2. Models that predict small policy effects on growth

To begin to understand some of the factors that might mitigate the large effects of policy on growth, suppose that there output is a function of two types of capital, only one of which can be taxed.

For example, suppose that the first type of capital (K1) is formal sector capital that must be transacted on markets in the open, while the second type of capital (K2) is informal sector capital that can be accumulated away from the prying eyes of the tax man.

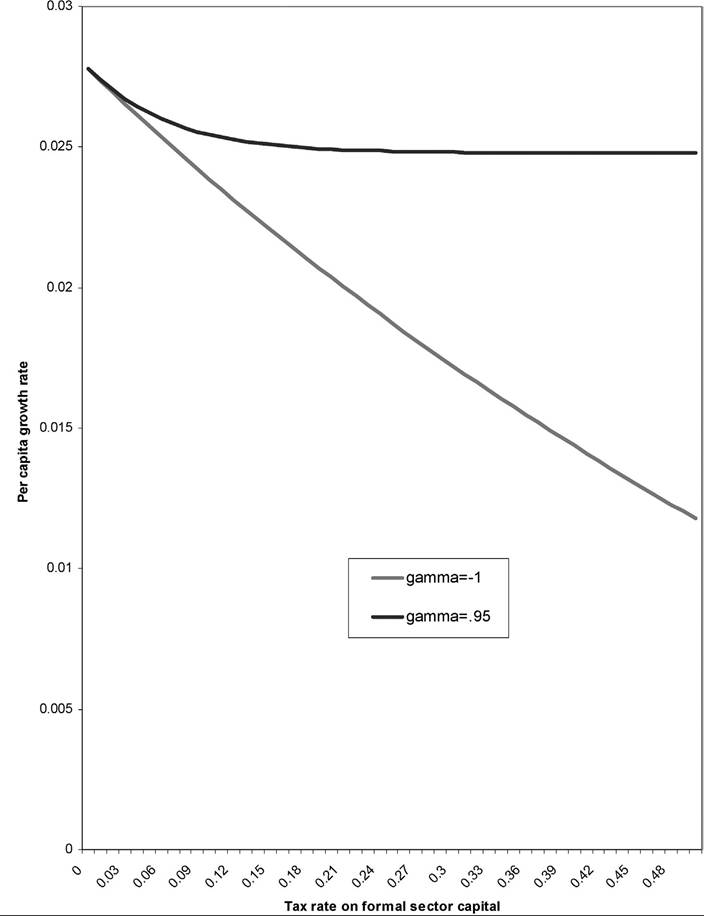

If these two capital goods are close to perfect substitutes, then the effects of taxes on growth go towards zero. Figure 4 shows the relationship between growth and tax rates at extreme values of γ. With γ close to 1 (close to perfect substitutability), there is only a minor effect of taxes and it is bounded from below no matter how high the tax rate. This is because with the elasticity of substitution greater than one, formal sector capital is not essential to production. The worst that high tax rates can do is drive formal capital use down to zero (which has only a small effect if the capital goods are close to perfect substitutes). After that, increases in tax rates have no further effect (explaining the flat segment of the curve in Figure 4). The effects of tax rates on growth continue to be strong if the elasticity of substitution between the two goods is less than one (the γ = -1 line in Figure 4).

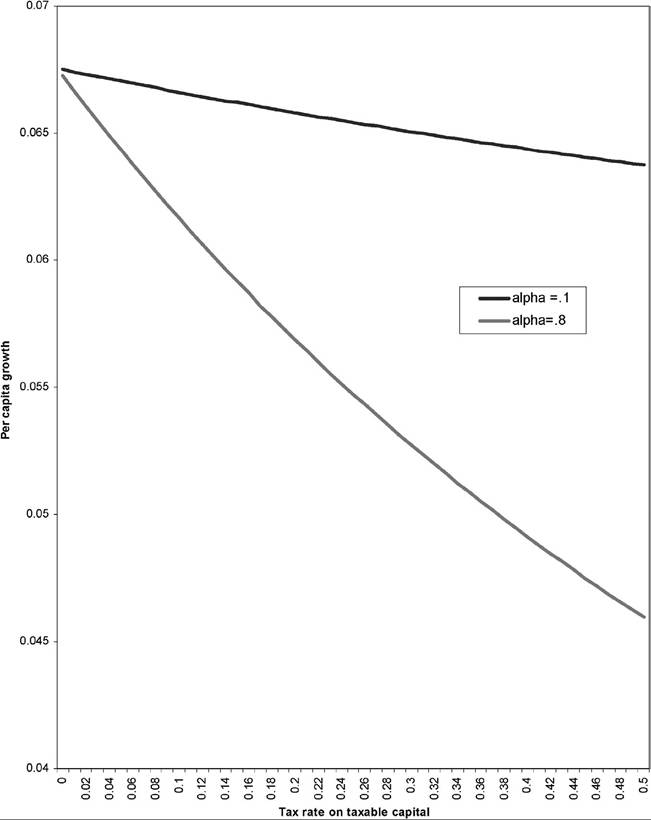

The other parameter that plays an important role in how damaging are tax rates is the share (α) of formal sector capital (or more specifically, the share of the capital that is actually subject to taxation). Figure 5 shows how different are the effects of taxing investment in this factor when its share (α) is 0.1 compared to when its share is 0.8 (assuming an elasticity of substitution of unity).

Of course, lowering the share of taxable capital would also limit the power of taxation in the neoclassical model.Another factor that mitigates the effects of policies on growth is that many policies distort relative prices amongst different sectors or different types of goods, rather than penalizing all capital goods. With a distortion of relative prices, some capital goods are more expensive but others are cheaper. For example, with a black market premium on foreign exchange, those who receive licenses to import goods at the official exchange rate receive a subsidy, while those who must pay the black market rate for inputs pay an implicit tax.[593] Unanticipated high inflation is a tax on creditors but a subsidy to debtors. An overvalued real exchange rate penalizes producers of tradeables but subsidizes producers of nontradeables. Trade protection taxes imports but subsidizes production for the domestic market. The rate of subsidy is clearly related to the rate of taxation. One way to pin it down is to specify that the revenues from the tax on the first type of capital must just cover the subsidy expenditures on the second type of capital.

Here are the equations I have in mind. I revert to Cobb-Douglas for simplicity:

(16) and (17) still represent the capital accumulation equations, and the consumerproducer maximizes (3) taking τ and s as given. Ex-post, the government must balance

Figure 4. Growth rates with different assumptions about elasticity of substitution between capital good types.

Figure 5. Tax rates and growth with different shares of taxable capital.

Because of the neat properties of Cobb-Douglas, the solution of the optimal capital ratio as a function of the subsidy rate (after taking into account the fiscal relation-

ship (21) between tax rates and subsidy rates) is very simple:

The growth rate will display offsetting effects of the subsidy-cum-tax rate - on the one hand, it distorts the allocation of capital away from K1 to K2, lowering the presubsidy marginal product of K2, while on the other hand, it of course subsidizes the rate of return to K2.

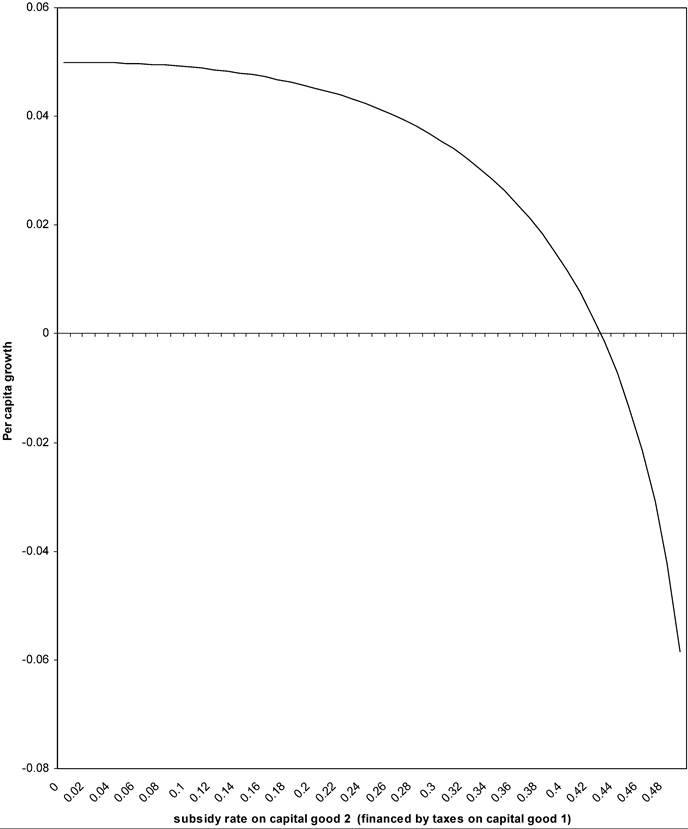

One can show that if (21) (the balanced budget requirement) is imposed, it is impossible for this kind of tax-cum-subsidy scheme to raise the rate of growth.8 The tax-cum-subsidy will imply an efficiency loss from the distortion of resource allocation, and this efficiency loss will have a negative growth effect if all types of capital can be accumulated. However, the relationship between the distortion and the growth rate is highly nonlinear. As is well known in the literature on relative price distortions, the cost of the distortion increases more than proportionately with the size of the distortion.9 In the traditional literature on “Harberger triangles”, this was an output loss. In an endogenous growth model where all inputs can be accumulated, the distortion between relative prices of the inputs induces a reduction in growth. A small distortion introduces only a small wedge in between marginal products of the two inputs and does not cause a huge growth loss. Eventually, however, the distortion forces far too much accumulation of one type of capital relative to the other, severely lowering the marginal product of the excessive capital good due to diminishing returns. An increasing rate of subsidy also requires a more than one for one increase in the tax rate, as the tax base is shrinking with increased taxes while the capital goods being subsidized are increasing. The nonlinear relationship is shown in Figure 6. Note that distortions do not have much effect on growth at all up to subsidy rates of about 0.2 and then have increasingly catastrophic consequences after about 0.4.

There are other factors that mitigate the effects of policy on growth that I do not explicitly model here. One is policy uncertainty. The announcement of a new policy may not be credible, perhaps because high political opposition to it may imply a high probability of subsequent reversal.

Many developing countries have a history of frequent reversals of incipient policy reforms, which makes any future reform less believable. For example, Argentina has been a chronic high inflation country for nearly half a century. Frequent stabilization attempts have subsequently come unwound; the fiasco of the Convertibility Plan in 2001 is only the latest example. In terms of the model above, the

Figure 6. Growth rate and subsidy rate financed by taxes.

certainty equivalent of the after-tax return on capital may not increase much even after an announcement that taxes will be cut.

There is also the possibility that policies whose main purpose was to create rents for political patronage will be replaced with other policies that create new rents. For example, if the black market premium is abolished, the holders of import licenses at the official exchange rate may seek new sources of income (for example, appointment as customs inspectors, where they can take bribes). There may be a law of conservation of political rents, akin to the second law of thermodynamics, if the factors inducing political rent seeking do not change.

Poor countries may be so close to subsistence consumption that they may not be able to take advantage of policy changes. Rebelo (1992) and Easterly (1994) show intertemporal utility functions with Stone-Geary preferences, in which consumers derive utility from consumption only above a certain floor of subsistence. This model predicts a very low intertemporal elasticity of substitution at levels of consumption close to subsistence. Intuitively, consumers close to subsistence have a limited ability to postpone consumption in order to take advantage of higher returns to saving. This model predicts a slow acceleration of growth even after a favorable policy change, as consumption must first rise well above subsistence.

Most importantly, policies may be offset or reinforced by more important factors that affect the growth and income. Achieving high output returns from a given set of inputs involves an incredibly complex set of institutions (such as enforcement of contracts and property rights), social norms, efficient sorting and matching of people and other inputs, advanced technological knowledge, full information on both sides of all transactions, low transaction costs, resolution of principal-agent problems, positive non-zero-sum game theoretic interactions among agents, resolution of public good problems, and so on. The development of institutions and social and political structures that address these issues successfully (from the standpoint of material production) is probably a long historical process.

The above models have a pale shadow of all this complexity in the parameter A. Note that the lower is A, the lower is the derivative of growth (or income in the neoclassical model) with respect to the policy parameter τ. Many authors have argued that differences in A explain a large part of income differences between countries [Hall and Jones (1999), Klenow and Rodriguez-Clare (1997a, 1997b), Easterly and Levine (2001)]. If a poor country is poor because of low A, then a change in policies may not do much to raise income or growth. Exogenous variation in A may also affect the political economy of policy - a high A country would be less likely to tolerate the costs of destructive policies, while bad policy may be tolerated in a low A country because it may not make much difference. Of course policy itself could influence A. However, if A really depends on all the complexities listed above, then the kind of macroeconomic policies I am considering in this paper may not have much effect on A.

2.

More on the topic 2. Models that predict small policy effects on growth:

- Innovation by Incumbents and Entrants and Sources of Productivity Growth

- Innovation by Incumbents and Entrants and Sources of Productivity Growth

- Step-by-Step Innovations*

- Externalities from Capital Accumulation and Economic Growth

- The Diamond Model

- What Macroeconomists Do

- Solow Model and Regression Analyses

- The Real Business Cycle Theory

- References

- NOTES