TYPES OF ONLINE LENDERS

Most people believe that all online lenders are peer-to-peer or marketplace lending platforms. This is incorrect. There are several different business models in online lending, and marketplace lending is just one of them.

However, even though their business models differ, all online lending platforms have several attributes in common. Table 2.1 summarizes the most important of these attributes, their goals and challenges.Authors Karen Gordon Mills and Brayden McCarthy identify three different kinds of alternative online lenders: online balance sheet lenders, marketplace lending platforms, and lender-agnostic marketplaces.7

Table 2.2 sums up the three types of online lenders, their business models, and challenges.

Let's now visit each of the three online lending business models in more detail.

2.3.1 Marketplace lending platforms

Marketplace lending or peer-to-peer lending means that individuals (“peers”) lend directly to borrowers without going through a traditional financial intermediary. Other names for this type of online lending are “social lending” and “lend-to-save.” Peer-to-peer lending underwent a rebranding as marketplace lending because many investors in loans are actually large investments funds and not the peers of borrowers. Marketplace lending is a more accurate term than peer-to-peer lending. In this book, we use the terms marketplace lending and peer- to-peer lending interchangeably to describe the same thing.

Marketplace lending platforms connect institutional and retail investors with prime and sub-prime quality borrowers, and many of the platforms use a proprietary credit model to assess borrowers. Revenue comes from origination fees and service fees. These lenders work by matching lenders and borrowers online. Their loans are short- to medium-term with a maximum term of 60 months, and their interest rates are fixed.

The innovation in marketplace lending is that platforms are not raising capital by themselves to lend. Instead, they connect willing lenders with borrowers directly, which allows them to reduce operating costs while maintaining scalability compared to a consumer loan department within a traditional bank. Their value proposition lies mainly in lower interest rates for borrowers than credit cardsTABLE 2.1 Actions, characteristics, goals, and challenges of online lenders

| Actions and characteristics | Goals Challenges |

| Transactions take place online on a largely automated platform; Heavy use of technology and Big Data | Matching supply and demand Intransparency when models without organizational are proprietary and overhead, lower search undisclosed; Potential costs and due diligence incongruency of data cost sources |

| Development of proprietary credit models for loan approvals and pricing | Superior credit scoring and Intransparency when models default preemption are proprietary and undisclosed; Overreliance on Big Data analytics as the only form of risk management |

| Offering online and mobile loan applications (often done in under 30 minutes) | Simplicity of application, Security; accuracy of speed of capital delivery, customer information greater focus on customer service; Verifying borrower identity, bank account, employment and income, performing credit checks and filtering out unqualified borrowers |

| Attractive to borrowers who have no other choice but seek alternative lenders High loan approval rates, on average above 60 percent (vs. around 20 percent traditionally)8 Platforms offer investors higher returns than conventional debt | Tapping into a market with Quality of counterparty, high high demand, generating correlation of borrowers, high fees for credit concentration risk Attracting borrowers with a Credit quality; Avoiding the high chance of approval; stigma of sub-prime Attracting lenders with high funding liquidity Attracting lenders with high Procyclical business model yields may disappoint under stress; Uncertain performance in times of economic downturn; High correlation of funding sources |

| Marketplace loans are uncollateralized; Loans are not protected by government guarantees | Rapid decisioning in the High-risk investments; absence of hard assets; Uncertain performance Tapping into a market with under stress; Difficult risk high demand, generating management high fees for credit |

or other alternative lenders, attractive returns for individual investors, and simple electronic interfaces for efficient transactions between lenders and borrowers.

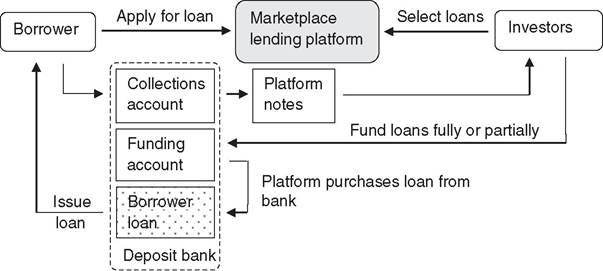

Figure 2.2 describes the marketplace lending process. This process has evolved over time, and it may change again in the future. Still, the overall mechanics will most likely remain.In contrast to other online lending platforms, marketplace lending platforms cater to both borrowers and lenders at the same time. Most retail investors can invest in loans on these

| TABLE 2.2 | Online lenders, business models, challenges | ||

| Marketplace lender | Online balance sheet lender | Lender-agnostic marketplace | |

| Description | Connects institutional and retail investors with prime and sub-prime quality borrowers; Proprietary credit scoring models; Loans remain off the balance sheet of the lender | Raises funds and lends them through three main channels: direct, platform partnerships, and brokers; Operates similar to a bank, but is unregulated; May package and securitize loans; Loans are on the balance sheet of the lender | Lists lenders and borrowers similar to a registry or catalogue; Loans remain off the balance sheet of the lender |

| Business model Commissions; Spread; Fees | Spread; Fees | Commissions | |

| Challenges | Regulatory uncertainty; High correlation of capital sources; Potentially risky loans might underperform in economic downturn | Regulatory uncertainty; High correlation of capital sources; Potentially risky loans might underperform in economic downturn | Not a financial institution but an information resource; Will not enjoy returns of a lending platform |

platforms, and they can diversify their investment across many loans. Because platforms have no banking license, they cannot accept deposits from investors directly.

To collect and transfer payments from lenders to borrowers, the platform uses two accounts at an affiliated depository bank: a funding account and a collections account. The early peer-to-peer lending model launched as an auction marketplace where participants determined loan rates by bidding in a Dutch auction system. Lenders had the responsibility for setting rates, despite the fact that they had little understanding of credit risk. Nowadays, platforms set interest rates according to their own internal rating of borrowers. Most investors invest indirectly and partially in

loans. In most instances, investors simply determine which loan grades they wish to allocate capital to and the size of each investment, and the platform does the rest. Each loan has a funding account that gradually fills up according to the risk appetite of lenders. This account serves a similar function to an escrow account, to ensure investors have the capital available that they promise the borrower. Once the funding account reflects the amount the borrower specified, the depository bank will advance the loan to the borrower. At the same time, the marketplace lending platform operator purchases the borrower loan from the depository bank at nominal cost with the funds in the funding account. The marketplace lending platform then issues so-called platform notes to the investors. Each note is a small fraction of the full loan amount, and it reflects the amount a lender invested in the loan. Notes work like fixed income instruments with regular principal repayment and coupon payments. The platform operator collects loan repayments from the borrower in a collections account from which he draws the payments for the platform note. A diversified portfolio of platform notes on marketplace loans can easily exceed the returns available through investment vehicles such as money market funds and certificates of deposit, but it can also be volatile and risky.9,10 Platform notes can be resold: Lenders can often auction off their notes on platform-specific marketplaces.

On some marketplace lending platforms, lenders pay a fee on the amount they lend to borrowers per year. Borrowers pay a borrowing fee if their loan application is approved. Marketplace lenders typically target mid-prime or near-prime borrowers and lend larger amounts for longer terms.

2.3.2 Online balance sheet lenders

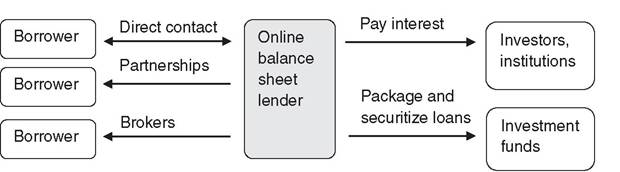

Online balance sheet lenders originate small business loans through three main channels: direct, platform partnerships and brokers. They use their own balance sheet and are raising capital from private and institutional investors. This is similar to how existing banks operate, and some online balance sheet lenders also package and securitize their loans.

The direct channel allows companies to select and contact borrowers through a variety of marketing techniques including direct mail, online media, and email. In platform partnerships, companies connect with prospective borrowers through strategic relationships with third party partners that have access to the small business community. Some balance sheet lenders partner with established banks and credit institutions for small business lending, with the platforms serving as the banks' prospecting, distribution and performance-monitoring systems.11 Through the broker channel, companies connect with prospective borrowers by entering into relationships with third-party independent brokers that typically offer a variety of financial services to small businesses including commission-based business loan brokerage services.

Balance sheet loans are typically short-term up to 24 months, and they fund working capital and inventory purchases for small and medium enterprises. Many of these loan products operate in a similar way to merchant cash advances, with a fixed amount or percent of sales deducted daily from the borrower's bank account over several months. Their business model is spread-based, as in conventional bank lending. Online balance sheet lenders use technology to automate their processes and to score their borrowers with data that banks rarely consider.

For example, they might screen a borrower's social networking accounts and instant messaging channels, investigating her connections and analyzing her posts. The loan application and decision process often take minutes, which is much faster than in a bank. On the whole, online

FIGURE 2.3 Lending process of an online balance sheet lender

balance sheet lenders function in similar ways to banks. Figure 2.3 describes the process of online balance sheet lenders.

Some online lenders are in essence just unregulated banks that issue uncollateralized loans. Online balance sheet lenders have no banking license. This prevents them from accepting deposits from retail investors. However, they invest capital from investment funds and other accredited investors. These platforms usually cater to borrowers only, and they secure funding for individual deals on the backend. To administer payments to investors, they rely on custodian accounts from licensed banks. Online balance sheet lenders charge origination fees on their loans as well as maintenance fees.

2.3.3 Lender-agnostic marketplaces

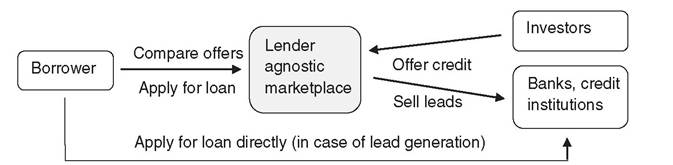

Another emerging online player in small business lending exists in the form of lender-agnostic marketplaces. This type of online lender creates a marketplace for borrowers to compare a range of loan products. On these platforms, term loans, lines of credit, merchant cash advances, and factoring products are on offer from alternative lenders to conventional banks, community banks, and regional banks. These online marketplaces reduce search costs, one of the biggest problems borrowers and lenders face. Figure 2.4 outlines the process of a lender-agnostic marketplace.

These marketplaces earn revenue by charging fees on top of the loan if a borrower gets funded and accepts the terms of a loan from the platform. Some of these lenders also sell business leads and contact details to loan officers. Such platforms are increasingly experimenting with ways to partner with banks, particularly community banks. Lender-agnostic marketplaces are encouraging banks to send small business borrowers they turned down to their online marketplace.

In this book, we focus on marketplace transactional marketplaces, which we will call marketplace lenders or peer-to-peer lenders from now on. Let's investigate the different meanings of the term peer-to-peer so we have clarity about the definition of the term.

FIGURE 2.4 Lending process of a lender-agnostic marketplace

2.3