SOME BACKGROUND ON PEER-TO-PEER NETWORKS

At the heart of a peer-to-peer (P2P) network architecture lies the idea that entities or peers can connect directly with each other. This is trivial in a sense, as one might argue that all interactions between people are direct in nature.

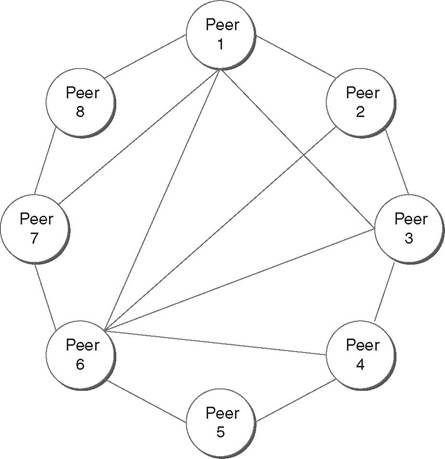

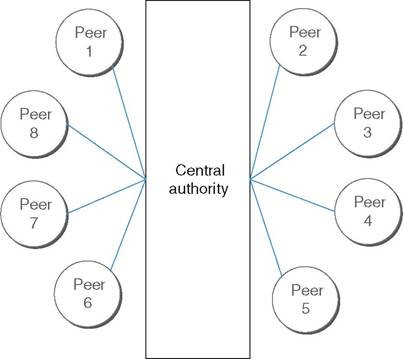

When the number of peers is small, this is true. They can easily find each other and match at a low cost. For example, as illustrated in Figure 2.5, all eight peers in the network can easily link to each other directly or indirectly. Assume that peer 6 would like to connect with peer 1: peer 6 can link to peer 1 either directly or via combination of peers, for example, {2}, {3,2}, {4,3,2}, {5,4,3,2}, {7}, and {7,8}.However, in a large set of peers, search costs are high. If many sellers and buyers exist in a market, it would take forever to meet every single person with whom they might want to enter into a transaction. In this case, a central authority may take on the burden of pooling all peers on one side of the transaction—such as the sell side—and represent itself as one peer that the other side can buy from. An example would be a supermarket; all producers sell directly to the supermarket, which becomes the convenient place to go for all buyers of produce. However, this convenience comes with several disadvantages. For instance, the central authority has a lot of power over buyers, as it is now the monopolist in the market with the power to set prices. If a supermarket has managed to lobby for laws that prevent individual sellers from selling directly to buyers, both sides are at the central authority’s mercy. Sellers have only one party to sell to, and buyers have only one party to buy from (Figure 2.6). This form of interaction is no longer a peer-to-peer network.

Even though the central authority often argues that the convenience he provides to customers comes at a high cost which justifies a high price, a centralized system is rife with the

FIGURE 2.5 Peer-to-peer networking with direct and indirect connections

FIGURE 2.6 Centralized systems architecture, a supplier-oriented marketplace

potential for abuse.

Is this really the best and most convenient system to transact? Clearly not. Enter peer-to-peer networks where many peers connect directly.For direct connection to be economical, peers must have information about each other. When all peers already know each other, this is simple, but the burden of finding the right peer quickly increases with the number of peers in a network. At the same time, a system with many peers benefits strongly from network effects: the more individual peers exist, the more permutations for connections exist, which gives buyers more variety and sellers a bigger market. However, there must be a mechanism or platform for peers to gather information about each other, which will facilitate connections. As a trade-off, peer-to-peer platforms allow only bilateral connections among lenders and borrowers, not linkages via other peers. As you can see in Figure 2.7, peer 6 can have only bilateral links with all others in the system (peers 1, 2, 3, 4, 5 and 7).

The scale of centralized structures that we saw in Figure 2.6 had clear advantages for users who had no other way to access a market or gain information about potential trading partners. However, with the emergence of the biggest peer-to-peer network in history, the internet, it has become easier to collect, structure and make available searchable information about a large number of peers. In a sense, online peer-to-peer networks reintroduce the ancient way of direct interaction that humans used in trade hundreds of years ago.

Whenever we bring up the term peer-to-peer, most people first think of illegal file sharing services, such as Napster. In technical terms, Napster was a first-generation peer-to-peer system: it still relied on a centralized server structure that eventually proved its Achilles heel. The system could have detected illegal file sharing activity on its infrastructure but chose to ignore it. Subsequent protocols, such as Gnutella or BitTorrent, did away with a central directory.

They completely distribute file searches and transfers among corresponding peers, with some systems, such as FreeNet, even providing client anonymity. The most advanced systems route requests indirectly through other clients and encrypt messages between peers. Illegal file sharing brought peer-to-peer applications into the mainstream. A few years later, the voice over P2P (VoP2P) application Skype proved that peer-to-peer technology had wider

FIGURE 2.7 Peer-to-peer platforms allow only bilateral linkage among peers

uses that also worked as a commercial business model. It expanded into other arenas, such as television, with P2PTV.12

2.4.1 Disintermediation or re-intermediation?

By encroaching on the turf of the established financial sector, FinTech startups profess to disintermediate the established players. Some platforms connect lenders and borrowers directly in a marketplace, so they make the gatekeeper obsolete, they say. Providers of mobile wallets and payment processors profess to abolish credit card companies. Cryptocurrencies aim to unseat central banks. However, even though a platform may be neutral, it will reroute traffic from elsewhere through its proprietary infrastructure. It is therefore more accurate to speak of a re-intermediation, not a disintermediation. Even though some of the startups may disagree, if their business models prove successful, there will simply be a new sheriff in town, in the form of the platform, ruling over a particular niche. Over time, these new incumbents will suffer a similar fate like the established players they unseated. They will have to be vigilant to stay agile, continuing to innovate.

The same has happened in other sectors, where technology has upended established companies. The book trade, for example, has seen widespread disruption, where traditional retailers of books and their publishers gave up a large market share to online marketplaces.

The music industry suffered a similar fate: instead of major music labels, a computer company— Apple—now dominates the online music space. While new entrants initially promised a flatter system devoid of monopolies, they have become the new monopolists themselves. Instead of watching for disintermediation, look out for re-intermediation and automated intermediation in the FinTech space. Because financial services are at the heart of every business in the economy, the issue might be more serious than the discussion about selling books or music online. Unless we understand the roles of new entrants clearly, we could end up with a gigantic shadow banking system that concentrates more risk on fewer unregulated intermediaries, which makes the system inherently unstable.2.4.2 Infomediaries, intermediary-oriented marketplaces, and the information value chain

Information is a powerful enabler of peer-to-peer networks, and the spread of online transactions has given power to a new kind of intermediary: the infomediary. Authors John Hagel and Jeffrey Rayport coined the term to describe the function of a central negotiator who collects information about customers and helps them identify the best deals. Negotiations with consumers for information cost time and money, and the information is often messy and hard to compare. At the same time, many companies may collect information about customers, but they organize them poorly. When Hagel and Rayport wrote about infomediaries in 1997, they noted the process of collecting consumer information was already under way. However, they pointed out that it might take several years to play out across broad segments of customers and products.13 Advances in online commerce and technology have pushed the necessity for information about counterparties into the mainstream. Consumers are also increasingly willing to share private information, such as their financial data, when they can benefit from it. When we look at the onboarding process of marketplace lending platforms, it becomes immediately obvious that information is at the core of this business.

At every step, online lending platforms are trying to get the customer to give up information that platforms can use later to customize their services. With every interaction on their platform, online lenders are building an information supply chain.When we compare the model of the infomediary to the supermarket we just discussed, we see how the supermarket could transform its business model to become an infomediary: instead of purchasing produce from sellers, it could simply collect information about their inventory in a database. When a buyer enters the store—offline or online—she could query that database and see which seller offers what she wants at this particular point in time. The buyer would then pay for the information and collect the products directly at the seller's location. Of course, markets have been infomediaries for quite a while. In parallel to the core business of selling produce, they have always collected information about buyers. Nevertheless, now that shopping increasingly shifts online, information has become more valuable and more important. Buyers search a database of products on a website where they complete the transaction. The seller receives a notification of a sale and the shipping address of the buyer to fulfill the purchase. This insight is by no means revolutionary because many marketplaces that operate this way exist, such as eBay, Amazon, or Alibaba. They are what author Dave Chaffey calls intermediary-oriented marketplaces, contrary to supplier-oriented marketplaces (which we saw in Figure 2.6) and buyer-oriented marketplaces. The organization that finances and runs the platform determines the orientation of a marketplace. In supplier-oriented marketplaces, the sellers of a good or service invest in information technology to attract buyers. In finance, this is what a bank would do by making available loan applications online, or by investing in online banking. When firms invest in setting up buyer-oriented marketplaces, they do this with the goal of reducing their procurement costs.

Potential suppliers then compete for the business of the buyer. Only large corporations can afford to run such a marketplace, such as General Electric, or governments who request proposals for tenders. The advantage of an intermediary-oriented marketplace is that buyers and sellers incur no cost to run the marketplace and maintain the technology. Marketplaces are neutral and only help to match buyers and sellers in a virtual environment with lower transaction costs for all counterparties.14 Many network systems have developed with the idea of decentralization in mind. Even though they may not necessarily meet the technical definition of a peer-to-peer software application, distributing a resource across its users has many applications offline as well. Most commercial peer-to-peer systems benefit from using a central directory to organize the information about individual peers. This is a prerequisite for facilitating the exchange of value between individual peers. If enough users are connecting directly between each other, and are part of a network, the network itself becomes valuable. For example, think of the car-hailing service Uber: how useful would it be if there were only a handful of drivers connected to a large number of customers? Customers may have to wait a long time until drivers became available, and they might just as well use a taxi at a higher cost. However, when customers have ample choice between drivers, network effects kick in and customers ride faster and cheaper by using the service. Network effects bring down the search cost and transaction cost.2.5

More on the topic SOME BACKGROUND ON PEER-TO-PEER NETWORKS:

- GOVERNANCE IN PEER-PRODUCTION COMMUNITIES: DIVERSE REDUNDANT MECHANISMS

- Opportunities for parliamentary accountability

- Understanding Context

- Emotional and Mental Well-Being in Multiple Pregnancy

- Introduction

- Economics in an Engineering School

- Youth in Sri Lanka

- Physicians

- Bauer J., Latzer M. (Eds.). Handbook on the Economics of the Internet. Edward Elgar,2016. — 603 p., 2016

- Faith and disenchantment