The Theory of General Economic Equilibrium

8.2.1. The first existence theorems and von Neumann’s model

The impasse in which general-equilibrium theory had remained trapped in the pre-war period was due to the problem of the existence of solutions.

The economists in this field had not gone much beyond counting the unknowns and the equations. In order to make further progress it was necessary for new scholars to enter the field who were ‘more mathematicians than economists’.A group with these characteristics did form, thanks to the work and support of Karl Menger, and became one of the most remarkable groups in the history of economic analysis. Karl Menger, son of the great Austrian economist Carl Menger, was an active member of the Vienna Circle, from which he drew the bases for an axiomatization and a definitive consolidation of the scientific work according to the Geometry model of the great Austrian mathematician David Hilbert. In the 1930s Menger established a permanent series of seminars, the Mathematisches Kolloquium, which were attended by many of the most important mathematicians and logicians of the period, including Gtidel, Alt, von Neumann, and Tarski. At the Kolloquium both pure and applied mathematical works were discussed, and among the latter were some of the most important works on mathematical economics of the 1930s. In these works, it was not so much the substantial aspects of the applications of mathematics to economic problems that were discussed but rather the underlying mathematical tools, so that the great mathematicians, who were relatively inexpert in economics, were able to take part. This was the beginning of a de facto separation between economics and mathematical economics; the latter being considered as the application of mathematical techniques by professional mathematicians, who are mostly uninterested in economics itself.

The attitude of the participants of the Kolloquium towards traditional economic theory is well summed up by the contempt in which John von Neumann held the works of contemporary economists, judging their mathematics ‘crude and primitive’, as if mathematical standards could judge the validity of economic research.

Given these premisses, it is easy to understand why the Kolloquium focused its attention on the problem of existence: this was the most suitable problem to be treated in purely mathematical terms.In the beginning, however, the proof of the existence of an equilibrium for a general case was not the object of special attention; the starting point was, instead, a case of fixed production coefficients. It was Frederik Zeuthen who proposed an ingenious solution to one of the main technical difficulties of the general-equilibrium model: the constraints requiring that the quantities of utilized resources are not higher than those available take on the form of inequalities. He then introduced a ‘slack’ variable, measuring the value of the unused resources; in this way each constraint could be written under the form of an equality.

However, Zeuthen did not manage to demonstrate the existence of solutions, not even for the ‘simplest’ problem. Neither did Schlesinger, a successful banker fond of economics who was an active member of the Kolloquium. Schlesinger financed the studies of Abraham Wald, a young mathematician of Romanian origin, who took part in the meetings from 1930 onwards. It was Schlesinger himself who assigned Wald the problem of the existence of general equilibrium. Armed with the suggestions of Zeuthen, who had also been recommended to him by Schlesinger, Wald managed to prove the existence of solutions for a stationary system of linear equations under some key hypotheses of convexity and non-saturation, hypotheses which have continued to be used in the literature. Contrary to what a great many members of the Kolloquium believed, the importance of Wald’s result lay precisely in its having demonstrated that the existence of an equilibrium can be ensured only by imposing important restrictions on individual preferences and the technology employed, and that it is impossible to obtain it under completely ‘general’ mathematical hypotheses. As Debreu was later to discover, the real difficulty in the ‘interesting’ demonstrations of existence is exactly that of imposing restrictions on behaviour and technology that are the least arbitrary possible but are at the same time significant from the economic point of view.

With the escalation of Nazism, the Kolloquium disbanded. At this point, another of the ‘great figures’ who had attended the meetings took on a key role: Oskar Morgenstern, a fervent member of the Kolloquium, a great admirer of logical positivism, and a strenuous defender of the application of its precepts in the field of economic theory. Even though he also suffered the consequences of the ascent of Nazism, Morgenstern helped Wald to emigrate to the United States. When Wald arrived there he took up the study of economic statistics, partially in collaboration with Morgenstern himself, and never returned to the existence problem. Morgenstern, however, remained very active, maintaining contacts with the survivors of the Kolloquium and ensuring that the results of the researches of the group did not fall into oblivion. In particular, he kept strong links with John von Neumann.

By the end of the 1920s von Neumann had already proved the existence of an equilibrium for some situations in which two individuals, who follow some ‘rational’ rules of behaviour, face each other. For this purpose he used a theorem which was to become extremely important, in its various versions, in many demonstrations of existence: Brouwer’s fixed-point theorem. After emigrating to the United States, and working independently of Wald, von Neumann managed to extend his first results to an economy in which all variables grow at a constant rate. We will discuss this shortly. In the meantime, we must say something about his intellectual exchange with Morgenstern, which in this period reached its high point. Morgenstern was aware of the ‘poverty’ of economic applications of mathematical techniques and, as a good logical positivist, was considering the titanic task of creating an ad hoc mathematical language for economic science, a language conducive to the rigorous formulation of the economic problems, and avoiding the ‘undesirable’ and limiting application of differential calculus. This was the origin of game theory, whose conceptual apparatus had been developed by von Neumann in his first existence proofs.

Undoubtedly, the classic book for this new language was Theory of Games and Economic Behaviour (1944), by von Neumann and Morgenstern. Game theory, according to Morgenstern, should be the nucleus of the new general language he hoped to give economics. Perhaps it did not achieve precisely what Morgenstern wished, but there is no doubt that it has experienced a growing success over time.Now let us consider the famous ‘von Neumann model’, the most important, perhaps, of the results of this branch of research. It is probable that the author began to think about it as early as the end of the 1920s, when he was Privatdozent (a university lecturer) in Berlin (see section 8.5.4). However, it was presented for the first time in 1932 in a seminar at Princeton, and it was only later that von Neumann came to hear about Wald’s work. Therefore its direct link with the Viennese Kolloquium is not at all certain. In fact, von Neumann’s article was published (in Ergebnisse eines mathema- tischen Kolloquiums) only in 1937, with the title of ‘liber ein (Skonomischen Gleichungs-system und eine Verallmeinerung des Brouwerschen Fixpunkt- satzes’. However, it only became known to a wider academic public after it was translated into English and published, with the title of ‘A Model of General Economic Equilibrium’, in the Review of Economic Studies (1945-6). The model is based on a series of rather brave assumptions: there are diverse methods of jointly producing different commodities by means of themselves; each of these methods, called ‘activities’, combines the diverse commodities according to determinate coefficients of input and output; if the economy is expanding, the ratio between input and output remains constant, i.e. there are constant returns to scale; the number of activities is not lower than the number of commodities, but it is not infinite; consumption is determined by the ‘necessities of life’ and is included in the productive inputs without distinguishing it from other inputs; there being no unproductive consumption, all the produced surplus is reinvested; there is no other money than the numeraire; there is perfect competition, so that, in equilibrium, the non- profitable productive processes are not activated, while the commodities in excess supply have a zero price.

Von Neumann proved that, under these assumptions, there is an equilibrium which guarantees non-negative prices and activity levels. In this equilibrium the rate of interest is equal to the rate of growth, which is a consequence of the assumption that all profits are reinvested. The rate of growth is uniform in all sectors, and therefore there is ‘balanced growth’, which means that the composition of commodities in the gross output remains constant through time. Finally, in this equilibrium only the most efficient productive methods are activated.

The model has played an important role in several developments of economic theory. As far as the general-equilibrium theory is concerned, it was important for the application of the fixed-point theorem and for the solution it supplied to the problem of existence. In those days, von Neumann’s model represented the most general of the equilibrium models for which the existence of solutions had been proved. Besides this, in the area of growth theory, von Neumann’s model opened the way to the multi-sectorial and normative theories of growth of the 1950s and 1960s; for example, the famous ‘turnpike theorem’ is a direct application of von Neumann’s model. In the theory of programming, this model has laid the foundations of the so-called ‘activity analysis’ and of modern methods of linear programming.

Finally, it is important to note that von Neumann’s model has aroused interest even among economists who are not supporters of neoclassical theory. In fact, it has many characteristics in common with the classical and Marxian theoretical systems: for example, the treatment of workers’ consumption as a technological input; the image of the ‘capitalist’ as a person in charge of the function of capital accumulation; a theory of value that does not make prices depend on utility or other subjective phenomena; the use of a notion of equilibrium which can be interpreted in terms of reproduction equilibrium; and, finally, the predominance of the idea of reproducibility over that of scarcity.

On the other hand, various characteristics typical of the neoclassical theoretical system are absent, besides the concept of scarcity: for example, the faith in consumer sovereignty or in the predominance of the conditions of demand over those of supply in the determination of prices and quantities produced.It is also interesting to note that von Neumann’s model solves one of the principal problems of Walras’s schema, that of the over-determination of the system of equilibrium equations in the case in which uniformity in the rates of return of the various capital goods is required. The model solves this problem, however, by eliminating its cause, which is the hypothesis of the existence of an arbitrarily given initial endowment of capital goods. This hypothesis was important in the Walrasian model, as it served to explain the remuneration of capital goods in terms of the forces of supply and demand. In von Neumann’s model, the structure of the capital goods is determined endogenously and depends, as does the remuneration of capital, only on the conditions of production.

8.2.2. The English reception of the Walrasian approach

General-equilibrium theory was rather late in reaching English academic circles and initially, that is, before the advent of Hicks’s work, stimulated no significant contributions.

An important event, not only for the reception of the Walrasian approach in England but, more generally, for the history of economic analysis, was the arrival of Lionel Robbins at the London School of Economics in 1929, when he was offered a senior professorship at the remarkably young age of thirty- one. In the inter-war period Robbins was, in fact, one of the most influential economists in England. This was the period in which an extraordinary generation of ‘young’ economists arrived on the scene—personalities of the calibre of Hicks, Kaldor, Roy Allen, and Abba Lerner. In a short time the London School of Economics became, under the driving force of Robbins, one of the most active centres for the production and discussion of economic theory on an international scale. Many of the most important economists of the time visited London in that period to discuss their research. The longest- lasting impression, however, was certainly left by Hayek, who in 1931 held a seminar course at the LSE from which he drew inspiration for his book Prices and Production. In the same year, he moved to London to teach at the university. All this can be at least partially explained by the atmosphere of enlightened liberalism which existed in the department under Robbins’s leadership.

The LSE soon became one of the centres in which general-equilibrium theory was studied with the greatest interest. It was also Robbins who introduced Hicks to Pareto’s works and offered him a course on general equilibrium. Robbins’s role was basically that of patron, able as he was in looking after the interests of the ‘young lions’ and in ordering the results of their work within his own methodological framework. Hayek, on the other hand, was the ‘prime mover’ of the group’s theoretical speculation.

At the centre of Hayek’s thought in that period was the attempt to apply the conceptual scheme of the general-equilibrium model to the ‘dynamic’ analysis of cyclical fluctuations. Historical events seemed to show that the instability of the real economy depends on the instability of monetary aggregates; and yet money had difficulty in finding an active role in the Walrasian conceptual system. We discussed the truly dynamic and macroeconomic component of Hayek’s theory in Chapter 7. Here we will say something about some contributions to general-equilibrium theory which he put forward, above all, in Prices and Production.

Despite the deficiencies of the general-equilibrium apparatus and the consequent analytical difficulties, Hayek was convinced that it was impossible to give a coherent and unitary explanation of the trade cycle without basing it on an equilibrium theory. However, the needs of dynamic analysis meant that the category itself of equilibrium, and the theoretical constructions which originated from it, had to be seriously thought out again, if not in their logical-formal dimension, at least in their interpretative dimension. For example, Hayek observed that in an economic context in which time does play a role, two quantities of the same good at two different moments must be considered to all intents and purposes as two different goods. On the other hand, arbitrage phenomena occur normally, not only in spatially separate markets, but also at different moments in time. It was from these suggestions that Arrow and Debreu were able to construct their famous model of intertemporal equilibrium, twenty years later.

Already in that period Hayek had also succeeded in causing a change of direction in economic analysis by demonstrating the crucial importance of the problem of expectations in the ‘dynamic’ versions of the Walrasian model: only if individuals manage to produce systematically correct predictions of the future conditions of the economic system is it possible to consider equilibrium as a ‘normal’ condition of the system itself. This point of view reverberated strongly in the innovative second part of Hicks’s Value and Capital (1939). In this work Hayek’s observations were translated into a new conceptual scheme which was to remain the reference point for all later theoretical elaborations of equilibrium analysis, regularly outliving each of these.

Hicks acknowledged on more than one occasion his intellectual debt to Hayek. It must be said, however, that, once the initial driving force had been exhausted, both Hicks and the majority of the ‘young lions’ of the LSE took up positions which were increasingly distant from that of Hayek. While Hayek was interested in the study of equilibrium processes in which, according to the Austrian tradition, the time dimension of production plays a central role, even at the cost of sacrificing the role of expectations by means of a hypothesis of perfect foresight, Hicks, and with him, albeit from quite a different position, Kaldor, Allen, and Lerner, were moving in another direction, trying to understand the way in which the process of expectation formation could influence the equilibrium characteristics of the economic system. This was a substantial opening towards the theories of disequilibrium; an opening which led Kaldor and Lerner, and later also Hicks, to abandon equilibrium methodology.

In order to understand the intellectual evolution of these economists it is necessary also to consider the influence of another ‘patriarch’ of the LSE, Arthur Bowley, an excellent statistician and mathematical economist. His lectures helped to enrich the mathematical knowledge of the ‘young lions’. In Allen’s case, Bowley’s teaching also ended up in a fruitful scientific collaboration which led to the production of a statistical work on family expenditures which was for many years a standard reference point.

8.2.3. ValueanddemandinHicks

The paper ‘A Reconsideration of the Theory of Value’, written with Roy Allen and published in Economica in 1934, the first three chapters of Value and Capital, and A Revision of Demand Theory (1956) contain the ordinalist reorganization of consumer theory. By taking advantage of some suggestions by Pareto, Hicks immediately realized that Edgeworth’s analysis of indifference curves would allow the theory of value to discard the cumbersome concept of cardinal utility.

In order to appreciate the importance of the shift from cardinalism to ordinalism made by Hicks, it is necessary to take into account the cultural atmosphere of the period and, in particular, the new criteria which neopositivism was proposing for the foundation of scientific work—above all, the criterion that any scientific proposition must be subject to an empirical verification procedure. Now, the notion of cardinal utility was formulated for principally philosophical ends; and this was not acceptable to the new epistemological orientations. If the Benthamian philosopher found no problem whatsoever with the scientific legitimization of the categories of utilitarian theory, this was not the case for those who had been won over by the spirit of the Vienna Circle. Thus Hicks, in Value and Capital, was able to say: ‘If one is utilitarian in philosophy, one has the perfect right to be utilitarian in one’s economics. But if one is not (and few people are utilitarian nowadays), one also has the right to an economics free of utilitarian assumptions’ (p. 18)

At the beginning of the 1930s, the notion of marginal utility had been definitively overtaken, at least at the LSE. In his famous 1932 Essay, Robbins had insisted more than once on the importance of avoiding metaphysical fog. The concept of economic science as a structure of abstract relations among scarce means and ordered preferences has no need for, nor offers any space to, the remains of Benthiam utilitarianism in economics. As we have already mentioned, Pareto was one of the first to understand the epistemological anachronism of cardinalism, and it was precisely because his proposal to leave it aside was so ahead of its time that his contribution remained for a long time without any appreciable acknowledgement or follow-up. It is true that in his pioneering ‘Sulla teoria del bilancio del consumatore’ (1915), Slutsky had forerun the use of the principle of indifference in overtaking the obsolete law of the saturation of needs, but this article did not circulate within the academic circles of the period.

In their 1934 paper, Hicks and Allen not only rediscovered Slutsky’s famous result, the decomposition of the price effect into an income and a substitution effect, but, more importantly, they decreed the replacement of Gossen’s first law (the law of decreasing marginal utility) by the principle of marginal substitution: as Hicks himself was to make plain later, in Value and Capital, all that is needed for the validity of the principle is the convexity of the indifference map. The observation that cardinal utility, far from constituting an advance on the interpretative front, actually took empirical content away from the theory, had as a consequence the abandonment, without regret, of the cardinalist approach.

8.2.4. General economic equilibrium in Hicks

The second line of research in Value and Capital concerns generalequilibrium theory. The influence of this line of thought on developments in economic theory was relatively modest at first, especially because the book was published in the middle of the Keynesian revolution, so that some of the most important of Hicks’s arguments were discussed within a conceptual framework that was basically extraneous to, and at the same time simpler and more effective than, the method of temporary general equilibrium.

With the passing of time, however, Value and Capital exercised increasing influence—and not so much for its specific contributions, even though these were numerous, as for the methods adopted. The static part of the work was the first to receive attention, especially in the USA, and contributed decisively to the resumption of general-equilibrium theory. But also the dynamic part, after a long period in obscurity, was finally appreciated, so much so that the method of temporary equilibrium has become, in recent times, the main instrument of short-run neoclassical analysis.

One of the most original and important elements of Value and Capital is represented by the application of comparative statics to general equilibrium. Before Hicks, in fact, theorists following this approach had limited themselves to studying the existence of equilibrium solutions, without attempting to use the model to solve even the simplest problems of change, for example, the effects produced by an increase in the ‘demand’ or ‘supply’ of a determinate good or factor. This is the origin of the widespread impression of sterility of the model. The fundamental ‘ingredients’ that allowed Hicks to escape from the blind alley of counting the number of equations and unknowns were basically two:

(1) the principle that a group of goods can be treated as a single good if relative prices remain constant—the well-known Hicks—Leontief aggregation theorem;

(2) the idea that the qualitative results of static comparative analysis can be derived from the conditions which ensure the stability of equilibrium. Hicks’s basic objective was to construct a dynamic theory, in the sense of a theory in which ‘each variable must be dated’. Static analysis was only considered as a useful, though indispensable, premiss for dynamic analysis. The main difficulty in the shift from statics to dynamics comes from the fact that, while in a static context the decisions of the agents depend solely on current prices, in a dynamic context they also depend on expected prices. The instrument used by Hicks to make static analysis serve dynamic ends was Myrdal’s and Lindahl’s ‘period’ method, the effectiveness of which he had already had the opportunity of experimenting in 1935. As we have seen in Chapter 7, Myrdal had introduced expectations among the determinants of relative prices: future anticipated changes produce effects on the economic process before they actually take place. This leads to the fact that the determination of an equilibrium must take into account expectations. Hicks later called Myrdal’s method the ‘expectations method’. On the other hand, as we also mentioned in the previous chapter, Lindahl had already opened the way for the analysis of a dynamic process in terms of a succession of temporary equilibria.

By dividing time into periods of an adequate length (‘weeks’) and by including among the data of a determinate period not only the traditional data of static theory (tastes, technology, and resources) but also the state of expectations, Hicks was able to use the static method to study the ‘temporary equilibrium’, i.e. the equilibrium reached by an economic system in one period. In particular, he tried to examine the stability and the comparative statics properties of an economy in temporary equilibrium. In this context, he treated the movement of the economic system through time as a succession of temporary equilibria, each differing both from the preceding one, owing to the accumulation of capital, technical progress, changes in consumers’ tastes, etc., and from the one expected by the economic agents. And this occurs both because the agents are not able to predict the future evolution of the data and prices and because individual consumption and production plans are generally incompatible, not to mention the fact that price expectations are also in general incompatible. From this point of view, the economic system is always in temporary equilibrium, but never in equilibrium ‘through time’, in the sense that in each period prices are generally different from what predicted by the agents when they formed their production and consumption plans.

Hicks maintained that a greater inter-temporal coordination of decisions would have been realized with future markets, provided there were future markets for all goods. In this case, all transactions would take place at the initial moment on the basis of the current prices of all the goods (present and future), while in successive periods there would be only the practical execution of the transactions stipulated in that moment. However, the uncertainty about the temporal evolution of preferences and resources limits the potential existence of future markets for goods. Consequently, it is not possible, according to Hicks, to study the operation of a real economic system by using inter-temporal equilibrium models even if, for certain ends, it may be worth resorting to the pure model of a futures economy, where present and future markets exist for all goods.

In the second part of Value and Capital, therefore, Hicks not only presented an original model for studying dynamic problems, but also anticipated, with his ‘futures economy’, some of the most important developments of the modern versions of the theory of general equilibrium: those which try to resolve the problems of time and uncertainty, while remaining within the field of static analysis.

8.2.5. The IS-LM model

In the article ‘Mr Keynes and the Classics’, published in 1937 but discussed in a seminar a year before, Hicks started, immediately after the publication of the General Theory, that process of reabsorption of Keynes’s analysis into the mainstream of orthodox theory which was to occupy the neoclassical economists for the next 30 years. Hicks apparently followed a Marshallian approach, assuming as given the stock of capital and interpreting the principle of effective demand in terms of a model of short-run equilibrium. In reality, he presented in that article an ambitious, though simple, model of temporary general equilibrium, in which he showed how macroeconomic equilibrium can be reached simultaneously in two markets, those of money and of savings.

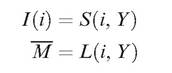

Hicks generalized the General Theory by reducing it to four equations: one for savings, S = S(i, Y), derived from the consumption function; one for investments, I = I(i), which incorporates the function of the marginal efficiency of capital; one for the demand for money, L = L(Y, i), expressed in terms of the demand for transactions and speculative purposes; and one for the money supply, assumed to be given exogenously, M = M. The variables Y and i represent the income and the rate of interest respectively. By equating the supply and demand for savings and the supply and demand for money, the following two equations are obtained:

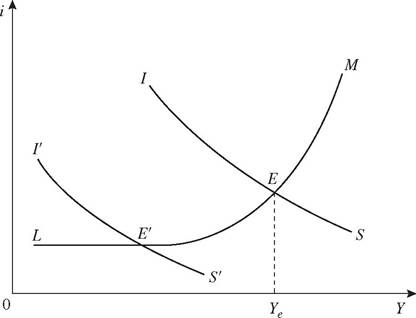

From them the IS and LM curves, shown in Fig. 9, originate. The IS curve exhibits all the combinations of income and interest rates that ensure real equilibrium. For example, an increase in income will raise savings and require a reduction in the rate of interest so as to induce entrepreneurs to increase investments. In this way there is a movement towards the right along the IS curve. The LM curve shows all the combinations of income and interest rates at which the demand for money coincides with the supply.

Fig. 9

For example, a rise in income will increase the transaction demand for money; if the supply is given, the demand for speculative motives has to decrease; and this will occur as a consequence of an increase in the interest rate. Thus there is a movement towards the right along the LM curve.

At point E the two markets are in equilibrium simultaneously. Once income has been determined in this way, the employment level may be calculated by knowing the production function. Given the monetary wage, the price level will be determined endogenously so as to ensure equality between the marginal productivity of labour and the real wage. However, Hicks did not give a definitive solution on this aspect of the problem. As we will see in the next chapter, it was from exactly this point that Modigliani began the ‘neoclassical synthesis’ after the Second World War.

With this model, Hicks tried to demonstrate that the General Theory was not as general as Keynes believed, but only a special case of (neo)classical theory: the case of the liquidity trap. In periods of depression the interest rate would be extremely low and speculators would not be much inclined to hold non-liquid balances; therefore, their demand for money would absorb any amount offered to them, so that any increase in the supply of money would be counterbalanced by a corresponding increase in demand, and the interest rate would not fall. The LM curve would be horizontal. In such a case, monetary policy would be totally ineffective; above all, it would be incapable of bringing the economy to full employment. It can be seen in Fig. 9 that, if Ą S' holds true, the equilibrium will be at point E' on the horizontal part of the LM curve; in this case an increase in the money supply will move the entire LM curve to the right, but not the equilibrium point.

In the next chapter we will see how Hicks’s model was to constitute, in the 1950s and 1960s, the core of the ‘neoclassical synthesis’, i.e. that macroeconomic approach which, in the attempt to assimilate Keynes into orthodox theory, was to completely distort his message. It is necessary to point out, however, that Hicks during the 1960s persistently rejected this interpretation of Keynes’s work.

8.3.