Moving Away from the Social Philosophy Around the Gaussian Distribution

6.2.1 The Historical Penetration of the Gaussian Distribution and Galton's Ideas

Lambert Adolphe Jacques Quetelet (1796-1874) is still well known as the proposer of the Quetelet index or Body Mass Index.

His enthusiasm penetrates various social ideas even to this day. However, advances in science are uncovering the fictitious background to Quetelet’s ideas.

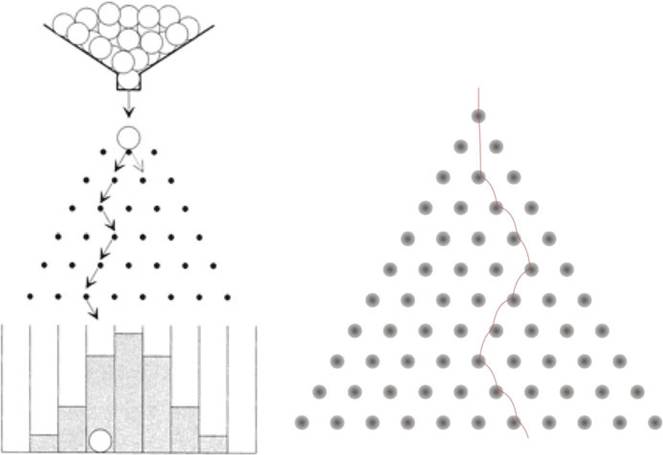

Fig. 6.4 Flexible Galton Board to generate a binomial distribution: p = 0.5, bin number = 10. Source: Figure 4 in Mainzer (2007, p. 50). The right panel is simulated from: http://demonstrations. wolfram.com/FlexibleGaltonB oard/

A key role is played by the astronomer and sociologist Lambert Adolf Jacob Quetelet, who, in 1835, for the first time, challenged others to think of the ‘average person’ as well as statistics. Does it matter that there are large error calculations in the natural sciences or in investigations of ‘normal distributions’ in society? It is today hardly comprehensible that natural and social scientists of the nineteenth century took large numbers and normal distributions as a universal rule in nature and society (Mainzer 2007, p. 48;trans. by the author).

Modern probability theory suggests that the Gaussian or normal distribution is not universal, instead taking the normal distribution as a special case stable distribution. This also changed the implications of the CLT. Unfortunately, many economists still hold to Galton’s conviction of the dominance of the normal distribution by means of the CLT.[66]

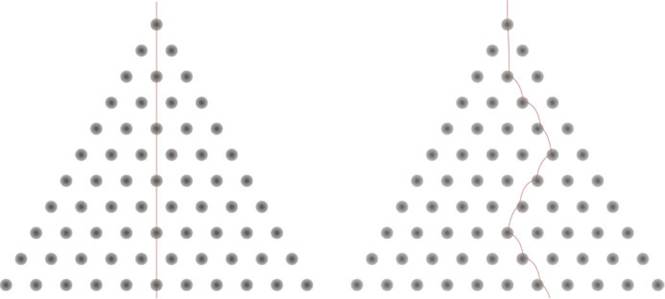

Fig. 6.5 A Galton board with frictionless and frictional cases. The details of parameters in this simulation are: In the left panel, earth acceleration 2; friction coefficient 0; initial position 0; initial velocity 0; initial angle π/2; In the right panel, earth acceleration 2; friction coefficient 2;initial position 0; initial velocity 0.5; initial angle π/2; Note: Nail parameters for both figures: thickness 0.2;strength 0.1; surface softness 2.

http://demonstrations.wolfram.com/GaltonBoard/Galton demonstrated an approximation of a binomial distribution using a nail board (see Fig. 6.4). Each time a ball hits a nail, it has a probability of bouncing either left or right. The balls accumulate in the bins at the bottom.

A visualization of the Bernoulli distribution can be traced back to Galton. On a perpendicularly standing board, nails are set at a constant distance in n parallel rows (see Fig. 6.4). Each nail is exactly in the gap between two nails in the row above. If balls of the diameter of the distance between nails are dropped from a funnel above the board, they may fall through without being affected by friction from the nails. If a ball hits a nail, it can fall either to the right or to the left. This procedure repeats itself in each row. The ball therefore falls in a random way on the nail board, being diverted to the right or left with equal probability. After going through the n rows, the balls land in the n C 1-th box. A ball would fall into box i if it were diverted i times to the right and (n — i/ times to the left. This process leads to a Bernoulli distribution of the balls (Mainzer 2007, p. 49; trans. by the author).

It is interesting to use simulation to verify and compare the frictionless and frictional cases. Even in the physical world, using an experimental method, we cannot reproduce an ideal state, and so it is hard to justify a world of normal distributions (Fig. 6.5).

Gallon’s belief therefore does not hold, as the CLT states. The CLT can be generalized to random variables without second (and possibly first) order moments and the accompanying self-similarity of the stable family. Even if the first moment is infinite, we can find an existing stable distribution, such as the power law distribution. A new definition of stable distributions thus contains the normal distribution as a special case. These findings were largely responsible for the focus on Gaussian distributions.

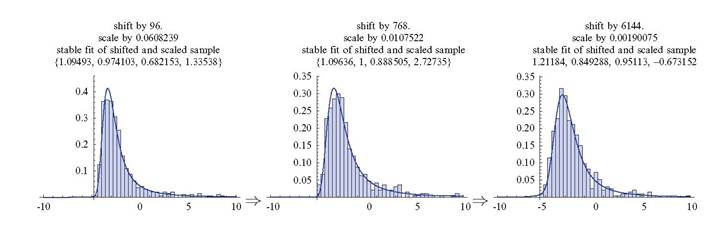

The role of non-Gaussian distributions was first noted by Benoit Mandelbrot, who proposed that cotton prices followed an alpha-stable distribution with a equal to 1.7, a Levy distribution.[67]6.2.1.1 Generalized Central Limit Theorem (GCLT)

It has often been argued recently that the “tail” behavior of sums of random variables determine the domain of attraction for a distribution. The classical CLT is merely the case of finite variance, where the tails lie in the domain of attraction of a normal distribution. Now, however, interest has moved to infinite variance models, bringing a new generalized CLT. This describes distributions lying in the domain of attraction of a stable distribution, or:

A sum of independent random variables from the same distribution, when properly centered and scaled, belongs to the domain of attraction of a stable distribution. Further, the only distributions that arise as limits from suitably scaled and centered sums of random variables are stable distributions.[68]

We now consider the generalization of the CLT. This explanation draws heavily on John D. Cook’s note “Central Limit Theorems”.[69]

The propagation of the idea of a Gaussian distribution was inseparable from the powerful role of the CLT. More interestingly, however, it has recently transpired that the theorem was applicable to non-identically distributed random variables, meaning that distributions other than Gaussian are possible in the context of the CLT. Under the generalized CLT, distributions other than Gaussian will be guaranteed a similar powerful role.

The classical CLT requires variables with three conditions: independence, identical distribution and finite variance. Let Xn be a sequence of independent, identically distributed (IID) random variables. It is assumed that X has finite mean μ = E(x) and finite variance var(X) = σ2. We then observe its normalized average as:

The CLT then states that Zn converges point-wise to the cumulative distribution function (CDF) of a standard normal (Gaussian) random variable.[70]

The CLT is not necessarily limited to identically distributed random variables with finite variance.

There are, therefore, two different types of generalized CLT, for non-identically distributed random variables and for random variables with infinite variance.We now discuss a generalized theorem for non-identically distributed random variables. We assume that Xn is a sequence of independent random variables, at least one of which has a non-degenerate distribution. We then define the partial sum and its variance:

We use the Lindeberg-Feller theorem to check the convergence of — using the Lindeberg condition for the CLT for non-identically distributed random variables. The Lindeberg condition is both necessary and sufficient for convergence. Let Fn be the CDF of Xn, i.e., Fn(x) = P(Xn < x). The Lindeberg condition is:

The Lindeberg-Feller theorem therefore holds and:

Sufficiency. If the Lindeberg condition holds, Sn converges to the distribution of a standard normal random variable.

Necessity. If ∣n converges to the distribution of a standard normal random variable, then the Lindeberg condition holds.

We now remove the assumption of finite variance while keeping that of independence, i.e., X0, Xi, X2 following IID:

Definition 6.1. The distribution of random variables is called stable if there is a positive c and a real d such that cX0 C d has the same distribution as aX1 C bX2.

We can check the convergence of the aggregation of random variables Xi for a < 2. Let F(x) be the CDF for X, and the slowly varying function h(x) so that:

Fig. 6.6 A generalized CLT of the Pareto distribution: a = 1.2, number of sums = 16, 128, 1,024. http://demonstrations.wolfram.com/GeneralizedCentralLimitTheorem/

F(x) will therefore look something like |x|“ in both the left and right tails. The aggregate random variables will be similar to the limiting distribution, giving a generalized CLT for infinite variance.

Figure 6.6 shows a simulation of the generalized CLT on the Pareto distribution9:

6.3