From Disequilibrium to Non-Walrasian Equilibrium

9.4.1. Disequilibrium and the microfoundations of macroeconomics

In the 1960s it had become almost universally clear (except to the authors of textbooks) that the Walrasian equilibrium model was not able to do justice to Keynes.

Already in 1956, Patinkin, in a book which presented a theoretical summa of the neoclassical synthesis, Money, Interest and Prices, had suggested that, as there was no space for Keynes in the general-equilibrium model, it was necessary to study disequilibrium situations to account for Keynesian problems. This suggestion was taken up by two economists who, though still following the neoclassical approach, in various articles published during the 1960s launched a powerful attack against the IS-LM model. Their intention was to search for the microeconomic foundations of Keynesian macroeconomics in the dynamics of disequilibrium. The economists in question are Robert Wayne Clower and Axel Leijonhufvud.Clower simply proposed to remove from the Walrasian approach the idea that exchanges are made in equilibrium. In equilibrium, all decisions of individuals are realized in such a way that they are compatible with each other. For this reason, ‘planned’ (or ‘notional’) demand coincides with actual demand. This correspondence disappears outside equilibrium. If the prices do not clear the markets, the individuals will not be able to buy or sell their planned quantities. In this way, the actual demand will be constrained by the monetary incomes actually realized. If the latter do not allow purchase of the quantities desired, expenditure plans must be revised. Thus, a type of ‘decisional dualism’ occurs. On the other hand, all transactions occur with the use of money, and this allows a clear separation between the decisions concerning the goods to demand and the goods to supply. Thus, instead of the traditional budget constraint which, in equilibrium, implies that the value of the supply of services must equal that of the demand for goods, the economic agent who operates in disequilibrium must be subjected to two different constraints.

The first is an expenditure constraint which requires that the purchases are sustained by monetary balances; the second is an income constraint, and implies that the accumulation of liquid balances is limited by the ability to generate an income by means of the sale of goods and services. Thus, the workers who do not succeed in selling all the labour services they wish may also be unable to buy all the consumer goods they would like. The firms will not then be able to sell all the goods produced. In this way, the initial excess demand can be transmitted through the whole economy by means of a multiplier process similar to that conceived by Keynes.Leijonhufvud held a similar position to that of Clower; however he insisted that the multiplier process was essentially a phenomenon of illiquidity, i.e. a process generated by the lack of liquidity (with respect to the desired balances) occurring when exchanges take place outside equilibrium. Besides this, he emphasized the role played by informative deficiencies as generating factors of the multiplication processes. This last point is important. Clower was not clear about one crucial question: whether rejection of the Walrasian model implied the abandonment of the auctioneer or tatonnement or even Walras’s Law. Leijonhufvud, by focusing on the lack of information generated by prices different from those in force in the Walrasian equilibrium, identified the key element in this theoretical approach and cleared the way for the models of non-Walrasian equilibrium formulated in the 1970s. The point is that it is not tatonnement that must be abandoned, but the auctioneer.

Before describing this type of model, however, we should mention another type of non-Walrasian modelling which was also developed in the 1960s: that of the ‘non-tatonnement processes’. We should not speak of it in this section, as it has nothing to do with any kind of Keynesian matter; but it is useful to do so, if for no other reason than to prepare the field for a comparison.

In the non-tatonnement processes, in fact, exactly the opposite happens to what occurs in non-Walrasian models of equilibrium, of which we will speak in the next section: tatonnement disappears but the auctioneer survives. The origin of this approach goes back to two works by Frank Hahn and Takashi Negishi. The model, originally formulated with reference to a pure exchange economy, was later extended to a production economy by F. Fisher.In this model the economic agents are price-takers; and the prices are fixed by an auctioneer. However, exchanges can also be undertaken at prices that do not clear the markets. Therefore, some agents may be rationed. After each exchange the auctioneer will calculate new prices; and on the basis of these the agents will take further decisions and undertake further exchanges. The economy moves through a sequence of periods. The data on the basis of which decisions are taken in one period (in particular, the individual endowments of goods) depend on exchanges undertaken in the preceding period. Therefore, the equilibrium to which this sequential economy leads will generally be different from the Walrasian equilibrium. In fact, the latter depends exclusively on the initial data, and is not influenced by the process by which equilibrium is reached.

9.4.2. The non-Walrasian equilibrium models

In the Walrasian models the economic agents are price-takers both in equilibrium and in disequilibrium. Even at disequilibrium prices they continue to ignore any possible quantitative constraint on their own decisions, as they undertake exchanges only when equilibrium prices have been reached. On the other hand, prices are perfectly flexible: they are not set by any single economic agent, but are called by the auctioneer, who decides on them by observing the excesses of demand. Thus the agents are able to use prices ‘parametrically’, whether they are correct or mistaken. Only they continue to revise their own decisions until they reach the correct prices, i.e.

those in force in equilibrium. The auctioneer, for his part, continues to modify the prices until all excess demand has been eliminated. Therefore the Walrasian equilibrium is an equilibrium, both in the sense that all excess demand has vanished in correspondence to a level of output that ensures the full utilization of resources, and in the sense that the economic agents are not induced to change their own decisions, so that there are no forces capable of modifying the equilibrium situation.A ‘non-Walrasian equilibrium’, instead, is a state in which, although part of the resources remain unutilized, there may be no stimuli to induce agents to change their decisions. It is an equilibrium only in the sense that the economy, once it has reached that state, is not pushed away from it, or, rather, in the sense that individuals have realized, in a certain sense, their own plans. An equilibrium of this type can be reached in a theoretical context in which some basic hypotheses of the Walrasian equilibrium are abandoned, especially that dealing with price flexibility. The theory which follows from this can be called the theory of ‘non-Walrasian equilibrium’ or ‘equilibrium with rationing’; but some people continue to call it the theory of ‘disequilibrium’, and others the theory of the ‘K-equilibrium’.

The most interesting models of this approach were formulated in the 1970s as a development of the contributions of Patinkin, Clower, and Leijonhufvud, and are due to Robert J. Barro, Herschel I. Grossman, JeanPascal Benassy, Jean-Michel Grandmont, Jaques H. J. M. E. Dreze, and Edmond Malinvaud.

Here we do not have room to deal with the internal evolution of the theory, which would have been interesting as only in the most recent work has it become clear that we are actually dealing with a theory of equilibrium. Nor have we time to dwell upon the marked differences between the models of the various authors. We will limit ourselves to presenting the maximum common denominator.

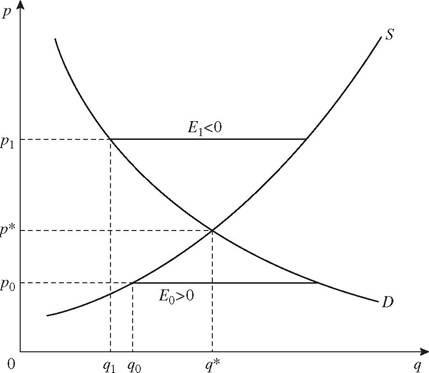

Fig. 13 shows the curves of demand, D, and supply, S, of one commodity. The Walrasian equilibrium price isp*. At pricep0 there is an excess demand E0 > 0: the scissors have a ‘long side’, in this case the demand, and a ‘short side’, the supply. The short side is that in which the sum of the desired transactions is smaller. Thus at price p1 the excess demand is negative, E1 < 0, and the short side is that of demand. q0 and q1 are the ‘effective’ supply and demand in the two cases; q* is the ‘notional’ demand.Two hypotheses are made to define the method of exchange. The first is the hypothesis of voluntary exchange, which states that no agent is forced to

Fig. 13

exchange more than he wishes. The second is the hypothesis of ordered markets, or frictionless markets, according to which there can only be a discrepancy between desired and realized transactions for the agents who are on one of the two sides of the market. The ‘short-side rule’, derived from these two hypotheses, states that only the agents who are on the short side of the market succeed in realizing their plans. The agents unable to realize their own exchange plans are rationed. In a situation of excess supply, the sellers are rationed; in one of excess demand, the buyers are. The rationed agents are subject to quantitative constraints. Therefore, it is legitimate to assume that in the formulation of their own plans, they take into account the information concerning quantities as well as prices. A hypothesis made in Benassy-type versions is that the agents, in order to decide about the supply or the demand to present on a market, take into consideration the quantitative constraints perceived on some other markets. So the worker, in deciding on the quantity of consumer goods to buy, will take into account the quantity of labour he actually sells.

On the other hand, the entrepreneur will decide on the labour demand taking into consideration the quantity of goods he actually sells. In the Dreze-type versions, instead, the agents take into consideration the constraints perceived on all the markets. Now, if the prices at which the exchanges are undertaken are those determined by the Walrasian equilibrium, nobody would undergo quantitative constraints. However, if the prices are different, quantitative constraints will arise on all markets.The key hypothesis of the non-Walrasian equilibrium models is that prices, or at least some of them, are fixed. It is basically for this reason that price and quantity signals enter into the functions of supply and demand. An equilibrium can be reached on the basis of such demand functions, but it is an unusual equilibrium. In it the subjects are not induced to modify their own decisions, for example by considering new or better possibilities of exchange, not because these do not exist, but because the perceived constraints induce them to believe they do not exist. Thus it is possible that unemployed workers convince themselves that there is no demand for labour, not even potentially, which is adequate to their own supply. They accept as permanent the income earned as unemployed or underemployed, and adjust their consumption demand to such incomes. The entrepreneurs, in turn, may think that the demand for goods determined in this way is normal, and therefore adjust the production and the labour demand to it. In this way the entrepreneurs justify the pessimistic evaluations of the workers, who, in turn, justify those of the entrepreneurs. A non-Walrasian equilibrium is a situation in which the ‘effective’ supply and demand formulated by economic agents, on the basis of price and quantity signals observed on the markets, are compatible. The demand is equal to the supply, but different from the ‘notional’ or ‘potential’ supply and demand, i.e. those that would be realized in a Walrasian equilibrium. On the other hand, the plans of the economic agents are actually fulfilled in a non-Walrasian equilibrium, and therefore there is no stimulus to modify them.

The particular kind of equilibrium which is reached will then depend on the particular hypotheses about which prices are fixed, which markets generate the quantitative constraints, and which agents are rationed. In this way, it is possible to have equilibria with ‘Keynesian unemployment’, in which both the prices of consumer goods and the money wages are fixed, and in which consumers are rationed on the labour market and firms on the goods markets. On the other hand, there are disequilibria with ‘classical unemployment’ when the real wages are ‘too high’ to guarantee full employment; in this case, while firms are rationed neither on the goods nor labour market, workers are rationed on both. There is also a particular type of equilibrium which seems able to account for the specific case considered by Keynes in the General Theory—that in which there are flexible prices for goods and rigid money wages. In this case, firms are not rationed on the goods markets, since prices are flexible. However, because of the unemployment generated by fixed money wages, the workers will be rationed on the labour market. And the ‘Keynesian case’ would be reduced to this. Is it not paradoxical that this was the fate of a line of research which originated from dissatisfaction with the neoclassical synthesis?

A strange destiny had awaited the neoclassical interpretations of Keynes. Beginning with the attempt to demonstrate that Keynes had studied a special case in which prices and/or wages are rigid, the neoclassicists created growing dissatisfaction among Keynesian economists and, through an incessant flow of polemics and counter-revolutions, they finally produced an evolution in thought which ended up by demonstrating that Keynes’s case is precisely that in which prices and/or wages are rigid. The difference between the departure-point, the neoclassical synthesis, and the destination, equilibrium models with rationing, is that, in the former, Keynes was reinterpreted as a case of temporary Walrasian equilibrium, in the latter, as a case of temporary non-Walrasian equilibrium—a difference which is less remarkable than it first appears. On the other hand, in both cases, there are devastating repercussions for Keynes’s general theory: as such, it simply does not exist.

9.5.