THE CONCEPT OF FINANCIAL FLEXIBILITY

Besides reflecting a company’s stage of development, and therefore the categories of risk it is most likely to face, the cash flow statement provides essential information about a firm’s financial flexibility.

By studying the statement, an analyst can make informed judgments on such questions as:■ How safe (likely to continue being paid) is the company’s dividend?

■ Could the company fund its needs internally if external sources of capital suddenly become scarce or prohibitively expensive?

■ Would the company be able to continue meeting its obligations if its business turned down sharply?

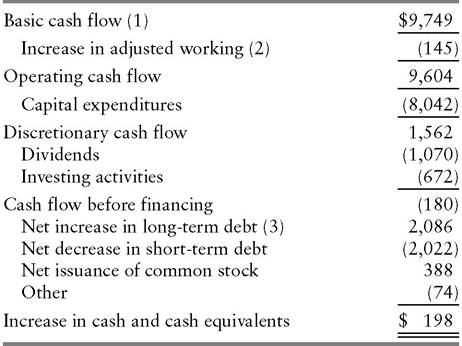

Exhibit 4.9 provides a condensed format that can help answer these questions. At the top is basic cash flow, defined as net income (excluding noncash components), depreciation, and deferred income taxes. The various uses of cash are deducted in order, from least to most discretionary.

In difficult times, when a company must cut back on various expenditures to conserve cash, management faces many difficult choices. A key objective is to avoid damage to the company’s long-term health. Financial

EXHIBIT 4.9 Wal-Mart Stores Inc.

Analysis of Financial Flexibility Fiscal Years Ended January 31, 2001 (000 omitted)

(1) Includes net income, depreciation and amortization, deferred income taxes, and other.

(2) Excludes cash and notes payable.

(3) Includes capital lease obligations.

Source: Wal-Mart Stores Inc.

Form 10-K/A April 17, 2001.flexibility, as captured by the presentation in Exhibit 4.9, is critical to meeting this objective.

Wal-Mart, the United States’ largest retailer, exhibited exceptional financial flexibility in the fiscal year ended January 31, 2001. Cash generated by operations, at a robust $9.6 billion, precluded any need to borrow or issue stock to pay for the company’s ambitious $8.0 billion capital spending program. Wal-Mart floated $2.1 billion of long-term debt (net of retirements), but that issuance merely refunded a similar amount of outstanding short-term debt. Proceeds of the company’s $388 million of net stock issuance essentially made up the small amount ($180 million) by which investing activities (primarily investment in international operations) exceeded internally generated cash after dividends.

Wal-Mart’s ability to self-finance most of its expansion is a great advantage. At times, new financing becomes painfully expensive, as a function of high interest rates or depressed stock prices. During the “credit crunches” that occasionally befall the business world, external financing is unavailable at any price.

Underlying Wal-Mart’s lack of dependence on external funds is a highly profitable discount store business. If this engine were to slow down for a time, as a result of an economic contraction or increased competitive pressures, the company would have two choices. It could reduce its rate of store additions and profit-enhancing investments in technology or it could become more dependent on external financing. The former approach could further impair profitability, while the latter option would earmark a greater portion of Wal-Mart’s EBITDA for interest and dividends. Loss of financial flexibility, in short, leads to further loss of financial flexibility.

If the corporation’s financial strain becomes acute, the board of directors may take the comparatively extreme step of cutting or eliminating the dividend.

(About the only measures more extreme than elimination of the dividend are severe retrenchment, entailing a sell-off of core assets to generate cash, and cessation of interest payments, or default.) Reducing the dividend is a step that corporations try very hard to avoid, for fear of losing favor with investors and consequently suffering an increase in cost of capital. Boards sometimes go so far as to borrow to maintain a dividend at its existing rate. This tactic cannot continue over an extended period, lest interest costs rise while internal cash generation stagnates, ultimately leading to insolvency.Notwithstanding the lengths to which corporations sometimes go to preserve them, dividends must be viewed as a potential source of financial flexibility in a period of depressed earnings. After all, the term “discretionary,” applied to the cash flow that remains available after operating expenses and capital expenditures, emphasizes that dividends are not contractual payments, but disbursed at the board’s discretion. When preservation of the dividend jeopardizes a company’s financial wellbeing, shareholders may actually urge the board to cut the payout as a means of enhancing the stock value over the longer term.

class=a7 style='text-indent:18.0pt'>To gauge the safety of the dividend, analysts can observe the margin by which discretionary cash flow covers it. In Wal-Mart’s case, the ratio is a comfortable $1.562 billion ÷ $1.070 billion = 1.46x. By the same token, that ratio would fall below 1.0x if Wal-Mart’s net income (a component of basic cash flow) declined by $1.562 billion - $1.070 billion = $492 million. That would represent a drop of only 8% in Wal-Mart’s earnings. (Net income, which is not shown in Exhibit 4.9, was $6.295 million in the fiscal year.)Wal-Mart, however, has an additional cushion in the form of potential cutbacks in its capital budget.

Management could not only reduce the pace of store additions, but also defer planned refurbishment of existing stores. The latter measure, though, could cut into future competitiveness. Retailers find that their sales drop off if their stores start to look tired. Similarly, industrial companies can lose their competitive edge if they drop back to “maintenance level capital spending” for any extended period. This is the amount required just to keep existing plant and equipment in good working order, with no expenditures for adding to capacity or upgrading of facilities to enhance productivity. Analysts, by the way, should seek independent confirmation of the figure that management cites as the maintenance level, possibly from an engineer familiar with the business. Companies may exaggerate the extent to which they can cut capital spending to conserve cash in the event of a downturn.A final factor in assessing financial flexibility is the change in adjusted working capital. Unlike conventional working capital (current assets minus current liabilities), this figure excludes notes payable, as well as cash and short-term investments. In Exhibit 4.9, the former is part of the net change in short-term debt, while the period’s increase or decrease in cash is treated as a residual in the analysis of financial flexibility.

For Wal-Mart, adjusted working capital represented a minor ($145 million) use of funds during the fiscal year. In general, inventories and receivables expand as sales grow over time. A company with a strong balance sheet can fund much of that cash need by increasing its trade payables (credit extended by vendors). External financing may be needed, however, if accumulation of unsold goods causes inventories to rise disproportionately to sales. Similarly, if customers begin paying more slowly than formerly, receivables can widen the gap between working capital requirements and trade credit availability. The resulting deterioration in credit quality measures (see Chapter 13), in turn, may cause vendors to reduce the amount of credit they are willing to provide. Once again, loss of financial flexibility can feed on itself.