The U-Mart System and Historical Background

4.2.1 The U-Mart System Approach to the Futures

Stock Market

In the final quarter of the last century, the futures market operation became a conspicuous feature of the global economy.

However, many econophysicists remain interested in price formation and distribution in spot markets, partly because of limitations of data availability. The U-Mart system (Shiozawa et al. 2008) is an AI market system to implement a virtual futures market with reference to the actual stock price index arbitrarily chosen, using agent-based simulation techniques. This system contains spot market trading as a special case. Agents must finally clear trades by the spot price at the end of trade (delivery date). A hybrid approach is employed in this system in the sense that a human agent can always join in the machine agent gaming setting.[50]There are two important features of the U-Mart system. An agent, whether machine (i.e., algorithm) or human, does not presume a certain personal rational demand function in advance (Koyama 2008; LeBaron 2006). The system adopts a hybrid approach, and a human agent can always join in the machine agent gaming setting. The latter is a technological feature, a new network innovation of an AI market system, while the former is an alternative approach to the neoclassical method.

The implementation of the rational demand function into the exchange system, and attempts to operate its artificial market, must not be realistic, because the market fluctuations require each agent to update or reconstruct their own demand function in each trading session. In this case, neoclassical computation should not be achieved. In the U-Mart system, therefore, any machine agent behaves according to its ‘technical analysis’ base. Each agent also uses a so-called technical analysis to estimate pricing on their own empirical base.

Otherwise, trading may place a heavy strain on the human brain or computer.Zero-intelligence agents (Gode and Sunder 1993) can earn in both the spot and futures market. We can easily show that the U-Mart system could be a test bed to analyze the behaviors of zero-intelligence agents in both markets. We also show why they can compete with intelligent agents to win the game, by employing a random strategy algorithm as the arbitrage mechanism and using position management by a trading agent. This will be explained further in Sect.4.3.

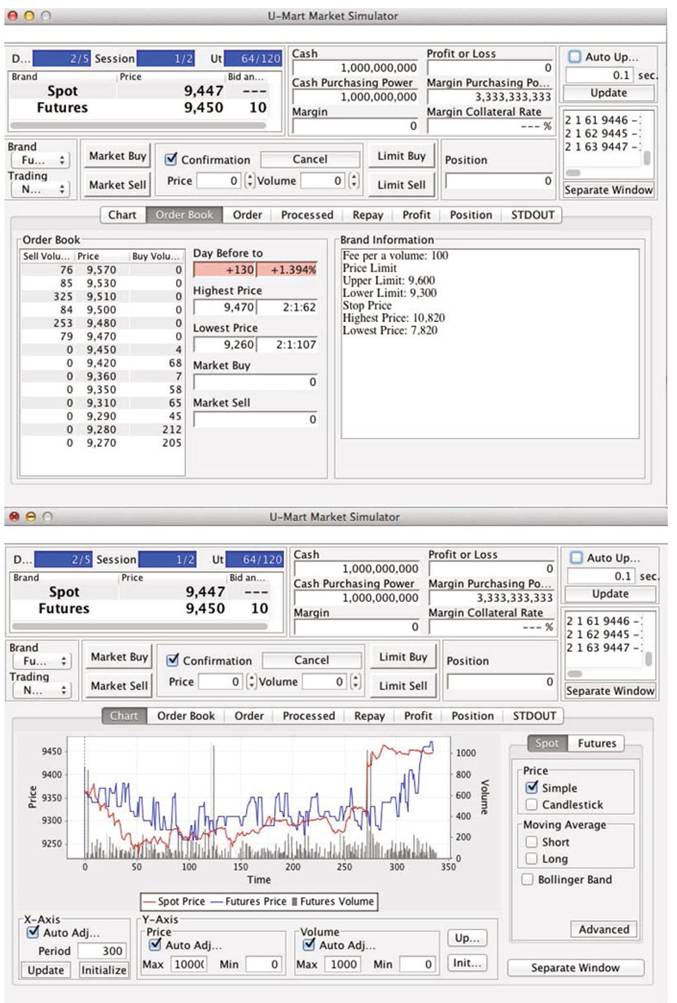

Japanese technology was advanced enough for Japan to be the first country in the world to construct a complete futures stock market. An examination of the differences between auction methods will clarify that they are institutionally sensitive. Theoretically speaking, the double auction in the stock exchange is a kind of continuous auction, but is bound by various rules and customs. These details are carefully fulfilled in U-Mart ver.4 as shown in Fig. 4.6. The Tokyo Stock Exchange therefore uses a Japanese term, “Zaraba”, which equates more to the English term “double auction” than “continuous auction”.[51]

We can show that the U-Mart system can easily produce a situation where nothing happens. A small perturbation of one parameter in the strategy could generate trading even if all the agents should employ a similar strategy with slightly changed parameters. Such a perturbation may make the dealing very effective.

4.2.2 Historical Background to the Tokyo Stock Market

The modern Tokyo Stock Exchange (TSE) inherits all its traditional terms from the Osaka Dojima Rice Exchange (Taniguchi et al. 2008). The Osaka Dojima was the first complete futures market in the world, with trading approved by the Shogun government in 1730, over 100 years before the Chicago futures market was founded. The Osaka Dojima is recognized by many authors as the first complete futures market in the world. Although a rice exchange, it contained no rice because of limited space.

Instead, traders exchanged securities called rice stamps.[52]

Fig. 4.6 U-Mart ver.4 GUI for the terminal trader. Note: This simulator is called the “standalone simulator”, to distinguish it from the U-Mart Market Server

Fig. 4.7 Hand gestures in the Dojima Exchange and the modern electronic trade at TSE. The left-hand side panel is cited from the picture of the wrapper of the book: Shima (1994). The righthand side panel is cited from Wikipedia: http://en.wikipedia.org/wiki/Tokyo_Stock_Exchange. Incidentally, the TSE trading floor using hand signs was closed on April 30, 1999, and replaced with electronic trading

The hand gestures typically employed in auctions survived until April 30, 1998, when the computer-based stock exchange was introduced.

A so-called circuit breaker, only introduced into the New York Stock Exchange after “Black Monday” in 1987, was implemented in the Dojima Exchange from the start. It is said that there were about 1,000 trading experts (brokers) working there at any time. This exchange continued to play an essential role in setting the standard rice price for the population of Japan throughout the eighteenth century (Fig. 4.7).

The two terms used for auctions in Japan, Itayose and Zaraba, are equivalent to the Western terms batch auction, a double auction on a single good to trade multiple units in sealed bid format, and double or continuous auction, an auction on a single good to trade multiple units in an open bid format.

Many economists use the term “auction” very generally, even where the market mechanism often cannot be identified as a simple auction.

4.3