Chapter 45 An Investigation of Greek Firms' Compliance to IFRS Mandatory Disclosure Requirements

Apostolos Ballas

Athens University of Economics and Business, Greece

Nicos Sykianakis

Technological Education Institute of Piraeus, Greece

Christos Tzovas

Athens University of Economics and Business, Greece

Constantinos Vassilakopoulos

Athens University of Economics and Business, Greece

ABSTRACT

The paper investigates the compliance with IFRS disclosure requirements and ultimately the quality of financial statements.

Using a checklist based on the IFRS disclosure requirements, a compliance score was calculated for a sample of 58 listed, non-finance, Greek firms for the 2006 and 2008 financial statements. Disclosure compliance was measured under the “dichotomous approach” and the “partial compliance unweighted method. ” Subsequently, univariate tests and a multivariate regression model were used to investigate what firm characteristics are related with disclosure compliance. Closely-held firms exhibit higher compliance rate, while disclosure compliance is not associated with firms’ profitability, leverage and size. There is a positive association between the engagement of a Big-4 international auditing firm and the compliance rate. This study can be of interest to accounting regulators who set disclosure requirements and capital market participants by providing indication regarding Greekfirms' compliance with IFRS disclosure requirements. In addition, it examines the disclosure compliance with the important disclosure items of all IFRS rather than focusing in the disclosure items of specific IFRS. By adopting both approaches proposed in literature for measuring compliance, the authors enhance the robustness of the findings of this study, while the authors provide empirical evidence concerning the extent to which the two approaches provide significantly different results. The authors found that the two methods do not produce significantly different results.DOI: 10.4018∕978-1-4666-6268-1.ch045

.

1. INTRODUCTION

This paper investigates the extent of Greek companies’ compliance to disclosure requirements laid out in International Financial Reporting Standards (IFRS) as well as some of the factors that may explain compliance. The disclosures included in the published financial statements of a sample of 58 Greek firms have been examined. In order to enhance the robustness of the findings of this study the compliance rate has been calculated by employing two approaches proposed in the literature, i.e. the “dichotomous approach” and the “partial compliance unweigheted method.”

Most ofthe studies concerning disclosure quality concentrate on voluntary disclosure and cover the period before 2005 when the application of IFRS was not mandatory. From January 1st 2005 onwards the listed companies in all EU countries have had to prepare their financial statements in accordance with IFRS. That development changed structurally the accounting environment of most EU countries, including Greece. This study focuses on mandatory disclosure and covers the period after 2005 when the application of IFRS is mandatory. Furthermore, within this study we examine the disclosure compliance with the most important disclosure items of all IFRS, while many studies have examined the disclosure compliance with specific IFRS. As a result the total number of information items that were examined in this study is significantly higher comparing to disclosure items examined in previous studies. The Greek business environment possesses certain characteristics that provide the researcher the opportunity to investigate the factors that influence disclosure compliance within a context which is quite different from that prevailing in many developed countries. In Greece, as in many European countries (e.g. France, Italy), the ownership structure ofthe majority of the firms is characterized by a high level of concentration (Nobes & Parker, 2000), while the main providers of funds for Greek companies are the banks.

Furthermore, in Greece there is a close linkage between tax accounting and financial reporting. These factors are generally not associated with high disclosure compliance and high quality published financial statements (Nobes & Parker, 2000). Indeed, Leuz et al. (2003) show that Greek companies appear to engage in some of the most extreme earnings management practices in the world. Bhattacharya et al. (2003) provide similar evidence, since in their study Greek firms are the most engaged in earnings management among firms from 34 countries. Florou and Galarniotis (2007) found that the corporate governance transparency of Greek firms is low while the compliance of Greek firms with corporate governance disclosure requirements provided by the Greek legislation is also low (51,8%). They conclude that Greek firms are reluctant to disclose information regarding their governance practices. On the basis of this discussion we would expect that the compliance of Greek firms with the IFRS disclosure requirements would not be particularly high. This study by adopting both approaches proposed in the literature for measuring disclosure compliance provides empirical evidence concerning the extent to which the two methods provide significantly different results. These two approaches in measuring disclosure compliance are considered to provide quite different results (see, Street & Gray, 2001; Tsalavoutas et al., 2010).The findings of statistical analysis suggest that ownership structure and the type of the external auditor applied are significant factors explaining compliance. Leverage, size and profitability appear to have less explanatory power. Furthermore, we found that the two methods for measuring disclosure compliance do not produce significantly results.

The rest of this paper proceeds as follows. In Section 2 we develop the hypotheses to be tested while in section 3 the sample and the research design followed in this article are described. Section

4 reports the results of the empirical investigation undertaken for the purposes of this study.

Section5 summarizes and concludes the paper.

2. HYPOTHESIS DEVELOPMENT

This paper adopts agency theory as a conceptual framework to examine the compliance of Greek listed firms with IFRS disclosure requirements. The information asymmetry between agents and principals is the fundamental issue upon which agency theory is developed (Jensen and Meckling, 1976). Information asymmetry emerges when the principal has a limited ability to oversee agent’s actions and performance (Setyadi et al., 2011). Within this context, firms’ managers (agents), due to their ability to conceal possible performance deficiencies from firms’ owners (principals), are likely to behave opportunistically by decreasing their performance and evading responsibilities. This conflict of interest between principal and agent gives rise to agency costs. When, owners and creditors cannot observe managers actions directly, they have a motive to impose costly monitoring systems that oversee managers’ actions. The significance of agency costs is associated with certain firms’ characteristics. The characteristics of the firm that are examined in this study relate to the financial performance of the firms and certain aspects of their corporate governance structures.

2.1. Leverage and Disclosure Compliance

According to agency theory, the creditors of highly leveraged firms have strong incentives to prompt management to disclose more information (Amran et al., 2009). More leveraged firms tend to be more speculative and riskier while the debt-holders have greater power over the financial structure of such firms (Oliveira et al., 2011). On the other hand, it has been argued that creditors can obtain the information they need by sources other than annual reports (Leuz et al., 2004). Importantly, in Greece as in other European countries (e.g. France, Germany), bank credit plays a dominant role in the financing of business enterprises. Banks developed a close relationship with many companies, while in certain cases they own part of the firm’s share capital.

Thus, banks in many instances may directly obtain any relevant financial information, without having to rely upon publicly disclosed data. Consequently, the importance of public accounting information may further diminish. Within this context, the demand for high quality disclosure is not expected to be high. Nevertheless, consistently with the arguments of agency theory we test the hypothesis:H1: The rate of disclosure compliance is positively associated with the firm’s leverage

2.2. Ownership Status and Disclosure Compliance

Ownership structure has been hypothesized to be associated with the disclosure compliance of a firm (Soderstrom & Sun, 2007); for those firms in which ownership is concentrated in the hands of a relatively small number of shareholders who actively control the firm’s management, managers can communicate any important information directly to shareholders without having to use published financial statements (Klassen, 1997). As a result lower disclosure compliance is expected for closely held firms. According to Birt et al. (2006) in more concentrated ownership structures there is less need for corporate disclosures since the major shareholders can actively monitor and control firms’ management. On the other hand, B arako et al. (2006) argue that in the more diffused ownership structures small shareholders may face difficulties in monitoring firms’ management. Within this context higher level of disclosure can be expected from widely-held firms. As mentioned above the ownership structure of most Greek firms is highly concentrated, particularly in the form of family ownership. In most cases, the owners are actively involved in their companies’ administration by occupying important posts within the organizational structure of their firms (Sykianakis, 2004; Tzovas, 2006). Managers can communicate information regarding firm’s performance directly to their superior ownermanagers without having to rely upon financial statements. Under these circumstances, there are no strong incentives for firms to provide high quality financial disclosures.

The provision of information has been identified as a factor that contributes in the protection of shareholders’ interests from opportunistic, self-interested and managerial behaviour (La Porta et al., 1998). The national legal rules can be an additional mechanism that complements shareholders’ protection (Florou & Galarniotis 2007). The voting and dividend rights provided by the Greek legislation are quite significant. In particular, La Porta et al. (1998) found that Greece is one of only 11 (out of 49) countries that “impose genuinely one-share one-vote rules.” Furthermore, is one of only seven (out of 49) countries, where firms have the legal obligation to pay as dividends a certain proportion of their profits. It can be argued, therefore, that Greek legislation provides significant protection to shareholders’ interests. As a consequence, the role of accounting information as protection mechanism of shareholders’ interest may not be crucial. Within this context, the demand for more accounting information may not be particularly high. On the basis of the above analysis, the association between disclosure compliance and the level of ownership concentration it can be hypothesised to be negative.It should be pointed out that when the ownership is so concentrated that a single shareholder effectively controls the company the agency problem may shift away from the manager vs. owner problem, to minority shareholders vs. controlling shareholders problem (Setyadi et al., 2011). When large shareholders control firms they pursue policies that aim to increase their benefits at the expense of minority shareholders (Shleifer & Vishny, 1997). Jensen and Meckling (1976) argue that convergence of interest can occur between outside investors and large shareholders when outside investors believe that large shareholders aim to maximize firm value. In this case outside investors will impose fewer contractual constraints in the firm. Within this context the agency costs will be low and the larger shareholders will not have strong incentives to manipulate and/or withhold information. On the contrary they will have incentives to maintain level of disclosure consistent with the maximisation of the value of the firm. As a consequence, the association between owners’ holdings and disclosure will be positive (Oliveira et al., 2011). Given the opposing arguments that have been developed concerning the impact that ownership structure may have upon disclosure compliance we do not predict a particular sign regarding the association between the two variables and we test the hypothesis:

H2: The rate of disclosure compliance is associated with the firm’s ownership structure.

2.3. Corporate Size and Disclosure

According to Cooke (1989) the size of a firm is a variable that can explain, to a considerable extent, the quality of firm’s disclosures. Larger firms are expected to possess the resources that are necessary for the preparation of an event such as the introduction of IFRS (Jones & Higgins, 2006). Furthermore, the financial statements of larger firms are more likely to be thoroughly examined and analysed by financial analysts and shareholders. As a result, considerable pressure is exercised to larger firms to improve the quality of their disclosure (Hossain & Adams, 1995). Within this context we test the hypothesis:

H3: The rate of disclosure compliance is higher for larger firms

2.4. Profitability and Disclosure

The compliance of a firm to the disclosure requirements prescribed by particular accounting standards is affected by the profitability of the firm (Palmer, 2008). When the introduction of a new or a revised accounting standard is expected to adversely affect firms’ income, companies are more concerned about issues relating to the implementation of the new standard and the way they will communicate to their shareholders their continuing underlying profitability (Jones & Higgins, 2006). According to agency theory the managers of profitable firms will disclose financial information to the external users of accounts in order to advance their interests. They will disclose detailed information in order to continue in their positions and their compensation arrangements. On the basis of the political costs theory, it can be argued that the firms with large political visibility will have an incentive to disclose more information in order to justify the level of their profits (Inchausti, 1997). Within this context, it is expected that the more profitable firms will have higher compliance rates than the less profitable firms (Inchausti, 1997; Palmer, 2008). We test the hypothesis that:

H4: The rate of disclosure compliance is positively associated with the firm’s profitability.

2.5. Auditor Type

The level of compliance with disclosure requirements is associated with the type of external auditors appointed (Street & Gray, 2001; Glaum & Street, 2003; Ali et al., 2004; Setyadi et al., 2011). In particular, it is argued that there is a positive association between the engagement of Big-4 international auditing firms and the level of a firm’s disclosure compliance. The choice of external auditor is a mechanism that aims to minimize agency costs. The companies audited by the major auditing firms have significant agency costs and they attempt to reduce these costs by employing the major auditing firms (Setyadi et al., 2011). Tsalavoutas and Evans (2010) found that only companies with non Big-4 auditors faced significant impact on net profit and liquidity on transition to IFRS. Chalmers and Godfrey (2004) argue that, in order to maintain their reputation and to avoid reputational costs, the larger and well-known auditing firms are more likely to demand higher levels of disclosure. Furthermore, the major international auditing firms have greater knowledge about IAS (Lopes & Rodrigues, 2007). In fact, Tsalavoutas and Evans (2010) found that the Greek firms that had experienced a smooth transition to IFRS, were the firms that were audited by Big-4 international auditing firms.

H5: The disclosure compliance is predicted to be higher in companies audited by the Big-4 auditing firms.

3. RESEARCH DESIGN

3.1. Sample Selection

The financial statements of a sample of Greek listed non-finance firms for the financial years 2006 and 2008 were examined. The year 2006 was the second year of compulsory application of IFRS for Greek firms. In order to smooth the progress of adoption of IFRS by Greek firms, in the first year of IFRS application (i.e. 2005), a number of exceptions were (unofficially) granted to firms with respect to the disclosures that they should include in their financial statements. These exceptions were over and above the exceptions allowed by IFRS1 for the first time adoption of IFRS. Therefore, if the present analysis was based on the 2005 financial statements, its results may not be indicative of the actual compliance of Greek firms. From 2009 onwards IFRS were subject of continuous revisions, while a number of revisions that had been decided in earlier periods became effective gradually after 2009. Thus, we decided to restrict our analysis in the financial statements of the periods 2006 and 2008.

3.2. Data Source

The disclosures included in published financial statements of sample of 58 Greek firms have been examined. The sample does not include firms from the financial sector. The firms included in the sample of listed firms were chosen in order to be representative of the (other) main sectors of the Greek Economy. The focus of this paper is compliance with the disclosure requirements of all IFRS; this would require testing whether a firm complies with more than 1,500items, which are not necessarily applicable in all sectors. Furthermore, checking the compliance of a company with all such requirements would be open to substantial bias because the authors could not be certain whether a disclosure requirement was pertinent to the specific company. On the other hand, there is a question regarding which are the most important disclosures. For this reason, this study uses the disclosures included in the proposal (as it then was) for a Standard for Small and Medium Sized Entities. This document supposedly focuses on the most important disclosure items. The total number of information items that were examined in this study is 436, which is significantly higher comparing to disclosure items examined in previous studies. For instance, Glaum and Street (2003) used an IAS disclosure checklist containing 153 items and a US GAAP one contained 144 items. Hodgdon et al. (2008) employed a disclosure list made up from 209 disclosure items and Setyadi et al. (2011) used a 29 item index.

3.3. Measurement of the Variables

3.3.1. Dependent Variable

For each category of disclosure it has determined which elements should be disclosed. Subsequently it has been examined whether the sample firms made the appropriate disclosures in their annual report. An issue with scoring disclosures in financial statements is whether or not an undisclosed information item is applicable to a sample firm. Several measures have been proposed in literature for dealing with this problem. Cooke (1989) proposed annual reports to be thoroughly examined before they were scored in order to determine whether the undisclosed information items were indeed inapplicable to the companies. Furthermore, the applicability of some items was determined by logical reasoning (Owusu-Ansah, 2000). For instance, it is sensible to expect a firm to disclose its accounting policy for securities valuation, if it owns a portfolio of securities. Both measures were adopted in this study.

With respect to the measuring of disclosure compliance two approaches are proposed in the literature. The most common approach, known also as the “dichotomous approach,” adopts an unweigheted disclosure index (see Ali et al., 2004).The disclosure compliance of a company is depicted as the value a compliance ratio computed for each company. The compliance ratio is the ratio of what a company disclosed in its annual report to what it is obliged to disclose for each category of disclosure. For each item of disclosure there are three possibilities: the information item is disclosed in the annual reports (OK); the information item is not disclosed item in the annual reports because it is not applicable in the particular company (non applicable NA); the information item is not disclosed item in the annual reports despite the fact it is applicable in the particular company and this company should disclose it (non-mentioned, NM). Thus, disclosure ratio under the dichotomous approach has been calculated as follows:

where Cj = the total compliance score for each company and 0≤Cj≤1; T = is the total number of items disclosed () by company j; and M = the maximum number of applicable disclosure items for company j that could have been disclosed.

This approach gives equal weight to the specific items required to be disclosed by all standards. As a consequence, it gives greater weight to standards that require more items to be disclosed (Tsalavoutas et al., 2010). Although, this method has been employed in most studies examining disclosure compliance, it appears to have the serious limitation that does not treat each standard equally (Tsalavoutas et al., 2010). Given that some standards require a large number of items to be disclosed while others a few items, the standards that require more items to be disclosed are not treated equally with these standards that require few items to be disclosed (Al-Shiab, 2008).

An alternative approach proposed in the literature is the “partial compliance unweigheted method” (see Street & Gray, 2001; Al-Shiab 2008). This approach is based on the assumption that each standard is of equal importance and gives equal weight to each standard (Tsalavoutas et al., 2010). Under this approach, the compliance rate of each entity is measured by adding the degree of each standard and the diving the total by the number of standards applicable to each company. Street and Gray (2001) found different significant associations under each method between disclosure compliance and a number of independent variables. Similarly, Tsalavoutas et al. (2010) found that the two methods produce significantly different results. They believe that the simultaneous application of the two methods will provide more robust results. Within this study we adopted both measures of disclosure compliance.

Under the “partial compliance unweigheted method” the compliance with each standard is calculated separately. Then the sum of these compliance scores (X) is divided by the total number of applicable standards (R) for each sample firm

j. Thus the compliance score for each firm is calculated as follows:

where PCj is the total compliance score for each company and 0≤PCj≤1.

3.3.2. Independent Variables

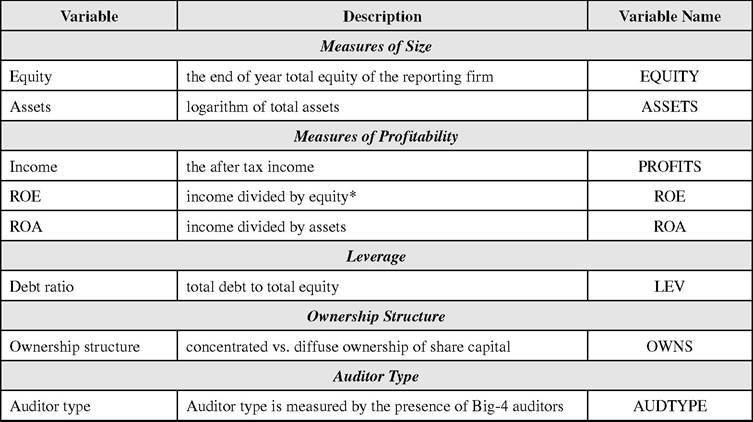

In accordance with the hypotheses developed above, the present study uses five independent variables in order to explain the disclosure compliance of the sample firms: size, leverage, profitability, ownership structure and auditor type. Two metric variables were considered as measures of size. The first one is equity (EQUITY), which is depicted by the end of year total equity of the reporting firm. The second variable is assets (ASSETS) and it is measured by the logarithm of a firm’s total assets. Profitability is depicted by three metric measures of profitability; income, Return on Equity (ROE) and Return on Assets (ROA). Income (PROFITS) is measured by net income after tax at the end of the fiscal year for each firm. ROE is the ratio of total income after tax divided by the average of equity. It should be noted that in the case where equity is negative this variable is not defined. The last measure of profitability is ROA, which comprises the ratio of income divided by the average of assets. Leverage (LEV) is measured by the debt ratio of each firm in the sample. The debt ratio is calculated as the proportion of total debt to equity.

A dummy variable has been used in order to indicate the ownership status of the sample firms. The dummy variable takes the value 1 when the firm is characterised by concentrated ownership and 0 otherwise. In order to determine the ownership structure of a firm a combination of criteria has been employed based upon the proportion of share capital owned by major shareholders and the composition of the board of directors. In particular, if three shareholders control 70% or more of firm’s share capital the firm is characterised as a closely-held firm, and three shareholders control 50% or more of firm’s share capital the firm is characterised as a closely-held firm, and one shareholder owns 20% or more than of share capital and no other shareholder owns more than 5% of share capital the firm is characterised by concentrated ownership. When none of the above criteria are met, the sample firm is characterised as a firm with diffused ownership. Finally, the remaining firms are categorised as closely held ones only if a firm meets at least one of the above criteria and one or more of the major shareholders participate in the board of directors.

A dummy variable has been used in order to indicate the type of the external auditor employed. The dummy variable takes the value 1 when the auditing firm is a Big-4 firm and 0 otherwise.

Table 1 presents the definitions of the independent variables.

3.4. Research Method

The statistical analysis has been conducted for both measures of disclosure compliance presented above on an individual year basis (i.e. year 2006 and year 2008) and for the pooled-sample as well. The univariate analysis aiming to examine the association between the compliance rate and each individual independent variable has been followed by a multivariate analysis. The multivariate analysis aims to identify the accumulated effect of the independent variables on the compliance ratio of the sample-firms. In particular, it has been examined the association between the disclosure compliance of the sample firms with the firms’ size, leverage, profitability, ownership status and the type of the external auditor employed.

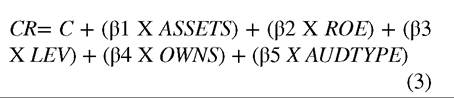

For the purposes of the multivariate analysis the following model has been estimated for each of periods 2006 and 2008 and for the pooled sample as well.

where CR = compliance rate, other variables as defined in Table 1.

Table 1. Independent variables

*It should be noted that in the case where equity is negative the variable ROE is not defined

4. RESULTS

4.1. Descriptive Statistics

Descriptive statistics for the firms in the pooled sample for years 2006 and 2008 are provided in Table 2. The average compliance rate under the “dichotomous approach” is 75%, while under the “partial compliance unweighted method” the compliance rate is 71.2%. It should be noted that the average compliance rate under the “dichotomous approach” for the year 2006 is 74.91%, while under the “partial compliance unweigheted method” the compliance rate is 70.9%. For 2008 the average compliance rate under the “dichotomous approach” is 75.55% and under “partial compliance unweighted method” the compliance rate is 71.57%. These results indicate that about a quarter of the required items are not disclosed by the firms in the sample on average.

The observed compliance rate raises some questions regarding audit quality and the enforcement of regulations in Greece especially since the financial statements of the companies in our sample were not qualified for inadequate disclosure.

Previous research has indicated that two methods for measuring disclosure compliance produce significantly different results (see Tsalavoutas et al., 2010). In our sample, the compliance rate under the “partial compliance unweighted method” is lower comparing to the compliance rate under the “dichotomous approach.” It has been examined the association between the results provided by the two methods. The results of the Spearman’s correlation test suggest that the results provided by the two methods employed for measuring disclosure compliance are correlated. In particular, for 2006 the value of the Spearman’s correlation rho is 0.87 (significant at 5%), while for 2008 the value of the Spearman’s correlation rho t is 0.95 (significant at 5%). These results suggest that the two methods do not produce significantly different results. This finding is not in line with the findings of Tsalavoutas et al. (2010) who found that the two methods produce significantly different results.

Table 2. Descriptive statistics for pooled sample (2006-2008)

| Variables | Mean | Median | Max | Min | Std. Dev. |

| Compliance rate - Dichotomous approach(%) | 75.2 | 76.4 | 91.9 | 49.0 | 9.2 |

| Compliance rate -PC unweighted method (%) | 71.2 | 73.8 | 92.3 | 42.0 | 11.5 |

| ASSETS | 687,104.9 | 102,991.0 | 14,000,007.0 | 11,782.0 | 2,358,292.0 |

| EQUITY | 242,061.5 | 32,102.4 | 5,078,431.0 | -78,954.7 | 836,132.6 |

| PROFITS | 14,202.0 | 1.420.5 | 730,800.0 | -305,879.0 | 96,579.3 |

| ROA (%) | 1.4 | 2.1 | 30.5 | -61.5 | 9.4 |

| ROE (%) | 4.8 | 5.7 | 103.7 | -105.6 | 20.0 |

| Leverage (%) | 60.0 | 62.9 | 142.3 | 5.9 | 20.6 |

Compliance rate - Dichotomous approach (%): is measured by the total compliance score for each company divided by the total number of items disclosed.

Compliance rate - PC unweighted method (%): is measured by the sum of the compliance scores for each standard divided by the total number of applicable standards (R) for each sample firm.

Assets: is measured by the logarithm of the total assets of firm i in fiscal year t.

EQUITY: is measured by the end of year total equity of firm i in fiscal year t.

PROFITS: is measured by net income after tax at the end of the fiscal year t for firm i.

ROE: Return on equity of company i for fiscal year t. It should be noted that that in the case where equity is negative the variable ROE is not defined.

ROA: is measured by the net income of firm i divided by the average of assets for firm i at period t and period t-1.

Leverage: Debt ratio of firm i in fiscal year t.

Under both measures of disclosure compliance the disclosure compliance of the sample firms for year 2006 does not differ significantly from the disclosure compliance for year 2008 (Table 3). The lack of improvement in the disclosure compliance suggests that the experience those Greek firms might have acquired regarding the implementation of IFRS did not affect significantly their compliance with IFRS disclosure requirements.

4.2. Univariate Analysis

In Table 4 the results of the univariate analysis concerning the association between the disclosure compliance and the independent variables for each individual year and for the pooled-sample are presented.

4.2.1. Corporate Size and Disclosure

As it can be seen in Table 4, for 2006 firms’ size as measured by the log of total assets is associated with disclosure compliance under both approaches used in order to measure the dependent variable. When size is measured by total equity the association is significant only under the “dichotomous approach.” For year 2008 there is a positive but not significant association between both measures of compliance and both measures of size. For the pooled-sample the association between the variables of interest does not appear to be significant. Overall, these findings provide weak evidence in favour of hypothesis 3 that the rate of compliance is higher for bigger firms. These findings are not in line with the findings of previous research that found a significant association between the two variables (see, Inchausti, 1997; Oliveira et al., 2011; Setyadi, 2011). Within the context of Greece, Florou and Galarniotis (2007) found that corporate governance quality increases with firms’ size. On the other hand, they did not find any systematic pattern regarding the aggregate level of non-disclosure by firm size and found positive relationship between size and disclosure compliance.

4.2.2. Profitability and Disclosure

The rank correlation coefficients between the three measures of profitability used in this study and the compliance rate measured under the “dichotomous approach,” presented in Table 4, are positive but not significant at the 5% level. This holds both for 2006 and 2008 and for the pooled- sample. Similar are the results when disclosure compliance is measured under “partial compliance unweighted method.” These findings provide no evidence in favour of hypothesis 4 that the level of compliance is associated with profitability. Previous research provides mixed evidence regarding the association of the two variables. Wallace and Naser (1995) found that the profitability of firm affects its compliance to disclosure requirements. On the other hand, Palmer (2008) found limited support for the hypothesis that more profitable firms disclose more information. Inchausti (1997), Dunmontier and Raffourmier (1998) and Street and Bryant (2000) do not provide evidence to support the argument that the rate of firm’s compliance is associated with its profitability.

Table 3. Compliance rate by year

| Compliance Rate % 2006 | Compliance Rate % 2008 | Test of Difference (T-Test) | |

| Dichotomous approach | 74.9 | 75.5 | -0.3734 |

| Partial compliance unweighted method | 70.9 | 71.5 | -0.3167 |

Table 4. Correlation coefficient among compliance rate and independent variables

| Year 2006 | Compliance Rate | Compliance Rate |

| Dichotomous Approach | PC Unweight Method | |

| Size | ||

| ASSETS | 0.240[*] | 0.222* |

| EQUITY | 0.271* | 0.195 |

| Profitability | ||

| PROFITS | 0.186 | 0.190 |

| ROE | 0.014 | 0.017 |

| ROA | 0.058 | 0.033 |

| Leverage | ||

| LEVERAGE | -0.084 | 0.050 |

| Year 2008 | Compliance Rate | Compliance Rate |

| Dichotomous Approach | PC Unweight Method | |

| Size | ||

| ASSETS | 0.122 | 0.143 |

| EQUITY | 0.137 | 0.132 |

| Profitability | ||

| PROFITS | 0.047 | 0.013 |

| ROE | 0.105 | 0.049 |

| ROA | 0.101 | 0.060 |

| Leverage | ||

| LEVERAGE | -0.050 | -0.006 |

| Pooled Sample (2006-2008) | Compliance Rate | Compliance Rate |

| Dichotomous Approach | PC Unweight Method | |

| Size | ||

| ASSETS | 0.171 | 0.162 |

| EQUITY | 0.184 | 0.135 |

| Profitability | ||

| PROFITS | 0.111 | 0.067 |

| ROE | 0.060 | 0.016 |

| ROA | 0.080 | 0.030 |

| Leverage | ||

| LEVERAGE | -0.050 | 0.029 |

4.2.3. Leverage and Disclosure Compliance

No significant association is observed between leverage and compliance ratio when the latter is measured under the “dichotomous approach.” This holds both for years 2006 and 2008 and for the pooled-sample. When the compliance is measured using the “partial compliance unweighted method” the results are similar. This provides no evidence in favour of hypothesis 1 that the level of compliance is associated with leverage. This result is consistent with the findings of previous research that found little evidence to support the hypothesis that there is a significant association between corporate disclosures and leverage (Abraham & Cox, 2007; Amran et al., 2009; Linsley & Shrives, 2006; Mohobbot, 2005). Oliveira et al. (2011) found that firms’ leverage is important in explaining the risk related disclosure.

4.2.4. Ownership Structure and Disclosure Compliance

The concentrated ownership firms exhibit a higher compliance rate comparing to the diffused-own- ership firms. This holds under both approaches being used in order to measure disclosure compliance. Yet this association is statistically significant only for year 2008 under the “partial compliance unweighted method” (see Table 5). A further statistical analysis being conducted by using the non-parametric Pearson chi-square test indicated that no significant association exists between the disclosure compliance and the ownership status of the sample firms. It should be noted that previous research has indicated that the widely-held firms comply better with the disclosure requirements of IFRS (Klassen, 1997; Birt et al., 2006; Soderstrom & Sun, 2007). On the other hand, Mohobbot (2005), Oliveira et al. (2011) and Setyadi(2011) found no relation between firms’ ownership structure and level of disclosure, while Abraham and Cox (2007) provide mixed evidence regarding the association between firms’ disclosure compliance and their ownership structure. Kajuter (2006) and Lajili (2007) found negative association between owners’ holdings and disclosure.

4.2.5. Auditor Type and Disclosure Compliance

The firms that employ one of the Big-4 international auditing firms exhibit a higher compliance rate comparing to the firms that appoint other auditing firms. This association is statistically significant for 2006 under both approaches being used in order to measure disclosure compliance (see Table 6). The application of the non-parametric Pearson chi-square test provided similar results. In particular, under the dichotomous approach the value of the Pearson chi-square test for the year

Table 5. Ownership structure and disclosure compliance

| Dichotomous Approach | |||

| Concentrated Ownership | Diffuse Ownership | Test of Difference (p-Values) | |

| 2006 | 0.756 (obs=42) | 0.730 (obs=16) | 0.349 |

| 2008 | 0.767 (obs=43) | 0.721 (obs=15) | 0.107 |

| Partial Compliance Unweighted Method | |||

| Concentrated Ownership | Diffuse Ownership | Test of Difference (p-Values) | |

| 2006 | 0.717 (obs=42) | 0.687 (obs=16) | 0.285 |

| 2008 | 0.736 (obs= 43) | 0.656 (obs=15) | 0.043 [†] |

2006 was 10.70 (significant at the 1% level) while for the same year under the “partial compliance unweighted method” the value of the Pearson chisquare test was 6.74 (significant at the 1% level). These results provide evidence in support of the hypothesis 5. These findings are in line with the findings of previous research. Inchausti (1997), Glaum and Street (2003) and Oliveira (2011) found positive relationship between disclosure and auditor type. On the other hand, Setyadi et al.(2011) found no relation between firms’ auditor type and level of disclosure.

4.3. Multivariate Analysis

Multiple regression analysis was used for multivariate testing of the hypotheses; the dependent variable, compliance rate, was regressed against the independent variables of Size, Profitability, Leverage and dummy variables for ownership status and auditor type. Assets were chosen as a proxy for size in order to be consistent with previous studies, while profitability is measured by reference to ROE.

Given the small size of the sample, the skewed distribution of the explanatory variables and therefore the possible presence of outliers that would make the analysis unreliable, a nonparametric estimation technique was used, namely quantile regression (Koenker & Hallock, 2001). This technique differs from traditional OLS because instead of minimizing the sum of squared residuals, the objective function is to minimize the mean absolute deviation (MAD). Regression results when the dependant variable is measured under the “dichotomous approach” are presented in Table 7. Panels A and B report estimated coefficients and standard errors for the 2006 and 2008 samples correspondingly. The estimated coefficients and standard errors for the pooled-sample are presented in Panel C.

Regression results when the dependent variable is measured under the “partial compliance unweighted method” are presented in Table 8. Panels A and B report estimated coefficients and standard errors for the 2006 and 2008 samples correspondingly. The estimated coefficients and standard errors for the pooled-sample are presented in Panel C.

In line with the findings of the univariate analysis the profitability and the leverage of sample firms do not appear to influence their disclosure compliance. Similarly, size is not associated with the disclosure compliance, although the univariate analysis has indicated that for 2006 the larger are more likely to comply with the IFRS disclosure requirements. The ownership status and the type of the external auditor appointed of the sample firms are factors are more likely to explain their compliance with the disclosure requirements provided by IFRS. In particular it appears that concentratedownership firms achieve higher compliance rates

Table 6. Auditor type and disclosure compliance

| Dichotomous Approach | |||

| Big-4 Auditing Firms | Other Auditing Firms | Test of Difference (p-Values) | |

| 2006 | 0.810 (obs=17) | 0.723 (obs=41) | 0.000 * |

| 2008 | 0.783 (obs=16) | 0.744 (obs=16) | 0.169 |

| Partial Compliance Unweighted Method | |||

| Big-4 Auditing Firms | Other Auditing Firms | Test of Difference (p-Values) | |

| 2006 | 0.772 (obs=17) | 0.682 (obs=41) | 0.000 * |

| 2008 | 0.750 (obs= 16) | 0.702 (obs=42) | 0.221 |

* Significant at 5% level

Table 7. Regression of size, profitability, leverage, ownership status and auditor type on disclosure compliance (dichotomous approach)

| CR= C + (β1 Χ ASSETS) + (β2 Χ ROE) + (β3 X LEV) + (β4 Χ OWNS) + (β5 Χ AUDTYPE) | |||

| Variables | 2006 | 2008 | Pooled Sample |

| Constant | 0.730* | 0.678* | 0.657* |

| (0.162) | (0.173) | (0.122) | |

| Assets | -0.003 | 0.004 | 0.004 |

| (0.015) | (0.016) | (0.011) | |

| ROE | 0.006 | 0.006 | 0.041 |

| (0.093) | (0.105) | (0.067) | |

| Leverage | 0.009 | -0.105 | -0.060 |

| (0.096) | (0.114) | (0.073) | |

| Ownership | 0.032 | 0.118* | 0.083* |

| (0.038) | (0.044) | (0.026) | |

| Auditor | 0.111* | 0.051 | 0.061 |

| Type | (0.049) | (0.052) | (0.036) |

| Pseudo R2 | 0.13 | 0.16 | 0.11 |

* Significant at 5% level. Standard errors in parentheses

Compliance rate - Dichotomous approach (%): is measured by the total compliance score for each company divided by the total number of items disclosed.

Assets: is measured by the logarithm of the total assets of firm i in fiscal year t.

ROE: Return on equity of company i for fiscal year t. It should be noted that that in the case where equity is negative the variable ROE is not defined.

Leverage: Debt ratio of firm i in fiscal year t.

Ownership: equal to 1 for concentrated ownership and 0 otherwise.

Auditor type: equal to 1 when the auditor of the firm is a Big-4 audit company and 0 otherwise.

compared to widely-held firms. This association is statistically significant for year 2008 and for the pooled-sample under both measures of disclosure compliance. The univariate analysis has found a significant association for year 2008 only under the “partial compliance unweighted method.” These findings support Hypothesis 2 that firms’ disclosure compliance can be associated with the ownership structure. Yet the observed relationship does not support the widely accepted contention that the widely-held firms comply better with the accounting standards’ disclosure requirements. In fact, it appears that closely held firms are more

Table 8. Regression of size, profitability, leverage, ownership status and auditor type on disclosure compliance (Partial compliance unweighted method)

| CR= C + (β1 Χ ASSETS) + (β2 Χ ROE) + (β3 X LEV) + (β4 Χ OWNS) + (β5 Χ AUDTYPE) | |||

| Variables | 2006 | 2008 | Pooled Sample |

| Constant | 0.671* | 0.462* | 0.474* |

| (0.158) | (0.263) | (0.130) | |

| Assets | -0.004 | 0.010 | 0.013 |

| (0.014) | (0.024) | (0.011) | |

| ROE | 0.044 | -0.010 | 0.091 |

| (0.090) | (0.160) | (0.072) | |

| Leverage | 0.039 | -0.035 | -0.005 |

| (0.093) | (0.173) | (0.077) | |

| Ownership | 0.039 | 0.201* | 0.0831* |

| (0.037) | (0.067) | (0.031) | |

| Auditor | 0.116* | 0.072 | 0.054 |

| Type | (0.047) | (0.078) | (0.039) |

| Pseudo R2 | 0.15 | 0.17 | 0.11 |

* Significant at 5% level. Standard errors in parentheses

Compliance rate -PC unweighted method (%): is measured by the sum of the compliance scores for each standard divided by the total number of applicable standards (R) for each sample firm.

Assets: is measured by the logarithm of the total assets of firm i in fiscal year t.

ROE: Return on equity of company i for fiscal year t. It should be noted that that in the case where equity is negative the variable ROE is not defined.

Leverage: Debt ratio of firm i in fiscal year t.

Ownership: equal to 1 for concentrated ownership and 0 otherwise.

Auditor type: equal to 1 when the auditor of the firm is a Big-4 audit company and 0 otherwise

likely to comply with disclosure requirements. The observed relationship can be explained within the context of agency theory. The major shareholders aim to maximize firm’s value and as a consequence the agency costs are low. As mentioned earlier when major shareholders aim to maximize firm’s value a positive association is expected between owners’ holdings and disclosure.

With respect with the type of external auditor appointed it appears that the firms that employ one of the Big-4 international auditing firms exhibit a higher compliance rate comparing to the firms that appoint other auditing firms. This association is statistically significant for the year 2006 under both measures of disclosure compliance. These results are similar with those provided by the univariate analysis. These findings support Hypothesis 5 that the disclosure compliance is higher in companies audited by the Big-4 auditing firms. Results regarding the auditor type are consistent with the findings of previous research. The fact that the association is significant for year 2006 suggests that the local auditing firms, and in general smaller auditing firms, might not have possessed in that year the superior knowledge and experience that the Big-4 international auditing firms possessed with respect to the application of IFRS and the auditing of financial statements prepared according to IFRS. As a consequence the disclosure compliance of the firms audited by Big-4 international auditing firms was higher comparing to the disclosure compliance of firms being audited by local auditing firms. However, by 2008 that gap between Big-4 international auditing firms and local auditing firms regarding the expertise upon the application of IFRS might have narrowed.

It should be pointed out that the two methods employed for measuring disclosure compliance do not produce significantly different results. In fact, we found similar association between the dependent variable (disclosure compliance) and the independent variables under each method employed for measuring dependent variable. This holds for both the univariate and the multivariate analysis. As mentioned previous research has indicated that the two methods can produce quite different results.

5. CONCLUSION

The objective of this article is to examine the compliance of Greek firms to the IFRS disclosure requirements. We examine the relation between disclosure compliance and certain firms’ characteristics for a sample of 58 Greek listed firms for 2006 and 2008. In order to examine the association between disclosure compliance and a range of firm’s characteristics, a compliance rate has been estimated under two approaches proposed in the literature, which are the “dichotomous approach” and the “partial compliance unweighted method.” Prior research has indicated that these two methods can produce significantly different results.

It appears that for the sample firms the ownership structure and the type of external auditor appointed are the most important factors in explaining disclosure compliance. Contrary to the findings of previous research, it seems that the closely-held firms exhibit higher compliance rate comparing to the widely held ones. Results regarding the auditor type are consistent with the findings of previous research, which indicated that firms that are being audited by one of the Big-4 international auditing firms comply better with the disclosure requirements of IFRS. On the other hand, the leverage of a firm its profitability and its size do not appear to be statistically significant variables in explaining disclosure compliance. It should be noted that the results were similar under both methods employed in this study for measuring disclosure compliance. This finding is not in line with the findings of previous research that found that the two methods provide significantly different results.

The findings of this study add to our knowledge regarding the factors that explain the disclosure compliance of Greek firms. Given the similarities of Greek business environment with the environment prevailing in other European countries the findings of this study can be useful to researchers that examine disclosure compliance in other European countries. Moreover, while prior research has examined the association between disclosure compliance and firms’ characteristics, mainly in a voluntary setting, we add to our understanding of the firm characteristics associated with disclosure compliance in mandatory environment. In addition this study examines the disclosure compliance with the important disclosure items of all IFRS rather than focusing in the disclosure items of specific IFRS.

This study contributes to the knowledge base that accounting regulators can use to determine the extent to which Greek firms comply with the disclosure requirements of IFRS and will assist in future directions in developing mechanisms that will monitor the implementation of IFRS.

Additional research could extent the time period under investigation by examining the period after 2009. The deep recession that plagues recently Greek economy since 2009 has eroded Greek firms’ profitability and their equity. A further research may be required in order to investigate Greek firms’ disclosure compliance under the prevailing adverse environment. Incorporating more explanatory variables and expanding the size of the sample can enrich this analysis.

REFERENCES

Abraham, S., & Cox, P. (2007). Analysing the determinants of narrative risk information in UK FTSE 100 annual reports. The British Accounting Review, 39, 227-248. doi:10.1016/j. bar.2007.06.002

Al-Shiab, M. (2008). The effectiveness of international financial reporting standards adoption on cost of equity capital: a vector error correction model. International Journal of Business, 13, 271-298.

Ali, J. M., Ahmed, K., & Herny, D. (2004). Disclosure compliance with national accounting standards by listed companies in South Asia. Accounting and Business Review, 34, 183-199. doi:10.1080/00014788.2004.9729963

Amran, A., Bin, A. M. R., & Hassan, B. C. H. M. (2009). Risk reporting: An exploratory study on risk management disclosure in Malaysian annual reports. Managerial Auditing Journal, 24, 39-57. doi:10.1108/02686900910919893

Barako, D. G., Hancock, P., & Izan, H. Y. (2006). Factors influencing voluntary corporate disclosure by Kenyan companies. Corporate Governance: An International Review, 14, 107-125. doi:10.1111/ j.1467-8683.2006.00491.x

Bhattacharya, U., Daouk, H., & Welker, M. (2003). The world price of earnings opacity. Accounting Review, 78, 641-678. doi:10.2308/ accr.2003.78.3.641

Birt, J. L., Bilson, C. M., Smith, T., & Whaley, R. E. (2006). Ownership, competition, and financial disclosure. Australian Journal of Management, 31, 235-263. doi:10.1177/031289620603100204

Chalmers, K., & Godfrey, J. (2004). Reputation costs: The impetus for voluntary derivative financial instrument reporting. Accounting, Organizations and Society, 29, 95-125. doi:10.1016/ S0361-3682(02)00034-X

Cooke, T. E. (1989). Voluntary corporate disclosure by Swedish companies. Journal of International Financial Management and Accounting, 1, 171-195. doi:10.1111/j.1467-646X.1989. tb00009.x

Dunmontier, P., & Raffourmier, B. (1998). Why firm comply voluntarily with IAS: An empirical analysis with Swiss data. Journal of International Financial Management and Accounting, 9, 216-245. doi:10.1111/1467-646X.00038

Florou, A., & Galarniotis, A. (2007). Benchmarking Greek corporate governance against different standards. Corporate Governance: An InternationalReview, 15, 979-998. doi:10.1111/j.1467- 8683.2007.00614.x

Glaum, M., & Street, D. (2003). Compliance with the disclosure requirements of Germany’s new market: IAS versus US GAAP. Journal of International Financial Management and Accounting, 14, 64-100. doi:10.1111/1467-646X.00090

Hodgdon, C., Tondkar, R., Harless, D., & Adhi- kari, A. (2008). Compliance with IFRS disclosure requirements and individual analysts’ forecast errors. Journal of International Accounting, Auditing & Taxation, 17, 1-13. doi:10.1016/j. intaccaudtax.2008.01.002

Hossain, M., & Adams, M. (1995). Voluntary financial disclosure by Australian listed companies. Australian Accounting Review, 5, 45-55. doi:10.1111/j.1835-2561.1995.tb00381.x

Inchausti, B. G. (1997). The influence of company characteristics and accounting regulation on information disclosed by Spanish firms. European Accounting Review, 6, 45-68. doi:10.1080/096381897336863

Jensen, M. C., & Meckling, W. H. (1976). Theory of the firm: managerial behaviour agency costs and ownership structure. Journal of Financial Economics, 3, 305-360. doi:10.1016/0304- 405X(76)90026-X

Jones, S., & Higgins, A. D. (2006). Australia’s switch to international financial reporting standards: a perspective from account preparers. Accounting and Finance, 46, 629-652. doi:10.1111/ j.1467-629X.2006.00186.x

Kajuter, P. (2006). Risk disclosures of listed firms in Germany: A longitudinal study. In Proceedings of the 10th Financial Reporting & Business Communication Conference, Cardiff Business School “Unpublished results.”

Klassen, K. J. (1997). The impact of inside ownership concentration on the trade-off between financial and tax reporting. Accounting Review, 72, 455-474.

Koenker, R., & Hallock, K. (2001). Quantile regression. The Journal of Economic Perspectives, 15, 143-156. doi:10.1257/jep.15.4.143

La Porta, R., Lopez-de-Silanes, F., Shleifer, A., & Vishny, W. R. (1998). Law and finance. The Journal of Political Economy, 106, 1113-1155. doi:10.1086/250042

Lajili, K. (2007). Corporate governance and risk disclosure. Working Paper No. 2007-24, University of Ottawa, Tefler School of Management, Ottawa, ON.

Leuz, C., Nanda, D., & Wysocki, P. (2003). Earnings management and investor protection: An international comparison. Journal of Financial Economics, 69, 505-527. doi:10.1016/S0304- 405X(03)00121-1

Leuz, C., Pfaff, D., & Hopwood, A. (2004). The economics and politics of accounting international perspectives on research trends, policy and practice. Oxford University Press. doi:10.1093/0199260621.001.0001

Linsley, P. M., & Shrives, P. J. (2006). Risk reporting : A study of risk disclosures in the annual reports of UK companies. The British Accounting Review, 38, 387-404. doi:10.1016/j.bar.2006.05.002

Lopes, P., & Rodrigues, L. L. (2007). Accounting for financial instruments: An analysis of the determinants of the disclosure in the Portuguese stock exchange. The International Journal of Accounting, 42, 25-26. doi:10.1016/j.intacc.2006.12.002

Mohobbot, A. (2005). Corporate risk reporting practices in annual reports of Japanese companies. Japanese Journal of Accounting, 16, 113-133.

Nobes, C., & Parker, R. (2000). Comparative international accounting (6th ed.). Financial Times-Prentice Hall.

Oliveira, J., Rodrigues, L. L., & Russell, C. (2011). Risk-related disclosures by non-finance companies: Portuguese practices and disclosure characteristics. Managerial Auditing Journal, 26, 817-839. doi:10.1108/02686901111171466 Owusu-Ansah, S. (2000). Noncompliance with corporate annual report disclosure requirements in Zimbabwe. Research in Accounting in Emerging Economies, 4, 289-305.

Palmer, P. (2008). Disclosure of the impacts of abandoning Australian equivalents of international financial reporting standards. Accounting and Finance, 48, 847-870.

Setyadi, A., Rusmin, R., Tower, G., & Brown, A. (2011). Measurement vs. disclosure of accounting compliance in Indonesia. International Journal of Accounting. Auditing and Performance Evaluation, 7, 94-119. doi: 10.1504/ IJAAPE.2011.037727

Shleifer, A., & Vishny, R. (1997). A survey of corporate governance. The Journal of Finance, 52, 737-783. doi:10.1111/j.1540-6261.1997. tb04820.x

Soderstrom, N. S., & Sun, K. J. (2007). IFRS adoption and accounting quality: A review. European Accounting Review, 16, 675-702. doi:10.1080/09638180701706732

Street, D. L., & Bryant, S. M. (2000). Disclosure level and compliance with IASs: A comparison of companies with and without U.S. listings and filings. The International Journal of Accounting, 35, 305-329. doi:10.1016/S0020-7063(00)00060-1 Street, D. L., & Gray, S. J. (2001). Observance of international accounting standards: Factors explaining noncompliance. ACCA Research Report No. 74. The Association of Chartered Certified Accountants.

Sykianakis, N. (2004). Factors affecting Greek FDI in the Balkans: The case of ice - cream industry. Archives of Economic History, XV, 85-107.

Tsalavoutas, I., & Evans, L. (2010). Transition to IFRS in Greece: Financial statement effects and auditor size. Managerial Auditing Journal, 25, 814-842. doi:10.1108/02686901011069560

Tsalavoutas, I., Evans, L., & Smith, M. (2010). Comparison of two methods for measuring compliance with IFRS mandatory disclosure requirements. Journal of Applied Accounting Research, 11, 213-228. doi:10.1108/09675421011088143

Tzovas, C. (2006). Factors influencing firms’ accounting policy decisions when tax accounting and financial accounting coincide. Managerial Auditing Journal, 21, 372-386. doi:10.1108/02686900610661397

Wallace, R. S. O., & Naser, K. (1995). Firmspecific determinants of the comprehensiveness of mandatory disclosure in the corporate annual reports of firms listed on the stock exchange of Hong Kong. Journal of Accounting and Public Policy, 14, 311-368. doi:10.1016/0278-4254(95)00042-9

This work was previously published in International Journal of Corporate Finance and Accounting (IJCFA), 1(1); edited by Constantine Cantzos and Constantin Zopounidis, pages 22-39, copyright 2014 by IGI Publishing (an imprint of IGI Global).

850