A Brief Summary of the Efficient Market Hypothesis

6.1.1 Disengagements from the Efficient Market Hypothesis

We noted in Chap. 5 that the efficient market hypothesis cannot really explain the current state of financial markets, nor the global financial crisis, because it relies on the idea of the market operating by a series of random walks.

A stock price time series under the random walk hypothesis may be represented as:

Pt will follow a Gaussian distribution. Here e is regarded as white noise. The expected price is calculated around P0, so the expected distance from P0 has a finite value. Each price change will be estimated from the next e0 C ei C ∙ ∙ ∙ C et. Each price change will therefore be the stochastic variant of a normal distribution. This is the simplest illustration of the efficient market hypothesis.

© Springer Japan 2015

Y. Aruka, Evolutionary Foundations of Economic Science, Evolutionary Economics and Social Complexity Science 1, DOI 10.1007/978-4-431-54844-7__6

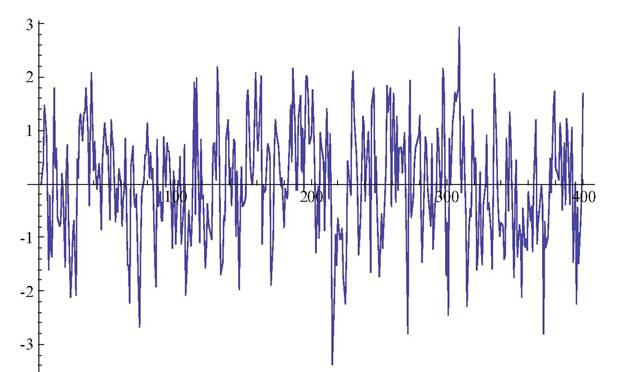

Fig. 6.1 A second-order auto-regressive model. Source: http://demonstrations.wolfram.com/Auto RegressiveSimulationSecondOrder/

There are several variants of this:

These auto-regressive models are linear, and are therefore described as linear auto-regressive models. There are several differences between AR and MR. The auto-correlation function will decrease and approach zero in AR, but in MR, it will instantly be zero whenever the parameters exceed a critical point. The partial auto-correlation function in AR will instantly be zero whenever the parameters exceed a critical point, but will decrease and approach zero in MR.

The power spectrum has a peak in AR, which will emerge around zero if the fluctuations are small. In MR, a valley emerges around zero if the fluctuations are larger (Fig. 6.1).We now show a simulation of AR(2), i.e., a second-order auto-regressive simulation. This Wolfram Demonstration uses a random variable drawn from a normal density with mean zero and variance unity. It is governed by the equation:

Here ξt is a random variable, N is the length of the series and the constants a are auto-regressive.

[1]A more sophisticated version of this is the auto-regressive integral moving average model, ARIMA(p, q, r). MA(1) is an approximate function of AR(∞).

series is stationary. A series of length 400 is created in every case in this Wolfram Demonstration.

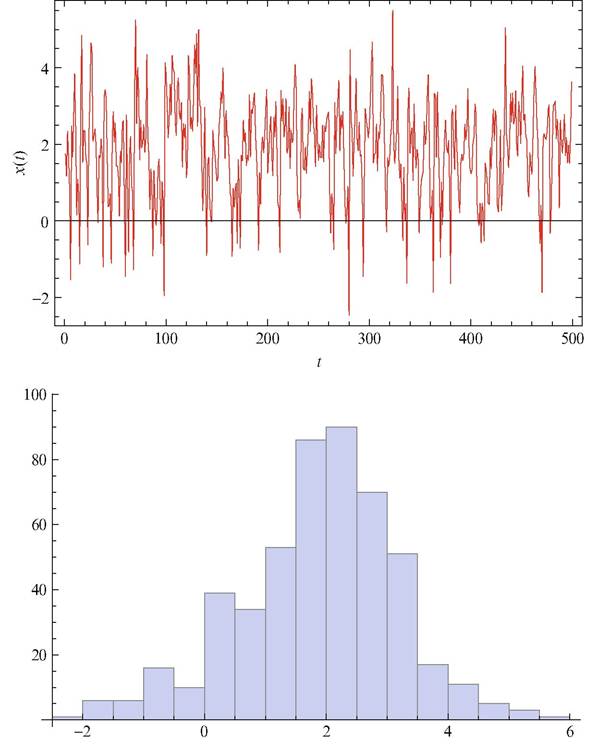

We then move to a more sophisticated regression, with two different regimes into and out of which the variable can move. Each regime follows a similar Gaussian/random process. We remove the trend item from the model, and make the process stationary and geometrically ergodic. In this case, however, the expected value E{x) generated by the two-regime model is not necessarily zero. The regimes may then be described by the condition:

We therefore obtain a two-regime threshold auto-regressive (TAR) first-order process (Fig. 6.2):

We set the constants ai as 0, and β1 = —1.5 in the first regime, β2 = —0.5 in the second regime. The series contains large upward jumps when it becomes negative, and there are more positive than negative jumps.

We then denote the actual profit of security i at term t by rit. It is then assumed that:

Here It is the information set available everywhere at term t. rit is a random error at t.It then holds that:

Efficient Market Hypothesis (Fama 1970).2

1. If the market were efficient, all usable information could affect market prices.

2. The efficiency of the market can measure all the responses of prices, given all the information It.

3. If anyone can obtain excess profit from some particular information, this market is not efficient in relation to this kind of information.

[1]Also see Fama (1965).

Fig. 6.2 Two-regime threshold auto-regressive model simulation: α1 = 1,a2 = 1,k = 1. Source: Two-regime threshold auto-regressive model simulation. http://demonstrations.wolfram. com/TwoRegimeThresholdAutoregressiveModelSimulation/

AWeakForm. Using price information, technical analytical traders can earn excess profit.

A Semi-strong Form. Basic information gives any trader a chance to earn excess profit.

A StrongForm. Insider information gives any trader a chance to earn excess profit.

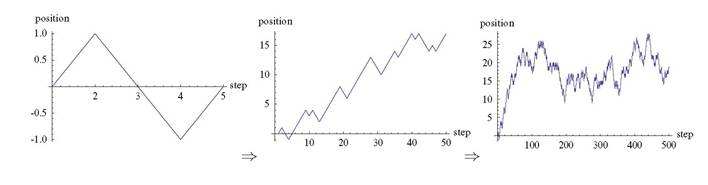

Fig. 6.3 Self-similarity in the random walk: scale = 5, 50, 500. http://demonstrations.wolfram. com/SelfSimilarityInRandomWalk/

In summary, in the world where the hypothesis holds, errors should not be systematically generated. This implies that:

6.1.1.1 Self-similarity in the Random Walk

A random walk process never excludes the emergence of self-similarity. We may therefore find a strange attraction in the efficient market hypothesis (Fig. 6.3). It is clear that:

Random walk ) Fractal motion

Fractal motion ≠ Random walk

We now show a simulation of a random walk to generate self-similarity. This is unchanged for any scaling as well as period length.

In the next section we verify the historical implications of the Gaussian distribution and the central limit theorem (CLT), and will then argue a generalization of the CLT. We will see that any distribution other than the Gaussian may benefit from a generalized CLT. It is also clear that the CLT would be valid even if there was no variance.

6.2