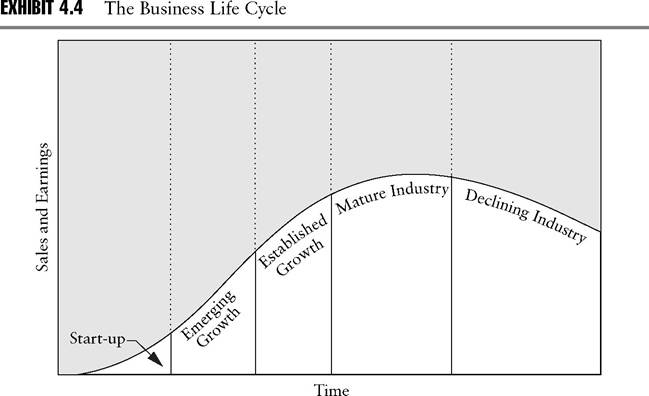

CASH FLOW AND THE COMPANY LIFE CYCLE

Business enterprises typically go through phases of development that are in many respects analogous to a human being’s stages of life. Just as children are susceptible to illnesses different from those that afflict the elderly, the risks of investing in young companies are different from the risks inherent in mature companies.

Accordingly, it is helpful to understand which portion of the life cycle a company is in and which financial pitfalls it is therefore most likely to face.Exhibit 4.4 depicts the business life cycle in terms of sales and earnings growth over time. Revenues build gradually during the start-up phase, during which time the company is just organizing itself and launching its products. Growth and profits accelerate rapidly during the emerging growth phase, as the company’s products begin to penetrate the market and the production reaches a profitable scale. During the established growth period, growth in sales and earnings decelerates as the market nears saturation. In the mature industry phase, sales opportunities are limited to the replacement of products previously sold, plus new sales derived from growth in the population. Price competition often intensifies at this stage, as companies seek sales growth through increased market share (a larger piece of a pie that is growing at a slower rate). The declining industry stage does not automatically follow maturity, but over long periods some industries do get swept away by technological change. Sharply declining sales and earnings, ultimately resulting in corporate bankruptcies, characterize industries in decline.

The characteristic growth patterns of firms at various stages in the company life cycle correspond to typical patterns of cash generation and usage.

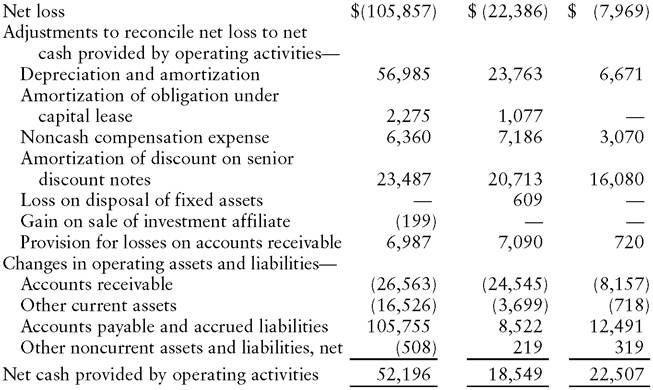

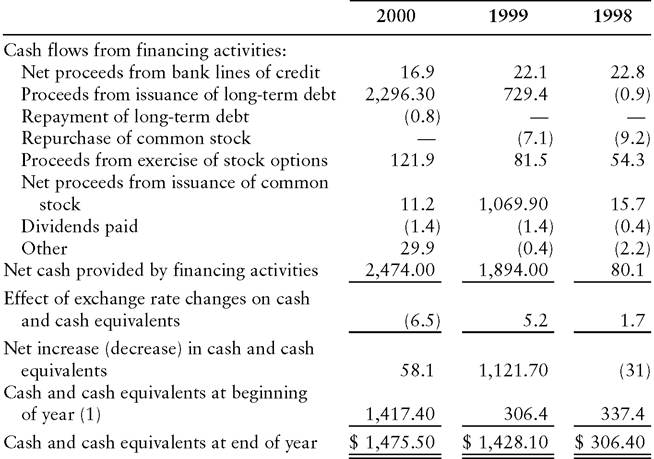

For example, outright start-up companies are typically voracious cash users. They require funds to pay the salaries of the employees who plan the initial attempts to gear up production and launch marketing efforts. With no revenues yet coming in, the risk is high that the organization will fail to gel. Such companies offer little basis for conventional financial statement analysis. Before offering their securities in the public market and subjecting their financial results to scrutiny by general investors, they operate as privately owned companies under the auspices of venture capitalists. “VCs” are professional investors with special expertise in evaluating infant companies. They assess the new ventures’ prospects for generating sufficient revenues to go public.3Emerging growth companies are start-ups that survive long enough to reach the stage of entering the public market. Focal Communications (Exhibit 4.5) illustrates the cash flow pattern of an emerging growth company. As a competitive local exchange carrier (CLEC), Focal offers long-distance voice and data telecommunications services to large business customers. Its market is characterized by rapid growth, but Focal is not yet at the point of being able to harvest profits on its large capital investments.

Consolidated Statements of Cash Flows for the Three Years Ended December 31, 2000 (Dollars in thousands, except share amounts)

2000 1999 1998

CASH FLOWS FROM OPERATING ACTIVITIES:

CASH FLOWS FROM INVESTING ACTIVITIES:

Source: Focal Communications Corporation Form 10K March 30, 2001.

Over the past three years shown in the exhibit, Focal has recorded mounting losses on operations.

Noncash expenses, principally depreciation and amortization of fixed assets and amortization of debt discount,4 represent much of the reported losses. With increases in accounts payable and accrued liabilities as additional sources, operations have been cash-flowpositive. Focal’s capital budget is several times as great as its depreciation charges, which conceptually represent the requirement to replace existing plant and equipment as a consequence of wear and tear. This large ongoing construction has required outside financing, consisting of both long-term debt and stock issuance.Heavy reliance on external financing creates substantial vulnerability in periods of limited access to capital. Late in 2000, emerging growth telecommunications companies lost the ability to raise funds in the public equity and high yield bond markets. By the summer of 2001, Focal indicated that it would run out of cash by the first quarter of 2002 unless it could raise new funds, either in the private market or as a result of the public markets reopening to telecom issuers. The company’s stock price and bond ratings declined in reaction to the funding squeeze.

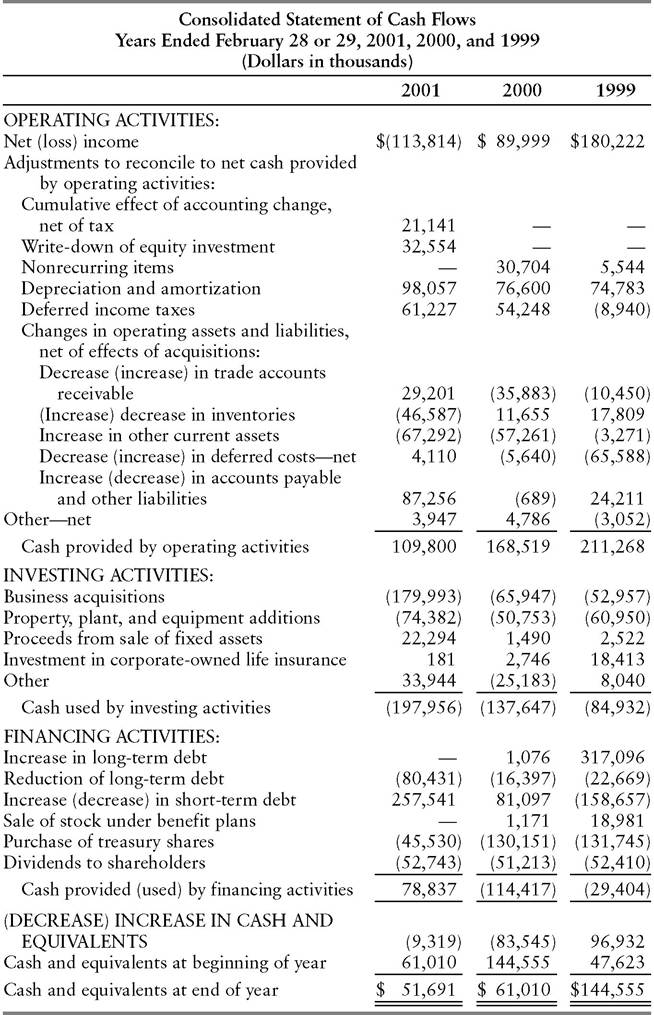

Established growth companies are in a less precarious state in terms of cash flow than their emerging growth counterparts. Solectron (Exhibit 4.6), a provider of electronics manufacturing and supply-chain management services, has reached the stage of profitability. Still in its high-growth phase, the company has chalked up increases of approximately 40% in each of the past two years. Capital expenditures exceed depreciation, although not by as large a margin as observed in emerging growth companies. In 2000, Solectron substantially increased its inventories and acquired $1.1 billion of manufacturing locations and assets. The company funded this expansion primarily with debt issuance.

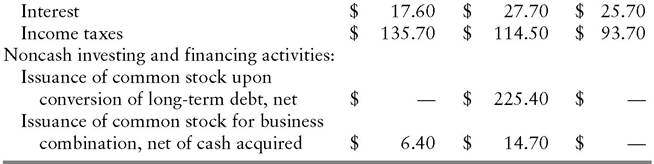

Mature industry companies such as American Greetings, the second- largest greeting card manufacturer in the United States (Exhibit 4.7), are past the cash strain faced by growth companies that must fund large construction programs.

Cash flow from depreciation and amortization more than covers American Greetings’s capital budget. Consequently, the company has consistently generated positive cash flow from operations, although working capital accounts represented a net use of cash in two of the past three years. Even in fiscal 2001, when the company suffered a net loss, operations generated $110 million of cash. The external funding requirement arose from $180 million of acquisitions, which included the purchase of Gibson Greetings, the third-largest company in its business. Consolidation is a typical feature of mature industries, where companies seek to bolster their diminishing profit margins by capturing economies of scale.EXHIBIT 4.6 Solectron Corporation Supplemental Consolidated Statements of Cash Flows (in millions)

Years Ended August 31

(continued)

EXHIBIT 4.6 (Continued)

Years Ended August 31

Cash paid:

Source: Solectron Corporation Form 10-K November 13, 2000.

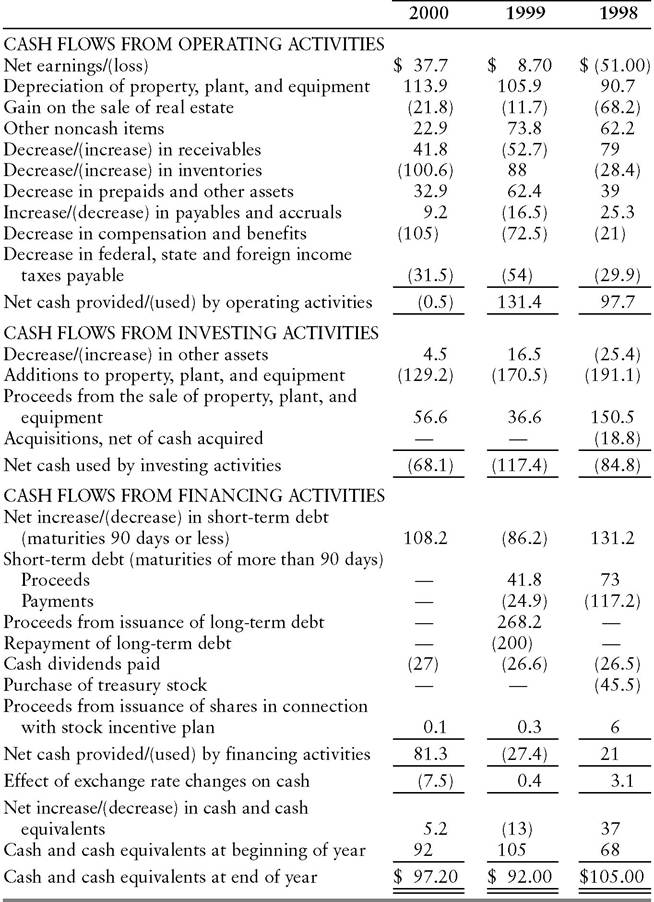

Declining industry companies struggle to generate sufficient cash as a consequence of meager earnings. Polaroid (Exhibit 4.8) earned no cumulative profit over the period 1998-2000.

For the three years, net cash provided by operating activities of $228.6 million fell considerably short of additions to property, plant, and equipment of $490.8 million. The camera manufacturer nearly made up the difference with $243.7 million of proceeds from sales of property, plant, and equipment. In 2000, however, the cash squeeze became more acute as a result of a rising need to finance inventories.

Source: American Greetings Corporation Form 10-K405 May 3, 2001.

Consolidated Statement of Cash Flows (Dollars in millions)

Year Ended December 31

Source: Polaroid Corporation Form 10-K April 2, 2001.

Polaroid’s underlying problem was deterioration in its core business. The company introduced instant photography with the Land Camera in 1947, following up that success with an instant color photography system in 1971. Consumer interest waned, however, with the advent of one-hour photo developing stores and digital cameras. New products failed to revive Polaroid’s fortunes, while costs became bloated through sales force expansion far in excess of sales growth.5 The company compounded its problems in 1988 by aggressively repurchasing stock in an effort to fend off an attempted hostile takeover, sharply increasing its financial leverage as a consequence. Polaroid had an opportunity to reduce its debt load in 1991, when it received $925 million from a settlement of a patent violation suit against Eastman Kodak. Instead, the company used the proceeds to retire more shares and purchase resource-planning software in an attempt to boost efficiency.6

By the summer of 2001, Polaroid was failing to meet its scheduled bond coupons. As a cost-saving measure, the company slashed health care benefits for employees and required retirees to shoulder an increased portion of their health care costs. After attempts to sell all or part of the company bore no fruit, Polaroid filed for bankruptcy on October 12, 2001.