A brief guide to externalities in growth models

In this section we briefly discuss the role that externalities play in prominent theories of economic growth. One class of growth theories features externalities in the accumulation of knowledge possessed by firms (organizational capital) or by workers (human capital).

Another class of growth models features externalities from the introduction of new goods, in the form of surplus to consumers and/or firms. Other theories combine knowledge externalities and new good externalities. Finally, some important growth theories include no externalities at all. Table 1 provides examples of growth models categorized in these four ways. At the end of this section, we will dwell a little on the predictions of no-externalities models in order to motivate the evidence we describe in the next section. The evidence in the next section will suggest that models with no externalities cannot explain a number of empirical patterns.Table 1

Some growth models by type of externality

| New good externalities | No new good externalities | |

| Knowledge externalities No knowledge externalities | Stokey (1988, 1991) Romer (1990) Aghion and Howitt (1992) Eaton and Kortum (1996) Howitt (1999, 2000) Rivera-Batiz and Romer (1991) Romer (1994) Kortum (1997) | Romer (1986) Lucas (1988, 2004) Tamura (1991) Parente and Prescott (1994) Jones and Manuelli (1990) Rebelo (1991) Acemoglu and Ventura (2002) |

2.1. Models with knowledge externalities

Romer (1986) modeled endogenous growth due to knowledge externalities: a given firm is more productive the higher the average knowledge stock of other firms. As an example, consider a set of atomistic firms, each with knowledge capital k, benefiting from the average stock of knowledge capital in the economy K in their production of output y:

Romer showed that, under certain conditions, constant returns to economy-wide knowledge, as in this example, can generate endogenous growth.

The external effects are, of course, critical for long-run growth given the diminishing returns to private knowledge capital. Romer was agnostic as to whether the knowledge capital should be thought of as disembodied (knowledge in books) or embodied (physical capital and/or human capital).Lucas (1988) was more specific, stressing the importance of human capital. Lucas sketched two models, one with human capital accumulated off-the-job and another with human capital accumulated on-the-job (i.e., learning by doing). Both models featured externalities. In the model with human capital accumulated off-the-job, Lucas posited

Here u is the fraction of time spent working, and 1 - u is the fraction of time spent accumulating human capital; h is an individual worker’s human capital, and H is economy-wide average human capital; k and n are physical capital and number of workers at a given firm. Because human capital accumulation is linear in the level of human capital, human capital is an engine of growth in this model. This is true with or without the externalities; across-dynasty externalities are not necessary for growth. As Lucas discusses, however, within-dynasty human capital spillovers are implicit if one imagines (2.3) as successive generations of finite-lived individuals within a dynasty. Within-dynasty externalities, however, would not have the same normative implications as across-dynasty externalities, namely underinvestment in human capital. Lucas (1988) did not argue that across-dynasty externalities were needed to fit particular facts. But he later observed that such across-household externalities could help explain why we see “immigration at maximal allowable rates and beyond from poor countries to wealthy ones” [Lucas (1990, p. 93)].

Tamura (1991) analyzed a human capital externality in the production of human capital itself. This formulation conformed better to the intuition that individuals learn from the knowledge of others.

Tamura specified

Because H represents economy-wide average human capital, β < 1 implies that learning externalities are essential for sustaining growth in Tamura’s setup. If applied to each country, this model would suggest that immigrants from poor to rich countries should enjoy fast wage growth after they migrate, as they learn from being around higher average human capital in richer countries. Lucas (2004) used such learning externalities within cities as an ingredient of a model of urbanization and development.

Models not always thought of as having knowledge externalities are Mankiw, Romer and Weil’s (1992) augmented Solow model and the original Solow (1956) neoclassical growth model. In Solow’s model all firms within the economy enjoy the same level of TFP. This common level of TFP reflects technology accessible to all. The Solow model therefore does feature disembodied knowledge externalities across firms within an economy. In Mankiw et al.’s extension, knowledge externalities flow across countries as well as across firms within countries. In Section 4 we will discuss models with more limited international diffusion of knowledge. In these models imperfect diffusion means differences in TFP can play a role in explaining differences in income levels and growth rates. We stress that the Mankiw et al. model relies on even stronger externalities than the typical model of international technology spillovers, such as Parente and Prescott (1994) or Barro and Sala-i-Martin (1995, Chapter 8). We will discuss these models at greater length in Section 4, when we calibrate a hybrid version of them.

2.2. Models with knowledge externalities and new-good externalities

Models with both knowledge externalities and new-good externalities are the most plentiful in the endogenous growth literature. By “new-good externalities” we mean surplus to consumers and/or firms from the introduction of new goods.

The new goods take the form of new varieties and/or higher quality versions of existing varieties. In Stokey (1988), learning by doing leads to the introduction of new goods over time. The new goods are of higher quality, and eventually displace older goods. The learning is completely external to firms, and what is learned applies to new goods even more than older goods. Hence learning externalities are at the heart of her growth process. In Stokey (1991), Intergenerational human capital externalities (the young learn from the old) are critical for human capital accumulation. Human capital accumulation, in turn, facilitates the introduction of higher quality goods, which are intensive in human capital in her model.Quality ladder models - pioneered by GrossmanandHelpman (1991, Chapter 4) and Aghion and Howitt (1992, 1998) - feature knowledge spillovers in that each quality innovation is built on the previous leading-edge technology. Such intertemporal knowledge spillovers are also fundamental in models with expanding product variety, such as Romer (1990) and Grossman and Helpman (1991. Chapter 3). In Romer (1990),

Intermediate goods, the x(i)'s, are imperfect substitutes in production. This is the Dixit- Stiglitz “love of variety” model. The stock of varieties, or ideas, is A. In (2.7) new ideas are invented using human capital and, critically, the previous stock of ideas. This is the intertemporal knowledge spillover. Jones (1995, 2002) argues that, in contrast to (2.7), there are likely to be diminishing returns to the stock of ideas (an exponent less than 1 on A). He bases this on the fact that the number of research scientists and engineers have grown in the U.S. and other rich countries since 1950, yet the growth rate has not risen, as (2.7) would predict. Intertemporal knowledge spillovers still play a pivotal role in Jones' specification; they are just not as strong as in Romer's (2.7).

More recent models, such as Eaton and Kortum (1996) and Howitt (1999, 2000), continue to emphasize both knowledge externalities and new-good externalities. We will elaborate on these in Section 4 below.

2.3. Models with new-good externalities

It is hard to find a model with new-good externalities but without knowledge externalities. We have identified three papers in the literature featuring such models, but two of the papers also have versions of their models with knowledge externalities.

Rivera-Batiz and Romer (1991) present a variation on Romer's (1990) model, as part of their analysis of the potential growth gains from international integration. In their twist, new intermediate goods are invented using factors in the same proportions as for final σoods production in (2 6)∙

They call this the “lab equipment model” to underscore the use of equipment in the research lab, just like in the production of final goods. In this formulation, they emphasize, “Access to the designs for all previous goods, and familiarity with the ideas and know-how that they represent, does not aid the creation of new designs” (pp. 536537). I.e., there are no knowledge externalities, domestic or international. Production of ideas is not even knowledge-intensive. Ideas are embodied in goods, however, and there is surplus to downstream consumers from their availability. Rivera-Batiz and Romer note that this model allows countries to benefit from ideas developed elsewhere simply by importing the resulting products. Just as important, international trade allows international specialization in research. Countries can specialize in inventing different products, rather than every product being invented everywhere.

In a similar spirit, Romer (1994) considered a model in which knowledge about how to produce different varieties does not flow across countries, but each country can import the varieties that other countries know how to produce.

For a small open economy, Romer posited

xj represents the quantity of imports of the jth variety of intermediate good. Because a < 1, intermediate varieties are imperfectly substitutable in production. Firms in the importing country will have higher labor productivity the more import varieties they can access. If exporters cannot perfectly price discriminate and there is perfect competition among domestic final-goods producers, the higher labor productivity (higher Y/N) will benefit domestic workers/consumers. If consumer varieties were imported as well, there would be an additional source of consumer surplus from import varieties. Romer analyzed the impact of import tariffs on the number of varieties M imported in the presence of fixed costs of importing each variety in each country. Although Romer’s model is static, growth in the number of varieties over time, say due to domestic population growth or falling barriers to trade, would be a source of growth in productivity and welfare in his model.

Kortum (1997) develops a model in which researchers draw techniques of varying efficiency levels from a Poisson distribution. Kortum does consider spillovers in the form of targeted search. But he also considers the case of blind search, wherein draws are independent of the previous draws. (Kortum fixes the set of goods produced but allows endogenous research into discovering better techniques for producing each good.) In the case of blind search, there are no knowledge spillovers. Growth is sustained solely because of population growth that raises the supply of and demand for researchers. It takes more and more draws to obtain a quality deep enough into the right tail to constitute an improvement. A constant population growth rate sustains a constant flow of quality improvements and, hence, a constant growth rate of income.

2.4. Models with no externalities

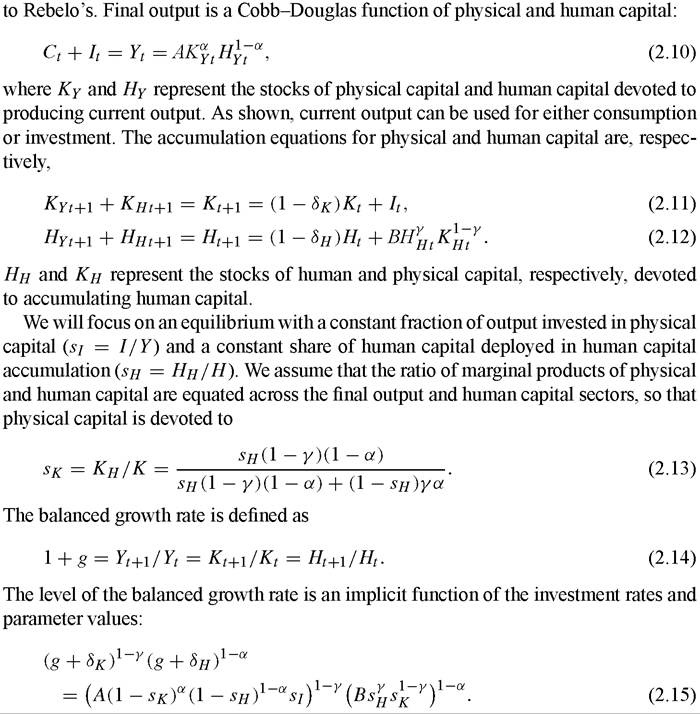

The seminal growth models without externalities are the AK models of Jones and Manuelli (1990) and Rebelo (1991). Inthe next section we will present evidence at odds with such models, so we dwell on their implications here. We consider a version close

Provided a < 1, human capital is the engine of growth. The growth rate is monotonically increasing in s1 because physical capital is an input into human capital accumulation whereas consumption is not. Related, the growth rate does not monotonically increase with the share of inputs devoted to producing human capital. This is because devoting more resources to producing current output increases the stock of physical capital, which is an input into human capital accumulation and hence growth.[500] When we look at the data in Section 3, however, we will find no country so high an sH or sκ as to inhibit its growth according to this model.

When α = 1 we have a literal Y = AK model, and the growth rate is solely a function of the physical capital investment rate:

Here there is no point in devoting effort to producing human capital, so sH = 0 and sκ = 0∙

In the special case γ = 1, human capital is produced solely with human capital. This might be called a BH model. Presuming a < 1 of course, the growth rate is simply

Unlike when γ < 1, the growth rate here is monotonically increasing in the effort devoted to adding more human capital. Lucas (1988) and many successors focus on this BH model because human capital accumulation is evidently intensive in human capital. Moreover, even AK models such as Jones and Manuelli (1990) construe their K to incorporate both human capital and physical capital. The consensus for diminishing returns to physical capital (a < 1) is strong. Constant returns are entertained only for a broad measure of physical and human capital. We stress (2.15), a hybrid of AK and BH models, because this generalization allows us to take into account the combined impact of physical and human capital investment rates on growth when physical capital is an input to human capital accumulation (γ < 1).

3.