Policy episodes and transition paths

A more informal approach to detecting the nature of policy effects on growth is to do episodic analysis - try to identify major policy reforms and simply examine what happened to growth and investment before and after.

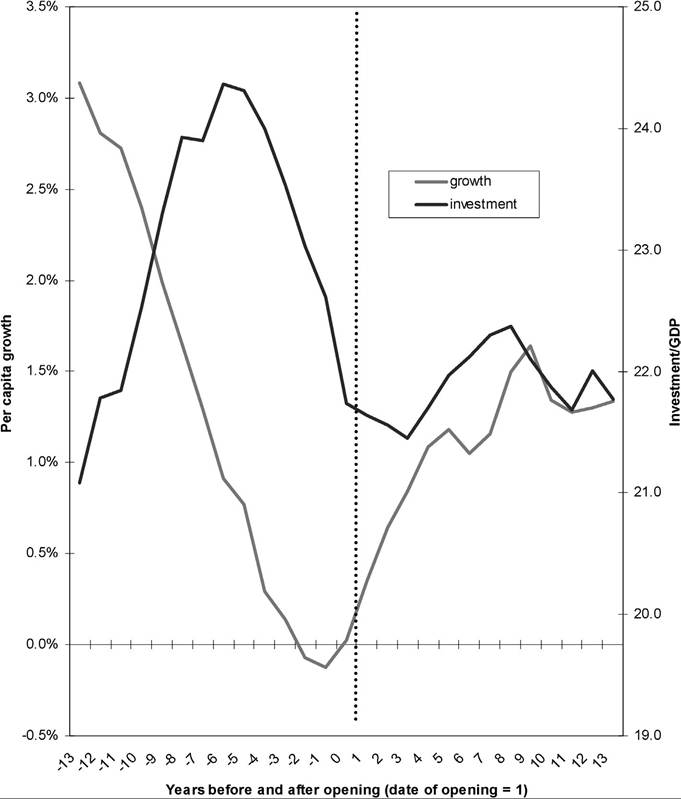

The shortcomings of this approach are that we do not control for other factors that affect growth and that it is somewhat arbitrary to define what are “major policy reforms”. The advantage is that we can see the annual path of growth rates and thus get a better test of the different prediction for post-reform transitional dynamics made by the models in the theoretical section.One ambitious attempt to identify major policy reform episodes was made by Sachs and Warner (1995). Sachs and Warner rate an economy as closed if any of the following hold: (1) a black market premium more than 20 percent, (2) the government has a purchasing monopoly at below-market prices on a major commodity export, (3) the country has a socialist economic system, (4) non-tariff barriers cover more than 40 percent of intermediate and capital goods imports, and (5) weighted average tariff of more than 40 percent on intermediate and capital goods. Note that only some of these criteria have anything to do with “trade openness” in the usual sense, as pointed out by Rodriguez and Rodrik (2001). The important thing for my purposes is that Sachs and Warner identify the dates of “reform” according to these criteria. I utilize an updated series of Sachs- Warner openness that goes through 1998.[603] I pick out countries with at least 13 years of growth data after opening. Since most openings happen towards the end of the sample period, this limits the sample of countries to only 13: Botswana, Chile, Colombia, Costa Rica, Ghana, Guinea, the Gambia, Guinea-Bissau, Israel, Mexico, Morocco, New Zealand, and Papua New Guinea. Figure 16 shows the path of growth and investment before and after opening, after first smoothing each country’s series individually with an HP filter.

The results do not support any of the above policies and growth models very convincingly. Investment is completely at variance with the predictions for its transitional path. Growth does show a steady acceleration after opening. This could be either a symptom of increasing returns or simply a process of increased credibility as the reforms take hold. Note however that growth was highest many years before the opening. Perhaps the story of closed and open economies is something more complex like temporary high growth under import substitution, which eventually crashed, followed by an opening of the economy and a partial recovery of growth.

Figure 16. Growth and investment before and after opening economy in 13 countries.

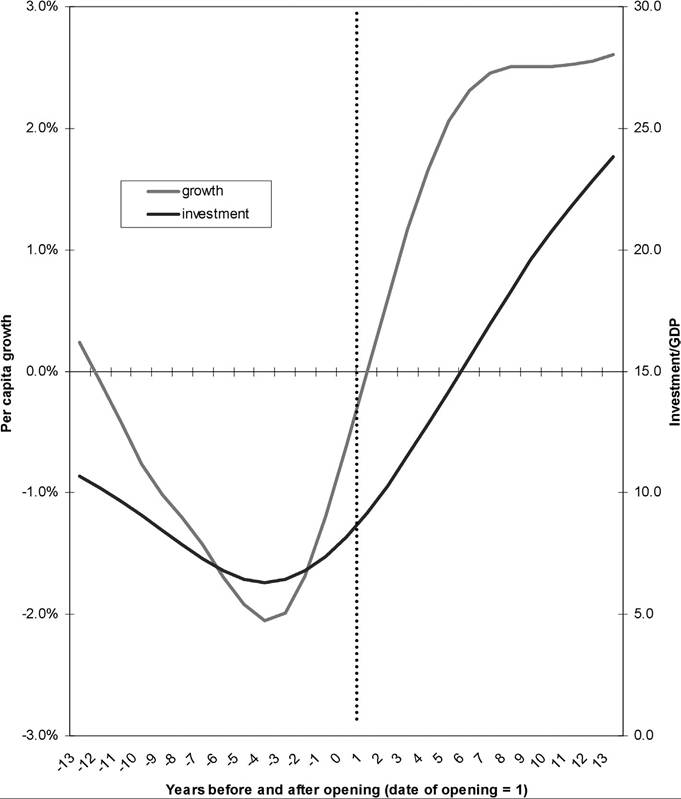

One of the few cases to fit the predictions of growth models as to transitional dynamics is Ghana, where both investment and growth increase after opening. Both keep rising after the date of opening, again supporting either an increasing returns story or increasing credibility of reform (see Figure 17).

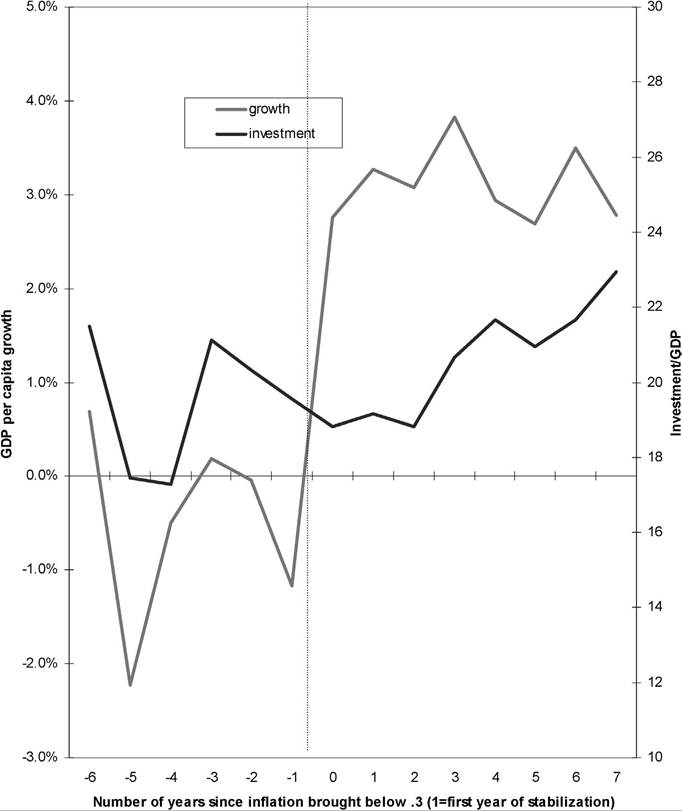

Another type of reform that lends itself to transition analysis is stabilization from high inflation. I record episodes of high inflation as following the above definition (log

Figure 17. Growth and investment before and after opening economy in Ghana.

rate of inflation above 0.3). I measure years of high inflation prior to stabilization, and then years after stabilization when inflation remains below 0.3. I require that there be at least two years of high inflation to rule out one-time spikes in the price level. The first year after inflation comes down is recorded as year 1. Figure 18 shows the behavior of growth and investment before and after inflation comes down. Growth fits the prediction of theoretical models in jumping to a higher path immediately after inflation comes

Figure 18. Investment and growth after inflation stabilization.

down. We only have a large enough sample for 7 years after inflation comes down, but growth seems to remain fairly constant post-stabilization. Investment fails to fit the transition predictions of any of the models.

We are left with a somewhat mixed picture. There is a fairly rapid growth effect after policy reform, either accelerating or constant. Investment in physical capital does not seem to respond to reforms in the way predicted by growth models. Of course, causality is up for grabs. There is also still the extreme policies problem, as episodes in which the country was closed or inflation was very high reflect asymmetrically destructive policies; it is not surprising that growth rebounds after these policies are terminated.

7.