Chapter 44 The Behavior Intention of Tunisian Banks’ Customers on using Internet Banking

Lanouar Charfeddine

College of Business Administration, Najran University, Saudi Arabia

Wadie Nasri

The Higher Institute of Management of Gabes, University of Gabes, Tunisia

ABSTRACT

This paper examines empirically the factors affecting the adoption of internet banking in Tunisia using the Theory of Acceptance Model (TAM) and the Theory of Planned Behavior (TPB).

Security and privacy construct were selected as additional factors because of their potent influence on the use of internet banking system. For this purpose, a Structural Equation Modelling (SEM) is employed to examine the inter-correlations among the seven proposed constructs. A survey involving a total of 284 respondents is conducted and confirmatory factor analysis used to determine the measurement efficacies. This study confirms the appropriateness of TAM, TPB, and the security and privacy construct in predicting intention to use internet banking in a Tunisian banking environment. This research reveals that TAM and TPB could be used to provide a solid theoretical foundation of internet banking in Tunisian acceptance case. The study contributes to the literature of internet banking in Tunisia.1. INTRODUCTION

The Internet has a profound influence on the banking industry. The adoption of internet by Banks can offer a new market such as internet banking services (henceforth IB). These new channels, the internet banking services, are considered now as a new important channel in addition to the traditional ones. The automated teller machine (ATM),

DOI: 10.4018∕978-1-4666-6268-1.ch044

Phone-banking, Telebanking, PC-banking among others are the most important IB services proposed by contemporary Banks (Daniel, 1999; Chang, 2003; “Online banking goes mainstream,” 2003).

The adoption of technology has led to greater productivity, profitability, and efficiency, faster service and customer satisfaction, convenience and flexibility, 24x7 operations, and space and cost savings.

Banks’ decision makers have recognized the importance of the adoption of IB on reduction costs and banks performance and have tried to develop strategies in order to grow consumer internet banking demand. Thus, understanding factors affecting the adoption of internet banking in Tunisia seems an important task for Banks’ decision makers. This helps Banks to adopt a better marketing strategies to increase the use of IB in the Tunisia country..

This paper investigates the behavior intention of Tunisian banks’ customers to use the IB. We use the Theory of Acceptance Model (TAM) and the Theory of Planned Behavior (TPB)

in order to investigate the internet banking acceptance system. Seven constructs was used to identify factors that influence intention to adopt Internet banking in Tunisia: perceived use, perceived ease of use, subjective norm, perceived behavior control, security and privacy, and attitude. Security and privacy were selected as additional factor to the TAM and TPB constructs because of their important influence on the use internet banking system. To do that, we collect data from bank customers in Tunisia. Two hundred eighty four usable responses are considered and Equation Structural Model (SEM) is used to fit data to the basic proposed model.

The remainder of the paper is set out in four sections. First, we provide a literature review of earlier studies of factors influencing consumers’ use of IB and set the proposed hypothesis for this work. Then, we report the empirical methodology that was employed. Afterwards, we provide empirical findings and discuss results according to the conceptual framework of the TAM of internet banking. Finally, we conclude and suggest future research directions.

2. LITERATURE REVIEW AND HYPOTHESIS DEVELOPMENT

2.1. The Theory of Acceptance Model (TAM)

The majority of empirical works that have investigated the intention to use IB have been conducted using the Theory of Acceptance Model (TAM) (Davis, 1992; Hsu, 2004; Hsu et al., 2006).

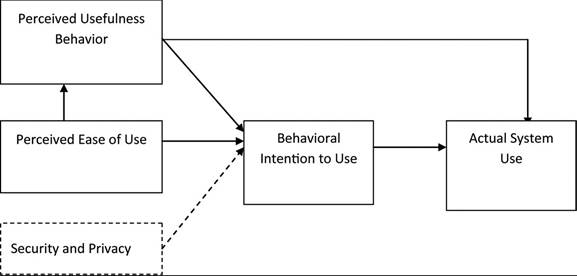

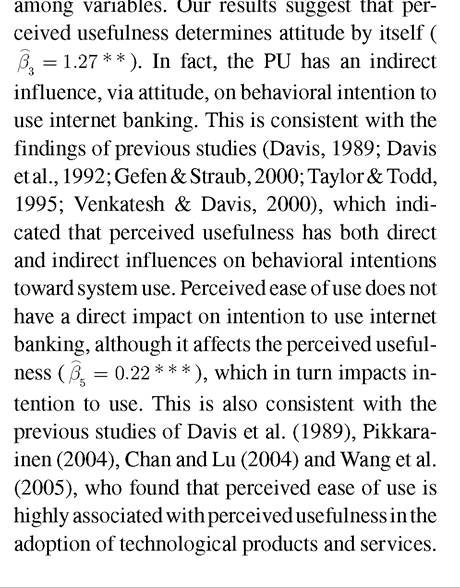

The TAM has been developed originally by Davis (1989). A graphic representation of the TAM is given in Figure 1. Following this theory, two theoretical constructs, Perceived Usefulness (PU) and Perceived Ease Of Use (PEOU), are considered as fundamental determinants of computer system use in organization. The first construct, the PU, reflects a person’s belief in the use of technology. The second construct, The PEOU, reflects the person’s belief of facility of use of the technology. These two factors are the most commonly used in the empirical literature (Davis, 1989; Venkatesh & Davis, 2000; Fagan et al., 2008; Hsu et al., 2006; Huang, 2008; Norazah & Norbayah, 2009; Norazah et al., 2008). Lederer et al. (2000), Moon and Kim (2001), and Wadie and Charfeddine (2011) among others have tested the TAM and have showed that the two constructs, PU and PEOU, influence positively the attitude and the attention to use Online Banking. Moreover, perceived of usefulness is supposed to be influenced by the perceived of ease of use.Figure 1. The TAM following Davis (1989) and Venkatesh et al. (2003) in solid line, and security and Privacy construct; Salisbury et al. (2001) in dash line.

In order to investigate the TAM, we emit the following 5 hypotheses,

H1: Perceived usefulness positively influences the intention to use IB.

H2: Attitude positively influence positively influences the intention to use IB.

H3: Perceived usefulness positively influences attitudes towards the use of IB.

H4: Perceived ease of use positively influences attitudes towards the use of IB.

H5: Perceived ease of use positively influences the perceived usefulness of the use of IB.

In addition, a new construct is introduced to the TAM. Following Salisbury et al. (2001), Miyazaki and Fernandez (2001), and Nissenbaum (2004), security and privacy is considered as an important factor that influence the use of IB, see for instance Godwin (2001) and Aladwani (2001).

The importance of security and privacy concerns in online banking environment has been broadly discussed and reported in many studies. Godwin (2001) reported that privacy and security concerns were found to be a major barrier to Internet shopping. This concern has been extended to the Internet banking environment. Security has been widely recognized as one of the main obstacles to the adoption of electronic banking (Aladwani, 2001), and privacy issues have proven important barriers to the use of online services (Westin & Maurici, 1998). White and Nteli (2004) reports that the level of increase of internet banking usage for banking purposes has not changed in the UK because of the continuing consumer fear about security. In a study about the adoption of internet banking (Sathye, 1999) reports that privacy and security were found to be significant obstacles to the adoption of online banking in Australia. Therefore, the following new hypothesis will be introduced to the TAM.

H6: Security and privacy positively influences the perceived usefulness of the use of IB.

2.2. The Theory of Planned Behavior (TPB)

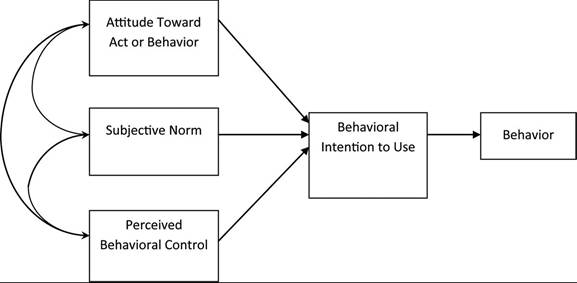

The Theory of Planned Behavior (TPB) was proposed by Ajzen (1985, 1991) as an extension of the theory of reasoned action (Fishbein & Ajzen, 1975). Figure 2 reports a graphic representation of the TPB. Following this theory, individuals do not have complete control over their behaviour (Ajzen, 1991). The TPB suggests that individual behaviour is determined by behavioural intentions. Theses laters are considered as a function of three constructs: the individual attitude toward the behavior, the subjective norms surrounding the performance of the behavior, and Perceived behavioral control. This later construct indicates that a person’s motivation is influenced by how difficult the behaviors are perceived to be, as well as the perception of how successfully the individual can, or cannot, performs the activity. Perceived behavioral control can influence behavior directly or indirectly through behavioral intentions.

To investigate the TPB, we emit the following two hypotheses:

H7: Subjective norm positively influences the intention to use online banking.

H8: Perceived behavior control positively influences the intention to use online banking.

Figure 2. TPB (Ajzen, 1985, 1991)

2.3. Research Model and Hypothesis

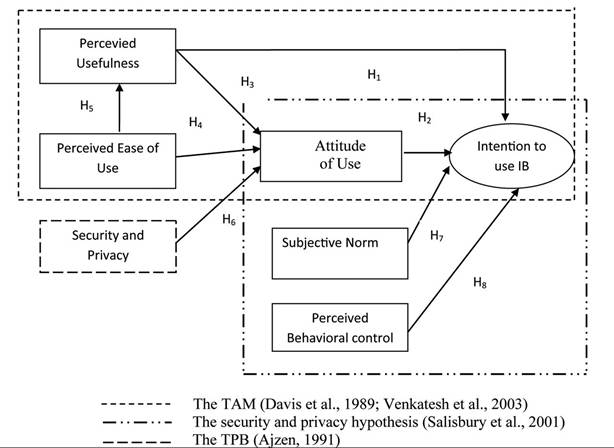

We use the two theories described in the previous section in order to develop our main research model and proposed hypothesis. By combining the TAM and the TPB in addition to the security and privacy construct we propose our main research model as described in Figure 3. The proposed model includes five independent variables, perceived of usefulness, perceived ease of use, security and privacy, subjective norm, and perceived behavioral

control, one intervening variable, the attitude of use, and the intention to use as the dependent variable. Our main object in this paper is to test the strength of the eight hypothesized relationships embedded in the theoretical model. Precisely, we investigate the robustness of the proposed model in predicting customers’ intention to adopt Internet banking in Tunisia. The eight hypotheses that we want to test in the empirical investigation are reported in Figure 3.

Figure 3. Proposed research model

In order to investigate the proposed research model, we follow a two step procedure as suggested by Anderson and Gerbing (1988) and Koufteros (1999). First, we estimate the measurement model in order to assess convergence and discriminant validity. Then, we examined the structural model in order to assess if the parameter estimates are expected to exhibit the correct sign and size, and to be consistent with underlying theory.

3. METHODOLOGY

3.1. Data

3.1.1. Measures

Questionnaire items were adapted from prior studies, which are described as follows.

Perceived usefulness (Cheng et al., 2006), perceived ease of use (Cheng et al., 2006), attitude (Cheng et al., 2006), intention (Cheng et al., 2006), subjective norm (Wu & Chen, 2005), perceived behavior control (Wu & Chen, 2005), and security and privacy (Pikkaraienen et al., 2004). In the questionnaire, the respondents were required to rate their level of agreement with a Five-point Likert scales with end points of “strongly disagree” and “strongly agree” in order to examine participant’s responses to these statements. The demographics characteristics were measured in terms of gender, age, education, occupation, and experience using online banking.3.1.2. Sample Profile

Data collection took place in April 2011. The questionnaire was administered by meeting the respondents on a one-to-one. The respondents engaged in this study, were if they used the internet and had a bank account. The questionnaires were distributed to 284 respondents randomly selected. Sample demographic are depicted in Table 1. Participants in the study were composed of 54.22% male and 45.78% female. Majority of the respondents were between 18 and 30 years old, which was 42.25 % of the total respondents. Majority of the respondents were college or university graduates (87.32%). 89.34% of the respondents posses personal computers whereas only 9.7% on them don’t. Moreover, 90.1 % have internet access.

3.2. Exploratory Factor Analysis

In order to investigate the uni-dimensionality of constructs, an exploratory factorial analysis (EFA) was conducted on the collected data. The principal components extraction method was adopted and the results were submitted to the Varimax rotation method. In the first step of the analysis, one item that didn’t have well defined factorial loads in their respective construct (Hair et al., 1998).

Table 1. Demographic statistics

| Means | Value | Frequency | Percentage (%) |

| Gender | Male | 154 | 54.22 |

| Female | 130 | 45.78 | |

| Age | 18 to 30 | 120 | 42.25 |

| 31 to 40 | 94 | 33.09 | |

| 41 to 50 | 66 | 24.26 | |

| Education Level | Primary | 8 | 2.82 |

| Secondary | 28 | 9.86 | |

| College/ University | 248 | 87.32 | |

| Possession computer | Yes | 254 | 89.34 |

| No | 30 | 10.66 | |

| Occupation | Executives | 154 | 54.22 |

| Middle-staff employees | 36 | 12.67 | |

| Blue-collar workers | 10 | 3.52 | |

| Independents | 14 | 4.93 | |

| Students | 70 | 24.64 | |

| Internet Access | Yes | 266 | 90.1 |

| No | 18 | 9.9 |

Based on these criteria, only one item (SP6) had to be dropped from the subsequent analysis. Thus from the 26 initial items, 25 are retained for the analysis1.

The results of the Cronbach’s alpha is reported at column 6 of Table 2. All obtained values range between 0.747 and 0.916 except for the PBC construct which have a value of 0.661. In order to keep the general form of the basic model, we decide to keep this construct.

3.3. Confirmatory Factor Analysis (Measurement Model)

To evaluate reliability and validity of the final measurement model, we use the following three criteria as suggested by Fornell and Larcker (1981).

1. All indicators factor loading should be significant and exceed 0.5,

Table 2. Construct reliability and convergent validity

| Constructs | Items | Factor Loading | t-Value | Average Variance Extracted | Cronbach’s Alpha |

| Perceived usefulness | PU1 | 0.58 | 7.46 | 0.455 | 0.797 |

| PU2 | 0.63 | 8.57 | |||

| PU3 | 0.68 | 6.30 | |||

| PU4 | 0.79 | 6.66 | |||

| Perceived ease of use | PEOU1 | 0.95 | 6.51 | 0.624 | 0.747 |

| PEOU2 | 0.81 | 7.57 | |||

| PEOU3 | 0.56 | 5.64 | |||

| Security and privacy | SP1 | 0.95 | 7.18 | 0.845 | 0.838 |

| SP2 | 0.90 | 10.12 | |||

| SP3 | 1.08 | 10.39 | |||

| SP4 | 0.83 | 8.55 | |||

| SP5 | 0.81 | 8.48 | |||

| Attitude | ATT1 | 0.72 | 7.55 | 0.680 | 0.838 |

| ATT2 | 0.87 | 10.47 | |||

| ATT3 | 0.83 | 8.11 | |||

| ATT4 | 0.87 | 9.30 | |||

| Subjective norm | SN1 | 0.91 | 15.78 | 0.781 | rowspan=3 bgcolor=white>0.916|

| SN2 | 0.86 | 14.83 | |||

| SN3 | 0.88 | 16.20 | |||

| Perceived behavioral control | PBC1 | 0.69 | 6.29 | 0.575 | 0.661 |

| PBC2 | 0.79 | 4.87 | |||

| PBC3 | 0.79 | 5.56 | |||

| Intention to use IB | INT1 | 0.91 | 11.18 | 0.746 | 0.856 |

| INT2 | 0.85 | 10.13 | |||

| INT3 | 0.83 | 9.09 |

2. Average variance extracted (AVE) by each construct should exceed the variance due to measurement error for the construct (e.g., AVE should exceed 0.5).

As shown in Table 2, all obtained value of the factor loading exceed the 0.5 and where significant at the 1% level. This indicates convergent validity for all latent variables. The result of AVE are well above 0.5 except for the first construct where the AVE is equal to 0.455. This result shows that discriminant validity is supported for all constructs (Fornell & Larcker, 1982).

3.4. Structural Equation Model (SEM)

3.4.1. Model Testing

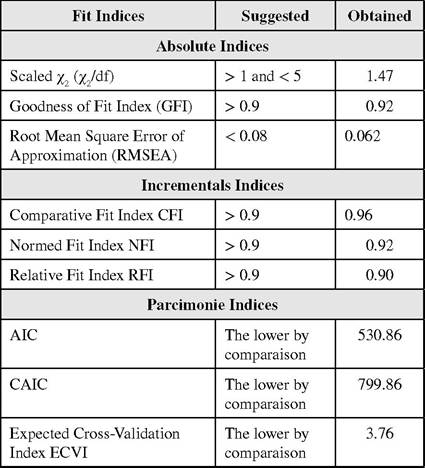

The final measurement model reached or succeeded all recommended thresholds, with a scaled (χ2Zdf) equal to 1.47, a goodness-of-fit index (GFI) of 0.92, the root mean square error of approximation (RMSEA) is 0.062, the comparative fit index (CFI) is 0.96, the normed fit index (NFI) is 0.92 and the relative Fit index (RFI) is 0.90. The results are reported in Table 3.

For the three AIC, CAIC and ECVI indices, by comparison, means that we compare the estimated model to the saturated model and the independent model. The values of the AIC, CAIC and ECVI for the saturated and independent models are respectively 650, 1935.64, 4.61 and 5394.57, 5493.46, and 38.26. For these three last indices, the results indicate that the three indices are adequate.

3.4.2. Hypothesis Testing Results

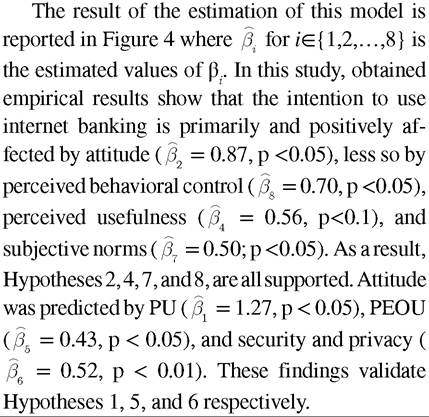

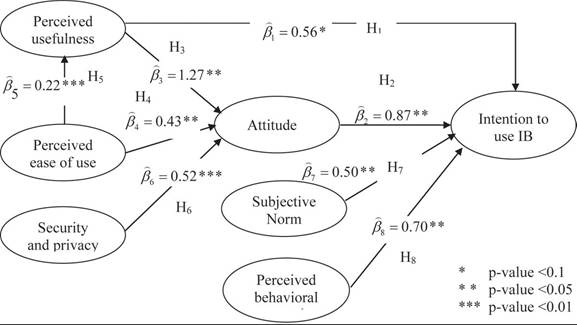

In order to test previous proposed hypothesis H1 to H8, we estimate the following structural model using the Lisrel 8.8. The results are reported in Figure 4. For each parameter β. we report the level of significance where *,** and *** indicate respectively the 10%, 5% and 1% level.

Table 3. Results of Goodness of Fit

Figure 4. Estimation results of the research model

3.5. Discussion, Conclusion and Limitations, and Futures Research

3.5.1. Discussion

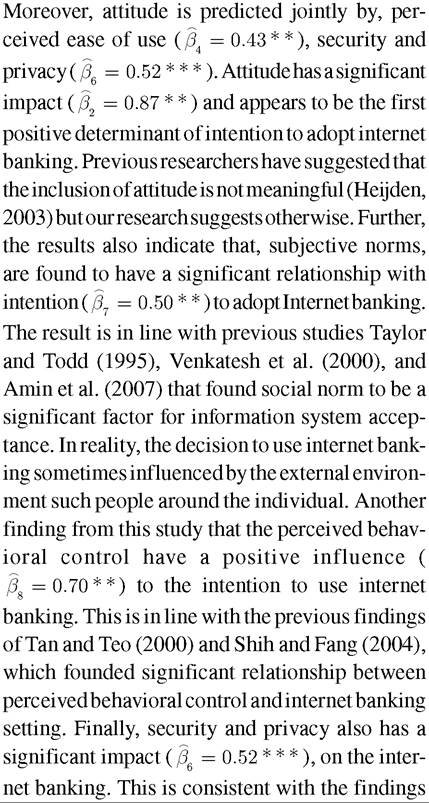

The results of this study provide support for the conceptual model presented in Figure 3 and for the hypotheses regarding the directional linkage

of Sathye (1999), Chung and Paynter (2001), Sohail and Shanmugham (2004), Gerrard and Cunningham (2003), Sayar and Wolfe (2007), and Sohail and Shaikh (2007), which have reported that these factors have positive influences on the acceptance, of information system.

4. CONCLUSION

Theoretically, this study confirms the appropriateness of TAM and TPB in predicting intention to use internet banking in a Tunisian banking environment. This research reveals that TAM could be used to provide a solid theoretical foundation of internet banking in Tunisian case. Security and privacy were selected as additional factors to TAM and TPB construct because oftheir potential influence on the use electronic system. The result of the statistical analysis showed that all the seven factors used to explain intention to use internet banking have a positive and significance influence on the adoption of the system. The result of this study clearly reflects that users find internet banking system useful, and easy to use. Attitude, perceived behavior control and perceived usefulness are the critical factor in explaining users’ adoption of internet banking. In order, to promote the use of internet banking by Tunisian customers financial institutions in Tunisia could take several actions. First, internet banking professional should create a positive perceptions among its customers regarding of internet banking services. Creating positive perceptions might be adequately achieved by offering free information without any charges or at minimum charges. To promote internet banking, there is a need to devise new marketing campaign so as to target more elderly people informing them of the facilities of this service and to make this technology easy to use. Also, banks should promote the advantages that online banking when compared to traditional ways of banking. Finally, banks in Tunisia should ensure that security and privacy of the internet banking systems are properly developed and users should also be made aware of their systems are secured and personal information is protected.

4.1. Limitations and Future Research

Although the results can be considered statistically significant, this research has some limitations; the first is the sample size comprised with 284 people. Future research requires a larger sample for the purpose of higher accuracy. Second, other factors such as convenience, confidence, cost, and experience were not taken into consideration and warrant the need for future research in the field of Internet banking adoption.

REFERENCES

Ajzen, I. (1985). From intentions to actions: A theory of planned behavior. In J. Kuhl, & J. Beckmann (Eds.), Action control: From cognition to behavior (pp. 11-39). New York, NY: Springer. doi:10.1007/978-3-642-69746-3_2

Ajzen, I. (1991). The theory of planned behaviour. Organizational Behavior and Human Decision Processes, 50, 179-211. doi:10.1016/0749- 5978(91)90020-T

Aladwani, M. A. (2001). Online banking: A field study of drivers, development challenges, and expectations. International Journal of Information Management, 21, 213-225. doi:10.1016/S0268- 4012(01)00011-1

Amin, H., Baba, R., & Muhammad, M. Z. (2007). An analysis of mobile banking acceptance by Malaysian customers. Sunway Academic Journal, 4, 1-12.

Anderson, J. C., & Gerbing, D. W. (1988). Structural equation modeling in practice: A review and recommended two step approach. Psychological Bulletin, 49, 411-423. doi:10.1037/0033- 2909.103.3.411

Chan, S. C., & Lu, M. T. (2004). Understanding internet banking adoption and use behavior: A Hong Kong perspective. Journal of Global Information Management, 12, 21-43. doi:10.4018/ jgim.2004070102

Chang, Y. T. (2003). Dynamics of banking technology adoption: An application to internet banking. Coventry, UK: Department of Economics, University of Warwick.

Cheng, T., Lama, D., & Yeung, A. (2006). Adoption of internet banking: An empirical study in Hong Kong. Decision Support Systems, 42(3), 1558-1572. doi:10.1016/j.dss.2006.01.002

Chung, W., & Paynter, J. (2001). An evaluation of Internet Banking in New Zealand. Auckland, New Zealand: Department of Management Science and Information Systems, The University of Auckland.

Daniel, E. (1999). Provision of electronic banking in the UK and the Republic of Ireland. International Journal of Bank Marketing, 17(2), 72-82. doi:10.1108/02652329910258934

Davis, F. D. (1989). Perceived usefulness, perceived ease of use, and user acceptance of information technology. Management Information Systems Quarterly, 13, 319-340. doi:10.2307/249008

Davis, F. D. (1992). User acceptance of information technology: System characteristics, user perceptions and behavioral impacts. International Journal of Man-Machine, 38(3), 475-487. doi:10.1006/imms.1993.1022

Davis, F. D., Bagozzi, R., & Warshaw, P. R. (1989). User acceptance of computer technology. Management Science, 35(8), 982-1003. doi:10.1287/ mnsc.35.8.982

Fagan, M. H., Wooldridge, B. R., & Neill, S. (2008). Exploring the intention to use computers: An empirical investigation of the role of intrinsic motivation, extrinsic motivation, and perceived ease of use. Journal of Computer Information Systems, 48(3), 31-37.

Fishbein, M., & Ajzen, I. (1975). Belief, attitudes, intention and behavior: An introduction to theory and research. Reading, MA: Addison-Wesley.

Fornell, C., & Larcker, D. (1981). Evaluating structural equation models with unobservable variables and measurement error. JMR, Journal of Marketing Research, 18(1), 39-50. doi: 10.2307/3151312

Gefen, D., & Straub, D. (2000). The relative importance of perceived ease of use in IS adoption: A study of ecommerce adoption. Journal of the Association of Information Systems, 1(8), article 8.

Gerrard, P., & Cunningham, J. B. (2003). The diffusion of Internet banking among Singapore consumers. International Journal of Bank Marketing, 21(1), 16-28. doi:10.1108/02652320310457776

Godwin, J. U. (2001). Privacy and security concerns as a major barrier for e-commerce: A survey study. Information Management & Computer Security, 9(4), 165-174. doi:10.1108/ EUM0000000005808

Hair, J. F., Anderson, R. E., Tatham, R. L., & Black, W. C. (1998). Multivariate data analysis. Upper Saddle River, NJ: Prentice Hall.

Heijden, H. V. (2003). Factors influencing the usage of websites: The case of a generic portal in The Netherlands. Information & Management, 40(2), 541-549. doi:10.1016/S0378-7206(02)00079-4

Hsu, M. H. (2004). Internet self-efficacy and electronic service acceptance. Decision Support Systems, 38, 369-381. doi:10.1016/j.dss.2003.08.001 Hsu, M. H. (2006). A longitudinal of continued online shopping behavior: An extension of the theory of planned behavior. International Journal of Human-Computer Studies, 64, 890-904. doi:10.1016/j.ijhcs.2006.04.004

Huang, E. (2008). Use and gratification in econsumers. Internet Research, 18(4), 405-426. doi:10.1108/10662240810897817

Koufteros, X. A. (1999). Testing a model of pull production: A paradigm for manufacturing research using structural equation modeling. Journal of Operations Management, 17, 467-48 8. doi:10.1016/S0272-6963(99)00002-9

Lederer, A. L., Maupin, D. J., Sena, M. P., & Zhuang, Y. (2000). The technology acceptance model and the World Wide Web. Decision Support Systems, 29(3), 269-282. doi:10.1016/S0167- 9236(00)00076-2

Miyazaki, A. D., & Fernandez, A. (2001). Consumer perceptions of privacy and security risks for online shopping. The Journal of Consumer Affairs, 35(1), 27-44. doi:10.1111/j.1745-6606.2001. tb00101.x

Moon, J. W., & Kim, Y. G. (2001). Extending the TAM for a World-Wide-Web context. Information & Management, 38(4), 217-230. doi:10.1016/ S0378-7206(00)00061-6

Nissenbaum, H. (2004). Will security enhance trust online or support it? In P. Kramer, & K. Cook (Eds.), Trust and distrust within organizations: Emerging perspectives, enduring questions (pp. 155-188). New York, NY: Russell Sage.

Norazah, M. S., & Norbayah, M. S. (2009). Exploring the relationship between perceived usefulness, perceived ease of use, perceived enjoyment, attitude and subscribers’ intention towards using 3g mobile service. Internet Journal, 3(3), 1-11.

Norazah, M. S., Ramayah, T., & Norbayah, M. S. (2008). Internet shopping acceptance: Examining the influence of intrinsic versus extrinsic motivations. Direct Marketing: An International Journal, 2(2), 97-110. doi:10.1108/17505930810881752

Online banking goes mainstream in U.S. and UK. (2003). Gartner.

Pikkarainen, T. (2004). Customer acceptance of online banking: An extension of the technology acceptance model. Internet Research, 3, 224-235. doi:10.1108/10662240410542652

Pikkarainen, T., Pikkarainen, K., Karjaluoto,

H., & Pahnila, S. (2004). Consumer acceptance of online banking: An extension of the technology acceptance model. Internet Research, 14(3), 224-235. doi:10.1108/10662240410542652

Salisbury, W. D., Pearson, R. A., Pearson, A. W., & Miller, D. W. (2001). Perceived security and World Wide Web purchase intention. Industrial Management & Data Systems, 101, 165-176. doi:10.1108/02635570110390071

Sathye, M. (1999). Adoption of Internet banking by Australian consumers: An empirical investigation. International Journal of Bank Marketing, 17(J'), 324-334. doi:10.1108/02652329910305689

Sayar, C., & Wolfe, S. (2007). Internet banking market performance: Turkey versus the UK. International Journal of Bank Marketing, 25(3), 122-141. doi:10.1108/02652320710739841

Shih, Y. Y., & Fang, K. (2004). The use of decomposed theory of planned behaviour to study Internet banking in Taiwan. Internet Research, 14(3), 213-223. doi:10.1108/10662240410542643

Sohail, M., & Shanmugham, B. (2004). E-banking and customers’ preferences in Malaysia: An empirical investigation. Information Sciences, Informatics and Computer Science. International Journal (Toronto, Ont.), 150(3-4), 207-217.

Sohail, M. S., & Shaikh, N. M. (2007). Internet banking and quality of service, perspectives from a developing nation in the Middle East. Online Information Review, 32(1), 58-72. doi:10.1108/14684520810865985

Tan, M., & Teo, T. S. H. (2000). Factors influencing the adoption ofInternet banking. Journal of the Association for Information Systems, 1(5), 1-42.

Taylor, S., & Todd, P. (1995). Understanding information technology usage: A test of competing models. Information Systems Research, 6(2), 144-176. doi:10.1287/isre.6.2.144

Venkatesh, V., & Davis, F. (2000). A theoretical extension of the technology acceptance model: Four longitudinal field studies. Management Science, 46(2), 186-204. doi:10.1287/ mnsc.46.2.186.11926

Venkatesh, V., Morris, M. G., & Ackerman, P. L. (2000). A longitudinal field investigation of gender differences in individual technology adoption decision-making processes. Organizational Behavior and Human Decision Processes, §3(1), 33-60. doi:10.1006/obhd.2000.2896 PMID:10973782

Wadie, E., & Charfeddine, L. (2011). Factors affecting the adoption of internet banking in Tunisia: An integration theory of acceptance model and theory of planned behavior. The Journal of High Technology Management Research, 23(1), 1-14. Wang, Y. D., & Emurian, H. H. (2005). An overview of online trust: Concepts, elements, and implications. Computers in Human Behavior, 21, 105-125. doi:10.1016/j.chb.2003.11.008

Westin, A. F., & Maurici, D. (1998). E-commerce & privacy: What the net users want. New York, NY: Privacy & American Business, and PricewaterhouseCoopers LLP. Retrieved from http://www. pwcglobal.com/gx/eng/svcs/privacy/images/E- Commerce.pdf

White, H., & Nteli, F. (2004). Internet banking in the UK: Why are there not more customers? Journal of Financial Services Marketing, 9(1), 49-56. doi:10.1057/palgrave.fsm.4770140

Wu, I. L., & Chen, J. L. (2005). An extension of trust and TAM model with TPB in the initial adoption of on-line tax: An empirical study. International Journal of Human-Computer Studies, 62, 784-808. doi:10.1016/j.ijhcs.2005.03.003

ENDNOTES

1 The results of the KMO, the factors contribution using the ACP and the Varimax for unidemnsality can be obtained upon request from the authors.

This work was previously published in International Journal of Innovation in the Digital Economy (IJIDE), 4(1); edited by Elena Druica and Ionica Oncioiu, pages 16-30, copyright 2013 by IGI Publishing (an imprint of IGI Global).

APPENDIX

Survey Instrument

Please rate the questions from regarding the bank’s Website service (Table 4) on the following scale: (1) Strongly Disagree; (2) Disagree; (3) Sans Opinion; (4) Agree; (5) Strongly Agree.

Table 4.

| N° | Item | (1) | (2) | (3) | (4) | (5) |

| Perceived Usefulness | ||||||

| PU1 | I think that using the online banking would enable me to accomplish my tasks more quickly. | (1) | (2) | (3) | (4) | (5) |

| PU2 | I think that using the online banking would make it easier for me to carry out my tasks. | (1) | (2) | (3) | (4) | (5) |

| PU3 | I think the online banking is useful. | (1) | (2) | (3) | (4) | (5) |

| PU4 | Overall, I think that using the online banking is advantageous. | (1) | (2) | (3) | (4) | (5) |

| Perceived Ease of Use | ||||||

| PEOU1 | I think that learning to use online banking would be easy. | (1) | (2) | (3) | (4) | (5) |

| PEOU2 | I think that interaction with online banking does not require a lot of mental effort. | (1) | (2) | (3) | (4) | (5) |

| PEOU3 | I think that it is easy to use online banking to accomplish my banking tasks. | (1) | (2) | (3) | (4) | (5) |

| Security and Privacy | ||||||

| SP1 | I trust in the technology an online bank is using | (1) | (2) | (3) | (4) | (5) |

| SP2 | I trust in the ability of an online bank to protect my privacy | (1) | (2) | (3) | (4) | (5) |

| SP3 | I trust in an online bank as a bank | (1) | (2) | (3) | (4) | (5) |

| SP4 | Using an online bank is financially secure | (1) | (2) | (3) | (4) | (5) |

| SP5 | I am not worried about the security of an online bank | (1) | (2) | (3) | (4) | (5) |

| SP6 | Matters of security have no influence on using an online bank | (1) | (2) | (3) | (4) | (5) |

| Attitude | ||||||

| ATT1 | I think that using online banking is a good idea. | (1) | (2) | (3) | (4) | (5) |

| ATT2 | I think that using online banking for financial transactions would be a wise idea. | (1) | (2) | (3) | (4) | (5) |

| ATT3 | I think that using online banking is pleasant. | (1) | (2) | (3) | (4) | (5) |

| ATT4 | In my opinion, it is desirable to use online banking. | (1) | (2) | (3) | (4) | (5) |

| Subjective Norm | ||||||

| NS1 | People who are important to me would think that I should use online banking. | (1) | (2) | (3) | (4) | (5) |

| NS2 | People who influence me would think that I should use online banking. | (1) | (2) | (3) | (4) | (5) |

| NS3 | People whose opinions are valued to me would prefer that I should use online banking. | (1) | (2) | (3) | (4) | (5) |

| Perceived Behavior Control | ||||||

| PBC1 | I think that I would be able to use the online banking well for financial transactions. | (1) | (2) | (3) | (4) | (5) |

| PBC2 | I think that using online banking would be entirely within my control. | (1) | (2) | (3) | (4) | (5) |

| PBC3 | I think that I have the resources, knowledge, and ability to use online banking. | (1) | (2) | (3) | (4) | (5) |

continued on following page

Table 4. Continued

Acronyms of Banks

AB: Amen Bank

ATB: Arab Tunisian Bank

ATTIJARIBANK: Attijaribank

BFT: Banque Franco Tunisienne

BH: Banque de l'Habitat

BIAT: Banque Internationale Arabe de Tunisie

BNA: Banque Nationale Agricole

BT: Banque de Tunisie

BTE: Banque de Tunisie et des Emarates

BTK: Banque Tuniso Koweitienne

BTS: Banques Tunisiennes de Solidarite

BZ: Banque Zitouna

STB: Societe Tunisienne des Banques

TQB: Tunisian Qatari Bank

UBCI: Union bancaire pour le Commerce et FIndustrie

UIB: Union International des Banques

832