Chapter 42 Racial Differences in Financial Socialization and Financial Behaviors of U.S. College Students

Michael S. Gutter

University of Florida, USA

Zeynep Copur

Hacettepe University, Turkey

Amanda Blanco

University of Florida, USA

ABSTRACT

This chapter focuses on the effect of race on financial socialization and financial behavior of college students.

Data (N = 13,845) were collected from current college students age 18 and over via an online survey throughout the United States during spring and fall of 2008. Results from means comparisons showed significant differences on the financial socialization between Black and White college students. Logistic regression results suggest important relationship exist between race and financial behaviors. Black students were less likely to save and more likely to engage in risky credit card behavior than White students after controlling for the effects of all other variables.INTRODUCTION

The capacity to manage personal finances has become increasingly important, particularly for college students. Students are now leaving schools without the ability to make critical financial decisions affecting their future lives and thus, are in

danger of beginning a downward financial spiral of debt. This is debt that they will not easily repay while in college or even after they have gained fulltime employment in the workplace (Henry, Weber, & Yarbrough, 2001; Grable & Joo, 2006). Henry et al. (2001) revealed that 68% of college students rarely budgeted or did not budget at all. In a follow up study, Joo et al. (2003) found that only half of the students paid their credit card bills in full each month and 40% did not know the annual percentage rate of their credit cards. Some researchers concluded that Black students with low income were more likely to engage in responsible financial management behaviors than their White counterparts (e.g. Perry & Morris, 2005). Lyons’ (2004) study showed racial differences with students who are having difficulty making credit card payments were more likely to be Black, and/or Hispanic.

Her study also found that Black students were also significantly more likely to have credit card balances of $ 1000 or more and not to pay their balances in full each month. Grable and Joo (2006) found that racial differences between Black and White students on financial behaviors; Where Blacks held more credit card debt than others and credit card debt was positively related to negative financial behaviors. Researchers have also speculated that White and Black families save differently and that these differences have important implications for wealth inequality (Brimmer, 1988; Parcel, 1982). Burlew, Banks, McAdoo, and Azibo (1992) suggested that a common goal among Blacks is to have a standard of living comparable to their peers, both Whites and Blacks. This goal might lead to a lower emphasis on savings (Yao, Gutter, & Hanna, 2005).DOI: 10.4018∕978-1-4666-6268-1.ch042

.

An analysis of the 2004 Survey of Consumer Finances showed that Black households were significantly less likely to have spent less than their income when compared to Whites. Based on an analysis of the 2004 Survey of Consumer Finances, with 41 % of Black households, and 60% of White households reporting that they spent less than they had in income (Bucks, Kennickell, & Moore,2006), and Black families saw a 24.1 percent decline in their median net worth from 2004 to 2007 (Bucks et al., 2009). Also Black households were significantly more likely than White households to have missed or been late on a loan payment (40% versus 18%). Controlling for income and other factors, Black households had higher predicted delinquency rates than White households (Bucks et al. 2009). What is less well known is how financial socialization differs based on racial background. Thus, the current study aims exposure to potential differences in financial socialization between Black and White college students and the effects that these differences may have on financial behaviors (budgeting, saving, and risky credit card usage).This research is important, in that it is vital for Blacks and Whites to gain financial knowledge.

A few papers examine the link between knowledge and behavior and authors found strong links between knowledge and behavior (e.g., Borden, Lee, Serido, & Collins, 2008; Hilgert, Hogarth, & Beverly, 2003; Robb, 2011). Both Black and White college students will eventually be responsible for their own finances. If Blacks are missing out on early positive financial socialization opportunities, they may be negatively affected later in life by financial issues, in which they have little knowledge or tools to resolve. By finding out whether or not individuals are socialized differently in the financial realm, we can determine next steps in closing this potential race gap.THEORETICAL FRAMEWORK

Socialization is often viewed as a social process by which norms, attitudes, motivations, and behaviors are transmitted from specific sources (commonly known as socialization agents) to the learner (Brim, 1966; Hira, 1997; McLeod &O’Keefe, 1972; McNeal, 1987; Moschis, 1981). Children who emulate their parents’ behavior through observations provide a good example of social learning (Bandura, 1977; Grossbart, Carlson, & Walsh, 1991; Maccoby, 1992; Mascarenhas & Higby, 1993; Moschis & Churchill, 1978). Based on social learning theory, consumer socialization research suggests that a great deal of consumer behavior, such as spending behavior among adults, is learned during the adolescent years through the influence of socialization agents such as parents, family members, and other influential individuals and can be taught from generation to generation (Churchill & Moschis, 1979; Moschis & Moore, 1984; Valence, d’Astous, & Fourtier, 1988). Consumer socialization theory explores the effects of both social-structural constraints (the social variables, such as social class, gender, and age, that can have an effect in socialization by influencing learning processes) and socialization agents (that is, parents, peers, school, and/ or television,) on the mental and behavioral outcomes (e.g., the process through which parents teach consumer skills to children) (Moschis & Churchill, 1978).

Several previous studies have revealed that parents’ intentional instruction and reinforcing activities can directly and indirectly impact their children’s financial knowledge and behavior. Parents appear to play an important role in the consumer socialization of their offspring, and they are instrumental in teaching them the rational aspects of consumption (Danes, 1994; Drentea & Lavrakas, 2000; Hayhoe et al., 2000; Lyons, Scherpf, & Roberts, 2006; Moschis, 1985).The cultural-difference version of the socialization hypothesis states that Blacks socialize their children differently because they have a different culture which requires social and other competencies different from those valued in the white culture (Ogbu, 1979; Rong & Brown, 2002). Race and ethnicity is representative of the shared history and socialization of a group and, thus, should impact financial preferences. Differences in socialization among different racial and ethnic groups might also influence preferences such as budgeting or saving behavior (Dilworth-Anderson, Burton, & Johnson, 1993). In particular, a history of less exposure to financial markets and financial information, greater labor force participation instability (Hsueh & Tienda, 1996), discrimination, having lower levels of wealth (Kennickell, Starr-Mcluer, & Surette, 2000; Aizcorbe et al., 2003) and differences in family composition are likely to make Blacks are less likely to engage in positive financial behaviors (Dilworth-Anderson et al., 2005). Therefore, it is expected that Whites are more likely to engage in positive financial behaviors than Blacks. Some differences might be related to other factors such as gender, income, and debt, but if significant differences remain after controlling for these factors in multivariate analyses, the financial socialization explanation presents a plausible alternative. Thus, this research aims to look at differences in financial socialization between Black and White college students and the effects that these differences have on financial behaviors, such as budgeting and saving.

In the current study, financial socialization is represented by financial social learning opportunities such as discussing financial matters with parents and peers; or observing their financial behaviors.Research Questions and Hypotheses

According to previous research (e.g. Chen & Volpe, 1998) we see that various behavior differences in Blacks and Whites may be partially affected by differences in socialization. There is evidence that race differences exist in various areas of financial behavior (e.g. Lyons, 2004). It stands to reason that if people are socialized differently based on race for some behaviors, that they may also be socialized differently for financial behaviors. This study seeks to expand that research to the area of financial socialization and financial behaviors, with the following hypotheses:

1. Exposure to financial social learning opportunities will differ by race of college students.

2. There is a relationship between race and financial behaviors when controlling for social learning opportunities, gender, marital status, income, amount of debt, and financial education.

METHOD

Data and Sample

Data for this study was collected as part of a larger study on the impact of financial education on financial behaviors during the spring and fall semesters of 2008. A stratified random sampling technique based on state policies toward financial education was utilized. Six policy categories were determined using the 2004 National Council on Economic Education report. States were randomly selected from each of the categories, with the target campuses being large state universities. The sampling pool consisted of college students, age 18 and over, from 15 public universities across the United States.

In total, emails were sent out to 172,412 students, with 16,876 students responding to the survey. Students who were not educated in the United States, who were homeschooled, who received a GED, or who did not indicate their state of high school attendance or whether they are Hispanic, Asian, and other ethnicity were removed from the sample, yielding a final sample of 13,845 students (5.3% Blacks, 94.7%Whites).

The sample profile is fairly typical, with an average age of 21.3 years. In addition, most students were female (65.6%), most were White (94.7%), and most were unmarried (85.5%).Measurement of Variables

Dependent Variables

Financial Behaviors: This includes budgeting, saving and risky credit usage behaviors. Budgeting was measured with the question, “Do you currently use a system to manage expenses and avoid overspending?” Saving was measured with the question, “Are you currently depositing/invest- ing money on a regular basis into some sort of account (includes employer plans, mutual funds, individual retirement account (IRA), savings, CDs)?” Responses included yes or no. Credit usage behaviors are based on a score of risky credit card behaviors. Students were asked “how frequently in the past year they had done the following: maxed out their credit, been delinquent, and carried a balance.” Responses included 0, 1-2, 3-5, 6 or more, and N/A represent if students doesn’t have credit card. For the analyses to each of the risky credit card behavior 1-2, 3-5, 6 or more were combined as 1 which indicated that students have engaged risky credit card behavior and 0 indicated that students have not engaged risky credit card behavior. Then, for the ordinal logistic regression analysis three risky credit card behaviors (“max out,” make late payments, and do not pay off credit card balance) combined as 0, (no risky credit card behavior) 1 (engaged one risky credit card behavior), 2 (engaged two risky credit card behavior), and 3 (engaged three risky credit card behavior) with more frequent behaviors indicating higher credit risk scores.

Independent Variables

Demographic Variables: The current study involved the following college students’ demographic variables: gender, race, and marital status.

Financial Variables: In this research, financial variables were measured using monthly income, amount of debt, and number of credit cards.

Financial Education: Financial education was measured with the question, “Were you taught about personal finances in high school?” and “Have you ever taken a course, program, or seminar on personal finance issues in your community, religious institution, or 4H-in other words not through school?” Responses were categorical and included yes or no.

Financial Social Learning Opportunities: The financial social learning opportunities score was a composite measure based on four dimensions: discussions with parents, discussions with peers, observing parents and observing peers. The score utilized responses to eight items representing these four dimensions. Scores for each dimension ranged from 8 to 40. This measure is based on the work of Gutter and Garrison (2008). Students were asked how frequently in the past five years they had discussed the following with their parents and friends or other students: “managing expenses and avoiding over spending,” “checking their credit report,” “paying bills on time,” “saving and investing,” “working with a mainstream financial institution,” “buying and maintaining health insurance,” “auto insurance” and “renters’ insurance.” A similar set of questions was asked but focusing on observations of the same behaviors. The student answered by using a 5 point scale from 1= never to 5= often. In order to test the reliability of the measure, Cronbach’s Alpha was selected. Cronbach’s Alpha internal consistency reliability was calculated to be.86 for both discussion with parents and discussion with friends. The inter-item reliability was high for both observing parents (α=.87) and observing friends (α=.86).

Analyses

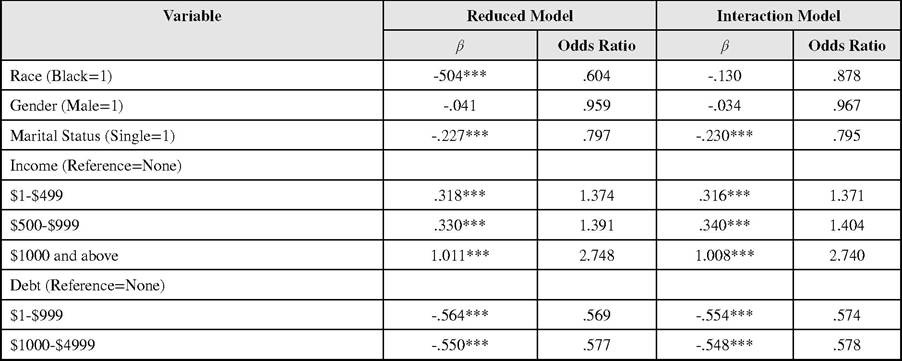

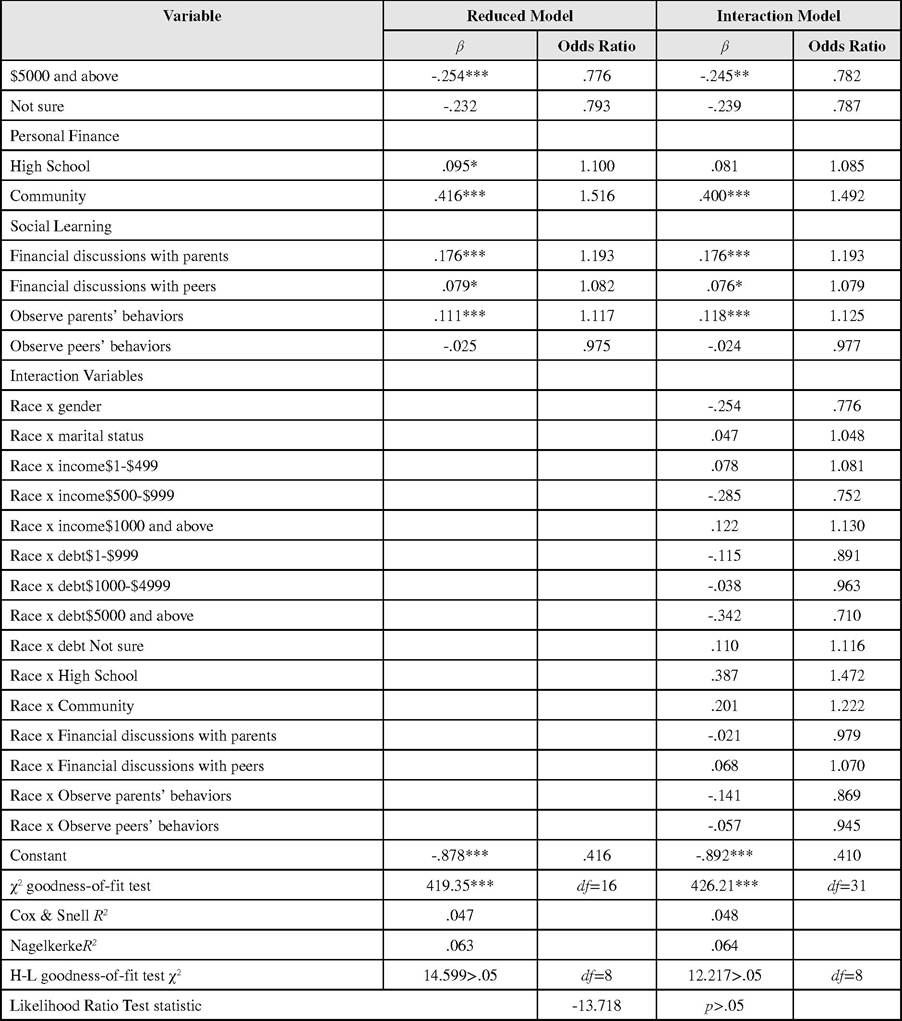

Preliminary exploration of the research questions included simple bivariate comparisons employing cross-tabulation tables and chi-square test to examine whether or not the profile of the sample, financial socialization, risky credit usage behaviors, and financial behaviors differed by race. For social learning opportunities, each of the four social learning opportunities scores was compared by race via independent sample t-test. The results of the t-test indicate overall significant race differences for each form of financial socialization. This was followed by binary logistic regression for budgeting, saving and ordinal logistic regression for risky credit card usage behavior. The dependent variables included using a budget, saving, and students’ risky credit usage behaviors. The purpose of this analysis was to determine the relationship of race on varying financial behaviors, controlling for financial social learning opportunities, gender, marital status, income, debt and prior financial education. The effect of race on varying risky credit card usage behavior also controlled for credit card number. Specifically, we used logistic regression equations to examine main effects and interaction models. Main effects models included race, gender, marital status, income, debt and prior financial education as predictors of financial behaviors and number of credit card as predictor of risky credit card usage. Interaction models added race by sample characteristics product terms (e.g., RaceXGender) to our main effects model. Interaction analyses addressed whether the effects of college students characteristics on financial behaviors differed between Blacks and Whites. The interaction model and the reduced model were compared to determine whether factors improved the model. This was tested using a likelihood ratio test. The test was significant and the reduced model was rejected in favor of the full (interaction) model.

RESULTS

Comparing Students’ Profile by Race

The sample was composed of 94.7% Whites and 5.3% Blacks. Many of the students in both samples reported having a course in personal finance (41.1% of Blacks, 38.8% of Whites) in high school (p>.05). Black students were significantly more likely to have a personal finance education (22.6%) in their communities compared to White students (8.5%) (pbgcolor=white>.902