Chapter 46 Corruption’s Effect on Foreign Direct Investment: The Case of Bosnia and Herzegovina

Elvira Pupovic

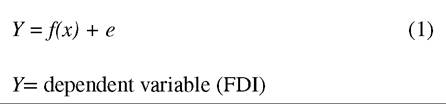

University of Montenegro, Montenegro

ABSTRACT

This study introduces a new perspective on the role of corruption in investment growth and provides quantitative estimates of the impact of corruption on the investment inflows.

Motivated by these issues, the main objective of this article is to empirically reexamine the effects of corruption on foreign direct investment (FDI) inflows in Bosnia and Herzegovina, by incorporating a further link between corruption and investment inflows as new understanding investment concepts. Using data from Transparency International report, World Bank and National Banking Statistical data, it is manifested in a cross sectional setting that corruption has a negative and significant impact on the foreign direct investment inflows. The new model of eliminated unexpected risk involved managing corruption’s effect on investments. One has to immediately consider the linkage between corruption and investment inflows and to learn how to manage this phenomenon like old risk of a new model.1. INTRODUCTION

A thorough understanding of the causes and consequences of corruption is an ever more pressing problem in the context of the challenges that supranational identities such as the European Union have to face in the forthcoming integration process of the transition countries. Only through this process will it be possible to find policy recommendations that target the problem precisely and discover viable solutions to the adverse effects of corruption such as the problem of income gap between the rich and poor regions of the world, which is for the most part due to the poor growth performance of the latter group. From a global perspective, it is extremely important to understand what role corruption plays in relation to growth, in order to come one step closer to the solution of the aforementioned problems.

Before proceeding further it is a good idea to define corruption for the purposes of this study. Corruption is commonly defined as the misuse of public power for private benefit. The act often consists of paying bribes to public officials by private beneficiaries as compensation for the abuse. However, not all acts of corruption result in the payment of bribes. A powerful minister can locate a new investment project in his home town unsuitable for that particular activity or he could influence the sanctioning of big business loans to his relatives and friends and still not take any direct bribe. This is indirect cash and capital inflows.

DOI: 10.4018/978-1-4666-6268-1.ch046

.

Hence, corruption was claimed to have a beneficial face that made Pareto efficiency tenable. This is known as the greasing the wheel argument and was supported by Leff (1964) and Huntington (1968) among many others. Holding the line, on the other side of the argument was the Nobel laureate Gunnar Myrdal. For example, Myrdal (1968) argued that bribes were a source of inefficiency, and even the sheer possibility of collecting bribes was enough to induce the bureaucracy to create artificial bottlenecks. To put it differently, corruption provided the wrong incentives. As such, it would then be expected to sand the wheels. Papers that have been mentioned so far mainly included theoretical approach and did not offer much in the way of state of the art mathematical treatments of this subject. In the 1980s corruption started taking its due share from a more formal treatment. One relevant example is Lui (1985) where in the context of a queuing model it was shown that corruption induced efficient outcomes in that the ones with the highest willingness to pay bribes were exactly the ones who had the highest opportunity costs of waiting.1

Corruption was also seen as a classical example of a phenomenon that is observable, but not measurable, Dogan and Kazancigil (1994). This picture changed drastically with the seminal work of Mauro (1995) that provided us with the first empirical treatment of the relationship between corruption and growth by using a cross-sectional analysis.

The presence of corruption causes substantial economic costs on an economy. Corruption is a double edged sword; it reduces both the volume and efficiency of investment and thus economic growth. This note identifies a simple concept of the macroeconomic efficiency of investment, establishes its linkage with corruption and estimates the relationship between them.

The aim of this paper is to highlight the relationship between corruption and the inflows of foreign direct investment in detail for the case of Bosnia and Herzegovina. However, to make motivation in this venture clear, it is necessary to say a few words on the relationship between corruption and growth, especially concerning the history of this topic. That corruption is one of the most ancient problems of mankind is well-known. However, how it affects economic growth has always been subject to debate. Under what can be termed as “greasing versus sanding the wheels debate,” scholars have forwarded ideas in either direction. In the first wave of the literature, it was not uncommon to argue that bribes act as speed money and help avoid bureaucratic efficiencies.

As mentioned above, first aim is to take a general look at this aforementioned relationship with using indicators of corruption. As expected, the regressions testify to a strong negative impact of corruption on FDI Inflows. Having done this, then decompose the corruption variable and test whether or not different perceptions of corruption have statistically different impact on the FDI Inflows. The answer to this question is also affirmative. The theoretical and empirical analysis suggests that the main fields through which the impact of corruption on FDI flows materializes are the crucial elements of business environment. In this case, granting of import/export permits, access to public utilities, annual tax payments and judicial decisions, are the most appropriate. The efficiency of investment variables computed by the authors and Transparency International’s Corruption Perception Indices are used as data.

The note concludes that substantial gains in terms of economic growth could be achieved if corruption is combating.Third aim is to show new model for measuring corruption effects on FDI. The results of Bosnia and Herzegovina model for measuring corruption impacts to the inflows of foreign direct investment will bring new lesson for understanding bad side of this phenomenon called corruption (cancer of economy).

As for the organization of the paper, Section 2 reviews the literature, Section 3 introduces the hypotheses, Section 4 introduces causes of corruption in Bosnia and Herzegovina, Section 5 introduces the results of Bosnia and Herzegovina model for measuring corruption impacts to the FDI, Section 6 presents the findings and discussion and Section 7 brings the conclusion.

2. LITERATURE REVIEW

2.1. Linkages between Efficiency of Investment and Corruption

In the recent past there have been a number of studies that have reported quantitative results on the effect of corruption on economic variables. These studies have used cross-section analysis of available corruption indices and relevant economic indicators.

Examining the relationship between FDI and the risk factor of the host country, Wheeler and Mody (1992) fail to find a significant relation. The justification of citing this study here is that the authors used a country risk variable that included corruption among others; moreover, this overall variable was highly correlated with corruption. Hines (1995) is a study based on US outward investment data, which leads to the conclusion that FDI is negatively related to the level of corruption. Hines, however, suggests that this is due to the U.S. Foreign Corrupt Practices Act of 1977.

Wei (2000) investigates whether or not FDI flows from US and other source countries are statistically different by using data on bilateral flows between 14 source countries and 45 host countries for the years 1990 and 1991. He concludes that corruption has a negative and significant impact on the levels of FDI, and that this impact does not vary according to the source country.

Smarynzka and Wei (2000) argue that host country corruption induces foreign investors to favor joint ventures over wholly owned firms. Lambsdorff and Cornelius (2000) maintain a negative impact of corruption on FDI for a sample of African countries. Wei and Wu (2001) is another study investigating the relationship between corruption and capital flows. The main conclusion of this paper is that corruption impacts on the composition of capital inflows in a way that reduces FDI, and increases the countries’ reliance on bank loans. This, in turn, makes the country in question more vulnerable towards financial/ currency crises.

Habib and Zurawicki (2001) examine the impact of corruption on both foreign direct investments and local investments. Accordingly, corruption has a stronger negative impact on FDI than on local investments. Lambsdorff (2002) asks the question of how corruption influences on the persistent capital flows. This study breaks down investment into two broad categories: domestic savings and net capital inflows. A significant negative impact of corruption on the latter variable is proven. Yet, no distinction is made between different forms of capital inflows. In order to identify potential channels of influence, this study also controls certain institutional variables such as the bureaucratic quality, civil liberty, government stability, and the law and order tradition of a country. A somewhat surprising result emerges in that the author finds all but the last variable to matter for attracting capital inflows.

On the flip side of the coin are a series of studies which remain inconclusive on the above mentioned link. Using cross-sectional data, Ale- sina and Weder (1999) fail to produce a significant parameter estimate for the corruption variable on FDI in spite of trying a series of model specifications. Working on data for Sub-Saharan Africa, Okeahalam and Bah (1998) also produce inconclusive results. To wrap up, it is fair to say that the literature has produced mixed results regarding the impact of corruption on FDI.

For the purpose of this research, in addition to previous research on this subject, the results of a survey conducted recently were also taken into consideration and will be specified later. The pioneering effort in this area was the study by Mauro (1995) who found that corruption lowers investment and thereby economic growth. Later, the study by Tanzi and Davoodi (1997) further extended and elaborated this line of causality by showing that corruption increases public investment while reducing its productivity.

The relationship between corruption and investment has long been a contentious area of research. Two deep and broad presumptions can be made regarding the effect of corruption on the efficiency of investment (EII). First, corruption distorts the sectoral allocation of investible resources by diverting resources from potentially productive sectors to unproductive sectors and thereby decreasing the overall output-generating capacity of the investment. A good example of the phenomenon in recent times has been the acquisition of large volumes of loans by many entrepreneurs in South East Europe countries by colluding with bank officials. These resources, sometimes obtained by fraudulent means, were often invested in unproductive sectors or activities, which contributed to the increase in nonperforming loans and the eventual contraction of gross domestic product (GDP) during the recent global economic crisis. A review of various forms of corruption, their causes and consequences can be found in Tanzi (1998) and Rose- Ackerman (1996). However, irrespective of the types or forms of corruption, it needs no argument that, as the act involves subjective misuse of power, it is both bad and illegal. In addition, the act distorts the purpose for which the discretionary power was given to the person who abuses it. These distortions inflict considerable costs on the economy.

Rose-Ackerman (1996) also notes that for business people in Eastern Europe payoffs are often necessary to obtain credit. Thus investments are made not on the basis of their rates of return but on the capacity of the entrepreneur to pay bribes.

The concept of FDI is a measure of foreign ownership of productive assets, such as factories, mines and land. Increasing foreign investment can be used as one measure of growing economic globalization. Representing the net inflows of foreign direct investment as a percentage of gross domestic product (GDP) makes the model to evaluate the impact of corruption on FDI efficient. The largest flows of foreign investment occur between the industrialized countries (North America, North West Europe and Japan). But flows to non-industrialized countries are increasing.

Bribes, which are often the major part in any act of corruption, increase the cost of production which ultimately gets reflected in a higher output price increase, reduction in demand and the eventual reduction in the incremental output capital ratio for the activity. Rose-Ackerman (l996) notes that a corrupt firm may bribe officials to win a contract and once selected it may pay again for the opportunity to charge an inflated price or to skimp on quality. Also, when firms and entrepreneurs are selected to undertake investment projects on the basis of their ability to establish crony contacts and pay bribes, there is no guarantee that the most efficient firm will be chosen. In fact, the efficient but unscrupulous entrepreneurs will almost always be rejected. Inefficiency and unfairness as the costs of corruption have been ably discussed by RoseAckerman (1996). Ultimately, the inefficiency will manifest itself as an output price increase and lead to a reduction of the incremental output capital ratio of the activity or sector. The above discussion lead us to formulate the following hypothesis: an increase in corruption will lower the efficiency of investment.

It means that when CPI increases or the level of corruption decreases there is a significant (with a probability of more than 95 per cent) increase in the efficiency of investment.

Efficiency of investment (EII) during any period under investigation is defined as the ratio of the annual average growth of real GDP to the annual average growth of real investment. The variable EII for a particular country represents the efficiency (productivity) of total investment during a period in generating value added and depends on how total investible resources are allocated between various sectors of the economy and the sectoral incremental output capital ratios. The latter can be taken as a measure of sectoral rates of return in a macro sense; higher values signifying higher returns and thus higher productivity of investment.

2.2. Corruption Effects on FDI

The first data about corruption was created by Business International (BI) (1984), a subsidiary of The Economist Intelligence Unit. The data set measures “the degree to which business transactions involve corrupt payments” on a scale of 1 to 10 for the period 1980 to 1983 and covers nearly 7o countries. Before this, corruption indices could have been derived from the Institutional Quality indices but these were not widely available.

World Economic Forum in Switzerland produced Global Competitiveness Report, a business publication which consists of a survey of top and project managers in the most dynamic firms of a large number of countries. Political Risk Services Group (PRSG) also started reporting corruption data and the measure of corruption for the countries.

Following theoretical arguments pointing to the damage corruption inflicts on the economy, several studies looked at the impact of corruption on the inflows of foreign direct investment. Many authors corroborated the assumption that corruption is a detriment to FDI and hence a liability to the host economy.

Based upon general economic studies showing the adverse impact of corruption on economic growth, inflation and investment, it follows that the logic would generally apply to foreign investors as well.

The first studies attempted then to isolate and estimate the overall impact of corruption on FDI. Expected, the format applied to such analysis was based upon the gravity models in which corruption as an independent variable was used along with the control variables such as the GDP of the host country and its growth rate, the GDP per capita, tax and exchange rates, labor market conditions (wages, unemployment), the degree of internationalization of the recipient economy, distance from the global markets, and political risk. Some variations also included other factors such as availability of the natural resources, the historical ties (metropolisformer colony), technological development and others. It is very important to emphasize that the scope of the initial studies was constrained due to the data limitations. First databases pertaining to corruption covered no more than 40 countries. The data did not permit any longitudinal analysis. Because the number of observations available was limited, the number of variables to be included in econometric models also had to be small as not to violate the statistical rules. The first results from this research did not confirm the expected relationship between variables of model. This was caused by the study which was taken for US firms developed by Wheeler and Mody (1992). The results show there is no significant negative relationship between the size of foreign direct investment and the risk factor of the host country, a composite measure which beyond twelve other indicators also includes corruption. A later study showed an overall insignificant effect of corruption on incoming FDI. However, at the same time, this work pointed to a negative impact of corruption on the FDI originating from the USA after 1977. This result was attributed to the effectiveness of the US Foreign Corrupt Practice Act (FCPA)2. Thus, it was not the corruption per se which acted as a detriment to the US outgoing FDI, but rather a perspective of being (severely) punished if caught by home country authorities. This distinction is still important today as it hints to why corruption is a deterrent. In addition, American investors tend to be no more averse to corruption in host countries than (on the average) investors from OECD countries with a possible exception of Japan.

Empirical studies suggest that corruption is, indeed, associated with a misallocation and misappropriation of public expenditures which are often inflated as a result.3 Gupta et al. (2000) find that corruption has the effect of reducing the provision of education and health care, and of increasing infant mortality. Mauro (1997) presents evidence that corruption distorts public expenditures away from growth-promoting areas (like education and health) towards other types of projects (e.g., infrastructure investment) that are less productivityenhancing. In a similar vein, Tanzi and Davoodi (1997) find that corruption leads to a diversion of public funds to where bribes are easiest to collect, implying a bias in the composition of public spending towards low-productivity projects (e.g., large-scale construction) at the expense of value-enhancing investments (e.g., maintenance of the existing infrastructure). The same authors conclude that, as a result of corruption, the amount of public investment tends to rise, while the quality of this investment tends to fall, where the latter are measured for example by the number of paved roads in bad condition and power supply faults.

Empirical results based on investigation from foreign firms of Asia and Latin America show the relationship between indicators of governance and foreign direct investment. Using a sample of countries from Asia and Latin America, that what was demonstrated is about link between corruption, ultimately, and foreign direct investment and its negative correlation. Following theoretical and empirical arguments pointing to the damage corruption inflicts on the economy, several empirical research looked at the impact of corruption on the inflows of foreign direct investment by controlling variables positively correlated with FDI (the rule of law, control of corruption, regulatory quality, government effectiveness, and political stability). The analysis indicates that US firms are less likely to invest in countries where bribery, as measured by the Corruption Perception Index (CPI), is widespread. Many authors examined US Foreign Direct Investment (FDI) outflows with respect to the level of corruption (in the form of bribery) in 42 recipient countries over a five-year period. As might be expected, the size of the foreign market is found to be a more robust factor determining US outward investment, with larger economies attracting more investment. The level of bribery, while significant by itself, loses its importance when included with other economies and cultural variables. The findings are discussed in the context of the Foreign Direct Practices Act (FCPA), which makes it illegal for US firms to bribe foreign officials to obtain business advantages.

It is important to emphasize that valuable inputs into understanding the impact of corruption were gradually produced not only by academics but also through the studies sponsored by business consulting companies. One of them -Control Risks- sponsored a survey which specifically asked a very pointed and differently phrased question: did you hold back from an otherwise attractive foreign investment on account of a country’s reputation for corruption? After this research many opinions were nearer the truth. A positive answer was provided by roughly the same percentage of the European and US companies and averaged 39%.4

By the late 1990s, additional analyses helped to detail the overall understanding of the impact of corruption on the FDI, while some other studies focused on more specific aspects. From the perspective of composition effects of public expenditures, Deverajan et al (1996) have shown that public capital expenditure has a negative effect on growth for developing countries and the effect gets dramatically reversed if the sample is for developed countries. They explain their result by suggesting that “expenditures which are normally considered productive could become unproductive if there is an excessive amount of them” and conclude by saying that “developing country governments have been misallocating their resources” by excessive capital spending. This result has been recently supported by Ghosh and Gregoriou (2007) in an optimal fiscal policy framework, again for developing countries. Interestingly as a suggestion for future work they posit a role for corruption in assuming away possible positive returns from public investment in developing countries. As for the first issue, the new studies attempted to estimate the evil of corruption with respect to FDI. In that respect, the quantitative models demonstrated to what extent corruption is a detriment to FDI relative to other factors.

In a series of studies, the general perception of the harmfulness of corruption and related phenomena received additional support. For example, the effect of non-transparency to foreign investors was tested. The notion of non-transparency combined corruption, unstable economic policies, weak and poorly enforced property rights, and inefficient government institutions that increase the risk and uncertainty associated with business. The corresponding scale was adopted from the International Country Risk Guide published by the US-based Political Risk Services (PRS). The results showed that a high level of non-transparency decreased the flow of foreign investment to the host country.

Further, corruption was shown to be detrimental in a number of ways and linked to other institutional phenomenon. For example, market entry has been shown to deteriorate with high levels of corruption. Empirical studies were proof that countries with heavier regulation of entry have higher corruption and larger unofficial economies. While not specifically concerned with the international enterprises, the results of the study in question certainly prove of their relevance to FDI.

Using data on foreign and local direct investments Habib and Zurawicki (2002) analyze the effect of corruption on bilateral FDI flows using a sample of seven source countries and 89 host countries. They hypothesize that the greater the absolute difference in the corruption level between the source and the host countries, the smaller the FDI inflows for the host countries. They regressed bilateral FDI on a set of control variables including the absolute difference between the corruption levels in the source and host countries. They find that foreign firms tend to avoid situations where corruption is visibly present because corruption is considered immoral and might be an important cause of inefficiency.

It is interesting, though, that the business cost of corruption does not need to be prohibitive and consequently moderates its effect on FDI. Kaufmann (1997) reported surveys in Ukraine on the amount of illegal payment made for various business activities. His results suggest that the payments, on average, amounted to a small percent of total sales. If this is true of most situations then corruption may not be a major deterrent for FDI. Showing the evil of corruption in relative terms (for example, compared to taxing profits) has been a useful method to show the role of various factors affecting FDI. This approach has been pioneered by the World Bank since 1991.5

All these studies use a cross-sectional methodology to test the relationship between corruption levels and FDI inflows, and ignore the fact that corruption is a complex phenomenon. Corruption is correlated with many other characteristics of the host country such as the quality of institutions, lack of competition, and cultural values. Also, there may be time-invariant unobserved effects that vary across countries and are correlated with corruption. Obviously, failing to hold all these factors constant, the estimated effects may be biased in either direction. These studies also have ignored the fact that corruption is not necessarily an independent variable. In particular, the level of corruption may be affected by other variables in the host country as the level of development, level of FDI inflows, quality of institutions and cultural values.

2.3. Consequences of Corruption

Persistent myths refer to corruption as the second best solution in view of inefficient government regulation or to its role as “the grease in the wheels of commerce.” Some of the authors present and then demolishe arguments about efficiency of corruption’s deals. Kaufmann (1998) lays to rest the “grease” argument (while corruption can make one transaction easier, it gives rise to a demand for more corruption - almost like adding sand to the machine, which will then require more grease.

We can say with some certainty that corruption is not good for economic growth and for economic development. It is quite possible that countries marked with bureaucratic corruption (not the efficiency of the allocation process, such as East European countries, witnessed a rapid fall of foreign direct investment because of a high level of corruption.6

Corruption changes prices and, hence, the equilibrium due to shifts in the supply and demand of public services. Corruption introduces distortions in factor markets. While corruption affects the whole economy, it seems to target the poor. First, consistent with current research which points to benefits for the poor from economic growth, corruption hurts the poor by lowering an economy’s growth rate. Second, corruption introduces costs and benefits that create a bias against the poor. Third, corruption can be causally linked to the worsening of income distribution.

A high level of corruption is trying to demolish the whole world economy, inflow of cash, industry, increase inflation by delivering high prices because of ”return of corruption costs,” lack of cash for workers, decline in working spirit, morale and good will for individuals. Because of all these bad things linked with corruption, all of us have to fight this social disease.

3. RESEARCH HYPOTHESES

Starting from the theoretical bases, research topic, and established aims, as well as from the previous and current empirical research results, the following hypotheses are formulated:

H1 - H6: Corruption and non-market rules have a negative impact on inflow of Foreign Direct Investment. These non-market rules are: spread and amount of corruption in public and private business (H1), likeliness to demand special and illegal payments in high and low levels of government (H2), lack of qualitative industrial products (H3), increase of net-exports (H4), decrease of government spending (H5) and increase of gross domestic production GDP (H6);

H7: Corruption consciousness about the consequences of corruption has a positive effect on individuals’ behavior about the negative effect of corruption’s on Foreign Direct Investment.

4. CAUSES OF CORRUPTION IN BOSNIA AND HERZEGOVINA

According to Conclusions on Bosnia and Herzegovina7, Bosnia and Herzegovina has made limited progress in addressing the political criteria. The need for an effective coordination mechanism between various levels of government for the transposition, implementation and enforcement of EU laws remains to be addressed as a matter of priority so as to enable the country to speak with one voice on EU issues and make an effective use of EU’s pre-accession assistance.

Strengthening the functionality and coordination mechanisms of the institutions remains an issue to be addressed as a matter of priority. It can be the first cause of corruption.

According to data obtained by the public opinion survey in Table 1 as the main causes of corruption aside the lawlessness and lack of rule of law, elsewhere there are moral and dishonesty, and the third is the general poverty. It is clear that these are the causes of the different groups. It would be expected to be generally perceived poverty as the main cause of corruption. That would be some sort of justification for all those involved in corruption and thus supplement the budget.

The economy of Bosnia and Herzegovina grew by 1.3% in 2011, supported by reviving domestic demand and - to a lesser extent - still growing external demand. The recovery process was reversed in early 2012 as a consequence of the worsened economic environment. Unemployment remained at very high levels. Some fiscal consolidation took place as a result of increased revenues and some expenditure cuts. However, the quality of public finances remained low and the fiscal sustainability was severely hampered by the

Table 1. Causes of corruption in Bosnia and Herzegovina

| Cause | Yes (%) | No (%) |

| general poverty | 49 | 51 |

| immorality and dishonesty | 45.3 | 54.7 |

| inefficiency of the judicial system | 27.8 | 72.3 |

| legacy of the previous communist system | 7.9 | 92.1 |

| bad legislation | 22.9 | 77.1 |

| war | 24.5 | 75.5 |

| political system | 18.6 | 81.4 |

| economic system | 5.4 | 94.6 |

| lack of clear administrative | 16.5 | 83.5 |

| low salaries of civil officials | 8.3 | 91.7 |

| lawlessness, lack of rule of law | 54.7 | 45.3 |

| mixing in the flow state | 3.2 | 96.8 |

| Human nature, such people are everywhere | 10.5 | 89.5 |

| something else | 0.3 | 99.7 |

| Do not know/refused | 0.3 | 99.7 |

Source: Transparency International BIH, 2001

protracted adoption of the State-level budget and of a medium-term fiscal strategy. The weakened consensus on economic and fiscal policy essentials had a negative impact on reforms at the country level. A new two-year IMF Stand-By Arrangement has been agreed to support the country’s efforts to counter the effects of the worsening external environment and tackle external and domestic vulnerabilities8.

Bosnia and Herzegovina made limited progress in aligning its legislation and policies with European standards (in the areas of free movement of goods, competition, intellectual property, research and a number of justice, freedom and security-related matters), internal market areas and area of movement of persons, services and right of establishment.

Growth model of Bosnia and Herzegovina is implementation of the institutional environment and the strengthening of institutions with the aim of attracting foreign direct investment. The next section of paper analysis what are effects of corruption for inflows of foreign direct investment using the model for measuring the impact of corruption on the economic development of Bosnia and Herzegovina.

5. MODEL FOR MEASURING THE IMPACT OF CORRUPTION ON THE ECONOMIC DEVELOPMENT OF BOSNIA AND HERZEGOVINA

Empirical evidence around the world shows that corruption reduces FDI. The results of research in Bosnia and Herzegovina evaluate the same conclusion.

Selected for this study is a linear one-dimensional model presented by equation:

Table 2. Estimation of model parameters for the dependent variable (FDI) and the independent variable (extent of corruption) in the case of Bosnia and Herzegovina

| Bosnia and Herzegovina Year | FDI-Y (mil.ˆ) | CPI-∖ Corruption Perception Index | Y∙∖ (FDI∙CPI) | CPI2 |

| 2007 | 1333.17 | 3.3 | 4399.46 | 10.89 |

| 2008 | 685.84 | 3.2 | 2194.68 | 10.24 |

| 2009 | 180.46 | 3.0 | 541.38 | 9.0 |

| 2010 | 220.97 | 3.2 | 707.10 | 10.24 |

| 2011 | 290.71 | 3.2 | 930.27 | 10.24 |

| Total | 2711.15 | 15.9 | 8772.89 | 50.61 |

Source: author’s calculations

Table 4. Chadock’s scale

Source: www.efos.hr/nastavnici/jhorvat

6. FINDINGS AND DISCUSSIONS

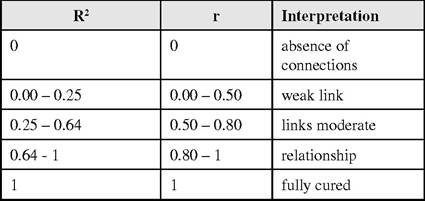

Considering capital flows as a general category, which also includes foreign direct investment among others, it can be argued that corruption affects the composition of capital flows in such a way that in turn, the probability of financial crises increases. The mechanism functions as follows: Corruption has a negative impact on FDI. In other words, it distorts the composition of capital flows by reducing the share of foreign direct investment in favor of short-term capital flows, such as bank loans. The second link is the one between this specific composition of capital flows-poor in FDI- and the increased likelihood of currency crises.

Figure 1 summarizes this argument. This latter link has been relatively well-researched, and it stands as a clear assertion that the lower the share of FDI within the total capital flows, the higher the likelihood of crises (Frankel & Rose, 1996; Radelet & Sachs, 1998; Rodrik & Velasco, 1999).

For testing the hypothesis regarding the effect of corruption on the efficiency of investment, we have estimated cross-section regression equations with efficiency of investment (EII) during the period 2007-2011 as the dependent variable and Transparency International’s 2011 Corruption Perception Index (CPI) for 10 countries as the independent variable. Annual indexes ofperceived corruption have been prepared by the organization Transparency International.

Corruption is seen as having negative effects on an economy, while FDI has been shown to be beneficial. Research combining the variables of FDI and corruption is lacking in transitional economies, partly due to the fact that it is a fairly new area, the lack of information and the diversity among the countries. Also, research on corruption tends to generalize its causes and effects among countries. Although this is helpful when looking at economic impacts, it is less so when examining ways to find solutions. Corruption can become very much a part of a country’s life and the causes and effects can be seen in its history and society. Since there are different types of corruption, there will also be different solutions.

In a 1995 study on investment and loan risk information, Ades and Di Tella found that an increase of $4,400 US in per capita income would improve a country’s ranking on a corruption index by two points out of ten. They also found that increased competition would lead to an improvement on the corruption scale. These

Figure 1. A basic sketch of the link between corruption, capital flows and financial crises Source: author’s research

studies show a link between the development of an economy and corruption and they also show that corruption has a strong economic dimension. Paolo Mauro’s 1997 study on 67 countries found that if a country could heighten the efficiency of its administration and improve its corruption score from 4 out of 10 to 6 out 10, the rate of investment would increase by 3% and the growth rate would increase by 0.5%. The study done by Shang-Jin Wei shows that decreasing Singapore’s corruption score of 10 to that of Mexico’s 3.25, would have the same economic effects of raising the tax rate by 21%. This empirical evidence shows there is a correlation between corruption and growth and between FDI and corruption.

The lowest level of corruption corresponds to an index 10 and the highest level being designated as 0.2. These indices are based on a “poll of polls” compiled by a team of researchers at Gottingen University. The questions asked to selected business people and the local population included spread and amount of corruption in public and private business (H1), likeliness to demand special and illegal payments in high and low levels of government (H2), lack of qualitative industrial products (H3), increase of net-exports (H4), decrease of government spending (H5) and increase of gross domestic production GDP (H6).

Foreign direct investment are the net inflows of investment to acquire a lasting management interest (10 percent or more of voting stock) in an enterprise operating in an economy other than that of the investor. It is the sum of equity capital, reinvestment of earnings, other long-term capital, and short-term capital as shown in the balance of payments. Table 5 shows net inflows (new investment inflows less disinvestment) in the reporting economy from foreign investors, and is divided by GDP.

Because of the linkage between inflow of foreign direct investment and level of corruption, the research was made for the same countries about corruption for this period and for 2011 (Table 6).

5. CONCLUSION

The paper will show foreign direct investment in Bosnia and Herzegovina as a country from the region that adopted the European legal entities, improved investment environment and strengthened the fight against corruption through the process of accession to the European Union. First, the linkages between efficiency of investment

Table 5. Foreign direct investment (% of GDP)

| Country Name | 2007 | 2008 | 2009 | 2010 |

| Albania | 6.2 | 7.4 | 8.0 | 9.4 |

| Bosnia and Herzegovina | 13.6 | 5.3 | 1.4 | 1.4 |

| Bulgaria | 31.4 | 19.3 | 7.0 | 4.5 |

| Croatia | 8.4 | 8.6 | 4.5 | 0,5 |

| Italy | 1.9 | -0.4 | 0.8 | 0,5 |

| Kosovo | 12.9 | 9.5 | 7.5 | 7.4 |

| Macedonia | 8.6 | 6.0 | 3.1 | 3.2 |

| Montenegro | 25.5 | 21.2 | 36.9 | 18.5 |

| Slovenia | 3.2 | 3.5 | -1.3 | 0.8 |

| Turkey | 3.4 | 2.7 | 1.4 | 1.3 |

Source: World Bank and National Banking Statistical data

Table 6. Level of corruption (CPI) for 10 mentioned countries

| Country Name | 2007 | 2008 | 2009 | 2010 | 2011 |

| Albania | 2.9 | 3.4 | 3.2 | 3.3 | 3.1 |

| Bosnia and Herzegovina | 2.9 | 3.3 | 3.2 | 3.2 | 3.2 |

| Bulgaria | 4.1 | 3.6 | 3.8 | 3.6 | 3.3 |

| Croatia | 4.1 | 4.4 | 4.1 | 4.1 | 4.0 |

| Italy | 5.2 | 4.8 | 4.3 | 3.9 | 3.9 |

| Kosovo | * | * | *9 | 2.8 | 2.9 |

| Macedonia | 3.3 | 3.6 | 3.8 | 4.1 | 3.9 |

| Montenegro | 3.3 | 3.4 | 3.9 | 3.7 | 4.0 |

| Slovenia | 6.6 | 6.7 | 6.6 | 6.4 | 5.9 |

| Turkey | 4.1 | 4.6 | 4.4 | 4.4 | 4.2 |

Source: Transparency International

and corruption is analyzed. After this corruption effects on FDI is shown. Beside others, Foreign Direct Investment is a key indicator for economic growth and development of Bosnia and Herzegovina and it reflects the value of total flows of foreign capital delivered within a certain period in the national economy. The dominant current definition of a direct investment entity, prescribed for balance-of payments compilations by the International Monetary Fund (1993), and endorsed by the OECD (1996), avoids the notion of control by the investor in favor of a much vaguer concept. “Direct investment is the category of international investment that reflects the objective of a resident entity in one economy obtaining a lasting interest in an enterprise resident in another economy. (The resident entity is the direct investor and the enterprise is the direct investment enterprise).

The lasting interest implies the existence of a long-term relationship between the direct investor and the enterprise and a significant degree of influence by the investor on the management of the enterprise” (IMF, 1993, p 86)10.

Consequences of corruption was the part which lead to research hypotheses and finally to causes of corruption in Bosnia and Herzegovina. In the case of the new EU member state (NMS), exactly Bosnia and Herzegovina, the dominance of negative over positive spill-over effects can be explained by the specificities of FDI in the period following transition.

The empirical evidence provided in the study suggests that corruption decreases some investment and reduces its positive effect on economic growth. If we consider data for Bosnia and He- zegovina about the flows of FDI for period 2007201111, and on the other side if we put Bosnia and Hezegovina CPI for the same years, and link these two variables to “wheel,” we will see that it cannot go “hand by hand.” In other words, only the countries with lower corruption can enjoy the efficient return on investment such that it raises growth. But in highly corrupt countries, the returns from investment are reduced by the corrupt agents in the economy and hence foreign direct investment fails to generate higher growth. In addition to its direct negative impact and indirect impact through reducing the returns to foreign investment, corruption has another indirect negative effect on growth through reducing private investment. These results suggest that the policies to deter corruption and to increase the efficiency of foreign direct investment could give very positive impulses to the economic growth. Based on these insights, we view our analysis as a promising step towards understanding an issue that is dominating the international development arena.

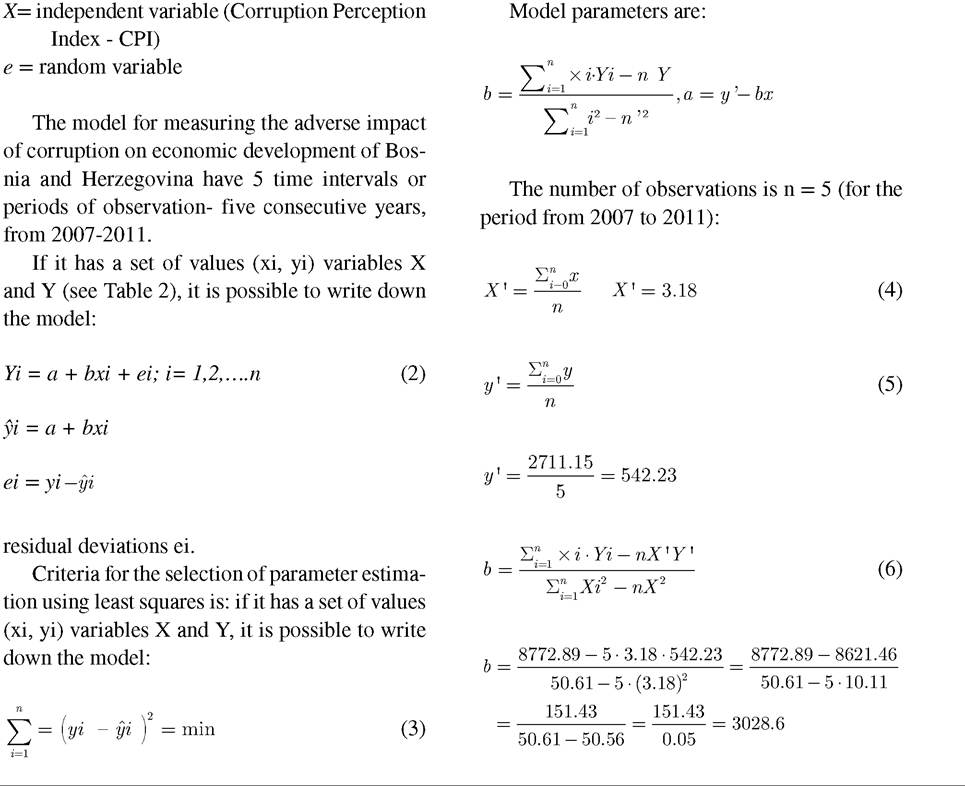

The new model for measuring the impact of corruption on the economic development of Bosnia and Herzegovina will show that corruption level can have a significant impact on FDI and this is a very strong correlation between this two variables (0.64< R2 by Dorel Dusmanescu and Andrei Jean-Vasile, pages 1-18, copyright 2013 by IGI Publishing (an imprint of IGI Global).