Theoretical models that predict strong policy effects

The simplest theoretical model of endogenous growth is the AK mode of Rebelo (1991). Rebelo postulated that output could be proportional to a broad concept of capital (K) that included both physical and human capital:

Y = AK.

(1)In principle, K could also include any kind of stock of knowledge, technology, or organizational technique that can be built up over time by sacrificing some of today’s consumption to accumulate such a stock. For example, technological knowledge could be accumulated by diverting some of today’s output into lab equipment or other machines that help make new discoveries feasible. Or knowledge or human capital itself could be used to create further knowledge or human capital rather than producing today’s output.1 However, unlike many other endogenous growth models that explicitly address knowledge or technology [e.g. Aghion and Howitt (1998)], K is treated in this model as a purely private good - both excludable and rival. I will address below what happens when we relax this assumption.2

Constant returns to the factors that can be accumulated is also a key assumption in this model’s prediction of a constant steady state rate of growth for given parameters and policies. This would rule out fixed costs in implementing a new technology, or increasing returns to accumulation at low levels of K, both of which feature in other growth models.

Since K is purely a private good, there is no role for government in this model. The market equilibrium yields the first best solution, and any government intervention in the form of taxes or price distortions must worsen welfare.

In this model, policies like tax rates have large effects on steady state growth. Consider first a tax (τ) on the purchase of investment goods (I). Consumption (C) is given by output less investment spending and taxes:

Suppose the population size is constant and each (identical) household-dynasty maximizes welfare over an infinite horizon:

1 Rebelo (1991) showed that as long as the capital formation function itself has constant returns to accumulated factors, endogenous growth is possible even if final production has diminishing returns to capital.

2 Since K in my models can always represent either technology or factor accumulation, I do not address the hot debate on how much factor accumulation matters for growth. On education, Benhabib and Spiegel (1994) and Pritchett (1997) show that cross-country data on economic growth rates show that increases in human capital resulting from improvements in the educational attainment of the work force have not positively affected the growth rate of output per worker. It may be that, on average, education does not effectively provide useful skills to workers engaged in activities that generate social returns. There is disagreement, however, Krueger and Lindahl (2001) argue that measurement error accounts for the lack of a relationship between growth per capita and human capital accumulation. Hanushek and Kimko (2000) find that the quality of education is very strongly linked with economic growth. However, Klenow (1998) demonstrates that models that highlight the role of ideas and productivity growth do a much betterjob of matching the data than models that focus on the accumulation of human capital. More work is clearly needed on the relationship between education and economic development. On physical capital accumulation, there is the debate between the “neoclassical” school stressing factor accumulation [Mankiw, Romer and Weil (1992), Mankiw (1995), Young (1995)] and the school stressing technology or the residual [Klenow and Rodriguez-Clare (1997a, 1997b), Hall and Jones (1999), Easterly and Levine (2001)].

Then the consumer-producer would invest at a rate that results in steady-state growth of

Here policy has large effects on steady state growth. If A = 0.15 and σ = 1, then an increase from a tax rate of 0 to one of 30% would lower growth by 3.5 percentage points. Such a policy pursued over 30 years would leave income at the end 65 percent lower than it would have been in the absence of a tax.

This is a strong claim for the effects of policy on economic development! It offers a possible explanation for the poverty of a poor nation - bad government policies (high τ) - which can be remedied easily enough by changing to good policies (low τ). It is clear why this has been a seductive theory for aid agencies and policymakers that seek to promote economic development.The effects on accumulation are even more dramatic. Solving for the broad concept of investment that includes physical capital, human capital, technology, and knowledge accumulation, we get:

The effect of taxation on investment does not depend on A. If σ = 1, the derivative of I/Y with respect to the tax factor 1/(1 + τ) is unity. An increase of the tax rate from 0 to 30 percent would reduce investment by 23 percentage points of GDP!

Before examining this claim in more detail, note that the tax rate on investment goods does not have to be an explicit tax on capital goods. First of all, there is an equivalent income tax that would have had the same effect on growth (given by t = 1 - 1/(1 + τ)), so policies here could be any government action that diverts income away from the original investor in production. (Note using the result above, that every one percentage point increase in the income tax rate reduces investment by one percentage point of GDP) Second, note that this result applies to the marginal effective tax rate on investment goods or income. While movements from 0 to 30 percent would be dramatic for average tax rates, a movement of 30 percentage points in marginal effective tax rates could easily come from a tax reform. Second, the tax on capital goods could stand for any policy that alters the price of investment goods relative to consumption.[591] For example, suppose that a populist government controls output prices for consumers but the investor must buy goods for investment on the black market.

Then the premium of the black market price over the official price would act much like a tax on investment goods. If the one good in this model is tradeable, then the black market premium on foreign exchange might be a good proxy for the wedge between official output prices and black market investment good prices (assuming that consumer goods can be imported at the official exchange rate, or at least that official output prices are controlled as if they could be). If we suppose that the purchaser of investment goods must hold cash in advance of a purchase of investment goods, then inflation would be indirectly be a tax on investment goods. One could also get similar results with institutional variables - a probability of expropriation of part or all of the capital good by the government or government officials demanding a bribe every time a new unit of capital is installed would act much like a tax on investment.The claims for large policy effects become even stronger in growth models with increasing returns to capital and externalities. Suppose that there is a group of large but fixed size where the capital held by each member of the group has non-pecuniary externalities for the rest of the group. For example, a high human capital individual in a residential neighborhood might benefit the rest of the neighborhood with whom she socially interacts. The knowledge and connections that this individual brings might raise the productive potential of others (this is loosely what is called “social capital” in the literature). If this is true for all social interactions in the neighborhood, and these interactions are identical, costless, and exogenous for all members, then there will be a spillover from the average human capital of the neighborhood to each inhabitant of the neighborhood. The production function for an individual member would look like this:

One can think of other similar examples of spillovers.

If k includes knowledge or technology, it is plausible that these goods are non-rival and partially non-excludable. For example, firms may benefit by example from new technology installed by other firms in the same trade. People in almost every human activity engage in “shop talk” that is incomprehensible to outsiders, but which apparently conveys productive knowledge to those involved in the activity.4Assuming the same maximization problem as above (Equations (2)-(4)), then the individual will invest in k taking everyone else’s investment as given (because the group is too large for her to influence its average). The optimal path of consumption is now given by

However, since all members of the group are assumed to be identical, then k = k expost, and the growth rate for each individual will be

4 The emphasis on the special properties of knowledge and technology was highlighted by Romer (1995) and Aghion and Howitt (1998). The idea of social capital has been stressed by authors such as Putnam (1993, 2000), Glaeser, Laibson and Sacerdote (2002), Narayan and Pritchett (1997), Woolcock and Narayan (2000).

There are multiple equilibria if α + β — 1 > 0, i.e. if both the original importance of broad capital to production is large plus there are strong spillovers. If we have the special case of α +β = 1, then we are back to the AK model, albeit one with suboptimal market outcomes because of the externality. If α+β — 1 < 0, then the model will feature similar prediction as the neoclassical model with a high capital share (discussed below).

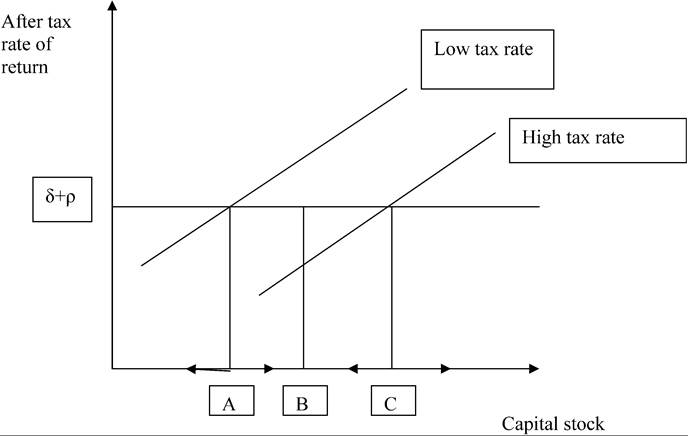

In the multiple equilibria case, the return to capital increases the more initial capital there is, the opposite of the usual diminishing returns to capital. Figure 1 illustrates the possible outcomes.

If the tax rate is low, the after tax rate of return to capital is the upper upward-sloping line. Any initial capital stock to the left of point A (where the after tax return is less than δ + ρ) will go into a vicious circle of negative growth of consumption and decumulation of capital. Any point to the right of A (such as B) will go into a virtuous circle of positive and accelerating growth of consumption and positive capital accumulation.[592] Now suppose that tax rates are increased, shifting the rate of return to the lower upward-sloping line in Figure 1. Now any point to the left of C will go into a vicious circle of decline. An economy with capital stock B, which was in the expanding region under low taxes, is now in the declining region under high taxes. A policy shift now has an even more dramatic impact on national prosperity - it could spell the difference between subsistence consumption (say Mali) and industrialization (say Singapore). Policy spells the difference in the long run between per capita income of $300 and $30,000 - rather a dramatic effect. As in all multiple equilibria models, initial conditions matter and small things (like policy) can have large consequences. If the first endogenous growth model was seductive to policymakers, this is even more so - one government official at the stroke of a pen could change a nation’s prospects from destitution to prosperity.This increasing returns model is much like poverty trap models like those of Azariadis and Drazen (1990), Becker, Murphy and Tamura (1990), Kremer (1993), and Murphy, Shleifer and Vishny (1989). It is also consistent with models of in-group ethnic and neighborhood externalities [Borjas (1992, 1995, 1999), Benabou (1993, 1996)] and geographic externalities [Krugman (1991, 1995, 1998), Fujita, Krugman and Venables (1999)]. Ades and Glaeser (1999) present evidence for increasing returns in closed economies.

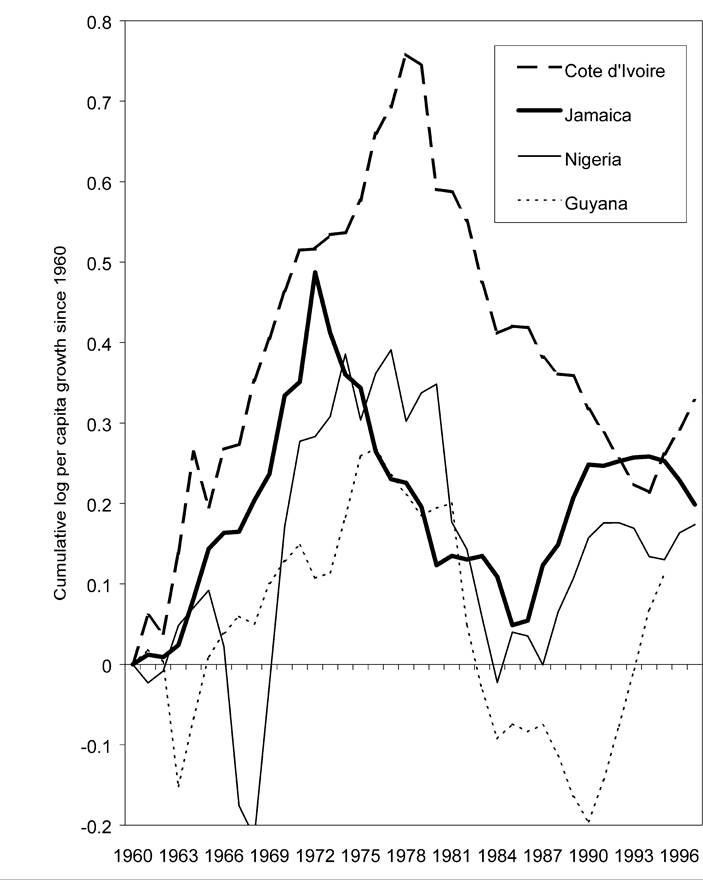

A story like that told in Figure 1 would also predict instability of growth rates if an economy is in the middle region B and is subject to continuous fluctuations in policies. The economy would keep shifting from positive to negative growth and back again as policies change. This is a possible story for some of the spectacular reversals in output growth that we have seen in countries like Cote d’Ivoire, Jamaica, Guyana, and Nigeria (see Figure 2).

It is often assumed that these strong claims for policy effects on growth are only a feature of endogenous growth models. However, the other innovation in the growth

Figure 1. Multiple equilibria with increasing returns to capital, alternative tax regimes.

literature of the last two decades has been to put a much higher weight on capital even in the neoclassical exogenous growth model. Again, the justification is that capital is a broader concept than just physical equipment and buildings. It should include at least human capital, if not the more technology and knowledge forms of capital discussed above. Attributing part of the labor income in the national accounts to human capital, this would raise the share of capital in output from around 1 /3 (if the only form of capital was physical) to something like 2/3.6 The high capital share is also necessary to avoid counterfactual predictions about very high returns to capital in capital-scarce countries, and the same in the initial years of a transition from capital-scarcity to capitalabundance.

The neoclassical production function with labor-augmenting technological change is:

In per capita terms, we have:

The consumer-producer's maximization problem is the same as before, using Equations (2)-(4). Technological progress (the percent growth in A) is assumed to take place

6 Mankiw, Romer and Weil (1992) and Mankiw (1995).

Figure 2. Examples of variable per capita income over time.

at an exogenous rate x. As is well known, accumulation of physical and human capital cannot sustain growth in the long run in the absence of technological progress. Since policy affects the outcome only through the incentive to accumulate capital, it follows that policy by itself cannot foster sustained growth in this model. With growth in A of x, the long-run steady state will have per capita output y, capital per worker k, and per capita consumption all growing at the same (exogenous) rate x. The tax rate on capital goods has no effect on the steady-state growth rate. However, policy does have potentially large effects on the level of per capita income. To see this, it is convenient to write both capital per worker and per capita income relative to the technological level A. The optimal growth of per capita consumption is now:

Since (12) must equal x in steady state, an increase in the tax rate τ must always be offset by a decrease in the relative capital stock (raising the pre-tax rate of return to capital because of diminishing returns, i.e. because a < 1). Setting (12) equal to x determines the k/A ratio in the steady state, which in turn gives the following for per capita income relative to technology:

A high tax on investment inhibits capital accumulation and thus lowers the level of income relative to the technology level. High taxes are still a possible explanation of relative poverty in the neoclassical model. With a capital share of 2/3 (including both human and physical capital), a tax rate decrease from 50 percent to zero raises income by a factor of (1.5)2, or 2.25 times. If the capital share were 0.8 (as writers like Barro and Mankiw have suggested), then the tax reduction would raise income by a factor of (1.5)4 or 5 times.

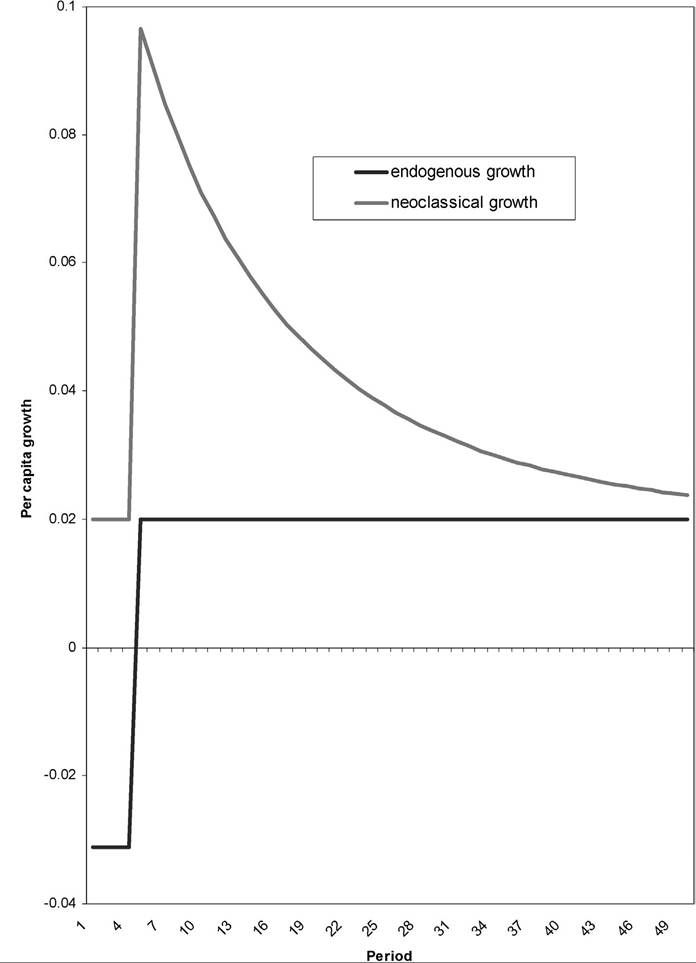

Although there is no effect of the tax change on steady state growth, there will be a dramatic change in growth in the transition from one policy regime to another. There is one unique saddle path to the new steady state; consumption will jump to that saddle path after the change in policy (in a world of perfect certainty of course). To solve for the transition involves solving for the saddle-path of consumption in transition to the new steady state. Figure 3 shows a simulation of a decrease in the tax rate on investment from 50 percent to zero, with the following parameter values:

For comparison, I also show a simulation of an endogenous growth rate model with A = 0.138, which gives the same 2 percent per capita growth rate at zero tax as the exogenous growth neoclassical model. Both models show dramatic growth rate effects after the policy change, still large after 20 to 30 years. It is only in the very long run that the neoclassical growth effect wears off with diminishing returns. Investment rates would show similar jumps after the policy change as growth rates.

Figure 3. Endogenous growth and neoclassical growth with a reduction of tax rate on investment from 50 percent to zero.

What is different for the purposes of empirical work is that the predicted difference in growth rates in the endogenous growth model before and after the tax decrease could equally apply to cross-section differences in growth between high-tax and low-tax countries. In the neoclassical model, the predicted effect of policy change on growth is only for a cross-time effect within countries. However, this difference has been handled in practice by testing the effect of current policies on growth, controlling for initial income. Initial income can be thought of as representing policy regimes prior to the period under study. If current policy predicts a higher steady state level of income than initial income, then the transitional dynamics like those shown in Figure 3 will be set in motion. The neoclassical model would predict instability of growth rates over time if frequent policy changes shift the steady state level above or below the current income level, which is ironically similar to the increasing returns prediction of growth rate instability.

One big difference between the three models is that the neoclassical model predicts falling growth and investment after the initial policy-induced increase in growth, the increasing returns to capital model predict rising growth and investment afterwards, while the constant returns to capital model predict constant growth. I will examine some case studies of major policy reforms below to see which of these predictions appears to hold.

All of the three models predict large growth effects of policy changes. I will examine below the evidence for or against these claims, but here I will note how much these bold predictions are different from many other fields of economics, as well as from the pre-1986 growth literature. The literature on tax policy, for example, thinks that it is a big deal to identify a benefit of 0.1 percent of GDP from a major tax reform that lowers distortions. The notion that economic development of a whole society can be achieved a few stroke-of-the pen policy reforms seems simplistic in retrospect. If this is so, why haven’t more countries successfully developed? Are large policy effects on growth an inevitable feature of new growth models?