Chapter 75 Banking Online: Design for a New Credibility

Francisco V. Cipolla-Ficarra

ALAIPO - AINCI, Spain and Italy

Jaqueline Alma

Electronic Arts - Vancouver, Canada

ABSTRACT

The authors present the first results of a communicability evaluation of a set of online banking systems aimed at the new credibility of those institutions.

They evaluate the strategies of interactive design, focusing on the presentation of the information on the interface. Finally, the first group of human factors is established which has affected negatively the veracity of banking information in Southern Europe in the last five years.INTRODUCTION

One of the key elements of the institutional image of the banking bodies has been trust factor towards intangible services related to money and finances (Karat, Brodie & Karat, 2006). Now this flux of information must be available electronically to its clients, 24/7 in every day of the week. Allegedly it is a premise that is guaranteed from the banking publicity to the clientele, but in reality it is not so. The financial institutions have information processes in real time and others in batch processing - in execution of a series of programmes (also called “jobs”) on a computer without manual intervention. This is a widespread reality in this kind of institutions, since the mid 20th century.

DOI: 10.4018∕978-1-4666-6268-1.ch075

The public in general doesn’t know this reality, which is a source of constant complaints (previous to the global financial crisis), whether it is with the remote services or in the banking seats themselves. Consequently, there are processes which are carried out immediately such as the data consultation of the banking headquarters, such as the IBAN code (International Bank Account Number), SWIFT (Society for Worldwide Interbank Financial Telecommunication), etc., and others which require a whole series of previous verifications such as the transfer of currency inside and outside a state.

From the point of view of communicability we can establish two kinds of factors, underlying and apparent. The underlying ones are the characteristics intrinsic to the information system, such as the information in real time or in batch, whereas the apparent are those which obey to the design factors of the computer programmes (Cipolla-Ficarra, 2005). For instance, it is not normal that an experienced or inexperienced user must resort to the Google or Yahoo searcher to find quickly the IBAN or SWIFT code of the banking institution he/she is member..

The issues related to the way of operating from the computer science point of view have j oined a myriad human factors of the banking staff towards their clients. The latter have practically lost their trust towards these institutions, without distinguishing whether the problems stem from the computer systems or the human factors (Cipolla- Ficarra, et al., 2011). When we talk about human factors we mean those excellent clients who have never had red numbers in their accounts and who operated in the banking offices or electronically. These clients interrelated with these institutions without any kind of inconveniences, but who have been swindled by the disingenuous publicity of the banking institutions, that is, the lack of clarity in the marketing information. In our group of adult and inexperienced users in computer science, that knowledge of the banking staff has been termed as sadism in 97% of the analyzed cases.

The current work is structured in the following way: state of the art and strategies followed for the selection of the universe of study and the users, elaboration of the instruments for the measurement of communicability, veracity and credibility of the banking information, interaction with the banking systems, compiling of the results, learned lessons, future lines of work and conclusions. The examples that are commented in the current work over the banking experiences refer to the period 2008-2012 are truthful 100% belong to cities of Southern Europe, and have been extracted from our universe of study.

These have been included to contextualize the data and the presented conclusions.THE UNIVERSE OF STUDY: BANKS AND CLIENTS

Our universe of study is made up by adult people, whose ages oscillate between 40-60 years, clients of banking institutions in Southern Europe. All of them have 15 years of seniority of having bank accounts in the same institution. Some of them have access to the online banking systems, but their knowledge of computer science is elementary. They use the computer for the search of information in Google, Yahoo, etc. and the reception/emission of messages mainly. The analyzed banking institutions have their local headquarters in Catalonia and Lombardy mainly although some of the examples that we will address belong to international financial groups. With these institutions our group of users interact virtually from the workplace and/ or the home and in the daily life. The emotional aspects deriving from scarcely transparent business practices have been quantified through the use of techniques stemming from the social sciences and statistics (Cipolla-Ficarra, et al., 2011). Some examples of these emotional variables are the result of financial prosperity and the deceitful publicity to get the excellent clients into debt are: the former Caixa in Barcelona, now CaixaBank, in the face of the closure of a small firm due to the global financial crisis does not allow the quick transformation of the debt into a personal debt. In contrast, they have chosen to demand the whole payment of the debt, increasing in 50% the overall amount of the debt, to end after several months of disputes in a personal credit to be paid back in several years. Another example is a Lombardian institution that dedicates itself to issuing double personal loans, which are managed externally from the bank, with pensioners who cash ˆ 600 per month and whose monthly fees surpass 50% of their revenue due to the double charge of interests in the amount of the loan. In the face of these two small examples, the credibility towards those banks and the rest of the financial system is equal to zero for those customers.

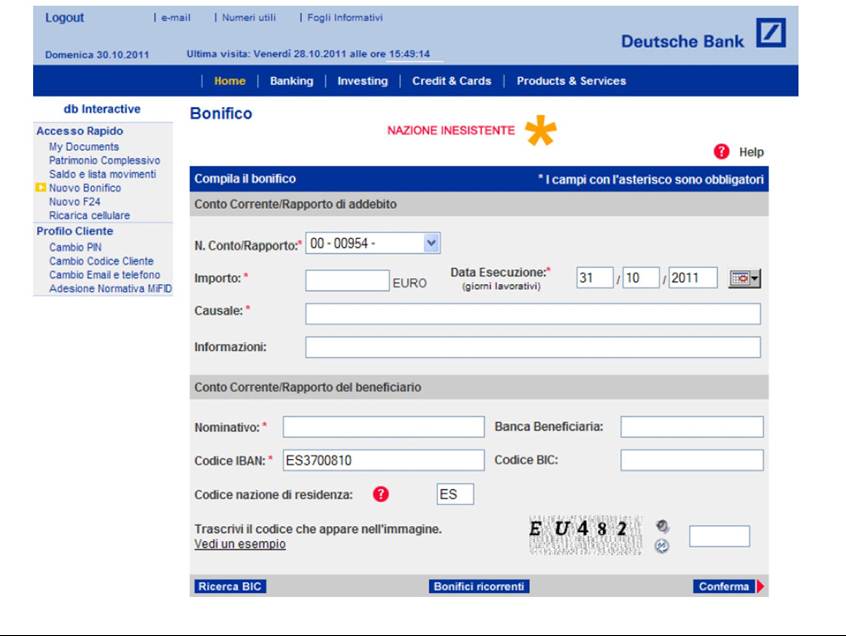

If we add to this the technological issues of not-functioning, such as the typical phrases in Latin America before making a payment with cards in a shop, hotel or even inside the banks themselves, “there is no system,” we can find even worse situations in Europe, as it can be seen in the following example of the Figure 1, where the operations with the Iberian Peninsula are thwarted and the message of “non-existent” nation appears, as is the case of Spain inside the German banking circuit. Obviously, the “there is no system,” is a lesser evil as compared to the “non-existent nation.”The example of “non-existent nation” with which not only it is not possible to make Internet banking operations from the south of the Mediterranean, makes apparent once again the real prejudices towards the clients, who must make the operations on the bank counter, pay fees and see how the batch process slows down the financial operations. Oddly enough, the call center does not inform over the exact date in which the service will be reactivated, nor are there dysfunction messages in the website. That is, that the credibility and the communicability of the online banking information is equal to zero. Of course the banking institutions between

2008- 2012 in Southern Europe have carried out a series of make-up operations in their real or virtual structures, such as placing statues of the “angel” at the entrance (Figure 2), similar to victory or freedom by many sculptors, organizing paintings exhibits, theoretically aiding the disabled, fostering museums of the sciences, etc. of course the opinion gathered in our universe of study indicates that some ofthese institutions are parochial, antiglobalization, uncouth, among other variables related to the human and/or social factors (Cipolla-Ficarra, et al., 2011).

Figure 1. Message of non-existent nation “Spain” (*) from an online service in Italy

Figure 2.

Digital newspaper: L’eco di Bergamo,03.25.2012 (www.ecodibergamo.it)

These real values will be downplayed to the utmost through the publicity rhetoric of the banking and/or financial institutions. These are persuasive publicity campaigns, which have taken avail of almost every media of both digital and analogical communication in order to foster consumerism. Where they practically forced their clients to run into debt with personal credits, mortgages for cars, houses, etc. All of this happened in the period 2000-2007 in countries like Spain and Portugal. Since the 90 down to the early 21st century has had one of the widest ATMs networks on the European continent, with which the phenomenon of wild consumerism in an exponential way.

ANALOGICAL AND DIGITAL INSTITUTIONAL COMMUNICABILITY

The analogical institutional communicability of the financial institutions right now only admits a single way of evaluation; the quality of the paper they use in their brochures, postcards, catalogues of artistic samples, calendars, notebooks, etc. Products produced in Asian countries but designed in Europe make apparent that the bridge between average and small clients with the great, middle-size and small credit institutions has been destroyed. From a linguistic point of view, these institutions try to get back or keep their customers with notions such as “partner,” “members of the same group,” “safety,” “future,” etc., that is, as elements which belong to a same set who must work for the sake of the future. However, these are obsolete communicational forms in view of the human factors, backed by the computer systems, for instance, the reduction of the limits in the credit cards or the increase of the control mechanisms to carry out long distance operations through the use of the internet.

Examining the home pages of the banking and financial systems through a set of quality attributes and metrics developed in the mid 90s and perfected in the current millennium, such as isomorphism, richness and accesibility (Cipolla-Ficarra, 1997), which the interested reader can look up in the following bibliographical references (Cipolla-Ficarra, 1998; Cipolla-Ficarra, 2012).

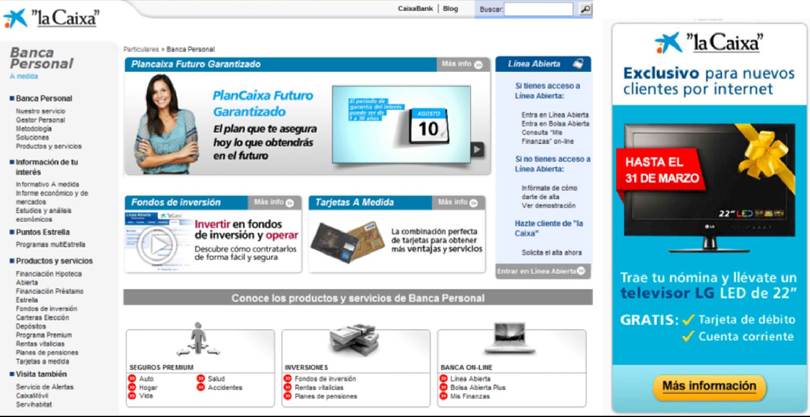

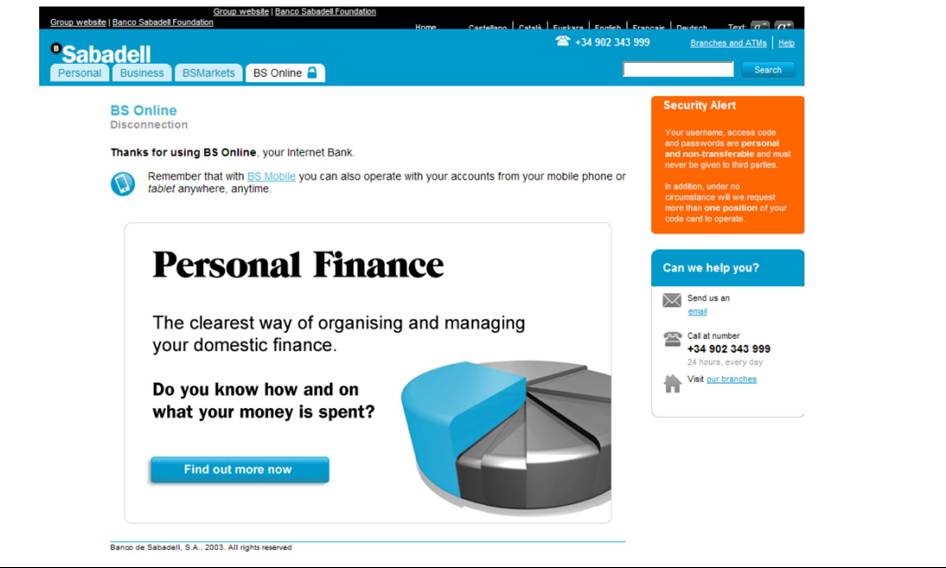

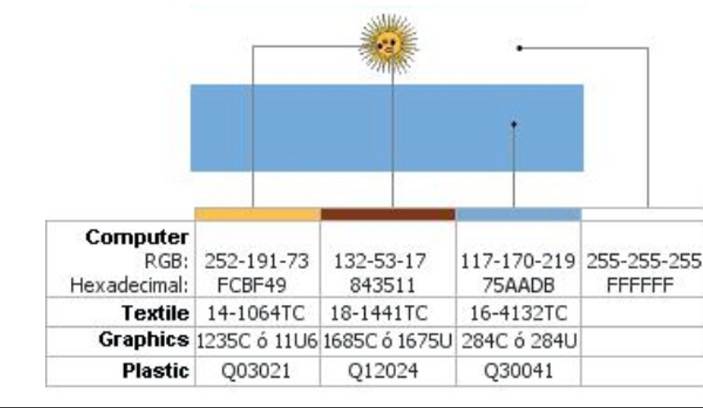

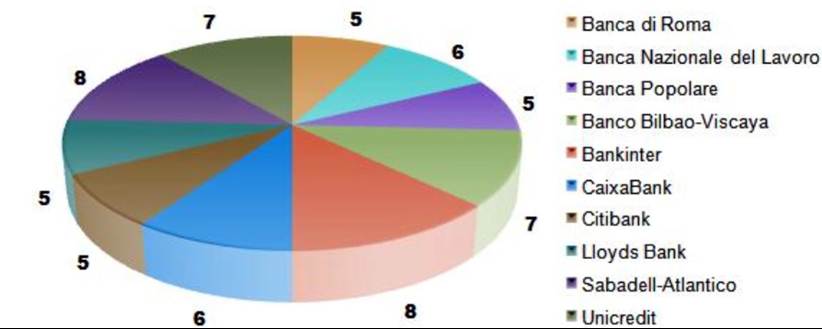

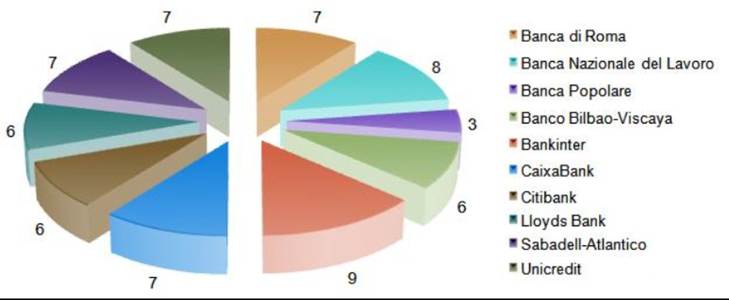

In our first work we will focus on two of the categories of interactive design such as are the presentation of the information and the content, applying the following table which was the basis of the set of quality attributes and metrics (Cipolla-Ficarra, 1998; Cipolla-Ficarra & Cipolla-Ficarra, 2008). The analyzed websites belong to the following banking institutions: B anca di Roma (Italy), Banca Nazionale del Lavoro (Italy), Banca Popolare (Italy), Banco Bilbao-Viscaya (Spain), Bankinter (Spain), CaixaBank (Spain), Citibank (Spain), Lloyds Bank (Italy), Sabadell- Atlantico (Spain), and Unicredit (Italy). All ofthem with headquarters in Spain and Italy. Evidently the visual factor of the websites (Alison et al., 1995; Gage, 2000; Brown, et al., 2002) of the Figures 3 and 4 makes apparent the existence of isotopy lines through the following colors: primary (red, blue, yellow), secondary (light blue, orange) and neuter (black and white). However, inside them can be seen the strengthening of the phenomenon called Argentinization of the colors and which are presented in the following flag with their matching values.Figure 3. The Argentinization of the design: Logo and banner in digital newspaper (www.elpais.es, www. elmundo.es, and www.lavanguardia.es, for example)

Figure 4. Argentinization of the design (www.bancsabadell.com)

Figure 5. Flag of Argentina: Colours and the different codes used in regard to the support that is used. The colors of this flag in a direct or indirect way are present in the banking websites.

Although in a portal we have a drawing made by Joan Miro such as the star of the current CaixaBank (Figure 3), the three colors are not so present in the intranet environments for the customers. In that environment it can be seen how the red is used few times, compared with the light blue, white and yellow. The former colours, light blue with white background of the websites, are currently fashionable even in the Spanish digital press such as can be the portals of El Pais (www.

elpais.es) El mundo (www.elmundo.es), La Van- guardia (www.lavanguardia.es) that is, they have also chosen the Argentinization of their portals. In some way the portals of the banking institutions also try to establish chromatic links with the daily information of the digital press. Next the results of the communicability from the point of view of presentation and the contents of the online information (minimum value 0, maximum value 10).

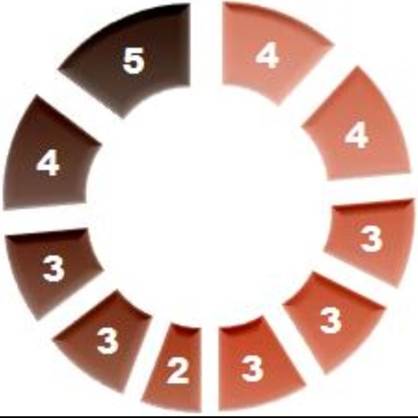

Figure 6. Results of the main components of the free access online interfaces

SAFETY AND DESIGN

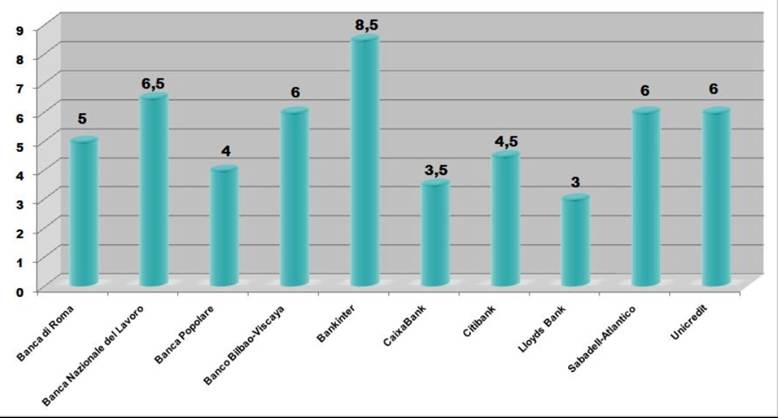

Without any doubt, this is an environment where the safety issue occupies a first place. Aside from all the mechanisms of computer safety applied to the current financial services and that they can be improved to avoid fraud, we focus on the ease of access the users have in our universe of study, without resorting to avant-garde technologies such as can be voice recognition, the iris of the eye, fingerprints, etc. As a rule, for the customers there are two or three keys before having access to their confidential information, such as can be the bank balances and/on movements of their bank accounts or credit cards. Now whereas in Spain with only four digits one can have access to the bank account through an ATM, in Italy it is necessary to type five digits to access the bank account. Here we have a first lack of uniformity of criteria of the banking systems inside a same European region, which have a common currency. This lack of uniformity does not respond to technical issues, but are rather political. Now these criteria create certain habits among the potential users who when they reach certain ages and/or certain educational levels do not grasp easily the logic of these differences. Nor is it easy to them the fact of having to introduce the components of a password in the shape of bidirectional coordinates (x e y), for instance, the firsr component of the key and below the second component. Next the result of the analysis made on the communicability for the ease of access to the online banking information of credit c ards of the group that made up our universe of study (minimum value 0, maximum value 10).

Of course here the dichotomous discussion between online safety and interactive design opens. However, the ideal thing is that this dichotomy could merge in a single reality where safety, communicability, usability and accessibility were present.

From a topological point of view in the access websites to the confidential information we can claim that 100% of the cases are to be found in the upper/central area of the interface. Evidently it is a cultural issue of the Western world, and it obeys to the principles of the “divine or perfect proportion,” in which the spectator focuses her vision on a rectangular or square figure and which Leonardo Da Vinci already used in his paintings.

The chronological factor also affects these two components that we are analyzing (safety and design), especially at the moment of finding out the movements of the bank accounts in the matching detail of the made operations. Whereas in some online systems it is possible to have access to the historical information in others it isn’t, since there is a calendar which sets a limit towards the past, for instance, 30, 60, 90, 180, etc. days. Besides, the detail of the operation may be presented in the shape of an enclosed file of the pdf kind or a.txt file with synthetized information.

Figure 7. The financial institution best valued by the users is Bankinter. The worst valued is Banca Populare.

Once again we are in the face of a reality where from the technological point of view it is feasible to offer the maximum possible information to the online user, that is, the remote customer. However, said alternative is not active in all the banks. This operation is not provided in some financial institutions because it is a way to generate additional revenue, for instance, by cashing a commission for asking all the movements of the account in a year.

Although these institutions do not take into account the waste of time that it means for the customer, who is forced to visit the banking office, since they are personal requests and are made in the counter of the bank. Here is another real situation which accumulates to the human factors as source of possible conflicts, especially for the users experienced in the use of computer systems but who are forced to go to the banks.

In the evaluation with users (20 in all) we have established a series of tasks to be carried out by them once they have reached the reserved or confidential areas. Some of these operations were doable and others not. In an affirmative case, the number of options that were chosen to reach the goal were counted (keyboard and mouse pulses). The same happened with those actions impossible to do in some websites. The tasks and their matching codifications are the following:

T1 = Knowing the balance; T2 = The last 20 movements;

T3 = Having access to the detail to each one of those movements;

T4 = Having access to a banking movement from 180 days back;

T5 = Having access to the information linked to a movement of 6 months back;

T6 = having access to the IBAN of the account.

The names of the banking institutions have been eliminated in the following graphic of results (confidential reasons).

The degree of difficulty to access wanted information is very high in the area of study that is made, if we compare the average of the results obtained by the evaluator who has carried out the set of tasks that the users had to perform.

T 1= 3 options (here is calculated the total, that is, those made both from the keyboard and the mouse which are equivalent to an input or an enter or a click).

T 2= 2 steps.

T 5= In the cases when it is feasible to reach the average is 5, in other financial websites this task is impossible to make.

T 7= it is not possible to carry out that operation.

Figure 8. Total of operations carried out from the keyboard or with the mouse to have access to confidential information in the online service of some financial institutions which operate in Southern Europe

RESULTS, LESSONS LEARNED, AND FUTURE WORKS

Next the evaluation of the users accessing = confidential information is presented, that is, both the banking intranet, extranet and Internet information. This evaluation has been grouped in relation to the analyzed banking institutions:

• Banca di Roma (Italy)

• Banca Nazionale del Lavoro (Italy)

• Banca Popolare (Italy)

• Banco Bilbao-Viscaya (Spain)

• Bankinter (Spain)

• CaixaBank (Spain)

• Citibank (Spain)

• Lloyds Bank (Italy)

• Sabadell-Atlantico (Spain)

• Unicredit (Italy)

The lessons learned from the current work can be summed up in three large areas. In the first place, the results obtained make apparent that the interactive design of the online systems

for banking institutions will not be able to give back the confidence and credibility of the information from those institutions to their clients or Internet users in all countries and regions south of Europe. Besides, the make-up operations which some financial institutions have made such as the change of name, linked to the pseudo interest towards the art, the sciences, the social assistance, grants, etc., can do little or nothing to solve the communicability problem between their websites and the references towards the real world, whether in relation to emulation or simulation situations of the reality of some interactive services of a high level of safety but of little informative transparency towards the clients or inexperienced users in the use of computers. Second, from the point of view of the online communicability of the banks there is a process to emulate the digital newspapers. This statement stems from the studies of the design categories belonging to the presentation of data in the interfaces as well as the way to distribute the contents on the screens of computers or mobile phones. However, the banks and the digital newspapers have plumped for the Argentinization of the interactive design, starting by the use of colours, and the topological distribution of the contents on the homepage, comparing them with the portals of banks and newspapers in France, for instance. Finally the human factors linked to the global economic context from 2008 to 2012 slow down the technological advances in the issue of safety which could be implemented in the online banking transactions. Besides, there is a rej ection towards those institutions with which the digital gap between clients and banking services will increase in the next years. A way of cutting it down would be to increase the operations in real time and reducing those which are made in the batch modality. In future works we will enhance the number of users in the experiments in keeping with the goal that the clients have at the moment of having access to the banking services and inserting motley categories of users, for instance, trade clerks, industrial workers, university students, freelance professionals, researchers. We will also include banking entities from the north of Europe to contrast them with the south of Europe.

Figure 9. The loss of credibility of the information and trust in the computerized services of the banking and/or financial institutions: Minimum value 0; maximum value 10

CONCLUSION

The negative human/social factors should be radically eliminated in the banks. Instead of carrying out operations of institutional make-up such as the sudden interest towards culture, nature, education, which do not help to restore a truthful and reliable interrelation between users and financial interactive systems. The institutional image of many financial entities with the global crisis has been totally destroyed in the credibility of millions of small and middle customers in the south of Europe. This is an image that was based on the absolute trust of the excellent clients or inexperienced users in computers. However, many of them have been swindled by the institutional communication. For instance, through the deceitful publicity design which has circulated in both a digital and an analog format. Those responsible for that mess have not reacted to the global crisis and keep on making portals where the “copy and paste” of foreign models prevails. See as an example the Argentinization factor of design. Perhaps the use of that fashion of the interactive design responds to the fact that the scandals occur always very far from where the banking institutions are located for which the interfaces for the computer systems are created. In the Spanish ATMs we have so far seen a minimalist design to facilitate the operations to millions of users for decades but little or nothing remains from that quality from the point of view of communicability in the current online systems. The online banking portals today not only have communicability errors, but also usability errors. Theoretically the usability problems in the interactive design should be overcome in the current era of communicability expansion.

REFERENCES

Alison, F. et al. (1995). Colours of life. Torino, Italy: La Stampa.

Brown, D. et al. (2002). Evaluating web page color and layout adaptations. IEEE MultiMedia, 9(1), 86-89. doi:10.1109/93.978356

Cipolla-Ficarra, F. (1997). Evaluation of multimedia components. In Proceedings of IEEE Multimedia Systems. IEEE.

Cipolla-Ficarra, F. (1998). MEHEM: A methodology for heuristic evaluation in multimedia. In Proceedings of 7th Symposi um on Analysis, Design and Evaluation of Man-Machine Systems - Human Interface. Kyoto, Japan: Elsevier.

Cipolla-Ficarra, F. (2005). Synchronism and diachronism into evolution of the interfaces for quality communication in multimedia systems. In Proceedings of HCI International 2005. Las Vegas, NV: HCI.

Cipolla-Ficarra, F. (2012). New horizons in creative open software, multimedia, human factors and software engineering. Bergamo, Italy: Blue Herons Ed.s.

Cipolla-Ficarra, F., et al. (2011). Handbook of computational informatics, social factors and new information technologies: Hypermedia perspectives and avant-garde experiencies in the era of communicability expansion. Bergamo, Italy: Blue Herons Ed.s.

Cipolla-Ficarra, F., & Cipolla-Ficarra, M. (2008). HECHE: Heuristic evaluation of colours in homepage. In Proceedings of Applied Human Factors and Ergonomics. Las Vegas, NV: AIE.

Gage, J. (2000). Color and meaning: Art, science, and symbolism. Berkeley, CA: University of California Press.

Karat, C., Brodie, C., & Karat, J. (2006). Usable privacy and security for personal information management. Communications of the ACM, 49(1), 56-57. doi:10.1145/1107458.1107491

This work was previously published in Advanced Research and Trends in New Technologies, Software, Human-Computer Interaction, and Communicability, edited by Francisco Vicente Cipolla-Ficarra, pages 71-82, copyright 2014 by Information Science Reference (an imprint of IGI Global).