Chapter 43 Explaining International Land Transactions in Africa

Yohannes G. Hailu

United Nations Commission for Africa, Rwanda

Adesoji Adelaja

Michigan State University, USA

Henry Akaeze

Michigan State University, USA

Steve Hanson

Michigan State University, USA

ABSTRACT

Rising global food prices and demand for biofuels have recently heightened global interests in agricultural land resources in Africa, resulting in increased International Land Transactions (ILTs).

While opponents of ILTs have dubbed it “land grabbing, ” proponents welcome the opening of Africa’s agriculture to foreign direct investment. Limited empirical work exists explaining the motivations of investor and host countries. This chapter attempts to expand the literature by providing an empirical explanation of country land targeting behavior. As the debate on “land grabbing” intensifies, understanding motivations of various actors in the land market becomes relevant.1. INTRODUCTION

We define International Land Transactions (ILTs) as “substantive land purchase or lease arrangements, or agreements, which involve participants from more than one nation.” Each transaction involves at least one host country (on the sale side of the market) and one buyer entity (which can be a foreign government, business, group ofindividuals or institutional investors, or combinations thereof). ILTs range from outright International Land Acquisitions (ILAs) to International Land Leases (ILLs). ILTs have recently become an important issue of concern (Mann and Smaller 2010; Aarts

DOI: 10.4018/978-1-4666-6268-1.ch043 2009; Robertson and Per 2010; Borras and Franco 2010a; Braun and Meinzen-Dick 2009), especially amongst international equity- and fairness-based organizations, Western donor countries and international financial organizations. However, little is known about why some African countries are targeted for land transactions and why some host governments may be more interested than others.

This chapter focuses on these issues.The United Nations Food and Agriculture Organization (FAO) estimates that between 2007 and 2010, some 20 million hectares of African land was acquired by foreign entities, with many such acquisitions involving more than 10,000 hectares and several more than 500,000 hectares (see Graham et al. 2010). The International Food Policy Research Institute (IFPRI) suggests that approximately 20 million hectares changed hands in the form of land grabs between 2005 and 2009 (see Borras et al. 2010b; Braun and Meinzen-Dick

.

2009). The World Bank similarly reports that 45 million hectares changed hands globally and that half of the global transactions have taken place in Africa (Deininger et al. 2011). Cotula et al. (2009) report that sub-Saharan Africa has become the site of the most speculative land deals, while Zoom- ers (2011) and Visser and Spoor (2011) indicate that major areas in Africa are being targeted for commodity and fuel crops investments and ecosystem services.

ILTs are certainly nothing new in many parts of the world.1 For decades, governments and businesses have ventured into other countries to acquire or lease land for a variety of reasons.2 However, the recent spike in the frequency of ILTs has sparked significant debate about the causes and appropriateness of these activities (Duanglak 2010; Cotula et al. 2009; Mann and Smaller 2010; Daniel and Mittal 2009). The scope and magnitude of ILTs were dismal in Africa until more recent years. The fact that Africa, a continent where most countries face significant food security challenges and which has previously been passed over by large-scale global private and public investors, is the focus of most deals is intriguing. In fact, most participants in the debate on ILTs in Africa have largely dubbed it “land grabbing,” which connotes that these transactions are driven by motives tied to the control of productive resources for speculative purposes and/or exploitation of local people and governments (Daniel and Mittal 2009; Li 2011).

Opponents of ILTs often cite the high degree of asymmetry in the knowledge bases of targeted countries (sellers) and targeting countries (buyers) which puts the former at a disadvantage at the negotiating table (Schutter 2011).One rationale for equating the large-scale incidents of ILTs in Africa to “land grabbing” is the fact that these activities spiked following the global food and commodity prices of 2007/2008. Another is that the incidence is heavily focused on Africa. The economic assumption behind this thinking, of course, is that when resource prices rise significantly, alternatives become attractive, and buyers shift more of their land demand toward those places that had previously been considered more risky, or less valuable. This storyline fits well with the African situation in that it explains ILTs in the context of a global competition for resources. The concept of “land grabbing” then becomes relevant only if one can prove that this shift of focus towards Africa goes well beyond the normal location substitution with respect to input source, and that resource buyers also have speculative motives which encourage them to hoard more land (or resources) than would be typical given the impetus of global price hikes and resource shortage. Proving “hoarding” or “speculative” behavior requires evidence of interest in long-term capital gains, which has not been provided in the literature. While some of the actors in ILTs in Africa may indeed have speculative motives, it is plausible that the motivations of others are consistent with standard optimal business or government behavior, which seeks to maximize food security and access to critical assets for food production.

Whether or not ILT activities in Africa qualify as land grabs, the major international organizations have dubbed it as such. The World Bank (WB), the Millennium Challenge Corporation (MCC), the Alliance for a Green Revolution in Africa (AGRA), the US Agency for International Development (USAID), the United Nations Food and Agricultural Organization (FAO), and the International Food Policy Research Institute (IF- PRI) are among the many organizations that have devoted significant efforts (meetings, conferences and reports) to the “land grabbing” issue.

Similarly, foundations such as the Bill and Melinda Gates Foundation, the Howard G. Buffet Foundation and the Omidyar Network have been active in the issue, based on concerns about the possible ills of “land grabbing.” The concern about ILTs has extended to international research organizations as well as support organizations such as Action Aid International, Heifer International, Oxfam, Global Witness, World Cocoa Foundation, Landesa, the Right and Resources Initiatives and the World Resources Institute.3International organizations, donor country governments and foundations who tend to view these contentious ILT issue as a problem are advocating for greater monitoring of the phenomenon and the creation of best practices that would maximize the benefits to host countries. In a general sense, these groups represent the opposition to large-scale ILTs, as they are currently occurring. Investment groups and host countries, however, have not fully embraced attempts by international organizations to define frameworks for responsible ILTs being proposed and demanded by international organizations. While these groups have not outright rejected oversight proposals, their opposition to what is perceived in what is a normal market activity is palpable. One investment banker proposed an alternative term to be used in describing what otherwise would be referred to as “land grabbing” - “price-gap arbitrage.” This seems to suggest adherence to free market behavior by international investors. In light of the above differences, ILTs in Africa have become contentious, one that intellectual and policy leaders in land use, land tenure and sustainable resource management have determined to be of significant importance.4 Greater research to clarify many of the contentious issues is not only important, but timely as well.

Empirical evidence of the harmful or negative effects of ILTs is lacking, obviously due to the fact that the heightened incidence of this issue is recent, and not enough time has passed to allow sufficient ex-post analysis in Africa.

Better understanding of the incidence of ILTs in Africa, the geographic expression of such activities, the characteristics of targeted countries, and the characteristics of targeting entities will improve understanding of the motivations behind these transactions and perhaps shed some light on the equity implications. The idea is to explore potential adverse effects based on better understanding of motivations. The issue of ILTs is too important for scholars and policy makers to wait for future impact assessment.Given the recent emergence of the issue at the forefront, much of the global discourse has offered not much more than emotional response to the issue. To provide insights to concerned entities and countries engaged in ILTs, it is important to first understand ILTs, their structure and implications to host and investing countries and entities. Research must address the concerns of key actors in this arena, in addition to providing information that can be used for capacity building and education to strengthen the institutional and human capital capacity of African countries as they manage ILTs. By understanding the motivations, one can gain significant insights not only into the desirability of ILTs, but also how to structure their provisions to be mutually beneficial. Attempts to explain the motivations of participating countries on the buy and sell sides have been limited.

Explaining ILTs in Africa through the modeling of the behavior of buyers and sellers is the subject of this paper. The approach employed is to better understand the etiology of ILTs before we declare them to be a moral challenge. The remainder of this paper is organized as follows. First, we review existing literature on ILTs in order to gain insights that are useful in the development of theories and hypothesis about the motivations of various actors in the process. Second, to provide a proper economic context within which ILTs can be better understood, a theoretical framework is developed and explained to characterize the behavior of land targeting entities and host countries.

Third, to provide empirical evidence about the driving forces behind the demand and supply of agricultural lands in Africa under ILTs, an empirical econometric model is developed. Fourth, this model, which aggregates the motivations of all buyers in the demand side of the market, is estimated. Fifth, the chapter discusses the nature and types of data collected to estimate the empirical model developed. Finally, discussions of the findings from the analysis of the incidence of ILTs in Africa are provided, along with conclusions and policy suggestions.2. UNDERSTANDING INTERNATIONAL LAND TRANSACTIONS

In this section, we delve into existing literature on ILTs in order to highlight priority issues requiring greater understanding and to establish a background for our modeling efforts to explain ILTs. The analysis starts with the complexity of ILTs, the reasons provided for the occurrence of ILTs, explanations of where ILT activities are likely to take place, explanations of the characteristics of the demand side of the market, explanations of the characteristics of seller side of the market, explanations of the motivations of various actors and other issues that are central to the ILT debate.

The issues surrounding ILTs are obviously complex, albeit their apparent simplicity. First, ILTs involve varying types of host countries with various characteristics, interests and motivations (Duangklad 2010). Second, ILTs involve a variety of buyer types, with varying types of actors and motivations (Spieldoch 2009; Visser and Spoor 2010). Third, and consequently, given these diverse seller and buyers, and interests and motivations, the structure of ILTs tend to vary from lease arrangements to actual purchases, from pure acquisition of land to collateral investments to beef-up productive capacity, and from schemes designed to feed the export of products back to the homelands of investors to ameliorate food security challenges (Schutter 2011), or enhance the performance of food firms (McMichael 2011), to those designed to enhance supplies to local markets. An understanding of the diverse interests in and motivations for ILTs will go a long way in helping policymakers and interested parties in learning how to best engage to enhance the efficacy of present and future land transactions.

2.1. Concerns and Opportunities in ILTs

In this section, we summarize some of the reasons for concerns about ILTs. One primary concern is long-term food security in Africa. Opponents caution that the significant incidence of change in control of productive resources could lead to a major food crisis in Africa (Graham et al. 2010; Cotula et al. 2009; Oppeln and Schneider 2009). Another reason is the potential for “land grabbing” to interfere with the right to feed oneself by diverting the potential for food for local consumption to be redirected toward exports (Graham et al. 2010; Schutter 2009). Another concern centers around speculative land deals whereby collateral investments in productive activity never gets made. The argument is that productive land can become tied-up in speculative endeavor, resulting in idling ofland resources and hampering local agricultural production.

Some concerns have been raised about the isolation of foreign-held agricultural operations even when collateral investments are made to produce agricultural products. Many have argued that these land transactions need to feature strong provisions to tie the activities of investors to capacity building activities in the host country (training local farmers, sub-contracting with local farmers, developing rural infrastructure, improving transportations facilities, improving storage capacity and enhancing market operations). Investments in land, labor, capital and technology in host countries would more likely yield better results than investments in land that do not spillover to the rest of the economy (Li 2011). A related issue is the intended market for the products produced, if in fact the foreign-held agricultural operation actually produces anything. If strong arrangements are in place to ensure that a certain proportion of the products are directed to domestic markets, these agricultural operations will essentially compete with local agriculture.

Another concern is the tendency for these transactions to compromise domestic land tenure arrangements (Berry 2002; Mann and Smaller 2010; Braun and Meinzen-Dick 2009). To the extent to which fewer quantities of land remain in the hands of local indigenous people and are under the control of foreign entities, the property rights of local people are compromised. In some cases, these land transactions occur at higher levels of government, undermining the right of indigenous people. This scenario, while expedient for investors, compromises even the potential for the acquired land to be usable in actual production. In some parts of Africa, a federal or state driven land transaction may mean little in terms of actual ownership, especially when local land owners believe the land belongs to them. Similarly, in cases where the transactions involve local government but not higher levels of government, it is difficult to obtain legitimate titles.

Other concerns include: asymmetries in information and knowledge about how to optimally structure deals and transaction terms; expertise gap between trained land investors and local officials who may not have adequate expertise to negotiate on multimillion dollar deals (Schutter 2011); lack of transparency and potential for corruption (Aarts 2009); the possibility that investments may not enhance agricultural productivity or benefit local farmers and peasants (Mann and Smaller

2010) ; the diversity of motives of buyers and the fact that host countries may not be well equipped to structure deals that recognize various investor motives; and the possibility that local land interest groups, who must ultimately cooperate for transactions to be successful, may not be engaged (Robertson and Pinstrup-Anderson 2010).

The literature also cites other relevant factors of concern related to ILTs. First is the issue of whether or not ILTs are ultimately beneficial to host countries. The literature suggest that host countries which sell land might be encouraged to do so because the buyers bring in Foreign Direct Investment (FDI) in the land purchase or on production equipment, which are often difficult for developing countries to attract (Visser and Spoor

2010). In the case of the latter, foreign investment to enhance the capacity of purchased land can result in collateral agricultural activities that can enhance local production, technology diffusion, employment, and workforce development. However, whether or not these investments are appropriate depends on the extent to which the host country benefits. The benefits range from local increase in agricultural productivity, increased agricultural production, the employment of local workers, the improvement of the talent pool of local agricultural workers, the increased supply of food to domestic consumers and the reduction of food insecurity, and possibly even poverty. Evidence is lacking as to whether or not these benefits accrue (see Li

2011), but then whether these benefits accrue is a convoluted issue related to the existence of strong agency problems and the potential for corruption in some countries.5

2.2. Characteristics of the Demand Side of ILTs and Deal Structures

The literature identifies some of the characteristics of buyer nations who participate in the sale or long-term lease of land and how these relate to the benefits to them (Visser and Spoor 2011). With respect to types of land purchasers and motivations, the following types have been identified as major players: (1) foreign governments whose interests are food security in their own countries;

(2) apostles or agents of foreign governments whose interests align with the foreign government but might be willing to take more of a portfolio or asset management approach (these include sovereign wealth funds and investment companies);

(3) investment banks and private equity firms who see market and portfolio opportunities in assembling land and working with corporations to get access to such lands for both investment and production purposes; (4) global food and energy companies who seek productive capacity closer to projected high demand emerging countries; and (5) individual/family investors who again see the upside and gains from strategic investments that farmlands in Africa offer.

The motivations above translate into alternative ways by which deals can be structured. The variability in the motivations and behavior of targeting entities suggest that ILTs are not generic, and that each transaction is different and unique. For example, participating buyer countries range from those interested in food and energy security to those interested in speculation; while seller countries ranged from places that have not engaged much in any international transaction, especially trade in agricultural commodities, to places that are actively involved in exports.6

These motivations are expressed through various structural arrangements for ILTs. Entities motivated by food or energy security must obviously make investments in production, and possibly in human capital development. In other words, the ILT may ultimately result in such investments as biofuel refineries, irrigation systems, biofuel crop production, storage capacity, training centers, road infrastructure and other investments that would exploit the gap between current and potential levels of productivity. These types of investments represent deeper FDIs and may have better potential to benefit the host country, depending on how they are structured. For example, if the host country is able to extract long-term training of human resources and the targeting of some of the products toward domestic markets from foreign investors, local food and energy productivity and security can be enhanced.

Entities interested in arbitrage, however, will most likely stop at the acquisition or lease level, and would most likely focus on an exit strategy that involves flipping the land to others who will make long-term investments. These arrangements, however, can be detrimental if they constrain the ability to use the land and facilitate idling. Another dimension of structural arrangements is whether or not the land is leased or outright purchased, and whether the lease arrangement is short-term or long-term. Obviously, while long-term leases facilitate enough protection for the lessee to encourage long-term investments, they also represent forgone productive opportunities and unnecessary tied down of resources that could be put to alternative uses. Outright sales also do have pros and cons related to “hoarding” without necessary long-term investment and productive use.

2.3. Why Africa and Why Now?

Various studies in the literature have attempted to explain the larger issue of why Africa and why now. Despite Africa’s significant land mass (30.3 million square kms), the Sahara (9 million square kms) and Kalahari Deserts (900,000 square kms) constrain the continent’s cultivation capacity. Low levels of human capital development and land productivity also characterize the agricultural sector in Africa. However, the existence of 2-3 growing seasons in much of Africa suggests significant land productivity potential in agriculture. Prior to 2007, this potential was largely overlooked globally as Africa did not engage in significant export of agricultural or bio-energy raw materials, and as advanced economies and donors focused largely on addressing food, health and poverty issues in Africa. So, land in Africa was viewed largely from the perspective of land tenure and the potential role it can play in enhancing people’s access to capital, wealth and the means of production. It was also viewed from the perspective of how the enhancement of human capital and technical inputs can be used to transform Africa. Large scale commercial farming is yet to materialize in a significant way in most African countries.

However, in few places, evidence exists to suggest significant potential for growth in productivity. For example, the recent migration of some Southern African farmers to parts of West Africa yielded enhancements in the productivities of such expatriate farmers, suggesting significant upside to improving production/productivity through human capital and agricultural technology enhancements. Today, many countries in Africa are open for FDI, welcoming opportunities for revenue, investments and economic activities, particularly in agriculture. Productivity and land value gaps between Africa and the rest of the world seems to have intensified significant surge in interest in African agricultural land resources and may have enabled African countries to tap these FDI opportunities.

With respect to why now, the potential for African agriculture to feed the world was a nonissue until the global spike in the price of food and natural resources in 2007 and 2008 (Deninger et al. 2011; Visser and Spoor 2011). Among the reasons for the growing interest in Africa were the global energy crisis (sharp rises in the price of energy resources) (Cotola et al. 2008; Boamah 2011; Borras and Franco 2010), rapid increases in income and wealth of countries previously designated as developing, and entrance of two major players (China and India) with combined population of approximately 2.7 billion people in to the market for energy and food (Braun and Meinzen-Dick 2009), the threat to food supply of net food importing countries, greater concern about long-term food supplies (Robertsonn and Pinstrup-Anderson 2010), food price volatility (Aarts 2009), development aid deficits (Cotula et al. 2009), and scarce water resources (Mann and Smaller 2010). Africa’s potential is significant, but the cost of acquisition of land is low. For those who believe that this is a new opportunity to optimize Africa’s productive use of land and to beef-up human capital, management capacity, trade capacity, food security, infrastructure development and economic buoyancy, ILTs can be seen as alternatives.

Hitherto, the African land market has been largely obscure from the global radar screen. However, the recent surge in interest has created a dilemma. While the international organizations mentioned earlier were concerned about how to increase productivity and secure land tenure designed to improve property rights, provide people with a means of production, increasing wealth, growing agricultural productivity and alleviate poverty, the issue of “land grabbing” seems to have risen to the forefront. The magnitude of ILTs, as they occur today, has brought in large number of actors who are seeking greater insights not only into motivations for ILTs, but also their consequences and impacts.

3. CONCEPTUAL FRAMEWORK

As mentioned above, ILTs involve various motivations both on the part of the selling country and various buyers from targeting countries. When a transaction occurs, it is likely to be the result of a market clearing activity. We recognize the host country representative (local/state/national government) as the primary market agent on the supply-side of the market. We recognize three alternative types of actors on the demand side:

1. A foreign government seeking to acquire land for the purpose of maximizing agricultural production through combination of in-country land resources and acquired/ controlled foreign land resources;

2. A private company seeking to maximize food production from a variety of alternative production places given the market for the products; and

3. A private equity or investment firm (or individuals similarly motivated) who seek to maximize the value of their long-term investment through land hoarding.

To provide a theoretical framework to explain the land management behavior of host countries in dealing with targeting entities, a theoretical discussion is provided next. We start first with the land management decision of a host country, followed by players on the demand side.

3.1. Host Country: Value Maximization from Agricultural Land Management

Consider a host country with known amounts of agricultural land resources. The host country attempts to manage its land resources optimally by deciding on three broader uses of the land: for domestic production; export-oriented production and land potentially made available for international investment opportunities. A part of the agricultural land may lay idle at any time. We assume that the objective of the host country is to maximize the value of its agricultural land resources under alternative agricultural uses.

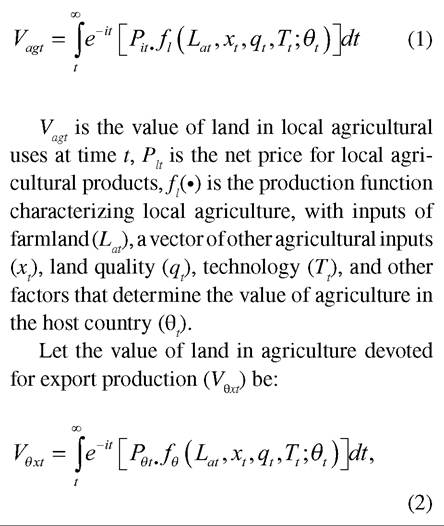

Let the value of land in agriculture for local production (Vιgt) be:

Therefore, given the above factors, the land management objective of a host country is to maximize the value of agricultural lands. This is expressed in Box 1.

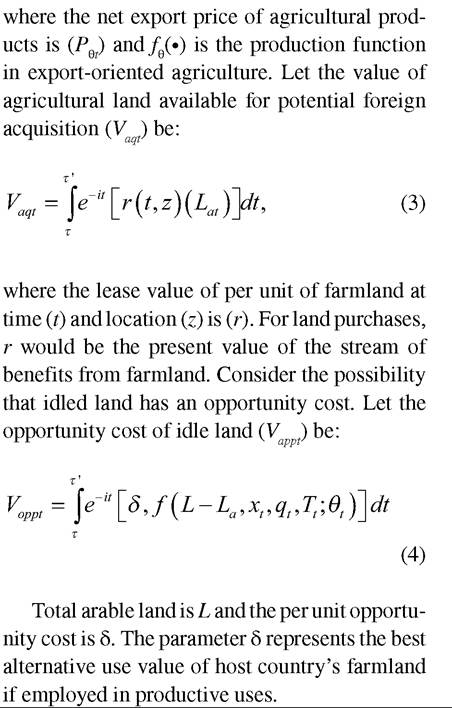

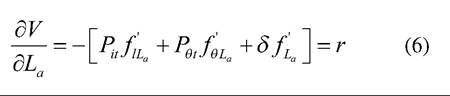

The condition for agricultural land value maximization, given agricultural land use choices, is shown in Equation (6). The relationship implies that host countries can optimally manage agricultural land resources such that land available for international acquisition would need to sufficiently compensate the opportunity costs of local uses. This, of course, depends on existing agricultural land uses before land transfers to foreign holders.

805

806

807

recent concerns. Data on the incidence of ILTs in Africa, although available, probably do not capture all transactions that have occurred. Grain, a small international not-for-profit organization, was one of the first to draw attention to the land grab issue in 2008 when it published its report titled “Seized! The 2008 Land Grab for Food and Financial Security” (http://www.grain.org/ article/entries/93-seized-the-2008-landgrab-for- food-and-financial-security). It reported specific transactions by targeting country and targeted country, respectively, across the globe. It reported details on over 100 land transactions targeting food security in 2008 alone, providing details on specific targeting countries, targeted countries, transaction costs and land mass involved. The International Food Policy Research Institute (IF- PRI) published a report in 2009 which highlighted over 100 transactions globally for the period July 2007-April 2009. The report also indicated recent agricultural funds that are created to target international land transactions. In June 2009, the Federal Ministry for Economic Cooperation and Development of the Republic of Germany issued a report on the battle for land as a scarce resource, listing international land transactions in Africa, Asia and other countries as at June 2009, listing transactions in 25 countries and highlighting the fact that countries such as Madagascar and the Sudan involved a large number of transactions.

In 2010, the Oakland Institute published a report which summarized a number of case studies for the period 2000 to 2010, with a focus on the roles of the International Finance Corporation. Similarly, Graham et al. (2010), on behalf of Food First Information and Action Network (FIAN), published “Land Grab Study” which reported on over 100 transactions in Africa and highlighted the nature and characteristics of each transaction. Deininger et al. (2011) of the World Bank published a study which began to organize the incidence of ILTs by targeting country or firm, targeted country, motivations and intended purpose. It also correlated these transactions with various causal factors highlighting the distribution of valuable land globally and how these relate to the incidence of ILTs.

We collated the data on ILTs from the above and other sources to develop a comprehensive database on known ILTs. We particularly focused on Africa, which is the reported epicenter of the “land grabbing” phenomenon. Given our interest in modeling what triggers a transaction to happen, our dependent variable is binary in nature and takes on the value of 1 if a transaction happened in a country, and 0 otherwise. In essence, we focused on the probability of a transaction happening in a country, not on the size or frequency of the transactions or the price of the transaction. Independent variables in our model include factors that have been identified, or suggested by previous studies, including our theoretical model. In essence, in our proposed regression, we set each hypothesized driver of an ILT up to be detected as a relevant determining factor.

Despite the plethora of data on transactions, very little empirical evidence exists to support how and why ILTs happen. Consequently, the debate about ILTs have centered around preconceived notions and emotionally-based conclusions (Deininger 2011). The two prior studies that attempted to explain why some countries are targeted for land acquisition deals do not provide sufficient basis for understanding ILTs.7 While informative, two limitations exist.

First, the decision of why host countries sell land leases (or allow purchases) is largely ignored, as is the motivation of the targeting entities in international land transactions. This shortcoming emanates from limited efforts in integrating economic theory in the analysis of the behavior of agents in the demand and supply side of the land transaction in Africa. By simply treating host countries as mere suppliers of land, and targeting countries as strategic players who seek to enhance their interests, most of the prevailing work offers limited insights on the underlying motivations on both sides of the transaction.

Second, the limited inclusion of factors in the empirical analysis has also limited the ability to broadly explain why some countries are targeted. For instance, one would expect that institutional quality, trade history, water supply, food security, soil fertility, agricultural capital, GDP per capita and other factors to also be relevant factors that may explain targeting behavior. But these considerations were excluded from prior empiric al studies.

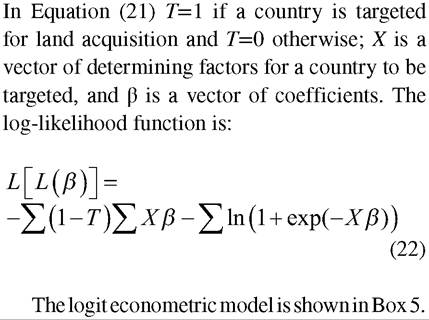

The main focus of this paper is therefore the identification of a broad range of factors that lead to country targeting behavior in land transactions in Africa. The driving factors are discovered based on observations about whether a country is engaged in international land transactions or not. A logit econometric modeling approach offers an ideal mechanism for identifying driving factors given binary incidence data. The logit model is specified as:

The dependent variable is whether international land acquisition occurred in country or not; the independent variables are: percent of agricultural land to total land (AglandP), net agricultural trade (NAgTr), agricultural value added (AgValAd), constrained soil fertility (SoilF), processed agricultural import (PAgIm), processed agricultural export (PAgExp), total agricultural export (AgExp), per capita gross domestic product (GDPPC), degree of property rights (PropR), corruption perception index (Corup), agricultural capital (AgCap), gross non-food productivity index (NFoodPI), gross food productivity index (FoodPI), paved roads (Paved), human development index (HDev), land equipped for irrigation (Irrig), undernourishment (UndNour) and food aid dependence (FoodAid). See Table 1 for descriptive statistics and source of the previous data.

The econometric model is estimated using logistic regression. Heteroskedasticity and multicollinearity problems are addressed by carefully selecting relevant variables and estimating coefficients using corrected standard errors. The correction is conducted through White’s procedure. Alternative model structures are also tested to verify the robustness of the estimated coefficients.

5. RESULTS AND DISCUSSION

We attempt to explain the country-targeting behavior of African land investor entities by incorporating the following categories of factors: characteristics of the agricultural sector; natural resources characteristics; agricultural trade; agricultural technology and development;

Box 5. Equation 23

Table 1. Data description and descriptive statistics

| Description of Variables | Source of Data | Mean | Std. Dev. |

| 1 if country is targeted, 0 otherwise | 7, 8, 9, 10, 11, other | 0.49 | 0.51 |

| Agricultural land (% of total land) | 1 | 47.65 | 23.54 |

| Processed agricultural import | 2 | 68.89 | 19.90 |

| Processed agricultural export | 2 | 42.86 | 34.53 |

| Rainfall | 1 | 791.51 | 627.17 |

| Area of severely constrained soil fertility | 1 | 6885.06 | 7835.66 |

| Net agricultural trade | 1 | -171.45 | 803.51 |

| Total agricultural export | 1 | -0.04 | 0.73 |

| Gross food productivity index | 1 | 114.68 | 21.66 |

| Agricultural capital | 1 | -253.13 | 12548.24 |

| Land equipped for irrigation | 1 | 26.38 | 60.95 |

| Paved ways | 5 | 12,005.90 | 2,0251.29 |

| GDP per capita | 2 | 2121.086 | 3,459.418 |

| Human development index | 3 | 48.76 | 16.72 |

| Corruption | 4 | 2.87 | 1.07 |

| Gross non-food productivity index | 1 | 100.67 | 53.25 |

| Property right | 6 | 27.45 | 18.18 |

| Undernourished | 1 | 26.22 | 19.54 |

| Food aid dependence (food aid received per person) | 12 |

Sources: 1 = FAO; 2 = World Bank; 3= UNDP; 4 = Transparency International; 5 = CIA - the World Factbook; 6 = International Property Rights; 7 = IFPRI; 8 = The Oakland Institute; 9 = Federal Ministry for Economic Cooperation and Development, Germany; 10 = FoodFirst and Action Network; 11 = GRAIN; 12 = World Food Program.

infrastructure development; economic and social performance; property right protection and food security. Table 2 summarizes the list of variables, along with estimated coefficients. Findings are discussed next.

5.1. Characteristics of the Agricultural Sector

To evaluate whether or not the characteristics of the agricultural sector itself explains the incidence of ILTs in a country, four factors are considered: Agricultural land (% of total land); agricultural value added; processed agricultural imports and processed agricultural exports. Agricultural trade experience of African countries enhances the chance of ILTs occurring, perhaps because trade experience signals better access of local agricultural to international markets. The fact that the export element of trade is significant and import is not makes this argument more valid. Land investors are not necessarily planning to importsubstitute for the targeted country, so may not weigh import patterns significantly. But exports experience is found to be important predictor of country targeting behavior. Compared to countries with poor agricultural exports, countries with exports experience are 1.062 times more likely to be targeted, with the likelihood increasing as the value of exports expands.

Similarly, agricultural value added is a significant factor. Countries with agricultural sector generating better value added are also likely to be targeted. Countries with better agricultural value

Table 2. Estimation results for ILT behavioral logit model

| Variables | Coefficient | P-value | Likelihoods |

| Characteristics of the Agricultural Sector | |||

| Agricultural land (% of total land) | -0.135** | 0.039 | 0.874 |

| Agricultural value added | 0.089* | 0.076 | 1.093 |

| Processed agricultural import | -0.060 | 0.491 | - |

| Processed agricultural export | 0.047** | 0.042 | 1.048 |

| Natural Resources Characteristics | |||

| Rainfall | 0.004* | 0.092 | 1.004 |

| Area of severely constrained soil fertility | 0.001 | 0.161 | - |

| Agricultural Trade | |||

| Net agricultural trade | 0.003* | 0.057 | 1.003 |

| Total agricultural export | -0.015 | 0.854 | - |

| Agricultural Technology and Development | |||

| Gross food productivity index | 0.106** | 0.036 | bgcolor=white>1.112|

| Agricultural capital | 0.001* | 0.082 | 1.001 |

| Land equipped for irrigation | -0.061* | 0.067 | 0.941 |

| Infrastructure Development | |||

| Paved ways | -0.0001 | 0.321 | - |

| Economic and Social Performance | |||

| GDP per capita | -0.002* | 0.065 | 0.998 |

| Human development | 0.284** | 0.030 | 1.328 |

| Corruption | 0.472 | 0.663 | - |

| Gross non-food productivity index | 0.057* | 0.093 | 1.059 |

| Property Right Protection | |||

| Property right | 0.073** | 0.041 | 1.076 |

| Food Security | |||

| Undernourished | 0.074 | 0.333 | - |

| Food aid dependence | -320.004* | 0.097 | ≈ 0 |

| Constant | -41.002 | 0.092 | |

| Psuedo R-squared | 0.67 | ||

| Log pseudo-likelihood ratio | -10.24 | ||

| Percent correctly predicted | 92% | ||

| N | 51 | ||

Note: * means significant at the 10% level, ** at the 5% level and *** at the 1% level.

added are 1.151 times more likely to be targeted than countries with poor agricultural value added. Value added can be a proxy for good agricultural land in a country.

Since most of the argument of host countries about ILTs suggests that they are leasing or selling idle lands, we introduced a crude measure of idle land (the reverse of percent cultivated land). Results suggest that as the share of agricultural land in use increases (hence idle land decreases), the incidence of targeting a country decreases 1.126 times. In other words, it is not necessarily the amount of cultivated land that determines targeting behavior, but the amount of unused idle land. All in all, the characteristics of the agricultural sector are prime determinants of being targeted.

5.2. Natural Resources Characteristics

Whether or not the characteristics and condition of natural resources determines the targeting behavior of countries is a relevant question. It is plausible to hypothesize that natural resources tied to the effective operation of agricultural lands can determine interest in a country’s land resources. Two factors are considered: amount of rainfall, as a proxy for water resource abundance; and severely constrained soil fertility. Water and soil are, of course, key elements of productive agricultural areas. Results suggest that rainfall is marginally relevant, while the condition of degraded soil in a country is not. A country with a millimeter better rainfall potential is 1.004 times more likely to be targeted. The fact that water is important, but marginally so may suggest that while water is a consideration, it is a consideration at the margin. This may be perhaps due to the collateral investments in water technologies in large farms that may require less reliance on rain-fed agriculture, which is dependent on the volume of rainfall. It may also be due to the fact that ground water resources may effectively be utilized, thus reducing reliance on rainfalls. However, rainfall profile of a country still remains important.

The condition of the soil at the country level was not a significant factor. One reason for this may be that investors can target fertile pockets of land in the host country, even when there are large areas with degraded soil quality. Another could be the possibility that application of fertilizer and other chemical inputs can mitigate the state of degraded soils.

5.3. Agricultural Trade

Whether or not total agricultural imports and exports of countries encourage or discourage interest in their land is a relevant policy issue. Agricultural trade offers a valuable opportunity to connect local producers with global agricultural markets, potentially enhancing agricultural viability in host countries. Results suggest that net agricultural trade (value of agricultural exports minus imports) is a significant factor in explaining country targeting behavior. In fact, countries with better net agricultural trade are 1.004 times more likely to be targeted than countries that do not, the total effect depending on the level of net surplus. From this finding, it is plausible to extend the notion that access to developing countries’ agricultural products in developed countries will enhance the likelihood of their agricultural land resources being targeted by investors.

5.4. Agricultural Technology and Development

Agricultural technology and agricultural sector development may encourage a host country to utilize much of its agricultural resources, and perhaps be less interested in land investments than would otherwise be the case. To test these hypotheses, three factors are considered: food productivity index; capitalization of agriculture and land equipped for irrigation. Findings suggest that while agricultural capitalization increases the likelihood of the country being targeted (by 1.001 times), land equipped for irrigation actually decreases it (by 1.056). However, the productivity of local agriculture was not a significant factor. These results may suggest a number of things. First, investors may already be targeting where productivity is low, realizing that these provides a tremendous upside for increased productivity by applying needed management, inputs and technology. Second, the fact that greater capitalization of agriculture attracts ILTs suggests an affinity for more modern agriculture where human capital and equipment are present and where other support services exist. Third, the negative coefficient of irrigation again suggests an interest in benefiting from the upside. Investors simply target places where the deployment of irrigation technology can increase productivity.

5.5. Infrastructure Development

Countries in Africa differ in the degree of infrastructure development. Whether or not this disparity has implications for ILTs is tested by incorporating the development of paved roads as an explanatory variable. The statistical insignificance of these variables suggests that investors are not looking for places where infrastructure exists, to the contrary, they may be looking for places where infrastructure investment can make the difference.

5.6. Economic, Social, and Institutional Conditions

Studies on determinants of foreign direct investment flows to Africa often cite the importance of economic, social and institutional factors as relevant determinants (Wheeler and Mody 1992, Thomsen 2005, Asiedu 2005, Naude and Krugell 2007). Whether or not these factors also determine investment in agricultural land resources is an open question. To test the effect of economic and social conditions on country targeting behavior, four factors are considered as proxies: GDP per capita; human development; corruption and non-food productivity. Results indicate that the productivity ofthe non-agricultural sector is not a driving factor in targeting a country. Surprisingly, a country’s corruption record is not statistically significant. The insignificance of corruption challenges one of the concerns typically put for the by opponents of ILTs, suggesting that these deals are not borne out of nor encouraged by corruption. One explanation for this is that since corruption is generally a problem in Africa, marginal differences across countries may not make that much of a difference in terms of where investment on agricultural land resources may go within Africa. Overall, interest in host country land resources seems to be motivated by factors other than non-agricultural sector productivity and corruption record.

However, degree of human development and stage of economic development matter. Countries with better human development are 1.369 times more likely to attract interest in their agricultural land resources than those with poor human development. Human development may signal availability of quality labor pool that can be gainfully employed in modern agricultural production and distribution. The stage of economic development is also relevant. Counties with higher per capita GDP are less likely to attract investment in their land resources. Poor countries are less able to fully utilize their natural resources, including agricultural lands. Therefore, poor countries are more likely to be targeted than African countries with higher per capita GDP.

5.7. Property Rights Protection

Investment in any asset is predicated on the knowledge, or perception, about property rights protection. Countries with poor record on property right issues are less likely to attract investment in their land resources, even with rich agricultural lands. Results confirm this observation. Countries with better property rights protection are 1.091 times more likely to be targeted than countries with poor property rights. Obviously, investors are looking for environments that protect their investments.

5.8. Food Security

One central debate in “land grabbing” discussions is whether or not the state of food security is exacerbated by ILTs. While resolving this debate requires time-series data and causality modeling, association between state of food security and ILTs can be informative in this debate. The finding in this study suggest that countries with food insecurity are likely to be targeted, compared with countries that are relatively food secure. In fact, it is estimated that food insecurity increases the likelihood of ILTs 1.093 times. Food insecurity may push governments to explore alternative avenues to attain long-term food security, including inviting foreign investment in agriculture as a potential solution. Poor countries may also be interested in land lease revenues to augment their hard currency reserves crucial to importing capital goods to support development efforts. Therefore, vulnerability in food security enhances the likelihood of being targeted. This highlights the potential for food insecure countries to structure ILTs and the products of foreign operated farms to address local food security concerns by setting aside some production for domestic consumption.

The role of food aid dependence on land transactions is also evaluated. Food aid may provide a false sense of food security, particularly for countries that have reliably received it for years, but can also signal inability of local producers to meet local demand. Whether or not food aid is disruptive to local producers has been a subject of intense debate in the literature, but the role in land transactions is not sufficiently explored. Findings in this study show a negative relationship, suggesting that countries with strong dependence on food aid (measured by food aid received per capita) are less likely to engage in land transactions. But this relationship is weak, as the likelihood of this happening is close to zero. In other words, like food insecurity, reliance on foreign food aid does not encourage ILTs.

6. CONCLUSION

This paper explores the issue of international land transactions in Africa. Rising global food prices and the increased demand for biofuels have recently spiked speculative and investment interests in agricultural land resources in Africa. While opponents of ILTs have dubbed it “land grabbing” and are proposing mechanisms to monitor and regulate land transactions in Africa, proponents, including investing and host countries, welcome the opening of Africa’s agriculture for foreign direct investment. The limited empirical work explaining, through supported theory, the motivations of investor and host countries in engaging in land transactions have largely limited rational debate about the issue. This paper attempts to close this gap by providing a theoretical explanation of the motivations of parties and empirically explaining the country targeting behavior of investors to better understand the systemic structure of where land deals are likely to occur.

Results from this study suggest that whether or not a country is targeted is predicated on the characteristics of the agricultural sector (in terms of degree of agricultural land potential utilized, agricultural value added and processed agricultural exports), characteristics of natural resources (water and soil conditions), agricultural trade (net export position in agricultural commodities), agricultural technology and development (capitalization and irrigation intensity), economic and social conditions (stage of development and human development), property rights protection and state of food security (degree of malnutrition and aid dependence) are relevant factors that explain the incidence of ILTs.

The policy implications of these findings is that countries that have poor economic and agricultural sector development, and with good land resources, are likely to be interested in foreign investment in their land resources as a solution to their agricultural sector problems. While foreign investment in agriculture can be optimally structured, including conditions outlined in the theoretical section of this paper, the fact that most deals are not structured in ways that meet the agricultural sector challenges of host countries (output retention clause, optimal lease determination, optimal contract longevity, etc) is a cause of concern. This study offers some insights on which countries are likely to be targeted, and how host countries may potentially structure beneficial land deals. As the debate on “land grabbing” intensifies, identifying parameters for beneficial deal structuring can offer alternative framework for land policy related to ILTs.

REFERENCES

Asiedu, E. (2006). Foreign direct investment in Africa: The role of natural resources, market size, government policy, institutions and political stability. World Economy, 29(1), 63-77. doi:10.1111/j.1467-9701.2006.00758.x

Boras, S., & Franco, J. (2010b). From threat to opportunity? Problems with the idea of a code of conduct for land-grabbing. Yale Human Rights and Development Law Journal, 13, 507-523.

Borras, S. M., & Franco, J. (2010a). Towards a broader view of the politics of global land grab: Rethinking land issues, reframing resistance (ICAS Working Paper Series No. 001). Initiatives in Critical Agrarian Studies, Land Deal Politics Initiative and Transnational Institute.

Braun, J., & Meinzen-Dick, R. (2009). Land grabbing by foreign investors in developing countries: Risks and opportunities (IFPRI Policy Brief 13). Washington, DC: International Food Policy Research Institute.

Cotula, L., Vermeulen, S., Leonard, R., & Keeley, J. (2009). Land grab or development opportunity? Agricultural investment and international land deals in Africa. London: IIED/FAO/IFAD.

Daniel, S., & Mittal, A. (2009). The land grab: Rushfor world’s farmland threatens food security for the poor. Oakland, CA: The Oakland Institute.

Deininger, K., Byerlee, E., Lindsay, J., Norton, A., Selod, H., & Stickler, M. (2011). Rising global interest in farmland: Can it yield sustainable and equitable development? Washington, DC: The World Bank. doi:10.1596/978-0-8213-8591-3

Duangklad, P. (2010). Land grabbing and food security of host countries in sub-Saharan African case. (Unpublished M.A. Thesis). Central European University, Budapest, Hungary.

Graham, A., Aubry, S., Junnemann, R., & Suarez, S. M. (2010). The impact of Europe’s policies and practices on African agriculture and food security: Land grab study. Heidelberg, Germany: FoodFirst Information Action Network.

Li, T. M. (2011). Centering labor in the land grab debate. The Journal of Peasant Studies, 38(2), 281-298. doi:10.1080/03066150.2011.559009

Mann, H., & Smaller, C. (2010). Foreign land purchases for agriculture: What impact on sustainable development?. Sustainable Development Innovation Briefs, 8.

McMichael, P. (2011). The food regime in the land grab: Articulating ‘global ecology’ and political economy. Paper presented at the International Conference on Global Land Grabbing. Sussex, UK.

Naude, W. A., & Krugell, W. F. (2007). Investigating geography and institutions as determinants of foreign direct investment in Africa using panel data. Applied Economics, 37, 1223-1233. doi:10.1080/00036840600567686

Robertson, B., & Per, P. A. (2010). Global land acquisition: Neo-colonialism or development opportunity? Food Security, 2, 271-283. doi:10.1007/s12571-010-0068-1

Schutter, O. D. (2011). How not to think of land-grabbing: Three critiques of large-scale investments in farmland. The Journal of Peasant Studies, 38(2), 249-279. doi:10.1080/03066150.2011.559008

Thomsen, S. (2005). Foreign direct investment in Africa: The private sector response to improved governance. Chatham House Briefing Paper, IEP BP 05/06.

Visser, O., & Spoor, M. (2011). Land grabbing in post-Soviet Eurasia: The world’s highest agricultural land reserve at stake. The Journal of Peasant Studies, 38(2), 299-323. doi:10.1080/0 3066150.2011.559010

Wheeler, D., & Moody, A. (1992). International investment decisions: The case of U.S. firms. Journal of International Economics, 33, 57-76. doi:10.1016/0022-1996(92)90050-T

Zoomers, A. (2011). Globalisation and the foreignisation of space: Seven processes driving the current global land grab. The Journal of Peasant Studies, 37(2), 429-447. doi:10.1080/03066151003595325

2.

3.

ENDNOTES

1∙ For example, foreign ownership of US ag

ricultural land has been well documented. Several studies have explored the adequacy or inadequacy of such foreign ownerships (Lapping and Lecko 1983; Dobitz and Kirby 1989; Krupa and Ross 1996). The general consensus is that such acquisitions are not necessarily threats, but are normal aspect of foreign company expression of interest in the best productive resources in order to achieve company growth and other objectives. Other countries where international land ownership has drawn significant attention include Australia, Canada, Brazil, and Belize.

4.

5.

Reasons typically cited in the literature include food security, speculation, increased production capacity, control of resources and long-term investments.

One of the intriguing aspects of ILTs is the involvement of private and corporate financial and investment banking organizations, as well as sovereign wealth funds. A significant percentage of recent land acquisitions have been made by Asian, Gulf region and European-based companies that typically would not make significant investments in Africa, let alone in African farmland. A range of companies have been directly or indirectly involved in ILTs. These include Altima Partners, Renaissance Capital, EKO Asset Management Partners, Pine Street Alternative Asset Management LLC, Emergent Asset Management Ltd, EBG Capital AG, Agland Investment Services, Global Impact Investment Network, and TIAA- CREF. These companies tend to look at these transactions as natural extensions of rational portfolio management strategies and as opportunities for optimizing returns on the investments of company owners and shareholders. Similarly, host countries tend to be in favor of these transactions, obviously since they are participating in them. Indeed, ILT was an important part of the agenda for the 2011 World Bank conference on Land and Poverty. It was immediately followed by a meeting of over 50 stakeholders from various organizations, organized in Washington by the USAID and the Millennium Challenge Corporation.

Considering the existence of strong agency problems in some of the host countries, the issue of corruption is also frequently raised, with the implication that one of the motives for a host country to participate is personal - government representatives engaging in these transactions for personal gains and not in the interest of the people they represent.

6.

7.

Some motives of host countries relate to long-term development of export capacity or capacity to exploit agricultural export potential. The fact that these transactions have involved places with significant food security concerns and places with high levels of capacity to feed themselves also suggest that long-term food security issues are at play. Nevertheless, it suffices to say that a number of factors affect host country’s participation and that the supply side of the market may have argument that typically would not be considered in traditional modeling of the supply side of the land market.

Deininger et al. (2011) included statistical analysis of the factors that lead to the likelihood of being targeted. Some of the factors considered were amount of unused land, yield gap and two measures of governance - investment protection and land tenure security. Results from this study suggest a negative impact of rural land tenure on land acquisition, weak effect of Doing Business rank and that investors with media exposure are more likely to target countries having large cultivable land. The study also empirically examines the factors that increase the chance of a country being targeted. The study considered non-forested non-cultivated suitable land (which positively influences the likelihood of being targeted), yield gap (with negative influence), rural land tenure recognition (with negative influence), and investment protection (with negative influence).

This work was previously published in Econometric Methodsfor Analyzing Economic Development, edited by Peter Č Schaeffer and Eugene Kouassi, pages 111-130, copyright 2014 by Business Science Reference (an imprint of IGI Global).

818