by hypothesis, are equal to the marginal productivity of labour. If there is unemployment the firms are not induced to lower wages and to take on unemployed people since, if they did so, they would induce a reduction in the efficiency of the workers employed. Whereas, if aggregate demand decreases, the firms have not a great advantage in reducing wages, since by doing so they would trigger an adverse selection process: they would lose their best workers, who would begin to look for better paid jobs. Thus, firms tend to leave wages unchanged and lay off the excess labour force. Furthermore, as firms are not able to ascertain individual levels of effort, they would choose to lay off workers randomly. Therefore, wages would not only be high, i.e. higher than those which would guarantee full employment, but would also be fairly rigid; and this is the simple consequence of the rational choice of the firms. In a capitalist economy unemployment is permanent, as the fear of losing one’s job is one of the factors that stimulates the workers’ efforts. There is no Pareto efficiency in this type of equilibrium, owing to the presence of unemployment; but firms maximize profits also thanks to unemployment.

In efficiency wage theories, it is the firms that decide to pay higher than market wages. In reality the workers too can take the initiative, as is maintained in insider-outsider models, for which we shall refer to the contributions made by A. Lindbeck and D. J. Snower. The basic hypothesis here is that firms are faced with turnover costs, i.e. costs sustained for labour turnover. These can be broken down into costs for research, advertising, staff selection, negotiation, and training. In addition there is another special and very important cost: firms with a rapid labour turnover offer unstable employment prospects; as a result workers have little incentive to dedicate themselves to production and build up a reputation of trust and efficiency—and this obviously reduces productivity. So firms have a margin to allow them to pay slightly higher than market wages, if they manage to save on turnover costs. Employed workers (insiders), are generally more unionized than the unemployed (outsiders). They are therefore able to take advantage of their bargaining power to induce firms to pay higher than market wages. The overall result is rigidity of real wages with a consequent persistence in unemployment. Furthermore, the model also accounts to some extent for employment stability; when faced with a modest recession, firms tend to ‘hoard’ their workers and dismiss fewer than would be justified by a flagging demand; in this way they save on turnover costs. Lastly, besides explaining the existence of permanent unemployment, the theory also explains its composition: young people, women, members of ethnic minorities, in other words, those workers who have not had a stable job in one of the strongly unionized sectors, tend to remain unemployed.

Real rigidities also occur in financial markets, besides in labour and commodity markets. This aspect of the problem has been investigated by B. C. Greenwald and J. E. Stiglitz, who, in a model recalling post-Keynesian views, argued that the main causes for unemployment are uncertainty, risk aversion and information asymmetries involving financial markets.

Since little information on the profitability of firms is made available to savers, this causes many firms to encounter difficulties in raising funds on the stock markets; thus, when they expand investments beyond their selffinancing capacity, they are obliged to resort to bank credit. But increased indebtedness raises the risk of bankruptcy, as Kalecki already established in his theory of increasing risk. Firms are quite adverse to risk, so that in the event of a recession, they tend to reduce production to ward off the risk of bankruptcy. As a consequence there is a reduction in aggregate supply together with demand, and prices do not fall. The recession may be aggravated by the banks’ aversion to risk; as soon as the banks sense their customers are running an increased risk of bankruptcy, they ration credit and raise interest rates. Consequently, there may be a credit squeeze even if the monetary authorities do not reduce the money supply. In a situation of rising finance costs and reduced availability of credit, the risk of bankruptcy further increases, thus giving rise to a sort of self-realization of expectations, and the economy becomes further sucked into the spiral of depression.

9.6.4 A comparison between some contemporary schools of macroeconomics

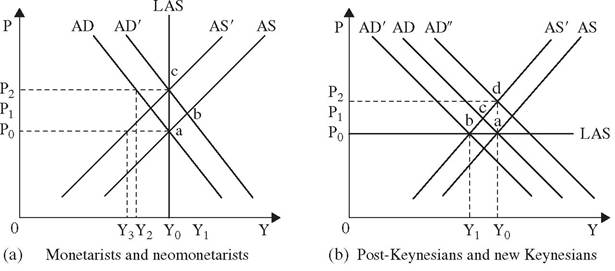

Following the monetarist counter-revolution, the IS-LM model fell into disuse, although in recent years it has shown signs of recovery. On the one hand, a growing number of variously oriented Keynesian economists found it unsuitable for correctly representing Keynes’ thought. On the other, the new classical macroeconomists also found it inadequate and criticized its unorthodox micro-foundations, the theory of non-neutrality of money and the hypothesis of exogenous and non-rational expectations. In addition, the ‘Lucas critique’ had laid some doubt on the stability of the IS and LM curves, arguing that they may shift as a consequence of the policies that the curves themselves suggest. But the decisive factor which led to the abdication of the model is that many economists, guided by interests in monetarist research, had shifted their attention to the problem of inflation. Now, the IS-LM analytical apparatus is based on the hypothesis that the price level is a datum, and only in a rather contorted manner can be used to explain the swings in equilibrium that follow variations in inflation. It was therefore replaced by a scheme known as the AD-AS model (aggregate demandaggregate supply), which has been devised precisely to account for variations in equilibrium in the presence of inflation. In its simplest version, it can be constructed as follows.

Assuming that the money supply in nominal terms, M, is given and considering an economy in macroeconomic equilibrium, we shall posit that the price level is determined at level P0, as illustrated in Fig. 17(a). The quantity of real money in circulation M/P0, the level of real liquid balances and real wealth, the demand for money and the interest rate will be determined. Then the level of investments and aggregate consumption, and consequently, real income, Y0, corresponding to the price level P0, will be determined. Now let us assume that prices increase up to level P2. Since the supply of nominal

money is given, the real supply will be reduced and consumption will diminish. In addition, the value of real liquid balances will be reduced and, consequently the demand for money will increase. This in turn will make the interest rate rise and investments diminish. Income will fall to level Y2. We have thus obtained an aggregate demand curve that plots real income in relation to the price level. It is obviously a downward sloping curve, like AD in Fig. 17(a). The curve shifts to the left when the supply of nominal money diminishes and to the right, for example towards AD', when the supply of nominal money increases.

We shall now construct the aggregate supply curve. In doing so, we assume that the nominal wage is given, in addition to technology. Positing that prices are at level P2, the real wage is known. According to the neoclassical approach, the level of production will be that at which the real wage corresponds to marginal labour productivity. Therefore the level of production is known, i.e. the aggregate supply: income Y0 on the AS' curve in Fig. 17(a) will correspond to price level P2. If we now lower prices to level P0, we obtain an increase in the real wage and a consequent reduction in employment and production. Aggregate supply will fall to Y3. The curve AS' illustrates how production declines when prices fall, given the nominal wage. It moves to the right, towards AS, for example, when the nominal wage diminishes because, at equal prices, the lower labour cost will make profits and consequently production increase.

Now let us consider the monetarist theories. A vertical long run Phillips curve (see section 9.3.2) will coincide with a long-run aggregate supply curve, like the LAS curve in Fig. 17(a). It is vertical because it is assumed that there is full employment in a long-run equilibrium, so the aggregate supply cannot increase in real terms when the quantity of money increases. In the short run, however, the decreasing Phillips curves will correspond to increasing aggregate supply curves. We shall start from point a, in which the economy is in equilibrium at income Y0 and at price level P0. If the nominal supply of money increases, the short-run aggregate demand curve shifts towards AD' and triggers an inflationary process. When an entrepreneur sees that the prices of his products are increasing, he is led to believe that his profits are swelling and real wages are decreasing. He will consequently boost production. Moving along AS, the economy will shift towards point b. Prices will rise to level P1 and income will pass to Y1. In this way, the full employment production level will be exceeded and monetary wages will increase. Sooner or later, the entrepreneurs will realize that not only the prices of their products, but also those of their inputs, including wages, have increased following the inflationary process and they will adjust their expectations of inflation. The short-run aggregate supply curve will shift towards AS'. In the end, the economy will achieve a new long-run equilibrium at point c, where income will again be that of full employment, Y0, while prices will stabilize at level P2. There will have been a temporary increase in production because unexpected inflation has deceived the businessmen. But after they have adapted their expectations of inflation, production will return to its equilibrium level. The increase in prices will however be permanent. If the monetary authorities want to keep the economy at level Y1, they must be prepared systematically to deceive the economic agents, by making the money supply and inflation rates continuously grow.

The neomonetarists have dissociated themselves from this model by criticizing the hypothesis of adaptive expectations and replacing it with one of rational expectations. In their opinion, businessmen are always able to foresee the inflationary effects of systematic economic policies, so that when the money supply increases, they are not deceived by inflation, but can anticipate its effects. This means that when the aggregate demand curve shifts towards AD0, entrepreneurs will expect increases in monetary wages and prices and will not raise production: The aggregate supply curve will immediately move towards AS0. The effects of monetary expansion will be purely inflationary and real income will remain riveted to level Y0.

We shall now consider the post-Keynesians. For these economists, the aggregate supply curve is determined by long-run investment decisions. Entrepreneurs build up excess capacity expecting to earn a stable normal profit in the long run. As the aggregate demand rises in the short run, they will not raise their prices but will increase real production. Furthermore, monetary wages will not depend on labour demand. They are determined through bargaining between social classes. Given the workers’ bargaining power, wages will not vary in the short run as employment varies. Therefore the supply curve is horizontal, as LAS in Fig. 17(b). Post-Keynesians do not consider increasing aggregate supply curves like AS and AS0. Starting from a situation of equilibrium as represented by point a, with income at level Y0 and prices at level P0 if the government reduces the money supply (but, above all, public expenditure) the aggregate demand curve will shift towards AD0. Firms will react by reducing production at fixed prices. The economy will shift towards point b and real income will fall to level Y1.

It is more difficult to synthesize univocally the theories of new Keynesian macroeconomists on account of the multitude of models they have elaborated. We think our brief description will, however, sufficiently represent their ways of reasoning. The aggregate supply curve has an upward trend, as in AS and AS0 in Fig. 17(b), and is not horizontal as in LAS. Starting from a situation of equilibrium as represented by point a, when there is a reduction in the money supply and the aggregate demand curve shifts to the left, entrepreneurs expect a recession; they perceive an increase in the risk of bankruptcy and therefore curb production. The supply curve shifts towards AS0. Monetary prices are not reduced because the aggregate supply has diminished together with demand. The economy will therefore stabilize at a point of equilibrium, as for example b, in which real income has fallen to level Y1. This is the adjustment process contemplated in the Greenwald and Stiglitz model. In this approach, price stability is a consequence of decisions to reduce production. According to the hypothesis of nominal rigidities, however, the reduction in production is a consequence of price stability: employment falls because firms tend to fix prices when demand diminishes. To account for the hypothesis of real rigidities, it is necessary to reason in yet another way. Let us suppose that there is a shock on the supply side, i.e. a growth in monetary wages caused by an increase in the bargaining strength of inside workers. The increase in wages will cause the supply curve to shift to the left. Prices too will increase, but less than nominal wages. Thus real wages will increase and employment will fall. Given the money supply, the economy will shift to point c moving along curve AD. Prices will increase to level P1 and income will reach a level between Y0 and Y1. If the government wants to oppose this recession, it will have to expand the money supply so as to shift the aggregate demand curve towards AD" and drive the economy to return to production level Y0 but with prices at level P2.