HOW DO ONLINE LENDERS DIFFER FROM BANKS?

Despite the emergence of online lending, bank credit is still the main source of small business credit. But, since the financial crisis, alternative sources of capital have grown significantly.

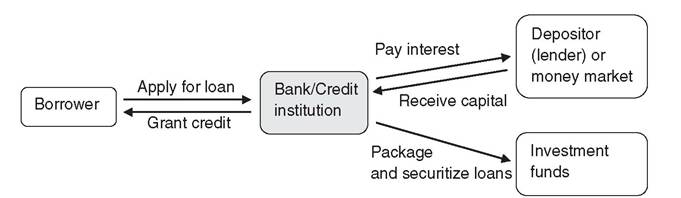

How do online lenders differ from established credit institutions? To answer this question, let's first examine how the lending process of established banks works in Figure 2.1.In their lending operations, banks make capital available to borrowers, or—in banking parlance—obligors who have the obligation to pay back a loan with interest. They raise capital from two main sources: from depositors who keep a savings account with the bank and from capital markets. When banks lend depositors' funds out as loans, they keep the spread between the rate they pay to depositors and the rate that obligors need to pay. When the interest rate is low, then banks have a better chance of generating a spread in their lending operations. In this case, they might raise additional funds from the capital markets. For this to work, banks need to balance their liquidity carefully so they never run out of cash. This is the job of the treasury,

which makes sure that the bank always has a good idea of the risks it has taken on and the obligations it needs to fulfill. We will discuss all this in more detail in the second part of the book, when we learn more about the operations of treasury in traditional bank lending. For now, let's acknowledge that banks are both lenders and borrowers at the same time, and that the loans they underwrite enter their balance sheet. This means they are liable if a borrower is unwilling or unable to pay back a loan. Obviously, it is in the interest of banks to take on as little risk as possible, but enough to still turn a profit. Some risk is necessary, but as long as banks understand this risk, they can manage it.

Some online lending platforms function in similar ways to banks: online balance sheet lenders raise money from private investors and lend it to borrowers. However, this is markedly different from the way in which marketplace lending platforms operate. At the same time, what all online lenders have in common is that they drive down their overhead by automating as many processes as they can. Let's look into the different types of online lenders and how they operate in more detail.

2.2