The Monetarist Counter-Revolution

9.3.1. Act I: money matters

While the neoclassical synthesis was being built at the Massachusetts Institute of Technology, Yale, and Harvard, Milton Friedman, at the University of Chicago, was working on his personal reconstruction of the neoclassical system.

The monetarist theory, as Friedman’s reworking of the traditional quantity theory of money was to be called, progressed at the same time as the neoclassical synthesis and grew, apparently, in conflict with it, as it presented itself as a criticism of Keynes’s economics, while the neoclassical economists of MIT were proclaiming themselves as ‘neo-Keynesian’. The monetarist counter-revolution began in 1956, when Friedman published ‘The Quantity Theory of Money: A Restatement’. This famous article was followed by other important works, later collected in The Optimum Quantity of Money (1969), which contains the foundations of monetarist theory.Friedman argued that the quantity theory had to be interpreted as a theory of demand for money and not as a simple explanation of the price-level. Only with the addition of specific hypotheses in regard to the supply conditions (of money and real goods) would it have been possible to use that approach to explain the price-level. He then reformulated the theory of money demand, taking into account the advances made by modern research. After various refinements, he proposed a model not dissimilar to those based on portfolio choices. He included among the arguments of the money demand function the interest rates on bonds and shares and the inflation rate (interpreted as a negative rate of returns on liquid assets), as well as wealth and other structural and institutional variables. This function contains nothing substantially new in comparison to the one used by the Keynesian neoclassical economists, and can be easily manipulated, as occurs when it is used in empirical research, in such a way as to transform it into a demand function which is only dependent on interest rate and level of income.

Friedman was convinced, even more than the Keynesian neoclassical economists, that this function is extremely stable.In a 1963 article written in collaboration with D. Meiselman, ‘The Relative Stability of Monetary Velocity and the Investment Multiplier in the United States, 1897-1958’, Friedman again presented the argument of the stability of the money demand function under the form of a hypothesis on the stability (and the magnitude) of the velocity of money circulation, which he renamed the ‘monetary multiplier’. He coupled this with a hypothesis on the income multiplier, which he maintained to be lower and more unstable than the monetary multiplier. He justified this hypothesis with a permanent-income theory of the consumption function. As consumption depends on permanent income, and therefore on the incomes received in past years besides that of the current year, the propensity to consume calculated on current income is lower than that calculated on permanent income. Moreover, current income always contains a transitory component which is random and extremely variable. Therefore the propensity to consume, and the Keynesian multiplier, are not only low but change markedly in response to changes in income-level. The conclusion was simple: impulses from fiscal policy, which act on the economy through the Keynesian multiplier, are less effective than monetary stimuli, which work through the monetary multiplier.

This conclusion was reinforced by the so-called ‘crowding-out thesis’, a modern reformulation of the traditional ‘treasury view’, which Keynes had fiercely fought against. Given the money supply, an increase in public spending financed by borrowing will raise the rate of interest, and consequently ‘crowd out’ private investments, so that aggregate demand will not increase. On the contrary, given public spending, a rise in the money supply will increase incomes, without raising the rate of interest: money matters. The extreme argument about crowding-out requires a vertical LM curve, but, generally, an LM curve which is steeper than the IS curve is enough to be able to conclude that money is more important than real stimuli.

However, Friedman did not derive from this argument the conclusion that discretionary monetary policy is advisable. In fact, in a monumental investigation carried out in collaboration with A. J. Schwartz, A Monetary History of the United States, 1861-1960 (1963), he believed he had demonstrated that the influence of the money supply is strong but irregular, the delay occurring between the monetary impulse and the real effects being long and variable. This means that, even though money is able to disturb the real economy, owing to the unpredictable nature of its real effects nobody would be able to use it as an instrument of discretionary policy. The best thing to do, for the monetary authorities, would therefore be to increase the money supply at the rhythm required by long-run real growth and to leave the market with the job of dealing with short-run adjustments.

9.3.2. Act II: ‘you can't fool all the people all the time'

The decisive blow against Keynesian neoclassical economics was struck, at the end of the 1960s, in two articles that attacked the theory underlying the Phillips curve: one by E. S. Phelps, ‘Phillips Curve: Expectations of Inflation and Optimal Unemployment over Time’ (1967) and one by Friedman, ‘The Role of Monetary Policy’ (1968). It was pointed out that, if the Phillips curve is interpreted in terms of the laws of supply and demand, and if agents are assumed to be rational, then the rate of unemployment should not be related to the variations in money wage, but to the variations in real wages. The growth rate of the real wage is given by the difference between the growth rate of the money wage and the expected rate of inflation. Given certain inflationary expectations, the monetary authorities are able to reduce the level of unemployment only if they increase the money supply in such a way as to generate an inflation rate which is greater than the expected one. Thus the entrepreneurs believe in a reduction in the real wage and increase the demand for labour.

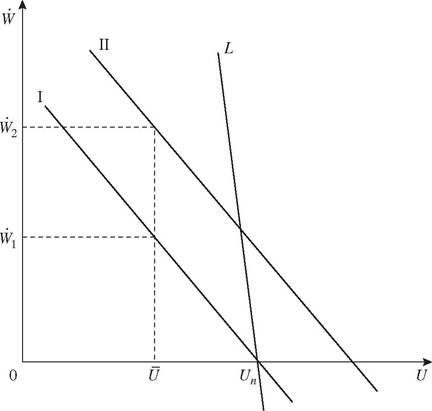

The money wage will increase, and the workers, given the inflationary expectations, increase the labour supply.A simple linear ‘short-run Phillips curve’ will be:

W = βPe - μ(U - Un)

where VV is the growth rate of money wages, Pe the expected rate of inflation, U the rate of unemployment, and Un its ‘natural’ level, the latter depending

on the preferences of the economic agents and on technology. In correspondence to given inflationary expectations, for example, Pe0 = 0 the short run Phillips curve will be negatively sloped, like curve I in Fig. 12. In order to obtain a level of unemployment such as U the money supply must increase in such a way that wages (and prices) rise at rate W1. However, individuals are not fooled for long. When they realize that the prices have risen, they will raise their expectations, for example to P1e > Fξ = 0. Now, if the wages continue to increase at rate W1, the workers will reduce the supply of labour, so that, in Fig. 12, there will be a horizontal shift towards Un. To maintain the unemployment at level U, the monetary authorities must increase the monetary supply even more than before, so as to generate an inflation rate equal to F2 >F 1e.

This will again fool the economic agents and cause a movement towards the left along curve II (corresponding to expectations F1e). In conclusion, to continue to fool the economic agents the authorities must trigger and maintain an accelerated inflation process. This is the so-called ‘accelerationist hypothesis’. In the presence of any rate of inflation, provided that it is constant and therefore known to the economic agents, nobody is fooled, and the economy will stabilize at the natural rate of unemployment, Un. In the long run there is no decreasing function between unemployment and the growth rate of money wages.

Or, in any case, it is an extremely weak relationship. With the ‘long-run Phillips curve’, the expected rate of inflation coincides with the actual one, and the curve itself will be more or less vertical, like the L curve in Fig. 12.

The long-run Phillips curve is obtained from the above formula when W = P = Pe, where P is the actual rate of inflation. Then:

from which it can be seen that the curve is vertical, i.e. U = Un, if β = 1.

In this case the monetary policy is completely ineffective as a fullemployment policy and has only inflationary effects. If, however, β < 1, the long-run Phillips curve is sloped, even if less than the short-run curve. β is the ‘expectation coefficient’, and expresses the degree to which the actual rate of inflation depends on the expected rate. The neo-Keynesian economists argued that depends on the size of monetary illusion: the stronger it is, the lower β will be. The difference between the Keynesian neoclassical and the monetarist neoclassical economists thus hinges on the size of β, the former wishing it to be low, the latter near to 1.

The various arguments put forward by Friedman against the Keynesian neoclassical system have always caused heated debates, as if they had been heresies. This may seem strange if one thinks that Friedman has accepted all the theoretical foundations of the neoclassical synthesis, from the consumption function to the money demand function, from the practical importance of wealth effects to the theoretical importance of price flexibility, from acceptance of the IS-LM model to allegiance to generalequilibrium theory. In effect, Friedman simply limited himself to drawing out the extreme logical consequences from the premisses of the neoclassical synthesis.

The apparent reasons for dissent mainly concern certain hypotheses about the size of some economic parameters, such as the propensity to consume, the money velocity of circulation, and the expectation coefficient. The real disagreement, though, was mainly about the consequences of economic policy that could be drawn from the sizes of those parameters. One is almost tempted to believe Friedman when he said that all differences of opinion could be resolved by empirical research. But empirical research has never been able to resolve policy differences of this type.How is it possible, then, to explain that towards the beginning of the 1970s monetarism finally broke through, suddenly conquering an unexpected hegemony, or almost? The reason is basically political. On the one hand, the stagflation of those years seemed to prove the monetarists right, especially in their insistence on putting the politicians on guard against the inflationary effects of Keynesian policies. Furthermore, with the accelerationist hypothesis, they called for the necessity of a long period of stagnation to reduce inflation. The monetarists, on the other hand, offered a simple remedy for all problems: block monetary expansion and deflate the economy. And this was welcomed not only by the simple-minded politicians but also by the shrewdest, such as those who, for example, while not

believing the monetarist argument that the trade unions were not responsible for inflation, thought that monetarist policies could at least serve to teach them a lesson.

9.3.3. Act III: the students go beyond the master

The triumph of monetarism was short-lived: Milton Friedman had just conquered the field, after more than fifteen years of struggle, when he was immediately swept away by ‘neomonetarism’. ‘Neomonetarism’ is perhaps the most appropriate term to define that school of thought which most call, exaggerating a little, the ‘new classical macroeconomics’. This school, which came to the fore towards the end of the 1970s, was explicitly and directly linked to the traditional monetarist school; but it differed from it in several respects, especially in the greater refinement of its theoretical and methodological position, but also for being more extreme, if possible, in regard to economic policy. The main exponents of this school are Robert E. Lucas Jr, Thomas J. Sargent, and Neil Wallace.

Monetarism showed its greatest weakness precisely on those subjects with which it seemed to have routed the field. The recognition of the existence of a short-run Phillips curve had, in fact, reinforced the position of those neo-Keynesians for whom economic policy served to ‘fine-tune’ the economy in the short run. Moreover, the admission of the possible existence of a negatively sloped, long-run Phillips curve had demonstrated that Keynesian policies could also have lasting effects, albeit not particularly dramatic. At the political and empirical level, therefore, the differences did not seem so great. On the theoretical level, however, Friedman had made a short step forward with respect to the neoclassical synthesis when he stressed the role played by expectations in the frustration of economic policy. As already mentioned, the IS-LM model, interpreted as a temporary generalequilibrium model, was adopted both by the Keynesian neoclassical economists and by the monetarists. In a temporary general-equilibrium model, if futures markets are not open for all goods, the only way to account for the influence of the future on current transactions is to introduce expectations about the prices of the goods available in the future. This is what Friedman did by introducing inflationary expectations. These are expectations about the future price of those consumer goods for which there are no futures markets. Friedman, however, following Phillip Cagan, assumed ‘adaptive expectations’, a kind of expectation formed in a rather mechanical way by extrapolating from past experience. This assumption not only did not have a solid theoretical justification but was also the main reason for the expectation coefficient of the Phillips curve being different from 1; or, in other words, for the possibility that economic agents let themselves be systematically fooled. In fact, adaptive expectations can give rise to systematic prediction errors.

Lucas avoided this difficulty with one jump, by adopting the ‘rational- expectations’ hypothesis—a hypothesis which had already been formulated in 1961 by John Fraser Muth in a famous article published in Econometrica and entitled ‘Rational Expectations and the Theory of Price Movements’. The main problem with adaptive expectations is that they are unable to deal with all the available information in a rational way. For example, as the formation process of adaptive expectations only takes into account past experience, the agent who follows it will ignore the announcements and the future effects of current economic-policy choices. In order to take into account these and other phenomena relevant to the decisions, the agents should reason by making use of the ‘correct’ economic theory. Rational expectations are formed on the basis of knowledge of all available information, and are elaborated by means of the ‘correct’ economic model. The ‘correct’ economic model is, obviously, the one accepted by Lucas. Being ‘correct’, it allows for the determination of the ‘true’ equilibrium values of the economic variables. So the hypothesis of rational expectations is basically the same as that of ‘perfect foresight’, the only difference being that it allows for stochastic disturbances—a significant difference, but not decisive from a theoretical point of view. Rational expectations do not eliminate every possible prediction error, but only admit random errors. The predictions based on rational expectations are ‘true’ only ‘on average’.

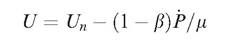

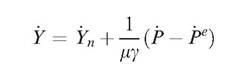

The neomonetarists took up Friedman’s hypothesis of the natural rate of unemployment and reformulated it, transforming the Phillips curve into an ‘aggregate supply function’. To do this they used ‘Okun’s law’, which postulates the existence of a decreasing function linking the unemployment rate and the difference between the growth rate of the national income and its trend. They reformulated this law in such a way as to obtain the equation (U — Un) = — g(Y — Yn). Here Yn is the ‘natural’ growth rate of income, i.e. the one which guarantees ‘natural’ unemployment. By substituting this equation into that of the Phillips curve (p. 337), and assuming and P = W and b = 1, we have:

from which it is easy to see that, if expectations are rational, then P = Pe and income will grow at the natural rate. Unemployment will also stabilize at its natural rate. There will be no short-run Phillips curve, while the long-run one will be vertical. This means that any systematic expansive economic policy is doomed to failure. If the monetary authorities announce their decisions, or if, while not announcing them, they take them by following a model which is known to the economic agents, the latter will immediately foresee the effects of the policy and will not let themselves be fooled. In this way they will condemn it to ineffectiveness.

How is it possible, then, to explain cyclical oscillations? Not by price rigidity and market imperfections, as the Keynesian neoclassical economists maintained. The neomonetarists assumed that prices are capable of clearing the markets at any moment, i.e. that they are perfectly flexible equilibrium prices. Then there is only one possibility left. Random shocks are not predictable, nor are non-systematic economic policies. Therefore surprises can occur in the short run, and P may not equal Pe. But for this to occur it is necessary to assume that information is not perfect; and this is what the neomonetarists did with the so-called ‘islands hypothesis’, already put forward by Phelps. Economic agents work in ‘local’ markets that are separated from each other, as if they were islands. The first information the agents acquire concerns their specific markets. If they interpret it as being specific to these markets, when it is not, they are fooled, at least temporarily. For example, an unexpected political decision with inflationary effects will cause a general increase in prices. Each entrepreneur will observe the increase in price of his own product. If he interprets it as an increase limited to his own market, he will believe that it is a change in relative rather than absolute prices, and will be induced to increase production. However, when all prices have increased, he will realize that he has been fooled and therefore will return production to its ‘natural’ level. Thus, economic policy can be effective in the short run, but only if it is unsystematic and unpredictable.

From this point of view, economic fluctuations are generated by unexpected exogenous shocks and are based on incomplete information. A criticism levelled against this conception is that it is only able to account for short and chaotic movements of the economic variables and not for a business cycle. In the real world the cycle is characterized by a succession of phases of various lengths in which different variables, production, employment, wages, etc. undergo fairly marked ‘co-movements’, i.e. they evolve through time, maintaining a strong correlation. This is the ‘persistence problem’. Lucas has replied to this type of criticism in two ways. He has suggested that the ‘islands’ on which the economic agents operate may be so far away from each other as to require a certain time lapse to fill the information gaps. And he has maintained that there are certain economic mechanisms, of the accelerator type for example, which tend to prolong the effects of exogenous shocks.

It was from this kind of problems that the literature on the ‘real business cycle’ arose, a literature which has flourished in the 1980s. Here we will limit ourselves to mentioning the two contributions which made the breakthrough and laid the ground for this line of research: ‘Time to Build and Aggregate Fluctuations’ (1982), by F. Kydland and E. C. Prescott, and ‘Real Business Cycles’ (1983), by J. B. Long and C. I. Plosser. These theories preserve two fundamental hypotheses of the neomonetarist approach: economic agents with rational expectations and markets in equilibrium at each moment. However, they focus on real rather than monetary shocks as the principal factors of cyclical movements, especially on those connected with the changes in the productivity of factors and in public expenditure. An increase in productivity raises the income of the factors and, given the inputs, the level of production, whereas an increase in public expenditure raises aggregate demand and wages on the one hand and interest rate and savings on the other. In boom phases there is an increase in the labour supply, but it is not caused by an increase in wages induced by excess demand. Wages, according to this line of thought, always coincide with the marginal productivity of labour, while the supply and demand of the services of all the factors equal each other at each moment. The main reason for the ‘co-movements’ of wages-employment-production is the rationality of workers’ behaviour. Workers plan the supply of their own factor over a fairly long period, let us say one to two years. Therefore, as they are able to predict the future evolution of incomes, they tend to work more when wages are higher and less when they are lower. And the main reason for the persistence of the effects of exogenous shocks is this phenomenon of inter-temporal substitution of leisure.

9.3.4. Was it real glory?

Right from its birth and increasingly so as it acquired an audience, the new classical macroeconomics has been inundated with criticisms. Today all its weak points are known. Here we will list those which seem to us to be the most decisive. We will just note its ability to ignore constant attacks from empirical research: not all theoretical economists take a great deal of notice of such defects, and many believe that this is not an irremediable type of defect, as empirical research is incessant and there are almost no limits to what can be asked and obtained from it. The theoretical difficulties, however, are much more serious.

There are problems above all with the notion of rationality of expectations. In neomonetarist theory this concept is basically used to reduce to a calculable risk those effects that an unpredictable future may cause in the present, and which Keynes defined in terms of uncertainty. The new classical economists have simply denied the existence of this problem by assuming that economic subjects are able to consider in their own calculations the whole range of possible events. In other words, they assume that no ‘residual uncertainty’ can exist, an assumption which is certainly difficult to swallow.

Another important problem concerns the hypothesis of stationarity of the equilibrium towards which the economy made up of rational economic agents converges. The theoretical model on which rational expectations are formed must represent an economy with a fairly persistent structure. Only in this case will individuals be justified in forming expectations on the basis of an estimate of ‘fundamental’ variables. Furthermore, it is necessary to hypothesize that there is one and only one correct model of the economy. This is a much less obvious hypothesis than it may seem at first sight. If the type of equilibrium to which the economy should converge itself depends on expectations, there will be not one but many rational-expectation equilibria, one for every expectation which is capable of self-fulfilment. There could even be a continuum of different theories; and the economic agents could use these to formulate their own predictions without being compelled to change their minds by the events caused by their actions.

Furthermore, rational-expectation models run up against serious problems of dynamic instability. In regard to this, the neomonetarists cannot behave in the same way as Friedman, simply assuming that the economy is always regulated by equilibrium prices and boldly ignoring disequilibrium dynamics and the connected problems of stability. This is because, besides the usual dynamic problems posed by the traditional Walrasian equilibrium model, other more specific problems arise when rational expectations are introduced. For example, the solutions of many rational-expectation models are of a ‘saddle-point’ type: there are an infinite number of paths that tend to lead the economy away from equilibrium and only one that brings it back. The neomonetarists were not frightened by this difficulty, and simply went ahead maintaining that the economy, whatever shock it may suffer, is always and instantaneously able to bring itself back onto that single, stable path. But a convincing justification for this way of reasoning has never been given.

A further problem of stability may arise when the process of expectation formation is described in terms of learning from errors. If the equilibrium towards which the economy should move itself depends on the expectations, it is possible that the changes in expectations generated by correction of errors may cause the equilibria to change explosively. Finally, the application of the rational-expectation hypothesis to the analysis of speculative behaviour on financial markets—perhaps the only real context in which it makes sense to use this hypothesis—can cause phenomena of self-fulfilling expectations, with all that this entails in terms of speculative ‘bubbles’, catastrophic crashes, etc.—possibilities that Keynes had already foreseen.

With all these reasons for concern, and others we have not had room to highlight, one can ask why the new classical macroeconomics was so widely accepted in the era of Reagan and Thatcher. One answer is immediate, the simplest and perhaps the truest: it was the era of Reagan and Thatcher. The neomonetarists were able to display a large and potent artillery of rhetorical devices, among which there was even the call to logic. But the effectiveness of this artillery was brought out by the triumph of neoconservatism in the 1970s and 1980s and, in the profession, by the groundwork undertaken by Friedman’s old monetarism.

However, the main reason for the success of neomonetarism, at least within academic circles, is the role it has played in the development of an extremely prestigious tradition: the ‘neoclassical synthesis’. In the evolution of that tradition, the new classical macroeconomics has represented the final point of arrival. From the neoclassical synthesis the neomonetarists accepted the fundamental theoretical reference of the Walrasian general-equilibrium model, as well as a series of other convictions of some importance, such as that for which Keynes would not have the right of citizenship in a world of flexible prices and rational individuals. Early monetarism had already knocked down a few doors, showing, on the one hand, the implications of the ‘flex-price’ hypothesis for the predominance of supply (as against effective demand) in determining properties of the general equilibrium, and, on the other hand, the ‘natural’ character of those properties. The neomonetarists have accepted both these theoretical implications of traditional monetarism. What they added, thus completing the process of disengagement from Keynes, was the rational-expectation hypothesis, the only one plausible, in fact, in a world in which subjects are perfectly rational (in the neoclassical sense) and markets perfectly competitive. Thus, beginning from the distant ‘Keynesian’ premisses of the neoclassical synthesis, it was impossible to avoid the extreme logical conclusions of the new classical economics. And the only real difference between fathers and sons, in the end, seems to be the different degrees of naivety with which it is possible to believe in the realism of the flex-price hypothesis.

This also leads us to note, in defence of the new classical macroeconomics (if it can be called a defence), that a great many of its weaknesses, e.g. those relating to its way of treating uncertainty, and the hypotheses dealing with stationarity of equilibrium and its dynamic properties, are also weaknesses of many other neoclassical Keynesian models. The contribution of neomonetarism in bringing these to light could be considered a merit.

Finally, there are two additions to the modern theoretical economist’s equipment which are due to the neomonetarists. The first is the systematic introduction into macroeconomics of the study of the processes of endogenous formation of expectations, together with the processes of elaboration and diffusion of information, which amounts to the addition of another important theoretical instrument to the toolbox of the economist: the economics of information. The second is extremely important: it is the ‘policy-evaluation proposition’. According to this proposition, Keynesian economic policies are mistakenly based on econometric models whose parameters are assumed stable. The parameters of the structural forms of the models are, in fact, derived from hypotheses about the behaviour and the decision-making rules of economic agents which are far from being a justification of their stability. In particular, in defining the functions to estimate, the expectations of the decision-making agents concerning the variables of the model are usually assumed as given. But if the expectations are endogenously formed, they will change with variations in the size of the variables and, above all, with variations in economic policy decisions. This means that the structural parameters are not stable, nor independent from the policies that their stability should justify. This not only pulls the rug out from under the feet of a great many neo-Keynesian discretionary economic policies but, more generally, undermines the theoretical bases of all econometric researches that are unable to take into account the endogenous formation of expectations.

9.4.