Somefacts about volatility in the United States

Three main empirical predictions emerge from the model in this chapter, namely:

1. The ratio of debt-obligations to firms' cash flow should peak toward the end of a boom, and thus increase sharply during the transition from a boom to a slump;

2.

The effective interest rate faced by the corporate sector is procyclical;3. The interest rates spread (e.g. the interest rate differential between 10-year bonds and 3-month commercial paper) should also increase sharply during the transition from a boom to a recession. The reason is that at the end of booms, firms have accumulated high levels of (long-term) debt and therefore face a high risk of bankruptcy or default over any new (long-term) debt issued during this period compared to the long run. Hence, it becomes hard for them to obtain further long-term credit, all they can hope for is to obtain short-term credit. This, in turn implies that the relative demand for short-term credit will increase sharply toward the end of booms.

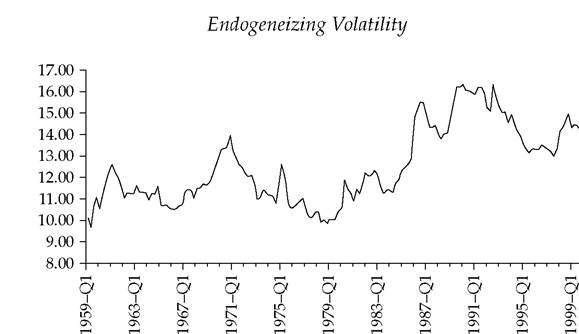

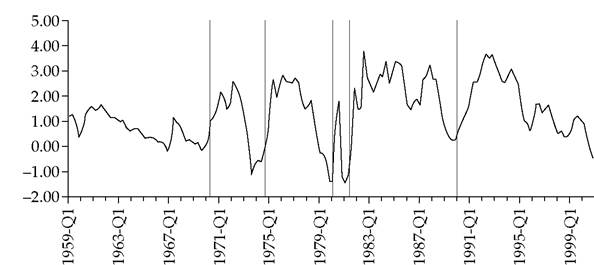

The above model is of a (large) closed economy. Therefore the United States is a natural place to look for supporting evidence. And as it turns out, these predictions appear to be borne out by the data, at least until the early 1990s. Figure 3.9 below shows the dynamic evolution of the debt/cash flow ratio over the period 1959-99. The vertical bars correspond to the lowest point of recessions, and one can see that, almost always, the debt/cash flow sharply increases either during the recession or right before. Figure 3.10 shows the evolution of the 10-year and 3-month interest rate spread over the same period, and again it appears that in most cases the spread sharply increases during a recession.[9] In fact, the above predictions fit the US data particularly well before the mid-1980s. From 1959 until 1983, high debt/cash flows and/or

65

Fig. 3.9 Debt/cash flow ratio.

Fig. 3.10 10-year and 3-month spread.

high spreads are good predictors of a forthcoming recession, and the average interest rate incurred by firms is indeed highly procyclical, as shown by Friedman and Kuttner (1993). However, since the mid-1980s, macroeconomic volatility in the United States appears to be lower, recessions occur less often, and the correlation between credit indicators and recessions becomes much weaker. This might reflect the increasing financial sophistication of the US economy, which as in our model, insulates the economy from credit-driven cycles.