The Post-Keynesian Approach

9.5.1. Anti-neoclassical reinterpretations of Keynes

It seems that there is a basic incompatibility between Keynesian and neoclassical theory. This is confirmed by the fact that all the economists who took Keynes seriously, and his conviction that he had formulated a general theory, ran up against prejudices of the neoclassical theoretical system.

The economists of this type are called ‘post-Keynesian’. They are a group of scholars with rather heterogeneous views, even in regard to the interpretation of Keynes. Perhaps one day an organic post-Keynesian theoretical system will emerge from their work. At the moment, we must content ourselves with classifying them into groups of affinity. And the simplest classification distinguishes the European from the American post-Keynesians. The birthplace of the first group was the University of Cambridge, where a direct Keynesian tradition, formed in the early 1930s around the ‘circus’, has survived until very recently. The main members of this group are Richard Kahn, Joan Robinson, Nicholas Kaldor, and Luigi Pasinetti. The second group gathered around the Journal of Post-Keynesian Economics. Its most important members are Hyman Minsky and Sidney Weintraub. A distant ancestor of all post-Keynesian economists is, however, the English economist G. L. S. Shackle. It is also worth mentioning another two economists who, at least partially, can be considered post-Keynesian: Lorie Tarshis who, although graduating at Cambridge in Kaleckian economics, is a member of the American post-Keynesian group; and Kenneth Boulding, an evolutionary economist who made important contributions to the construction of the Cambridge theory of distribution. Finally we should mention Joseph Steindl, a ‘Kaleckian’ who is difficult to classify and who worked in an original way, especially on the theory of normal prices in monopoly conditions.

The most recent generation of post-Keynesians, who are legion, especially in the USA, Great Britain, and Italy, are working on the difficult task of integrating the various components of post-Keynesian theories in the attempt to produce a complete and coherent theoretical system.The most important difference between the two main groups concerns their favourite field of investigation, growth and distribution for the Europeans and monetary dynamics for the Americans. This leads to the presumption that the two approaches are not basically incompatible and their theories are complementary. Both groups, in their rejection of the neoclassical synthesis, have endeavoured to reinterpret Keynes by separating what is really Keynesian in the General Theory from the neoclassical and Marshallian residues.

The essence of Cambridge interpretation of Keynes has been well expressed in two works by Garegnani and Pasinetti. In ‘Note su consumi, investimentie domanda effettiva’ (1964-5), Pierangelo Garegnani put forward the idea that the principle of effective demand refers to an economy in a reproduction equilibrium. In this state, savings equal investments in such a way as to guarantee equilibrium between effective demand and the quantity supplied of produced goods, but not necessarily the full utilization of resources or full employment. The adjustment of savings to investments occurs through the variations in income caused by the investments themselves, and not through the determination of the interest rate. The latter is not an equilibrium value for the price of the capital services. The rejection of the neoclassical conception of the interest rate led Garegnani to downgrade the notion of marginal efficiency of capital, and to accept the liquiditypreference theory only as an auxiliary construction, necessary to give an alternative explanation of interest. He also rejected the idea that Keynes’s theory was of a short-run type, or, rather, argued that the principle of effective demand is of more value in the long run, when it makes sense to assume that the economy grows along an equilibrium path in which normal prices prevail.

Pasinetti moved along a similar interpretative line in ‘The Economics of Effective Demand’ (in Growth and Income Distribution, 1977), in which he endeavoured to reinterpret the General Theory from a Ricardian point of view, ending up by rediscovering in Keynes the power of the ‘Ricardian vice’. By means of this, Keynes avoided being misled by the love of elegance and symmetry and aimed instead at investigating a few clear and simple causal relationships among the main economic variables. In this way he was able to identify the existence of a unidirectional causal chain which goes from money to consumption, passing through the determination of interest rate, investments, and the level of income.

This interpretation of Keynes in a long run perspective is centred around the idea that the principle of effective demand cleverly solves a problem which had got the better of both classical and neoclassical economists: determination of output and employment levels. Ricardo, for example, at times assumed the aggregate output level as exogenous, while at others he determined it as full employment on the ground of the Malthusian law of population. The neoclassical economists, on the other hand, determined it as full employment assuming Say’s law and maximizing behaviour. All these hypotheses, the law of population, Say’s law and maximizing behaviour are unrealistic. In fact full employment is not a typical result of real economies. According to the principle of effective demand, aggregate production is determined by autonomous demand components, especially by investments and fiscal policy, and may stabilize at any level, although it is unlikely to be that of full employment.

It is here that enter the stage Shackle’s interpretation. In his first works on uncertainty and ‘crucial choices’, Shackle rejected the probabilistic conceptions of expectations with the argument that choices, once made, destroy the possibility of repeating the experiments. The economic agents are aware of this fact, and therefore avoid formulating expectations about all possible events, and instead tend to focus their attention on pairs of objective possibilities which they judge to be particularly important.

These possibilities concern events which, ex ante the economic agents judge potentially able (or unable) to produce surprises.Uncertainty is at the centre of Shackle’s reinterpretation of Keynes; it is considered the principal factor of economic fluctuations and the basic cause of the intrinsically unstable nature of capitalism. The concept of marginal efficiency of capital is re-evaluated, from this point of view, but not before being reinterpreted in an anti-neoclassical sense. Shackle believes that the marginal efficiency of capital has nothing to do with the productivity of capital; instead, it is no more than a sort of ‘psychic alchemy’, a mental construction by means of which the entrepreneurs try to deduce from basically non-rational expectations some evaluation criteria about the convenience of investments. When facing uncertainty, intended as the awareness of the surprises that may be produced by unpredictable events, the entrepreneurs’ expectations are ephemeral and volatile. This is the cause of the basic instability of capitalism. Obviously, from this point of view the liquidity-preference theory plays an important role, as, given the impossibility of reducing uncertainty to risk, money is an indispensable insurance instrument in the face of unpredictable events. As such, however, money can also contribute to economic instability, in that liquidity preference and the irrational behaviour of speculators may amplify the depressive effects of uncertainty and the lack of confidence of entrepreneurs. Therefore it is important to study the functions it accomplishes in economic activity, above all the way in which its production and control is organized.

9.5.2. Distributionandgrowth

A great many of the Cambridge post-Keynesian theories were developed in the 1950s and 1960s in opposition to the neoclassical growth models of the Solow-Swan type. The polemic manifested itself first of all in an attack on the marginalist theory of capital and distribution.

However, this part of the debate used as its main reference point the Sraffian theoretical approach rather than the post-Keynesian in its strict sense; and we shall therefore deal with it in Chapter 11.The specific contribution of the post-Keynesians consisted in the formulation of an alternative theory of growth and distribution. This theory can be traced back to the ‘widow’s cruse’ theorem, according to which the incomes earnt by capitalists ultimately depend only on their expenditure. As we saw in Chapter 7, there is a Keynesian and a Kaleckian version of this theorem. The main difference between the two concerns the level of output, which Keynes, in the Treatise, assumed fixed at full employment, while Kalecki maintained it to be at an underemployment level. Post-Keynesian theory was born of the attempt to extend the results of that theorem to a theoretical context in which the level of income grows over time.

The Kaleckian conception was developed especially by Joan Robinson’s in some articles (particularly ‘Normal Prices’ and ‘A Model of Accumulation’) collected together in Essays in the Theory of Economic Growth (1962). In the models of growth with unemployment and under-utilization of plant, the key hypothesis is that prices are fixed by applying the mark-up rule to direct costs, which are assumed constant. This implies that, given the techniques, the distribution of income is determined by the price policies of the firms, and depends on the average degree of monopoly prevailing in the economy. In her later formulations, Robinson tried to reduce the importance attributed to the structure of markets and, by developing some of Kalecki’s suggestions, focused on the role played by trade unions. She then linked the average mark-up, and therefore the distribution of income, to the power relationships among social classes. In any case, in the presence of unemployment the distribution of income turns out to be independent of the levels of output, or its rate of growth.

In the simplifying hypothesis that all wages are consumed, profits will be determined in such a way as to provide the flow of finance necessary to sustain the growth of capital. Therefore, profits depend on investments, while the rate of profit depends on the capital-output ratio and the growth rate of income. If neutral technical progress is assumed, in such a way as to assure a constant capital-output ratio, all that is needed to ‘close’ the model is knowledge of the behaviour of capitalists concerning investments. But this is exactly what the economic theory does not allow us to determine endogenously. Investment decisions depend on the ‘animal spirits’ of the capitalists, a social-psychological variable which has a rather more Marxian than Keynesian flavour. The economy may grow at any rate: it can be an equilibrium rate, or warranted, in the Harrod-Domar sense, but it does not necessarily ensure full employment.Robinson considered growth with full employment as a limiting case which is difficult to obtain in a laissez-faire regime. This limiting case was defined, with a little irony, as the ‘golden age’. A golden-age economy with neutral technical progress would grow in steady state, i.e. all the variables would grow at the same rate, including employment. Full employment would be ensured by a growth rate of income equal to that of the stock of capital, and also equal to the sum of the growth rates of population and labour productivity. The golden-age growth model is ‘closed’. In it, investment decisions are rescued from the volatile moods of the entrepreneurs and are determined endogenously as those which guarantee steadystate growth. Two hypotheses must be made to obtain this result: ‘perfect foresight’ and ‘perfect tranquillity’. The former serves to eliminate uncertainty, the latter ensures that expectations can be formulated correctly. Both can be reduced to the assumption that the economy grows in a steady state. The circular nature of the argument should not be surprising. And this is one of the things that Robinson wished to show: in order to have steady-state growth, the economy must always have grown in a steady state.

Kaldor was less sceptical about the ability of the capitalist economy to grow with full employment. Thus, he made greater efforts than Robinson to account for the proper conditions of steady-state growth. Among his principal contributions to the construction of the post-Keynesian theory of growth and distribution we will recall ‘Alternative Theories of Distribution’ (1956) and ‘A New Model of Economic Growth’, published in 1962 with J. A. Mirlees.

Kaldor preferred the Keynesian to the Kaleckian version of the widow’s- cruse theorem. He believed that, in a process of growth with full employment and full utilization of capacity, it is impossible to separate the problem of income distribution from that of growth, as had occurred in Robinson’s open model. The economy cannot grow, in real terms, more rapidly than the natural rate. Assume that it does not grow less rapidly. Then the growth rate of capital stock is endogenously determined. Assuming there are two classes of income earners—the profits earners and the wage earners—with the former’s propensity to consume lower than that of the latter, the distribution of income must be determined endogenously in such a way as to ensure flows of savings sufficient to finance investments. At any given moment, the higher the investment rate (in relation to income), the higher the profit share will be; and this is so because a higher percentage of profits are saved than of wages, and only a higher profit share is able to guarantee a higher percentage of savings on aggregate income.

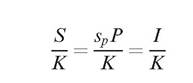

This result is also valid for a growing economy. In an economy which is growing in equilibrium, the growth rate of wealth is equal to that of the capital stock.

s t_

K ¼ K

Under the ‘classical savings hypothesis’, according to which the workers do not save, S = spP, where sp is the propensity to save out of profits. Therefore

from which the famous ‘Cambridge distributive equation’ is obtained:

The rate of profit, r = P/K, only depends on the expenditure decisions of the capitalists, i.e. on their propensity to save and their investment decisions, being gn = I/K = DI/I.

The demonstration that this result does not depend on the restrictive classical savings hypothesis was given by Pasinetti in ‘Rate of Profit and Income Distribution in Relation to the Rate of Growth’ (1962). Let us consider an economy in which there are only two social classes, workers and capitalists. Their propensity to save, sl and sc respectively, is such that 0 < sl < I/Y < sc < 1. Then the workers will also be owners of capital, as they accumulate wealth by savings. Therefore they will earn profits (dividends and interest), besides wages. Pasinetti demonstrated that the savings made by the workers from their wages and their own profits coincide with the reduction in the capitalists’ savings caused by the fact that the capitalists themselves do not receive all the profits. It is as if, by paying the workers part of the profits, the capitalists had partially delegated to them the function of saving. The amount the capitalists save less, the workers save more. Therefore, in regard to the financing of investments it does not matter whether the workers save or not, or whether they receive part of the profits or not. Since the overall amount of savings depends on investments, the distribution of income between wages and profits remains determined by the expenditure decisions of the capitalists, and the Cambridge equation still holds true.

A special feature of the post-Keynesian models of growth, which they share with the Harrod-Domar model, concerns the capital-output ratio, which is a constant. This is not a simplifying hypothesis but, rather, an essential property of these models. In fact, by means of it, any possibility of accounting for the distribution of income on the basis of the marginal productivity of factors is radically eliminated, while a complete alternative to the Solow-Swan type of growth theory is given. Kaldor made the greatest effort to legitimate the assumption of a constant capital-output ratio, and tried to give it an empirical justification as well as a theoretical explanation. From historical observation, Kaldor came to the conclusion that in the course of its evolution capitalist accumulation had been governed by a series of empirical regularities which he defined as ‘stylized facts’. Particularly important are

those relating to the constancy of the wage share and the profit rate, both properties of steady-state growth models. Constancy in the capital-output ratio is also included in his list of stylized facts.

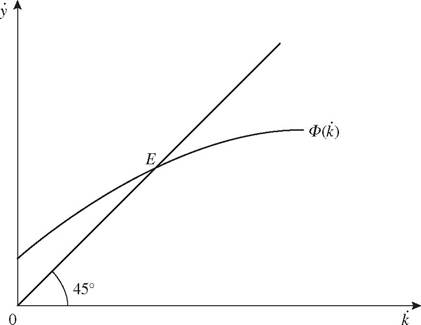

The problem is how to explain these facts. The technical-progress function was invented by Kaldor, in part, to answer this question. The function relates the growth rate of labour productivity, y, with that of the capital-labour ratio, k, and has the form y = F(k). This function is assumed to be increasing at a decreasing rate, as shown in Fig. 14. There is a point at which y and k grow at the same rate and therefore the capital-output ratio is constant; this is point E, where the function cuts the bisector line of the quadrant. The economy tends to stabilize at this point. In fact, if it were to the left of it, production (and aggregate demand) would grow more rapidly than the stock of capital, which would create optimistic profit expectations and would make the capitalists more dynamic. Investments, the stock of capital, and the capital-labour ratio would increase, causing a movement towards the right along the technical-progress function. If, instead, it were to the right of point E, this would mean that aggregate demand was increasing less rapidly than the stock of capital. The capitalists would expect a reduction in the rate of profit and would slow down their investment activity. The economy would again converge towards point E. At this point, not only the capital-output ratio but also the expected rate of profit must be constant (and equal to the actual one). The economy will grow in steady state, and in ‘perfect tranquillity’—as Robinson would say.

We cannot close this section without mentioning another work by Pasinetti, Structural Change and Economic Growth (1981), in which he made an ambitious attempt to integrate the post-Keynesian theory of growth with some theoretical implications of the approaches of Leontief, von Neumann,

and Sraffa. The post-Keynesian growth model was disaggregated in order to account for the evolution of an economy composed of various productive sectors. The population grows at a constant exogenous rate. Productivity also grows at a constant exogenous rate, but this is not uniform over the various sectors. The demand for consumer goods varies according to an Engel’s Law modified to take into account new goods. The economy grows in equilibrium if it is able to ensure two conditions: first of all, productive capacity must grow in each sector to satisfy sectorial demand; second, aggregate demand must grow in such a way as to absorb the investment goods producible over and above the production of consumer goods. An economy obeying these conditions will grow in ‘natural’ equilibrium. But it will be unbalanced growth. The sector profit rates, which are dependent on the production techniques, will not be uniform. Wages, as in other postKeynesian models, remain determined residually.

9.5.3. Money and the instability of the capitalist economy

Even though they can be traced back to the solid tradition of the Radcliffe Report of the Committee on the Working of the Monetary System (London, 1959) and, even more so, to Keynes’s various ideas on the endogenous nature of the money supply, the modern post-Keynesian monetary theories were mainly formulated in the 1970s and the early 1980s. But it is worth noting that one of the first important contribution to the elaborations of these theories was given by Tobin in 1963, and it is to be found in his famous article, ‘Commercial Banks as Creators of Money’, in which he sketched out some fundamental theoretical presuppositions of a theory of endogenous money supply. However, this was only an embryo of a theory, and continued for some time to live its embryonic life. Then the happy event occurred in the early 1970s, the monetarist discovery of the anticipation of money with regard to income acting as the midwife. Friedman’s discovery concerned the fact that the rate of variation of the money supply occurs in cycles similar to those of income, and precede them systematically, even though at variable time-spans. The monetarist explanation was that there is a causal link from money to income—an explanation which, supported as it was by empirical evidence, went on to form one of the main points of the monetarist attack on neo-Keynesian theory.

The post-Keynesian theories, however, not only came out of this debate unscathed but were even strengthened by the monetarist discovery. In fact, a theory that makes the level of income depend on the autonomous decisions of the entrepreneurs is naturally induced to assume that the money supply varies endogenously in relation to the demand for investment finance. From the post-Keynesian point of view, there is a double causal link which moves from investments to the demand for money and from investments to aggregate demand. If the money supply adjusts promptly to demand, then its variations must anticipate those in income, In fact, the Keynesian multiplier transmits the investment impulse to income only after a certain delay. The two most important contributions to emerge from that debate were Kaldor’s ‘The New Monetarism’ (1970) and Tobin’s ‘Money and Income: Post Hoc ergo Propter Hoc?’ (1970).

The theory of the endogenous money supply was brought to extremes by B. J. Moore, who argued that the money supply curve is horizontal because, through the creation of credit, the banking system tends to give the economy all the money it demands without varying interest rates. This concept is further borne out by the theory which holds that the real causal relationship in the bank multiplier process is the reverse of what it is generally thought to be: credit expansion makes the money supply grow by dragging the monetary base upwards.

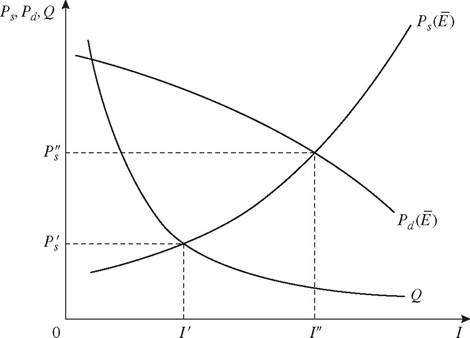

The endogenous nature of the money supply has ambivalent effects on the dynamics of the capitalist economy: on the one hand, it allows for growth in investment to go beyond the immediate capacity of self-financing; on the other, by doing so, it exacerbates the intrinsic instability of a laissez-faire regime, e.g. by creating the conditions for catastrophic financial crises and drastic interruptions in growth. The destabilizing effects the structure of the financial system can have on the real economy have been studied in depth by Minsky in various papers written in the 1970s and collected in Can ‘It' Happen Again? Essays on Instability and Finance (1982). Minsky has recently put forward, besides an original reinterpretation of Keynes as a theorist of financial instability, an interesting theory of the crisis reminiscent of the earliest lessons of Marshall and Fisher. At the centre of his theory is the Keynesian distinction between ‘debtor risk’ or the risk of the entrepreneur, which is that of not realizing his own profit expectations and, therefore, of being unable to repay his debts, and ‘creditor risk’, which is that of being unable to get the loans repaid. With the hypothesis of increasing risk, of Kaleckian origin, Minskyjustified the existence of a decreasing curve for the marginal efficiency of capital, or the demand price of capital. Such a curve, defined over the aggregate of all the firms, and assuming the entrepreneurs’ expectations given at level E, is represented as Pd (E) in Fig. 15. A hypothesis of increasing risk for creditors was used to justify the existence of an increasing curve of supply price of capital, such as PfE). Curve Q is an equilateral hyperbola, and represents the expectations of self-financing at a given moment.

If firms limited themselves to self-financed investments, these would be fixed at level I', where the supply price, P's, is equal to what can be paid by resorting to internal finance. But the demand price is higher; therefore, the firms are induced to expand the investments by running into debt. At the I'' level of investments the firms will run up debts to obtain an amount of finance equal to P"I'' — P'sI'. During phases of economic expansion, the state of confidence of capitalists improves, E will increase, and the curves Pd(E) and Ps(E) will shift to the right. This will heighten investments, but also

Fig. 15

the indebtedness and financial burdens of the firms. Thus, as the boom progresses, the financial fragility of the system mounts. Financial fragility can be measured in terms of the ratio between indebtedness and income produced by firms. It swells in a boom, when the risk increases of the need to refinance a rising volume of long-term indebtedness with short-term debt. Then the expectations of a downturn in the business cycle are sufficient to cause a financial crisis. Given the high level of indebtedness and the concatenation of the debts of firms, both industrial and financial, any attempt of one of them to reinforce its own liquidity position by reducing expenditure will reflect negatively on the other firms. Besides this, any attempt to make the portfolios more liquid will increase the supply of long-term financial assets and thus lower their value. This will raise the cost of finance and give the economy further deflationary impulses. The consequences will be catastrophic: cumulative processes of reduction in investments, in income, and in the availability of internal finance, possibly accompanied by chain bankruptcies and financial crashes. So a slight downturn in the real economic cycle, even if expected, can cause a collapse. This, in Minsky’s social philosophy, should justify the adoption of cautious monetary management policies, which is exactly the opposite to what demanded by the monetarists. And, in this view, if a crisis such as that of 1929 has never occurred since, the credit is due to the adoption of Keynesian-type monetary policies by the governments of the principal capitalist countries.

9.5.4. Heterodox microfoundations of macroeconomics

With the works of Bain, Sylos-Labini, Eichner and others, post-Keynesians have made very innovative contributions to the theory of the firm which we

shall, however, deal with in the following chapter. Here it is necessary to show how those contributions microfound the macroeconomy on radically different bases from neoclassical ones and consequently justify economic policy views that are at variance with the neo-Keynesian, monetarist and neo-monetarist stances.

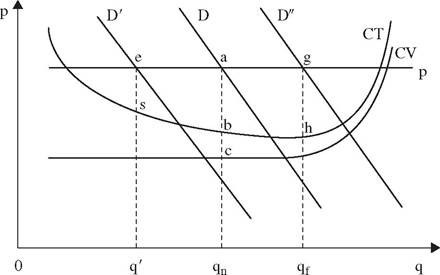

By developing the ideas put forward by Kalecki and Kahn, postKeynesians assumed that the variable cost curve of a business is flat until all plants are fully utilized. This theory is substantiated by empirical research which, beginning with an important work by P. W. S. Andrews of 1949, Manufacturing Business, had shown that the average and marginal cost curves of a firm are typically basin-shaped rather than U-shaped. Average and marginal costs are constant in the normal operation range of the business. In addition, again following in Kalecki’s wake, post-Keynesians assumed that prices are fixed by applying the mark-up rule. This theory has also been checked empirically, research in this field having been prompted by the fundamental work of Robert Hall and Charles Hitch, Price Theory and Business Behaviour, dated 1939. In its simplest version, the mark-up rule consists in determining the price, p, by applying a gross profit margin, μ, to variable costs, CV, in accordance with the formula p = CV(1 + μ). The gross margin is calculated so as to ensure a normal profit in the long run and to cover fixed costs when plant and machinery are exploited at normal level (roughly, two thirds of full capacity). When firms make investments, they consciously build up surplus capacity to be able to cope with increases in demand that arise in periods of prosperity. It follows that plant and machinery are systematically under-utilized in normal periods.

In Fig. 16, CV is the average variable cost curve and CT that of average total costs. The level of normal utilization corresponds to production qn, while qf is the quantity produced when the plant is fully exploited. With demand curve D the firm produces quantity qn and sells it at price p.

The gross average profit is represented by the segment a-c, net profit by the segment a-b and fixed costs by segment b-c. During a recession, the demand curve shifts towards D'. The firm does not lower its price, but reduces production to level q'. In this way average net profits are reduced to segment e-s. When the demand curve shifts towards D00, the firm will increase production, while average profits will grow up to the level g-h.

Businessmen know that the economy is subject to systematic, albeit unforeseeable, fluctuations. That is why they provide for surplus capacity. Investment decisions are made in a long-run perspective with the expectation of earning a normal profit on average. When the demand falls or increases, firms do not substantially alter their prices for two reasons: to avoid spoiling the market by betraying their customers’ expectations and to avoid triggering dangerous price wars with competitors. They are therefore content to earn less during recessions, relying on being able to make up for their losses during boom periods. As W. A. H. Godley and W. D. Nordhaus showed, the macroeconomic effects envisaged in this theory are widely borne out by empirical data.

Prices tend to rise only when there are generalized cost increases. At macroeconomic level, all variable costs are taken to be reducible to labour costs (which is admissible for a closed economy) and the price level, P, is determined by a simple formula put forward by S. Weintraub, P = (1 + μ)w∕y, where w is the average monetary wage and y average labour productivity. If the mark-up does not change, a pure cost inflation theory is obtained. The inflation rate will be defined as the difference between the growth rate of wages and that of productivity.

Others, following Kalecki, maintain that inflation is determined by the distributive conflict. In periods of strong expansion, the reduction in unemployment strengthens workers’ unions which then succeed in carrying off substantial increases in real wages. If these exceed the growth in productivity, an inflationary spiral is triggered in which the mark-up may be reduced. Thus class conflict, through inflation, may succeed in raising the wage share of the national income. The inflationary surges seen in periods of economic growth are explained not by increase in demand, but by exacerbation of the distributive conflict. Post-Keynesians in fact reject both the short-run and the long-run Phillips curve. A theory of this kind was formulated by R. Rowthorn.

The aggregate supply curve that emerges from the post-Keynesian approach is horizontal, as we shall see in section 9.6.4. This leads to conclusions diametrically opposed to those of the monetarists and neomonetarists: a contraction of aggregate demand gives rise to a fall-off in production and employment, without prompting automatic adjustment processes to restore the economy to full employment. An increase in demand has the opposite effect. And this fully justifies the adoption of Keynesian type expansive fiscal policies. If economic growth were to generate inflation by setting the distributive conflict in motion, the government should not react by curbing expansion, because in doing so it would prompt a recession. The cure for inflation, according to post-Keynesians, should not entail regulating aggregate demand. Instead, it should take the form of an incomes policy, aimed at convincing the social parts to moderate their distributive claims so as to render them more compatible with each other.

9.6.

More on the topic The Post-Keynesian Approach:

- 15 Demand for Money: The Post-Keynesian Approach

- Bibliography

- The New Keynesian Macroeconomics

- PREFACE TO THE SECOND ENGLISH EDITION

- Agarwal Vanita. Macroeconomics: Theory & Policy. Pearson,2010. — 408 p., 2010

- Index of Subjects

- Relevant Works

- Bibliography

- The Controversy on Marginalism in the Theory of the Firm and Markets

- 1 An Introduction to Macroeconomics