ANALYSIS AND RESULTS

Based on the results of the Hausman test, we use the random effects model for the panel data to estimate Equation (1). The results are reported in Table 7.

4.1. Effects of Monetary Policy Instruments on Bank Risks

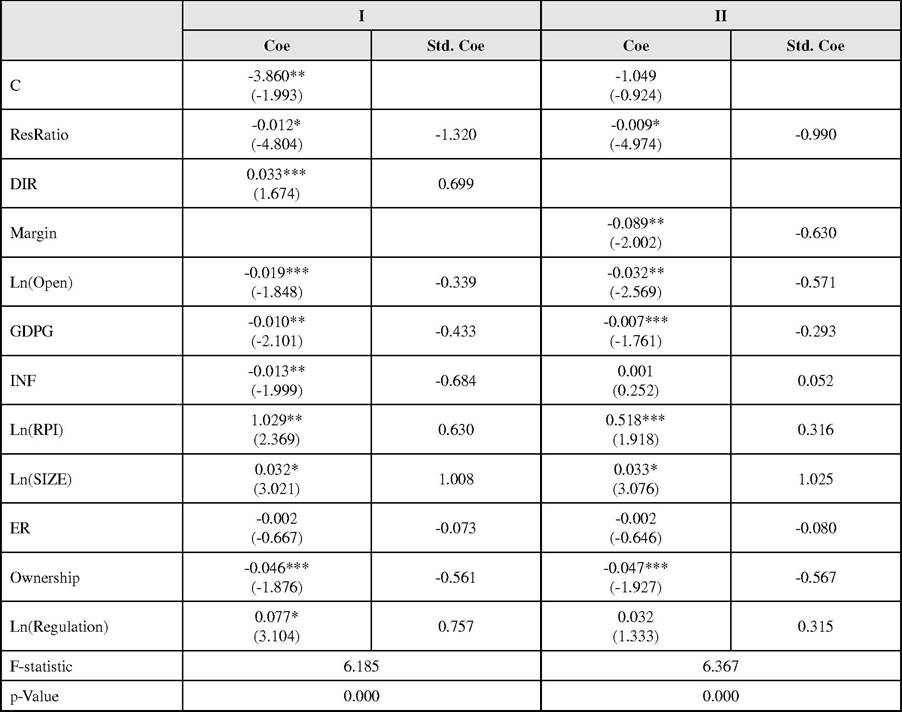

From the results of regression I, the interest rate has the second largest effect on bank risk among the three monetary policy instruments, and it has a significant (at 10% level) and positive effect (0.699) on bank risks, which is in accord with Hypothesis 1.

As for the reserve requirement ratio, its effect on bank risk is the greatest among the three monetary policy instruments, which supports Hypothesis 4. But it has a negative effect (-1.320) on bank risks and is significant at the 1% level, which verifies Hypothesis 2.

The effect of open market operation on bank risk is the weakest among the three monetary policy instruments. Open market operation has a negative effect (-0.339) on bank risks and is significant at the 10% level, which supports Hypothesis 3.

Table 7. The random effects regressions for the panel data

Note: The table reports coefficients and t-statistics (in parentheses). In regressions I and II, the variables that relate to the interest rate are respectively DIR and Margin. The explanatory variables are as follows: ResRatio represents the reserve requirement ratio. DIR denotes the RMB 1-year benchmark deposit rate,.Margin equals the RMB 1-year benchmark loan rate less DIR. Open means open market operation, measured by the turnover of T-Bond trading (including spot trading and repo.trading). GDPG means real GDP growth rate and INF denotes inflation rate, measured by CPI growth rate. RPI demotes real estate price index. SIZE represents size of the bank. ER denotes equity ratio that is defined as the ratio of shareholders’ equity and total assets.Ownership represents the bank ownership.Regulation denotes the banking regulation intensity.

The F-statistic and its associated p-value denote the significance of the regressions. C denotes the constant term. Coe represents coefficient. Std. Coe means the standardized coefficient that can eliminate the impact of the dimension and equals Coe* (standard deviation of the explanatory variable/standard deviation of the dependent variable). *, ** and *** denotes respectively the statistical significance at the 1%,5% and 10% level.Obviously, the effect of the reserve requirement ratio on bank risks is the largest among the three monetary policy instruments.

The effect of the interest rate on bank risk is smaller than that of the reserve requirement ratio on bank risk. The reason may lie in the different features of the effects of the interest rate and the reserve requirement ratio. Changes of the interest rate affect not only the amount of banks’ available fund, but also the cost of banks’ liabilities. Facing the changes of the interest rate, banks must consider not only the allocation of funds, but also the cost of the liabilities, which makes decisionmaking of banks complex. As for the freedom in decision-making, banks are free to some extent, such as the right of making loan rate float, but the risks of bank are more restricted by the residents, companies, the interbank and the central bank. The reason is that the changes of the interest rate may affect the cost of bank’s liabilities to residents and companies and the costs of banks’ financing from the interbank or the central bank. The effects of the interest rate may be slow and complex.

However, the effects of the reserve requirement ratio are very obvious and it has a direct impact on the amount of the available funds of the banks instead of the cost of banks’ liabilities. Facing the changes of the reserve requirement ratio, banks are easier to make decisions and the allocation of funds is banks’ priority. The reserve requirement ratio is an administrative command that banks must comply with it unconditionally. The reserve requirement ratio directly reflects the monetary authority’s intent and its effect is the most direct and rapid.

As a result, the effects of the interest rate and the reserve requirement ratio on bank risk may be different in the sign and intensity.As for the effect of the open market operation, it is partly constrained by weaker purchasing willingness on the part of commercial banks while the reserve requirement ratio gives the central bank greater initiative in managing liquidity and has the capability to freeze an enormous amount of liquidity to normalize money and credit growth. Hence, the effect of the open market operation on bank risks is smaller than that of the reserve requirement ratio.

The results of regression II are derived by substituting the explanatory variable, Margin, for DIR in regression I. The reserve requirement ratio has still a negative effect (-0.990) on bank risks and is significant at the 1% level, which further affirms the larger effect of the reserve requirement ratio on bank risks. The interest rate margin has a significant (at 5% level) and negative effect (-0.630) on bank risks, which verifies Hypothesis 1. The sign and significance of the effect of open market operation on bank risks have not been changed, compared with the result of regression I.

4.2. Effect of the Control Variables on Bank Risks

From the results of regression I, the effects of real GDP growth rate and inflation rate on bank risk are all significance at 5% level. The coefficient of real GDP growth rate is -0.433, indicating that a fast pace of economic development will reduce bank risk, probably due to the fact that the banks’ business operation is good and the revenue is stable under an up economic environment and the banks do not need to take risks to achieve a higher income. The coefficient of the inflation rate is -0.684, showing that the banks have lower risks when facing a higher level of inflation. The possible reason is as follows. In the circumstance of high inflation, banks do not dare to take risks to retain the high-risk assets, thereby reducing the bank risk.

The real estate price index has a positive effect (0.630) on bank risks at 5% significance level. The probable reason is that China’s real estate market is relatively hot in recent years, which attracts banks to loan a lot to the real estate market to aim at a high yield, causing an increase in bank risk.

The banks’ total assets has a positive and significant (at 1% level) effect (1.008) with the probable reason that the banks with a larger size have a stronger motivation to engage in risky activities, leading to the greater risk faced by banks.

The equity ratio is not statistically significant on bank risks. The possible reasons are that in order to satisfy the requirement of the regulatory authority, the ratio of the shareholders’ equity to total assets in Chinese banking industry is relatively reasonable, which has no significant effect on bank risks.

The bank ownership has a significant (at 10% level) and negative effect (-0.561), showing that the risks of state-owned banks are lower than those of other commercial banks to a certain extent with the probable reason that the implicit guarantee of government for state-owned banks is relatively high.

The banking regulation intensity has a positive effect (0.757) on bank risks at 1% significance level. The probable reason is as follows. The regulation of banking restricts the flexibility of adjusting strategy of the banks, which causes the continuity of bank risks (Borio & Zhu, 2008).

The results of regression II show that most control variables are significant and their effects on bank risks have the same sign while the inflation rate and the banking regulation intensity have been insignificant, compared with the results of regression I.

5.