BALANCE sheet ratios

The most immediate danger faced by a lender is the risk that the borrower will suffer illiquidity—an inability to raise cash to pay its obligations.

This condition can arise for many reasons, one of which is a loss of ability to borrow new funds to pay off existing creditors. Whatever the underlying cause, however, illiquidity manifests itself as an excess of current cash payments due, over cash currently available. The current ratio gauges the risk of this occurring by comparing the claims against the company that will become payable during the current operating cycle (current liabilities) with the assets that are already in the form of cash or that will be converted to cash during the current operating cycle (current assets). Referring to Johnson & Johnson’s balance sheet (Exhibit 13.1), the company’s current ratio as of December 31, 2000, was 2.16 (dollar figures are in millions):| Current assets | $15,450 |

| Current ratio....... = Current liabilities | — 2.16 $7,140 |

Analysts also apply a more stringent test of liquidity by calculating the quick ratio, or acid test, which considers only cash and current assets that

EXHIBIT 13.1 Johnson & Johnson

Consolidated Balance Sheets at December 31, 2000 ($000 omitted)

Source: 10-K405 March 30, 2001.

can be most quickly converted to cash (marketable securities and receivables).

Johnson & Johnson’s quick ratio on December 31, 2000, was 1.43:![]()

Besides looking at the ratio between current assets and current liabilities, it is also useful, when assessing a company’s ability to meet its nearterm obligations, to consider the difference between the two, which is termed working capital. Referring once again to Exhibit 13.1, working capital is $8.31 billion.

![]()

Analysis of current assets and current liabilities provides warnings about impending illiquidity, but lenders nevertheless periodically find themselves saddled with loans to borrowers who are unable to continue meeting their obligations and are therefore forced to file for bankruptcy. Recognizing that they may one day find themselves holding defaulted obligations, creditors wish to know how much asset value will be available for liquidation to pay off their claims.1 The various ratios that address this issue can be grouped as measures of financial leverage.

New Roman">A direct measure of asset protection is the ratio of total assets to total liabilities, which in the example shown in Exhibit 13.1 comes to:

![]()

(Total liabilities can be derived quickly by subtracting stockholders’ equity from total assets.)

Put another way, Johnson & Johnson’s assets of $31,321 billion could decline in value by 60% before proceeds of a liquidation would be insufficient to satisfy lenders’ $12,531 billion of claims.

The greater the amount by which asset values could deteriorate, the greater the “equity cushion” (equity is by definition total assets minus total liabilities), and the greater the creditor’s sense of being protected.Lenders also gauge the amount of equity “beneath” them (junior to them in the event of liquidation) by comparing it with the amount of debt outstanding. For finance companies, where the ratio is typically greater than 1.0, it is convenient to express the relationship as a debt-equity ratio:

Conventionally capitalized industrial corporations (as opposed to companies that have undergone leveraged buyouts), generally have debt-equity ratios of less than 1.0. The usual practice is to express their financial leverage in terms of a total-debt-to-total-capital ratio:

Banks' “capital adequacy” is commonly measured by the ratio of equity to total assets:

Many pages of elaboration could follow on the last few ratios mentioned. Their calculation is rather less simple than it might app ear. The reason is that aggressive borrowers frequently try to satisfy the letter of a maximum leverage limit imposed by lenders, without fulfilling the conservative spirit behind it. The following discussion of definitions of leverage ratios addresses the major issues without laying down absolute rules about “correct” calculations.

As explained later in the chapter, ratios are most meaningful when compared across time and across borrower. Consequently, the precise method of calculation is less important than the consistency of calculation throughout the sample being compared.What Constitutes Total Debt?

At one time, it was appropriate to consider only long-term debt in leverage calculations for industrial companies, since short-term debt was generally used for seasonal purposes, such as financing Christmas-related inventory. A company might draw down bank lines or issue commercial paper to meet these funding requirements, then completely pay off the interim borrowings when it sold the inventory. Even today, a firm that “zeros out” its short-term

debt at some point in each operating cycle can legitimately argue that its true leverage is represented by the permanent (long-term) debt on its balance sheet. Many borrowers have long since subverted this principle, however, by relying heavily on short-term debt that they neither repay on an interim basis nor fund (replace with long-term debt) when it grows to sufficient size to make a bond offering cost-effective. Such short-term debt must be viewed as permanent and included in the leverage calculation. (Current maturities of long-term debt should also enter into the calculation of total debt, based on a conservative assumption that the company will replace maturing debt with new long-term borrowings.)

As an aside, the just-described reliance on short-term debt is not necessarily as dangerous a practice as in years past, although it should still raise a caution flag for the credit analyst. Two risks are inherent in depending on debt with maturities of less than one year. The first is potential illiquidity. If substantial debt comes due at a time when lenders are either unable to renew their loans (because credit is tight) or unwilling to renew (because they perceive the borrower as less creditworthy than formerly), the borrower may be unable to meet its near-term obligations.

This risk may be mitigated, however, if the borrower has a revolving credit agreement, which is a longer-term commitment by the lender to lend (subject to certain conditions such as maintaining prescribed financial ratios and refraining from significant changes in the business). The second risk of relying on shortterm borrowings is exposure to interest-rate fluctuations. If a substantial amount of debt is about to come due, and interest rates have risen sharply since the debt was incurred, the borrower’s cost of staying in business may skyrocket overnight.Note that exposure to interest rate fluctuations can also arise from long-term floating-rate debt. Companies can limit this risk by using financial derivatives. One approach is to cap the borrower’s interest rate; that is, set a maximum rate that will prevail, no matter how high the market rate against which it is pegged may rise. Alternatively, the borrower can convert the floating-rate debt to fixed-rate debt through a derivative known as an interest-rate swap. (The forces of supply and demand may make it more economical for the company to issue floating-rate debt and incur the cost of the swap than to take the more direct route to the same net effect, that is, to issue floating-rate debt.) Public financial statements typically provide only general information about the extent to which the issuer has limited its exposure to interest rate fluctuations through derivatives.

Borrowers sometimes argue that the total debt calculation should exclude debt that is convertible, at the lender’s option, into common equity. Hardliners on the credit analysis side respond: “It’s equity when the holders convert it to equity. Until then, it’s debt.” Realistically, though, if the conversion value of the bond rises sufficiently, most holders will in fact convert their securities to common stock. This is particularly true if the issuer has the option of calling the bonds for early retirement, which results in a loss for holders who fail to convert.

Analysts should remember that the ultimate objective is not to calculate ratios but to assess credit risk. Therefore, the best practice is to count convertible debt in total debt, but to consider the possibility of conversion when comparing the borrower’s leverage with that of its peer group.Preferred stock2 is a security that further complicates the leverage calculation. From a legal standpoint, preferred stock is clearly equity; in liquidation, it ranks junior to debt. Preferred stock pays a dividend rather than interest, and failure to pay the dividend does not constitute a default. On the other hand, preferred dividends, unlike common dividends, are contractually fixed in amount. An issuer can omit its preferred dividend, but not without also omitting its common dividend. Furthermore, a preferred dividend is typically cumulative, meaning that the issuer must repay all preferred dividend arrearages before resuming common stock dividends. Furthermore, not all preferred issues have the permanent character of common stock. A preferred stock may have a sinking fund provision, much like the provision typically found in bonds, that requires redemption of a substantial portion of the outstanding par amount prior to final maturity. Such a provision implies less financial flexibility than is the case for a perpetual preferred stock, which requires no principal repayment at any time. Another preferred security, exchangeable preferred stock, can be transformed into debt at the issuer’s option. Treating it purely as equity for credit analysis purposes would understate financial risk. In general, the credit analyst must recognize the heightened level of risk implied by the presence of preferred stock in the capital structure. A formal way to take this risk into account is to calculate the ratio of total fixed obligations to total capital:3

Total debt + Preferred stock + Preference stock

Total debt + Minority interest + Preferred stock + Preference stock + Common equity

Off-balance-sheet lease obligations, like preferred stock, enable companies to obtain many of the benefits of debt financing without violating covenanted limitations on debt incurrence. Accounting standards have partially brought these debtlike obligations out of hiding by requiring capital leases to appear on the balance sheet, either separately or as part of longterm debt. Credit analysts should complete the job. In addition to including capital leases in the total debt calculation, they should also take into account the off-balance-sheet liabilities represented by contractual payments on operating leases, which are reported (as “rental expense”) in the Notes to Financial Statements. The rationale is that although the accounting rules distinguish between capital and operating leases, the two financing vehicles frequently differ little in economic terms. Indeed, borrowers have used considerable ingenuity in structuring capital leases to qualify as operating leases under GAAP, the benefit being that they will consequently be excluded from the balance sheet and, it is hoped, from credit analysts’ scrutiny. Analysts should not fall for this ruse, but should instead capitalize the current year rental payments shown in the Notes to Financial Statements. The most common method is to multiply the payments by seven or eight, a calculation that has been found to be reasonably accurate when actual figures on capitalized value of leases have been available for comparison.

Other Off-Balance-Sheet Liabilities

In their quest for methods of obtaining the benefits of debt without suffering the associated penalties imposed by credit analysts, corporations have by no means limited themselves to the use of leases. Like leases, the other popular devices may provide genuine business benefits, as well as the cosmetic benefit of disguising debt. In all cases, the focus of credit-quality determination must be economic impact, which may or may not be reflected in the accounting treatment.

A corporation can employ leverage yet avoid showing debt on its consolidated balance sheet by entering joint ventures or forming partially owned subsidiaries. At a minimum, the analyst should attribute to the corporation its proportionate liability for the debt of such ventures, thereby “matching” the cash flow benefits derived from the affiliates. (Note that cash flow is generally reduced by unremitted earnings—the portion not received in dividends—of non-fully-consolidated affiliates.) In some cases, the affiliate’s operations are critical to the parent’s operations, as in the case of a jointly owned pulp plant that supplies a paper plant wholly owned by the parent. There is a strong incentive, in such instances, for the parent to keep the jointly owned operation running by picking up the debt service commitments of a partner that becomes financially incapacitated, even though it may have no legal obligation to do so. (In legal parlance, this arrangement is known as a several obligation, in contrast to a joint obligation in which each partner is compelled to back up the other’s commitment.) Depending on the particular circumstances, it may be appropriate to attribute to the parent more than its proportionate share—up to 100%—of the debt of the joint venture or unconsolidated subsidiary.

Surely one of the most ingenious devices for obtaining the benefits of debt without incurring balance sheet recognition was described by The Independent in 1992. According to the British newspaper, the Faisal Islamic Bank of Cairo had provided $250 million of funding to a troubled real estate developer, Olympia & York. As an institution committed to Islamic religious principles, however, the bank was not allowed to charge interest. Instead, claimed The Independent, Faisal Islamic Bank in effect had acquired a building from Olympia & York, along with an option to sell it back. The option was reportedly exercisable at $250 million plus an amount equivalent to the market rate of interest for the option period. Because the excess was not officially classified as interest, said The Independent, the $250 million of funding did not show up as a loan on Olympia & York’s balance sheet.

The Independent noted a denial by an Olympia & York spokesperson that “any such loan existed” (emphasis added). If, however, the account was substantially correct, then the religious-prohibition-of-interest gambit succeeded spectacularly in diverting attention from a transaction that had all the trappings of a loan. Barclays Bank, one of Olympia & York’s most important lenders, commented that it had never heard of the Faisal Islamic Bank transaction.4

Of a somewhat different character within the broad category of off- balance-sheet liabilities are employee benefit obligations. Under SFAS 87, balance sheet recognition is now given to pension liabilities related to employees’ service to date. Similarly, SFAS 106 requires recognition of postretirement health care benefits as an on-balance-sheet liability. Projected future wage increases are still not recognized, however, although they affect the calculation of pension expense for income statement purposes. Unlike some other kinds of hidden liabilities, these items arise exclusively in furtherance of a business objective (attracting and retaining capable employees), rather than as a surreptitious means of leveraging shareholders’ equity.

Generally speaking, pension obligations that have been fully funded (provided for with investment assets set aside for the purpose) present few credit worries for a going concern. Likewise, a modest underfunding that is in the process of being remediated by an essentially sound company is no more than a small qualitative factor on the negative side. On the other hand, a large or growing underfunded liability can be a significantly negative consideration—albeit one that is hard to quantify explicitly— in assessing a deteriorating credit. In bankruptcy, it becomes essential to monitor details of the Pension Benefit Guaranty Corporation’s efforts to assert its claim to the company’s assets, which, if successful, reduce the settlement amounts available to other creditors.

Are Deferred Taxes Part of Capital?

Near the equity account on many companies’ balance sheets appears an account labeled “Deferred Income Taxes.” This item represents the cumulative difference between taxes calculated at the statutory rate and taxes actually paid. The difference reflects the tax consequences, for future years, of the differences between the tax bases of assets and liabilities and their carrying amounts for financial reporting purposes.

Many analysts argue that net worth is understated by the amount of the deferred tax liability, since it will in all likelihood never come due and is therefore not really a liability at all. (As long as the company continues to pay taxes at less than the statutory rate, the deferred tax account will continue to grow.) Proponents of this view adjust for the alleged understatement of net worth by adding deferred taxes to the denominator in the total-debt-to-total-capital calculation, thus:

Total debt

Total debt + Deferred taxes + Minority interest + Total equity

In general, this practice is sound. Analysts must, however, keep in mind that the precise formula for calculating a ratio is less important than the assurance that it is calculated consistently for all companies being evaluated. The caveat is that many factors can contribute to deferred taxes, and not all of them imply a permanent deferral. A defense contractor, for example, can defer payment of taxes related to a specific contract until the contract is completed. The analyst would not want to add to equity the taxes deferred on a contract that is about to be completed, although in such situations specific figures may be hard to obtain.

The Importance of Management's Attitude toward Debt

As the preceding discussion has established, companies use numerous gambits in their quest to enjoy the benefits of aggressive financial leverage without suffering the consequences of low credit ratings and high borrowing costs. Analysts should note that corporations’ bag of tricks is not confined to accounting gimmicks. Some management teams also rely on a bait-and- switch technique.

size=2 color=black face="Times New Roman">The ploy consists of announcing that management has learned the hard way that conservative financial policies serve shareholders best in the long run. Never again, vows the chief executive officer, will the company undergo the financial strain that it recently endured as a result of excessive borrowing a few years earlier. To demonstrate that they truly have gotten religion, the managers institute new policies aimed at improving cash flow and pay down a slug of short-term borrowings. On the strength of the favorable impression that these actions create among credit analysts who rely heavily on trends in financial ratios, the company floats new long-term bonds at an attractive rate. Once the cash is in the coffers, management loses its motivation to present a conservative face to lenders and reverts to the aggressive financial policies that so recently got the company into trouble.

Not everybody is taken in by this ruse. Moody’s and Standard & Poor’s place heavy emphasis on management’s attitude toward debt when assigning bond ratings (see “Relating Ratios to Credit Risk” later in this chapter). They strive to avoid upgrading companies in response to balance sheet improvements that are unlikely to last much beyond the completion of the next public offering. In reward for such vigilance, the agencies are routinely accused of being backward-looking. The corporations complain that the bond raters are dwelling unduly on past, weaker financial ratios. In reality, the agencies are thinking ahead. Based on their experience with management, they are inferring that the recent reduction in financial leverage reflects expediency, rather than a long-term shift in debt policy. As evidence that the rating agencies have good reason to take corporate managers’ assurances with a grain of salt, consider Viacom International’s long-run record on stated objectives and actual financial practices.

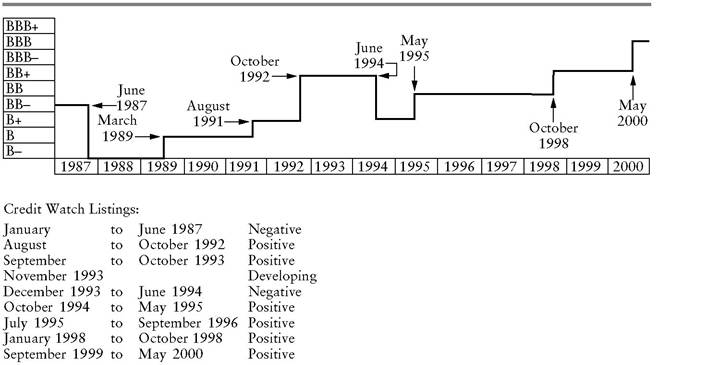

Since 1987, Standard & Poor’s has raised and lowered the diversified media company’s rating several times (see Exhibit 13.2). The graph tracks the company’s subordinated debt rating because for much of the period, the company had no public, rated senior debt outstanding. A leveraged buyout precipitated a downgrading from BB- to B- in early 1987. The rating rebounded to B in 1989 on the strength of strong operating performance and, with the additional help of a stock offering, to B+ in 1991.

Viacom president and chief executive officer Frank J. Biondi enunciated a corporate drive toward further improvements in July 1992, when he commented on the company’s plans to redeem an issue of high-cost debentures:

The expense associated with the debt redemption represents a one-time investment which will have a quick payback in subsequent quarters as Viacom continues to achieve a lower cost of borrowing.5

EXHIBIT 13.2 Rating History: Viacom International.

Sources: Standard & Poor's.

Based on Biondi's statement that the corporation's objective was to continue reducing its cost of borrowing, a logical inference was that Viacom would strive to raise its debt rating. After all, a higher rating would signify lower credit risk and enable the company to borrow at lower interest rates. Viacom did, in fact, achieve an upgrade to BB+ at the subordinated level in October 1992. Less than two years later, however, Viacom acquired another media giant, Paramount. The resulting increase in Viacom's ratio of debt to capital precipitated a June 1994 downgrade back to the previous B+ subordinated rating. Evidently, the company's stated objective of continuing to reduce its borrowing cost did not necessarily mean that management would continue in that direction for very long.

In fairly short order, however, the picture improved once again. Viacom merged with the video store operator Blockbuster, which had a moderately leveraged balance sheet and a lot of cash. The combined company not only had a strong financial position, but also declared that it would liquidate debt by selling both its cable television operations and its partial ownership of Spelling Entertainment Group. On the strength of these developments, Standard & Poor's watchlisted Viacom for possible upgrading in August 1994. The subordinated rating climbed to BB- in May 1995 as the cable television sale was completed and S&P said that a further boost would follow the completion of the planned Spelling transaction.

Once again, though, Viacom’s upward progress was interrupted. President Biondi, who had a reputation as a good financial manager, abruptly resigned in January 1996. The trade press claimed that he was forced out. Chairman Sumner Redstone took over the chief executive officer duties and announced that the company would adopt a more “entrepreneurial, aggressive” management style. To Moody’s, which had watchlisted Viacom for upgrading in July 1995, this suggested a possible sidetracking of the company’s debt-reduction plans.

Redstone sought to allay such concerns, which were likely to cool investors’ enthusiasm for Viacom’s bonds. “Viacom has been and will remain absolutely committed to strengthening its capital structure,” he said, adding that further upgrading would remain a major corporate priority. He repeated that pledge on February 21, 1996, as speculation began to mount that the company would repurchase shares, an action at variance with the goal of reducing the debt-to-equity ratio.

style='text-indent:18.0pt'>Investors did not have an inordinately long wait to learn how Viacom would reconcile management’s stated objective of boosting credit quality with the securities analysts’ claims that management was hinting at a stock buyback. In May 1996, the company abandoned its plan to sell Spelling, the transaction on which further upgrading by Standard & Poor’s hinged, saying that the offers it had received were inadequate. Then, in September 1996, Viacom and Redstone’s investment firm announced plans to repurchase 5.2% of the company’s shares. Even as the price of the company’s bond fell in the secondary market, the company once again insisted that it remained committed to achieving further upgrading. Standard & Poor’s nevertheless removed Viacom from its upgrade watchlist.Credit analysts were rewarded for being skeptical about Viacom’s dogged insistence, from late 1992 through 1996, that reduction of financial leverage was a top priority. Not until October 1998 did the company’s subordinated debt rating recover to the BB+ perch from which it fell in June 1994. The rating continued to rise thereafter, suggesting that at some level, management truly did see it as important to move in the direction of lower debt to capital. Along the way, however, Viacom was willing to take a few steps back, in the form of strategic acquisitions and share-boosting stock repurchases, before moving forward.

In general, credit analysts should assume that the achievement of higher bond ratings is a secondary goal of corporate management. If a company’s stock has been languishing for a while, management will not ordinarily feel any urgency about eliminating debt from the capital structure, an action that reduces return on shareholders’ equity (see Chapter 14). Similarly, the typical chief executive officer, being only human, finds it difficult to resist a

chance to run a substantially bigger company. Therefore, if a mammoth acquisition opportunity comes along, the CEO is likely to pursue it, even if it means borrowing huge amounts of money and precipitating a rating downgrade, rather than the hoped-for upgrade.

Like other types of financial statement analysis, finding meaning in a company’s balance sheet requires the analyst to look ahead. When management’s probable future actions are taken into account, the company’s prospects for repaying its debts on schedule may be better or worse than the ratios imply. The credit analyst cannot afford to take management’s representations at face value, however. When a chief executive officer claims that obtaining a higher bond rating is the corporation’s overriding objective, it is essential to ask for specifics: What are the elements of the company’s action plan for achieving that goal? Which of the steps have been achieved so far?

Above all, the credit analyst must listen closely for an escape clause, typically uttered while the company is engaged in a debt offering. It can be heard when a prospective buyer asks whether management will stay on course for a rating upgrade come hell or high water. The CEO casually replies, “Of course, if a once-in-a-lifetime major acquisition opportunity were to come along, and it required us to borrow, we would have to delay our plans for debt reduction temporarily.” The credit analyst can generally assume that shortly after the bond deal closes, the once-in-a-lifetime opportunity will materialize.