The Trade-Off Between the Real Economy and the Financial Economy, and the Differential Effects on Each

Finally, I discuss a recent interactive financial process. The story of globalization, since the 1990s, has been around a very limited number of international investment banks. Globalization was driven by over-saving worldwide, typically observed in pension funds, accumulated by the baby-boom generation born just after the Second World War.

Over-saving must be compensated for by investments. But investments must be financial. The investment banks therefore invented a series of financial commodities to satisfy this need for investment products.To do so, they needed a new design for financial capitalism. The selected design was a system of reassurance, which was set in an attractive system to transform loans into assets via investment partnerships outside the official stock exchange. The reassurance market became a symbol of this new form of capitalism, created solely to absorb individual savings. The debt bond swap was actually a classical way to absorb a potential surplus of money, often seen in feudalistic or medieval society. In other words, the idea is obsolete in a sense. Under this new mechanism, a financial network grew rapidly, but this explosive expansion, with its accompanying ups and downs, is closely connected with asymmetrical option trading, which always leads to over-inflated prices. Since modern option trading is on the margins, and without recourse to the main market, we can no longer estimate the true transaction balances. This has come about as a natural result of its institutional settings.

As the collapse of Lehman Brothers showed clearly, private bankruptcies involving large amounts of money need to be remedied by government. This has led to two diverging features: a quick recovery in the financial sector, and slow progress for many national economies. In the US economy and that of other countries, in particular Japan, national savings are falling fast. The United States reached negative national savings in the 1990s, and Japan is rapidly following suit, experiencing negative national savings in the 2010 fiscal year (although a change of accounting operations meant that the amount was formally nearly zero).[12] The financial crisis is having an effect on national wealth on a global scale.

There is a trade-off between financial balance and real economic values such as GNP. This is why it is impossible to separate the affairs of any one country from international financial matters. Large amounts of money, exceeding the sum of the US and Japanese GDP, have flowed offshore from domestic economies, although this does not take account of movement of money derived illegally, otherwise known as ‘shadow movement’.[13]

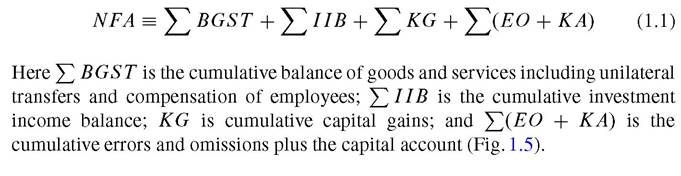

Habib (2010, p. 15) published some figures of net foreign assets (NFA), i.e., excess returns on net foreign assets.

1.8

More on the topic The Trade-Off Between the Real Economy and the Financial Economy, and the Differential Effects on Each:

- INTRODUCTION

- Chapter 34 Gynecologic Procedures

- Cossack Tatar Fighters

- Diagnosis of Bovine Tuberculosis in Zambia