Reconsidering the Law of Supply and Demand in the Free Market

Michio Morishima was a great twentieth-century economist, rare in recognizing the function of auctions (Morishima 1984). Many economists describe an auction mechanism as either a batch or Itayose auction, since these are both realistic forms.

In a pure form, however, the idealized auction mechanism is different. We therefore first consider the auction mechanism proposed by Morishima. He suggested that an actual auction may be incomplete. In this “ideal Walrasian auction”, no trades will be contracted until equilibrium has been confirmed. The auctioneer must behave neutrally and provide no information to any one trader about the situation of others.Maurice Potron (1872-1942) was a French Catholic priest who was also interested in mathematical economics, thanks to his interest in the stuff of ordinary life, such as bread (Bidard et al. 2009). Potron used the Perron-Frobenius theorem (Frobenius 1908,1909; Perron 1907) in his model as early as 1911, and in doing so anticipated some aspects of Frobenius’s (1912) generalizations. The importance of this theorem for economic theory was really only acknowledged after the Second World War. Since they were writing in the late nineteenth and early twentieth centuries, it is perhaps not surprising that these economists focused on bread as the main object of an auction. In this chapter, we will show the transition of trading methods in parallel with the change in what is being traded, from real to financial commodities.

4.1.1 The Classical Auction with Complete Ignorance of Others’ Preferences

The market is normally regarded as unfair if any participating agent knows in advance the situation or preferences of any other. A classical auctioneer coordinates a set of orders, but without collecting all asks/bids from the participating agents. In this context even a sealed bid may violate the fairness of the market.

The classical theory of auctions therefore works on the assumption of complete ignorance. This implies that the auctioneer does not employ any cumulated form of supply or demand, i.e., the supply/demand curve. The visible curves may no longer be compatible with the assumption of ignorance. We now examine a numerical example (Morishima 1984).Without ignorance of personal information, we can immediately construct the supply curve by combining the orders at each price starting with the lowest (the market order), and the demand curve by combining the orders starting with the highest price (the market order). These curves are therefore independently derived. We call this the collective method. Using a numerical example we then verify that the classical procedure results in the same equilibrium as the collective method (Table 4.1).

Table 4.1 Classical auction 1

| Seller | Price | Quantity | Buyer | Price | Quantity |

| A | MO | 300 | E | MO | 400 |

| B | 20 | 300 | F | 23 | 100 |

| C | 21 | 200 | G | 22 | 300 |

| D | 22 | 100 | H | 20 | 300 |

MO: Market Order

Source: Table 8 in Aruka and Koyama (2011)

| Asking price | Ask | Bid | Balance |

| ~19 | 300 | 400 | +100 |

| 20 | B300 | H300+MO100 | +H100 |

| 21 | C200 + H200 | F100 + G300 | ±0 |

Note: MO will be matched first, then H.

H200 purchased at ¥20 is resold at ¥21, because H only desired to buy at the price lower than ¥21

4.1.1.1 A Numerical Simulation

Provided that the auctioneer holds to the ignorance of personal information, we do not have any means of combining prices in this way. We therefore need a different method to find an equilibrium.

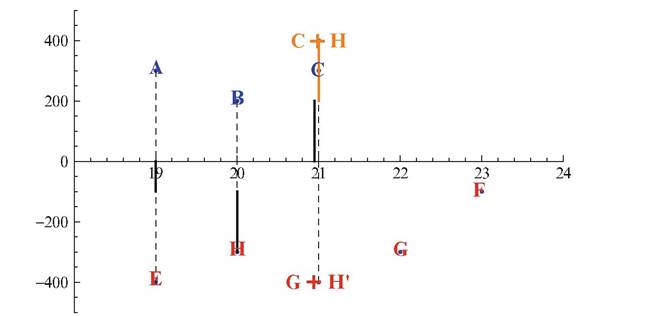

Market custom prescribes the initial settlement of market orders, leaving an excess demand of 100. Custom also requires the asking price to be quoted from the lowest, and bids from the highest. This custom regulates matching to control direction. It is readily apparent that custom could guide sellers and buyers to match at an equilibrium price. The demand may then be appropriated from Seller B, who wants to sell 300 at ¥20. This creates availability of 200 at ¥20. At ¥20, Buyer H can purchase 200 but still wants a further 100. As the quoted price is raised to ¥21, H may prefer not to purchase. H can, however, cancel the obtained right to 200 at ¥21 because H demanded only 200 at ¥20 or less. Buyer H must then become Seller H of 200 units as the quoted price becomes ¥21. At a price of ¥21, there are C C H = 400 units on the sellers’ side and F C G = 400 units on the buyers’ side. The price of ¥21 is therefore an equilibrium one, and cannot be blocked by any further ask or bid. If D tries to sell 100 at ¥22, nobody will buy it. If B tries to sell 300 units at ¥20, there will be no other seller at ¥20, so B cannot fulfill the total demand for 400 units. ¥21 is therefore an equilibrium price. This is shown in Fig. 4.1.

4.1.1.2 An Equilibrium Quantity

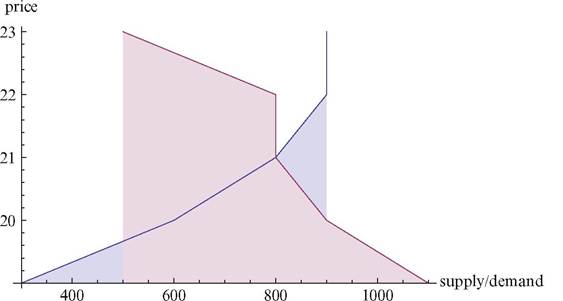

Until arriving at ¥22, the total orders on the sellers’ side may vary by price from A100 at ¥ 19; to 100 C B300 C H200 = 600 at ¥20 and 600 C C200 = 800 at ¥21. Thetotal orders from buyers may vary fromE400CF100CG300CH300 = 1,100 at

Fig.

4.1 Classical matching

Fig. 4.2 Intuitive demand and supply curves

the price ¥19 to 1100 - H200 = 900 at ¥20, 900 - H100 = 800 at ¥21 800 at ¥22; and 800 — G300 = 500 at ¥23. At ¥21, A, B and C have therefore sold their stocks while E, F and G have purchased. The right-hand side of Fig. 4.2 shows a matching process that may lead to the same equilibrium as the supply and demand curves based on the collective method, except for multiple equilibria. We employ the rule of re-contracts and evaluate which orders are finally feasible at the equilibrium price, after eliminating the previous re-sales or re-purchases. In the collective method, we do not need to do this.

Agent H, who can become a seller instead of a buyer by reselling his purchases, has a particular role.

Under the assumption of ignorance, as we saw above, Agent H must recover his income by reselling previously purchased stock at the previous price. This kind of transaction is irrelevant to other activity. This handling would be invalid if the ignorance clause was relaxed. In other words, this additional behavior of reselling will be deleted in the collective method by the independent supply/demand curve. Other steps are required to detect equilibrium with the assumption of ignorance.

4.1.2 Auctions in the Financial Market

As we saw, the above tatonnement may derive the same equilibrium as the collective method, i.e., the supply and demand curves, as long as the local equilibrium is the same. The collective method provides the participants with all the information about supply and demand. This knowledge is sufficient to activate agent reactions to the configuration of orders to bring about the second stage of coordination. This may no longer be based on the original preferences but instead interactive effects among the agents.

4.1.2.1 A Welfare Implication in Financial Market Auctions

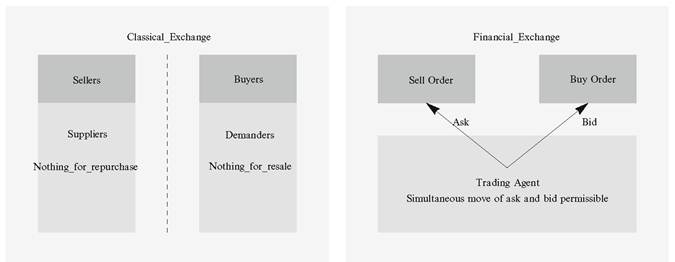

We can suggest an alternative rule, the financial market rule.

Here, a buyer could become a seller, or vice versa. In the financial market, “buyer” or “seller” are temporal forms, which change over time. The transition from buyer to seller must be realized in the financial market. In the example above, the buyer who temporarily gives up his demand can wait for a future price rise to sell, so this is only a bifurcation step that divides the welfare meanings of trades between the Walrasian and financial steps. In the latter, an agent wants extra profit, so must bet or gamble on rising prices.In the Walrasian tatonnement, however, any agent only expects to fulfill his original desire, following the classical economic idea of fairness. If we move away from this, we can easily diverge the market allocation from the original set of demand and supply. This divergence may often induce the market to float away from the real distribution of supply and demand, because many trades realized may be the by-products of psychological interactions among agents. Even in these interactions, the collective method may be constructed, as in a batch or Itayose auction. The collectively composed supply and demand curves may not have any detached ground. The agent’s expectation drives strategy (buy, sell, or nothing) as well as the reactions of other agents. Added orders are the results of interactive

Fig. 4.3 Classical and financial exchanges

summation, so the collective curves may no longer reflect the classical curves constructed using the agents’ independent preferences (Fig. 4.3).

According to Arthur (2009, p. 154), it is not quite correct to say that derivatives trading ‘adopted’ computation:

That would trivialize what happened. Serious derivatives trading was made possible by computation. At all stages from the collection and storage of rapidly changing financial data, to the algorithmic calculation of derivatives prices, to the accounting for trades and contracts computation was necessary.

So more accurately we can say that elements of derivatives trading encountered elements of computation and engendered new procedures, and these comprised digitized derivatives trading.Large-scale trading of derivative products took off as a result.

4.1.2.2 The Historical Alteration of Trading Methods from the Classical Collective Method to the Double Auction

As mentioned at the beginning of Chap. 3, the keen interest in the theory of price and production that dominated the 1920s and 1930s had decreased drastically by the early 1970s. Similarly, there had also been an alteration in trading methods, from the classical collective method to the double auction. We use the phrase ignoratio elenchi for this change, which is often characterized as “irrelevant conclusion”, indicating a logical fallacy that consists in apparently refuting an opponent, while actually disproving something not actually asserted for either market:

The collective method could be valid in some cases for both the Walrasian free market and the contemporary financial market to find equilibrium. We must, however, be careful as the results obtained have different meanings for

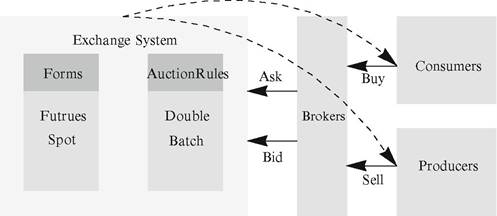

Fig. 4.4 Exchange system

the two markets. The financial market is the institution or the set of rules required to activate the trading, and may never guarantee certain welfare for the participating agents. In futures trading an element of gambling is introduced. If we regard both free markets as sharing the same functions, we will have ignoratio elenchi.

If any agent has not decided whether to act as seller or buyer before entering the market, that agent’s preference could simply depend on interactive reactions. If the agent also has dealings in the futures trade with leverage, they can only play a psychological game in seeking profit. This game is then irrelevant to the real economy, even though it contains some indirect linkage to reality. These collective dynamics are irrelevant to optimal allocation, but an essential feature of the futures market. As econophysics has proved, therefore, high volatility produces still higher volatility.

The collective method for determining supply and demand can no longer hold in the general ask/bid auction or double auction. This means that we will struggle to obtain any useful analysis of the financial market using the supply and demand curves.

In short, as we noted before, price no longer plays a crucial role in the economy, and the equilibrium price system is no longer the sole decisive factor in the fulfillment of trades. This suggests that a replacement of the trading method will occur, which has been seen in the move away from batch auctions towards continuous double auctions. This is also reflected in the metamorphosis of production shown in a service-dominant economy (Fig. 4.4).

4.1.2.3 The Ask and Bid Auction

The initial price on resumption after a trade halt—for example, overnight on stock exchanges—is established by the ask/bid method. This is usually employed on

Table 4.2 Ask and bid auctions

| MO for sell | Ask (Sell) | Price | Bid (Buy) | MO for buy |

| 15 | 1,798~ | 30 | ||

| 15 | 82 | 1,798 | 30 | |

| 15 | 73 | 1,793 | 30 | |

| 15 | 38 | 1,779 | 30 | |

| 15 | 44 | 1,778 | 30 | |

| 15 | 91 | 1,776 | 30 | |

| 15 | 1,770 | 37 | 30 | |

| 15 | 93 | 1,763 | 6 | 30 |

| 15 | 57 | 1,759 | 23 | 30 |

| 15 | 1,758 | 34 | 30 | |

| 15 | 1,741 | 71 | 30 | |

| 15 | 1,733 | 30 | ||

| 15 | 1,729 | 30 | ||

| 15 | 1,719 | 30 | ||

| 15 | 1,684 | 21 | 30 | |

| 15 | ~ 1,684 | 30 |

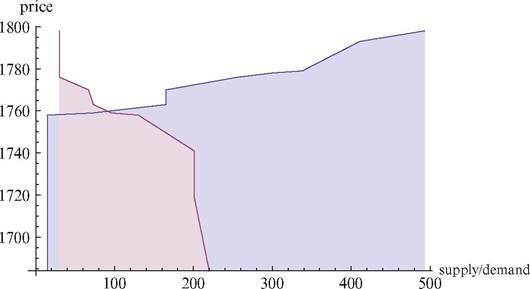

| Supply | Price | Demand |

| 493 | 1,798~ | 30 |

| 493 | 1,798 | 30 |

| 411 | 1,793 | 30 |

| 338 | 1,779 | 30 |

| 300 | 1,778 | 30 |

| 256 | 1,776 | 30 |

| 165 | 1,770 | 67 |

| 165 | 1,763 | 73 |

| 72 | 1,759 | 96 |

| 15 | 1,758 | 130 |

| 15 | 1,741 | 201 |

| 15 | 1,733 | 201 |

| 15 | 1,729 | 201 |

| 15 | 1,719 | 201 |

| 15 | 1,684 | 222 |

| 15 | ~ 1,684 | 222 |

Table 4.3 Supply and demand in ask/bid auctions

stock exchanges for the opening and closing prices in both morning and afternoon sessions. The price when a special quote is indicated is also determined by this method. The rest of the time, the Tokyo Stock Exchange at least uses the double auction method (Tables 4.2 and 4.3; Fig. 4.5).

Fig. 4.5 Supply and demand curves

4.1.2.4 English Auctions and Dutch Auctions

There are two main alternative auction rules: Dutch and English. Given a single order book, two kinds of equilibrium can usually be achieved. This result suggests that the idea of equilibrium depends on the rule employed. In Dutch auctions, the auctioneer quotes the prices in descending order. In English auctions, they are quoted in ascending order. Let si{p) be the quantity supplied by agent i at price p, and di the demand of agent j at price p. The necessary conditions for establishing equilibrium are:

English auction The total balance of supply at the quoted price is smaller than the total balance of demand at the same quoted price.

Dutch auction The total balance of supply at the quoted price is greater than the total balance of demand at the same quoted price.

It is clear that equilibrium is always unique for the strict equality case. In these cases, we need piecemeal stipulation. In an auction session, any orders remaining after settlement will be carried over to the next session. The equality case will not necessarily hold in the discrete price change actually employed. We will only guarantee a unique equilibrium in the case of imaginary continuous change.

Now we take an example to show two equilibria. In this numerical example, for simplicity, we drop the market orders on both sides of ask and bid (Tables 4.4 and 4.5).

| S | Price | D |

| 165 | 1,770 | 67 |

| 165 | 1,769 | 67 |

| 165 | 1,765 | 67 |

| 165 | 1,764 | 67 |

| 165 | 1,763 | 67 |

| 165 | 1,762 | 73 |

| 165 | 1,761 | 73 |

| 165 | 1,760 | 73 |

| 72 | 1,759 | 96 |

| 15 | 1,758 | 130 |

Table 4.4 Two equilibria in ask and bid auctions

| Supply | Price | Demand |

| 493 | 1,798~ | 30 |

| 493 | 1,798+ | 30 |

| 411 | 1,793 + | 30 |

| 338 | 1,779+ | 30 |

| 300 | 1,778+ | 30 |

| 256 | 1,776+ | 30 |

| 165 | 1,770 E/.),,,,;, | 67 |

| 165 | 1,763 | 73 |

| 72 | 1,759 e⅛ | 96 |

| 15 | 1,758* | 130 |

| 15 | 1,741* | 201 |

| 15 | 1,733* | 201 |

| 15 | 1,729 * | 201 |

| 15 | 1,719* | 201 |

| 15 | 1,684* | 222 |

| 15 | ~ 1,684 | 222 |

Table 4.5 The same equilibria finely resolved

4.1.2.2 The Interactive Environment-Dependent Process

for Matching in the Futures Market

Realistically, agents may arrive or leave this market randomly. We can therefore no longer presume a perfect collection of asks and bids during a unit of time, even employing the collective method of supply and demand. It is easy to verify that we have invalidity of the supply and demand curves in the case of a continuous double auction.

In the market system, any agent can be either a seller or a buyer. In a trade, there must be a constant quantity for supply and a given array of bids. The set of both ask and bid orders should not be changed within the unit time duration, whereas either in the batch auction or the double auction, we can presume a variable stock of supply, because any order can be accepted within one period of time. However, this assumption leads to a variable environment around the trade in any given period. Given a variable environment, it is better to employ the master equation dynamics for solving the equilibrium of trading. It is still not known whether this solution is equivalent to an auction solution, so we must observe that we have different notions of equilibrium between constant and variable environments at a given time.

An agent may intermittently arrive at the market. The arrival rate can change, and the agent’s order is unknown, as is their mode of trading: sell, buy, or nothing. It therefore becomes important for the stock exchange system to induce all the agents to decide their trades by exhibiting a feasible price range. The way to do this is an institutional technique linked to a historical custom.

4.2