Conclusion

In this chapter we have developed a simple framework to study currency crises and assess the effects of monetary policy. This “third generation"model is particularly well-suited to analyze the case of economies such as those in Asia, where the source of currency crises lay primarily in the deteriorating balance sheets of private domestic firms and commercial banks rather than in uncontrolled budget deficit policies by local governments (e.g., see Mishkin 1999).

Three main conclusions emerged from our analysis. First, an economy with a large proportion of foreign currency debt is more likely to face currency crises associated with large recessions and currency devaluations; but the presence of large competitiveness effects will instead decrease the likelihood of a crisis. Second, a currency crisis may occur both under a fixed or a flexible exchange rate regime as the primary source of such a crisis is the deteriorating balance sheet of private firms. Third, public sector imbalances can have destabilizing effects on the domestic currency through the crowding out effects of public debt (especially public foreign currency debt) on the balance sheet and credit access of private firms.

A natural next step if this framework is to be used for policy purposes, is to empirically assess the relative importance of the various effects pointed out in the chapter. In particular, we need to learn more on the determination of actual foreign currency debt ratios, and also on the relative speeds of price versus interest rate adjustments as our analysis suggests that the optimal design of monetary policy, is potentially sensitive to the degree of price stickiness, or more precisely to the duration of the deviation from PPP following the initial shock.

Appendix: The Credit Multiplier

The credit multiplier mt is derived, as in Aghion et al.

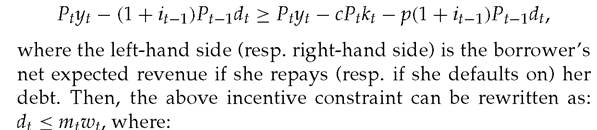

(1999b), from ex post moral hazard considerations. Namely, suppose that domestic entrepreneurs can either produce transparently and fully repay their loan or instead can hide their production in order to default on their debt repayment obligations. There is a nominal cost to hiding, which is proportional to the amount of funds invested: cPtkt. Yet, whenever the entrepreneur chooses to default, the lender can still collect his due repayment with probability p. Thus, the borrower will decide not to default if and only if:

The multiplier mt is increasing in the monitoring probability p (which in turn reflects the level of financial development of the economy) and it is decreasing in the real interest rate rt-1. The currency composition of debt does not affect mt since lending is determined before any shock occurs, that is at a time where both the PPP and the interest parity conditions hold.