Chapter 41 Investment Attractiveness of Visegrad Group Countries: Comparative Analysis

Tomasz Dorozynski

University of Lodz, Poland

Anetta Kuna-Marszatek

University of Lodz, Poland

ABSTRACT

The aims of this chapter are to evaluate the main determinants of the inflow of FDI into selected countries of CEE and to examine the volume, dynamics, and structure of FDI inflow into these countries.

Due to certain similarities, the authors focus the analysis on four countries: Poland, the Czech Republic, Hungary, and Slovakia. The reasons are geographic proximity, political, economic, and cultural similarities, as well as shared experiences of economic transformation. This chapter focuses on matters pertaining to foreign direct investment, mostly on the reasons motivating FDI inflow in light of selected studies and theories. The authors also provide characteristics of the dynamics and structure of FDI inflow into the V4 countries. The final part of the chapter compares investment attractiveness, the system of incentives, and identifies barriers facing investors in the analyzed countries.INTRODUCTION

One of the main features of the modern economy is the internationalization of economic operations, which is connected with globalization and regionalization, This consists mainly of establishing and developing transnational links among companies. These links may take various forms, starting from simple ones (e.g. exports) up to the much more advanced channels of international capital flows.

DOI: 10.4018/978-1-4666-6268-1.ch041

One of the ways to expand into a foreign market is foreign direct investment (Stawicka, 2007, p. 7).

As mentioned, foreign direct investment (FDI) is linked to regionalization and globalization, particularly when it comes to the selection of investment localization. Regionalization may be considered at two levels. Firstly, there is international economic integration, i.e. the establishing of regional integration groupings (regionalization of the world economy).

Secondly, there is also the currently observed phenomenon of increased importance of regions and their emergence as separate structures (regionalization of national economies). Globalization, in the context of economic development, may lead, on the one hand, to differentiated effects and marginalization of some areas and, on the other hand, to the increased importance of a territory and location as a source of competitive advantage. Thus, we are dealing with two apparently contradictory phenomena, whereby globalization increases the importance of a territory at the regional and local level. In the literature this is referred to as glocalization (Robertson, 1994; Svensson, 2001; Swyngedouw, 2004; Pietrzyk, 2004)..

International capital flows, also in the form of FDI, are among the main factors conducive to globalization. At the same time, investors are seeking locations that would meet their specific expectations and boost business development. The countries of Central and Eastern Europe (CEE), when implementing systemic transformation at the beginning of the 1990s and opening up their markets for foreign investors, also had to face these new trends in the global economy. Since 1991 these countries are also members of the Visegrad Group (V4), established with the initial objective to support the aspirations of Poland, Czechoslovakia (later the Czech Republic and Slovakia) and Hungary on their path to EU accession. After 2004, in accordance with its Declaration, the V4 has aimed at optimum cooperation with all countries, in particular with its neighbouring countries, and its ultimate goal is the development of democracy in all parts of Europe. Moreover, its members support the building of European security based on cooperation and coordination within existing European and Transatlantic institutions and structures. These countries are also connected by their cooperation within the structures of the European Union (EU), NATO, OECD, and WTO.

The countries of Central and Eastern Europe by offering relatively good location and human resources at relatively low operational cost, and by investing in infrastructure, they became attractive investment locations.

For over 20 years Central and Eastern Europe in particular the Visegrad Group countries, has become an ever more attractive destination for long-term capital investment. According to the assessment of Ernst & Young, Central and Eastern Europe is the third the most interesting investment region globally (Ernst & Young’s, 2012). The reasons behind this are not only systemic transformation and the opening up of their economies to foreign investors, but also general security, related to membership in international organizations and being a part of the European single market. The countries’ EU accession in 2004 particularly boosted investors’ interest in the region, providing the guarantee of stability and relatively high economic and legal predictability.As a corollary of the V4 countries’ EU membership, entrepreneurs achieved access to numerous State aid programs. They may expect better economic operational conditions with the support of the EU structural funds, the Cohesion Fund, as well as other external sources of funding, such as, e.g. the Norwegian Financial Mechanism, EEA Financial Mechanism, and bilateral cooperation programs with Switzerland. Thus, the Visegrad Group countries offer investors benefits connected with economic and political security and the access to a large and affluent market at relatively low business operational costs, plus all sorts of allowances and preferences (Ministry of Economy, 2012).

Contrary to common opinion, however, the assessment of FDI inflow to countries and regions is not without ambiguity. For this reason, in this Chapter we try to illustrate the overall effect of FDI inflow to the countries of Central and Eastern Europe, using the example of Visegrad Group members, i.e. Poland, the Czech Republic, Hungary, and Slovakia. Besides the overview of selected theoretical aspects and empirical studies, the Chapter focuses on the dynamics and structure of FDI inflow to a region and on the assessment of the investment attractiveness of the analyzed area.

BACKGROUND: FDI IN THEORY AND EMPIRICAL STUDIES

Definition and Types of FDI

Capital migration in the form of FDI is one of the most important consequences of globalization and, at the same time, it is a catalyst for the internationalization of manufacturing, services, and trade, and a leading source of technology and know-how. Besides, among the various sources of foreign capital, FDI is regarded as the most beneficial and the safest type of international capital flows and a way of financing restructuring and development in the host countries. FDI inflow results not only in the transfer of financial resources but it also brings concrete investment goods. Under a favourable combination of systemic and structural factors, it is the most efficient way of receiving foreign capital and a vital factor for accelerating growth. Its role is most clearly visible in those countries which underwent systemic transformations, including the countries of Central and Eastern Europe, which for over two decades have been trying to generate a good business climate for foreign investors. Thus, investors may help a country (region) improve its image in international business circles, which, in turn, impacts its ability to compete for more investors and to generate growth. This is why FDI is so valuable for areas competing within Regional Trade Agreements (RTAs). So the first question naturally is: What is FDI?

According to the OECD definition, foreign direct investment “reflects the objective of establishing a lasting interest by a resident enterprise in one economy (direct investor) in an enterprise (direct investment enterprise) that is resident in an economy other than that of the direct investor” (OECD, 2008, p. 48). The process may take the form of (Swierkocki, 2004, p. 93):

1. Acquisition of shares giving the right to manage a business,

2. Acquisition of all of the business,

3. Starting a business from scratch, including the purchase of real estate (known as a greenfield investment).

When starting a business from scratch a common business entity employed is a joint venture. This may involve the establishment of a new company in cooperation with a domestic operator. This solution is beneficial to both sides. The foreign partner profits from the domestic operator’s better knowledge of the target market and its institutional and legal environment. The domestic operator, in turn, may count on subsidies and the transfer of knowledge, technology and management methodology from the foreign partner.

Acquisitions include brownfield investments. They mostly consist of modernization of existing companies. The changes usually relate to production organization, assortment, machinery, and staff. Moreover, e.g. in Poland, foreign investors may open their branches based on the principle of reciprocity. In such instances, an entrepreneur may pursue economic activity only within the scope specified for its parent company (Official Journal of The Republic of Poland, 2013, art. 85.1-86).

Foreign entrepreneurs may also establish their representations abroad. However, the scope of their activities may cover only advertising and promotion of a foreign business (Official Journal of the Republic of Poland, 2013, art. 93-94).

A transaction in a host country is considered a FDI when it entails investment in a company’s equity. FDI also covers subsequent capital flows between a parent company and the direct investment enterprise, such as reinvesting profits, net purchases of shares in the company and/or debt instruments by the direct investor, and internal borrowings from the direct investor. In addition, the involvement of a foreign investor in the domestic company may consist of membership in the Supervisory Board, involvement in management, in-kind transactions between companies, replacement of management staff, making knowledge and technology available, and granting long-term loans on terms more favourable terms than those offered on the market. The usual threshold that allows a particular investment to be classified as FDI is ownership by the foreign investor of at least 10% of stock or shares of the direct investment enterprise (Klysik-Uryszek, 2011, pp.

16-17; OECD, 2008).Hence FDI is a much more complex phenomenon that just capital flow itself. Establishing a multinational business entails, e.g., opening branches abroad, technology transfer, production organization, and ensuring appropriate labour resources, including management staff. FDI should be distinguished from Foreign portfolio investments, which are capital flows that consist of the acquisition of foreign financial instruments, e.g. stock, bonds, deposits by residents of another country etc.

As already indicated, the assessment of the significance of FDI to the global economy has been the subject of many studies and analyses. Their conclusions, depending on internal and external circumstances, are not without ambiguity. There is one point, however, where all the authors agree: FDI plays an important role (positive or negative) in the global economy. The importance of an investment may be measured by the size of flows, i.e. with the value of an investment in subsequent years, and by their overall value, i.e. the sum of amounts cumulated in a specific period (Swierkocki, 2004, p. 93).

Motives and Determinants of FDI Inflow to a Country (Region)

In recent decades, the development of economic activity of multinational companies has prompted a great deal of research concerning the motivation behind the inflow of foreign direct investment. FDI is considered one ofthe most important stimulants of growth, which also provides support to an economy in times of stagnation. Thus studying foreign investors' motivations may be especially useful for public administration officials. A rich review ofthe theory and empirical studies devoted to reasons behind FDI inflow can be found in, e.g., Assuncao, Forte, Teixeira (2011).

Numerous theories of the 1960s sought to explain the determinants of FDI inflow. Some of them were based on microeconomic factors, such as organizational aspects, cost reduction, and economies of scale. Others related to macroeconomics, e.g., availability and allocation of resources, barriers to entry, political stability, market size, etc. (Dunning, Lundan 2008; Faeth, 2009).

The first studies of the premises for FDI, based on models by Heckscher-Ohlin (1933), MacDougall (1960) and Kemp (1964), referred to the benefits from operation on a foreign market resulting from e.g., lower cost of labour and reduced transaction risk. The theory of internalization was initiated by Buckley and Casson, who pointed out that companies decide to invest abroad when transaction costs are higher than the costs of internalization in the host country (Faeth, 2009; Assuncao, Forte, Teixeira, 2011).

However, the most comprehensive approach was proposed by Dunning (eclectic theory/OLI paradigm), who linked internalization with traditional trade theory and classified the benefits attained by companies as a result of the internationalization of economic operations. Undoubtedly, Dunning’s main contribution to the theory of economics is the listing of various theories and concepts as well as variables relating to ownership, location and internalization which determine the international activities of companies (Dunning, Lundan, 2008). Factors which belong to the OLI model are most often analyzed as FDI location determinants: infrastructure, human capital, economic stability, and production costs. Also institutional factors are taken into account (corruption, political stability, quality of public institutions, and tax and financial incentives) and factors resulting from the new trade theory (market size, market growth, openness of the economy and factor endowments) (Assuncao, Forte, Teixeira, 2011).

In fact, entrepreneurs, when making decisions on foreign investment, are guided by an array of factors. Obviously, above all, they wish to improve the economic performance of their companies and to strengthen their position on the international market. This means economic factors are the main reasons for FDI. Specific location is selected based mostly on the domestic market potential (possibly including the potential of neighbouring markets or of the market of an integration group as well) and on demand-specific factors. Investors analyze e.g. the size and structure of a particular market, per capita income, consumer preferences, and soft and hard infrastructure. The growth rate of the host economy is also relevant - Mottaleb (2007) and Busse and Hefeker (2007) list it as an important determinant of FDI inflow. Market size is especially important for the so-called market-seeking FDI undertaken with a view to gain access to the local market and to circumvent barriers protecting the market.

Not all of FDI, however, is motivated by the wish to enter a particular market. Direct investors also want to find a location which will ensure access to specific resources unavailable in their countries (regions) of origin. These resources may also be cheaper or better in the host country. Here we have in mind mainly raw materials, labour, and production capacity. Often investors want to improve the international competitiveness of their companies, and sales on the domestic market are less of a motivation.

Human resources and social capital, R&D potential, innovation, institutional framework, territorial forms of production organization (clusters), and other intangible assets are also important determinants of FDI inflow. These are typical of better developed areas and may be attractive for more advanced types of economic operations. Some of them may be generated or supported by national, regional and local authorities, which can influence the investment attractiveness of an area in question.

The wish to rationalize costs by consolidating production, benefiting from more favourable regulations (e.g. tax and labour laws) and gaining access to a bigger market of a regional integration group are also among the reasons for a foreign investment in a particular location (Kiysik-Uryszek, 2011, pp. 18-19). Bevan and Estrin (2004) demonstrated that the mere prospect of EU accession of the countries of Central and Eastern Europe was an important determinant of FDI inflow. Similar conclusions were reached by Egger and Pfaffermayr (2002), who showed that the prospects for changes in an integration group, be it in qualitative terms (e.g., intensification of integration) or resulting from the accession of new countries, impacts FDI inflow.

Foreign investors are also motivated by legal and institutional premises, such as (Klysik- Uryszek, 2011, pp. 20-21):

1. Economic, political and social stability, security, and predictability of legal and administrative regulations;

2. Tax policy, State aid, including investment incentives and allowances;

3. Regulations concerning market entry, operations, and protection of competition;

4. Efficiency of state administration and institutions involved in the business environment (the so-called ‘business climate’).

Depending on the type of activity pursued, infrastructure in the region may also be a determinant for a location decision. Investors may consider various types of infrastructure: telecommunication, transport, but also social infrastructure including health, education, sports and leisure, or culture. All of these are elements of the overall assessment of the investment climate of a country (region), which serves as the basis for the location decision for an FDI and its future continuation.

The motives most often listed in the literature are confirmed in empirical studies conducted, inter alia, in the countries of the Visegrad Group. One example may be the 2010 direct study of a sample of companies with foreign capital conducted in Poland at the regional level (Dorozynski, Urbaniak, 2011). The sample studied was representative - it included companies of different sizes, with differentiated involvement of foreign capital, types of operations and geographical structure of sales. The results to a large extent confirmed theoretical considerations, but also have a practical dimension as they identify issues to be taken care of by the public administration responsible for the policy vis-a-vis foreign investors.

According to the foreign investors surveyed, the most important motives for FDI location in Poland were connected with the availability of labour with appropriate skills. Other important reasons for FDI location included low costs and wages and the availability of the required qualifications. Favourable geographical location also strongly motivated investors, who expected income from sales on the internal market, interpreted here as also encompassing the EU market. The most discouraging factors were poor transport and social infrastructure and red tape, i.e. the protracted administrative procedures and incompetence of administration officials. However, the problems were not so big as to cause foreign investors to resign from their location decisions.

A review of the literature on the motives for FDI location shows it depends on many factors connected with the particular circumstances of the investing enterprises and the development level of the host country. In most cases, however, resource- and market-related determinants prevail. The former are connected with the wish to find better and cheaper production factors; the latter are focused on increasing or maintaining sales.

Benefits and Costs of FDI in the Host Country

As stated earlier, the impact of FDI on the host country is ambiguous. The economic changes implicated by the entry of foreign economic operators are of interest to many market actors and economists dealing with developmental subjects. FDI consequences for the economy can be observed at various levels. It is often the case that positive changes in one or more areas are accompanied by unfavourable changes in other areas. Generally, however, it is assumed that FDI-related benefits offset the undesirable effects and provide a positive impulse to the economy of the country and region in which they are located. However, there are some of studies which question this thesis.

Due to the complexity of FDI’s effects on the economy, we usually take into account only some key areas over time - those most sensitive to the impact exerted by investors and the best reflecting the economic situation of regions where FDI is located (Kiysik-Uryszek, 2010, pp. 79-80). In most cases the effects are changes in production, GDP (Fortanier, 2007), the productivity of production factors (Haskel, Pereira & Slaughter, 2007), quantitative and qualitative changes on the labour market, changes in competition, innovation, and dissemination of knowledge and technological progress (Kathuria, 2000).

Many works provide examples confirming that FDI inflow acts as an impulse for regional development. Since Keynes it has been known that business cycles depend on the changes in investment rates and in the capital intensity of investment (Harrod, 1939; Domar, 1946). This thesis is the starting point for models where growth is a variable, dependent on increased capital supply. According to Rostow (1971), author of the idea of economic convergence, countries with insufficient capital resources may make their growth more dynamic by attracting foreign direct investment. These theories remain up-to-date. The key change which occurred since they were put forward is that at present global investors are not only American, Japanese and West European holdings, but also companies from Arab and Asian countries, which were mostly established as a result of redeployment of the production equipment of huge corporations.

Theories of economic development provided the background for concepts linking FDI inflow with economic development. Japanese economists were particularly committed to the subject and made several attempts to explain it, e.g. Ozawa, Fukuchi, Oguchi, Yoon, etc. (Nytko, 2009). These models are similar, yet only Ozawa’s model of economic development stages was broadly disseminated throughout the world (Ozawa, 1992). Based on theories of economics and the experiences of Asian countries, in particular Japan, the countries of South-East Asia and Latin America, Ozawa observed that they developed successfully by opening up their economies to the external world. That contributed to the creation of a favourable climate for multinational corporations to transfer their operations to these countries, allowing local companies to absorb modern management, production and marketing solutions, all of which taken together helped modernize their economies. Thus, the general conclusion may be that FDI development changes the structure of the economy, with daughter companies supporting the emergence of comparative advantages in international trade and impacting on ownership advantages of local companies, as a result of which they may operate on foreign markets. The perspective of an improved position on international markets for the less developed countries, created by innovations flowing with and from FDI, is also demonstrated by Akamatsu (1962) in his “flying geese” model.

A large portion of the studies demonstrating the impact of FDI on the host country focus on the analysis of developing countries (Aitken & Harrison, 1999; Nunnenkamp, 2002; Sumner, 2005), mainly the so-called emerging markets (Whitman, 1999; Report of the Working Group of the Capital Markets Consultative Group, 2003; Zhang, Li, Li & Zhou, 2010; Globerman, Shapiro&Tang, 2004; Hailu, 2010). There are much fewer studies devoted to the highly developed countries (Lipsey, 2000). As most of them point to positive effects of FDI inflow into economies and regions, many countries offer attractive conditions to foreign investment, treating it as a transfer medium for scientific and technological progress and an economic development factor. This is confirmed by the examples of South Korea, Taiwan, Singapore, and Malaysia. The positive effects of FDI for the economy of India has been described by Marwah & Klein (1998), and similar results were documented for China (Li, Liu & Rebelo, 1998) and Singapore (Lim & McAleer, 2002).

While the results of some studies, e.g., by Aitken & Harrison (1999) and Konings (2009) point out neutral or negative effects of FDI on the host country’s economy, according to Gorg & Greenway (2004) this is due to the fact that the positive effects of an investment are noticeable in the long-run and may not be captured in short-term analyses (which dominate in literature). Besides, multinational corporations may deliberately hide benefits of their investment from local competitors. It is also worth mentioning that the positive impact of FDI may be visible only in selected industries and “occur not horizontally (intra-industry) but vertically through relationships that are missed in conventional spillover studies” (Gorg & Greenway, 2004, p. 180).

The level and dynamics of GDP are often used as measures of FDI’s impact upon a given economy. Studies based on econometric models usually highlight the positive effects of FDI inflow when it comes to a host country’s GDP, independent of its development stage. In the work by Roy & Van Der Berg (2006) such effects are presented using the example of the U.S. economy. Analyses for countries of East Asia were conducted e.g. by Baharumshah & Thanoon (2006), for Malaysia - Karimi and Yusop (2009), and for India and China by Agrawal & Khan (2011). FDI promotes economic growth, but the scale of benefits additionally depends on other factors, e.g. trade policy regulations, workforce qualifications, and absorptive capabilities. Horizontal studies by Choe (2003) on a sample of 80 countries representing different development levels (e.g., Japan, countries of Western Europe, Africa, and Latin America) also demonstrate the influence of economic growth on attracting further FDI.

FDI also impacts the labour market, a phenomenon which has also been widely studied.1 Usually changes in the size of employment, wages, and “quality” of jobs are analyzed in this context. According to Cieslik (2003), the quantitative effects of FDI inflow depend on the structure and flexibility of the labour market. On one hand, foreign companies create new jobs but, on the other hand, they restrict the employment in the domestic sector by competing for access to capital with local operators. When wages are rigid and foreign companies invest in production which is more capital-intensive than the local one, financing it with domestic capital, employment in the host economy may decline. When FDI is financed completely with foreign capital or brings with it greenfield investments, employment may increase.

In the opinion of Klysik-Uryszek (2010), the effects of FDI inflow for the labour market in the host economy may be simultaneously positive and negative, and they materialize at three levels: quantitative, qualitative, and location-specific. The first level means e.g. increased net capital, which creates new jobs in local cooperating companies, but may push domestic competitors out of the market. Qualitative effects may mean higher wages and improved productivity resulting from the applied technology and better work organization, but may also bring with it the implementation of undesired employment practices (longer working hours, restrictions vis-a-vis trade union membership, etc.). Location-specific effects (of a regional dimension) may lead to the creation of new and better jobs (generating more value added) in regions of high unemployment, or it may contribute to the further concentration of economic activity in urban areas, which deepens regional imbalances (Klysik-Uryszek, 2010, p. 85).

There are studies in the literature showing that FDI raises the demand for skills in the host country. This means that local workers, prior to gaining employment in a multinational company, must participate in additional, costly training, unless they can take advantage of special training offered by corporations. These processes increase the resources of highly qualified workforce on the local market. Confirmation can be found in studies by Feenstra & Hanson (1997), who argue that U. S. FDI into Mexico contributed to rising Mexican demand for higher-skilled workers across both regions and industries. However, studies by Blonigen & Slaughter (2001) do not confirm the existence of a relationship between skill upgrading within

U.S. industries and either outward or inward FDI. Surely, however, FDI may result in skills upgrading on the local market, with domestic companies having to compete with the foreign companies, both in terms of knowledge and attracting skilled labour. According to Aitken, Harrison & Lipsey (1996) this provides an impulse to local companies to improve management efficiency and human resource quality, while knowledge transferred by workers facilitates reproducing organizational and management solutions, as well as imitating technologies and procedures of market leaders.

Some researchers are trying to prove that the presence of multinational corporations where employees receive higher wages may raise the wage rate in the domestic economy. Aitken, Harrison & Lipsey (1996) analyzed FDI’s impact on wages in domestic firms in Mexico, Venezuela and the US. They detected a positive impact of FDI on wages in domestic firms in the US, but in the remaining two countries the impact was negative,

i. e. the increasing presence of FDI in Venezuela and Mexico led to a reduction in wages paid by domestic firms. Girma, Greenaway & Wakelin (2001) studied the same effect with respect to the UK manufacturing sector, but they could not confirm that FDI impacts domestic wages in any way.

FDI may also have differing impacts on the productivity of domestic firms. A positive influence is due to the fact that skilled workforce, trained in corporations, may later decide to start their own businesses (Fosfuri, Motta & Ronde, 2001). Besides, foreign corporations may create demand for local inputs, increasing the specialization and efficiency of upstream and downstream activities and generating positive externalities for local industries (Markusen & Venables, 1999). On the other hand, the presence of multinational companies may adversely affect the productivity of local companies, which is especially visible in the short-term, or it may have no influence at all (Gorg & Greenaway, 2004).

Corporations may also monopolize local markets and draw demand away from domestic firms, causing them to cut production and reduce their efficiency (Aitken & Harrison 1999). Moreover, they may replace local suppliers with foreign ones, and thus negatively impact the regional economy (Lall 1978). Very interesting conclusions can be found in Siotis (1999). He reveals that FDI may be initiated by a company without any particular skills, in the hope of acquiring valuable skills from local firms. Effects of penetration may thus be absorbed not only by FDI firms, but also by the parent company in the country of origin. From the point of view of local firms, such FDI may be harmful as they capture competitive advantages.

Along with the flow of capital, foreign companies transfer technology by selling licenses, patents or technological solutions, and offering technical assistance, education or knowledge. Modern studies focus not only on the effects of technology transfer but also on its reasons and diffusion channels between economic entities. Technology transfer, its diffusion and promotion of innovation are definitely among the most desired benefits of FDI. Kokko (1992) identifies the following ways of technology transfer to the host country:

1. Demonstration effect - imitation;

2. Competition effect;

3. Effect of international relationships;

4. Effect of learning (subcontractors).

Multinational corporations are usually more often and more willingly invest in R&D than domestic entities. OECD data show that R&D outlays in corporations are substantial, even when compared with aggregate R&D expenditures of countries (OECD 2010, p. 121) and public funding of R&D in the business sector in a number of countries (OECD 2009, p. 120). Thus, we may conclude that R&D expenditures in a joint venture with foreign capital may influence the total R&D operations in the host country. It also happens that the fear of multinational corporations entering the domestic market increases R&D outlays in local companies (Aghion, Blundell, Griffith, Howitt & Prantl, 2009). Another benefit may be the “diffusion of information and knowledge to host country organizations. Potential receivers of this knowledge are domestic firms, universities, or research centres” (European Commission 2012, p. 8).

However, the technology transferred to new locations is not always the first/best technology. Older ‘mature’ technology may be transferred, already withdrawn from highly developed countries but still allowing for competitive advantage in a given location. The literature is dominated by the opinion that second-best technology may be more favourable for the host economy, as its assimilation is easier (Blomstrom & Kokko, 2003; Glass & Saggi, 1998).

FDI inflow makes the economy more competitive internally, better integrated with the international system, more open and perceived as more competitive (Kiysik-Uryszek, 2010). FDI inflow may also increase exports (Banga, 2006) and their diversification (Jayaweera, 2009), which will be visible mostly when investors export their products to international markets or when they buy in international markets. Corporations which exploit low costs of production in the host country may generate trade if FDI is designed to service the global market. Such conclusions can be found in Ekholm, Forslid & Markusen (2007), who see a clear link between FDI and the growth in exports, some of which may be to new markets or in new industries, thus also diversifying exports. Harding & Javorcik (2012) prove that FDI offers the potential for raising the quality of exports in developing countries. The research sample described in the publication included 105 countries in the period between 1984-2000. If local companies improve their productivity and become more competitive as a result of cooperation with other corporations, they may expand to foreign markets.

The review of the literature on FDI’s effects for the host country shows they may go in different directions, and are not always positive. They depend on a wide range of factors connected with the features of the investing company, the development stage of the host country, and the local environment. Thus we should be very cautious in assessing FDI effects and always consider circumstances specific to a given region and to the host country.

STRUCTURE OF FDI INFLOW IN THE VISEGRAD GROUP COUNTRIES

Direction of FDI in the World Economy

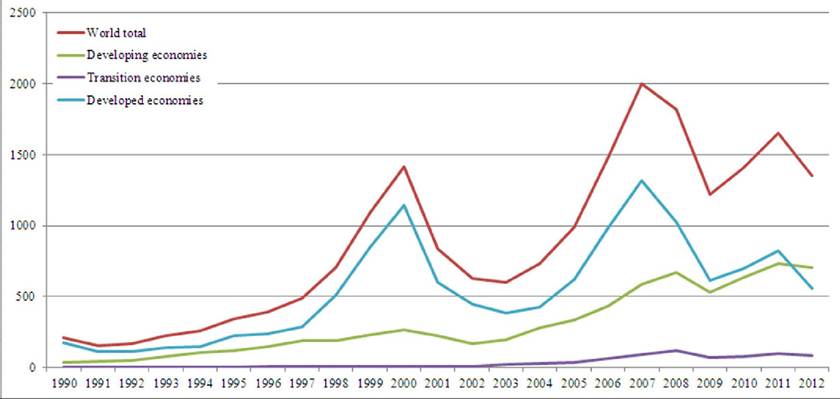

The dynamic increase in global FDI started in the mid-1980s. To date we have witnessed three breakdowns in its upward trend, connected with general slowdowns in global growth dynamics (Figure 1).

In 1985 less than USD 60 bn were invested all over the world, while in2000 the figure reached as much as USD 1.4 trln. At the beginning of the 21st century, global FDI was significantly reduced as a result of the global economic downturn, which was accompanied by lower investment activity of multinational corporations, but this trend reversed in2004. FDI flows from developed countries2 grew by roughly 40% on average from 2003 until the end of2007, supported by high economic growth in key host economies and strong corporate performance (Sauvant, Maschek & McAllister, 2009, p. 2).

Figure 1. Inward foreign direct investment flows from 1990 to 2012 (bn USD)

Source: UNCTADStat

The year 2007 was the record-breaking year for FDI inflow, which reached USD 2 trln. The financial crisis, which began in 2008, visibly influenced international capital flows. FDI inflow dropped by 20% compared to the previous year, reaching even 33% declines in developed economies. In 2009 FDI was further reduced by 40%. The drop was caused mainly by the drastic decrease in mergers and acquisitions (by 2/3) and, to a lesser extent, by the reduced number of greenfield projects. In addition, terms of loans became more rigid and firms’ profits dropped, which significantly reduced their investment potential (Poulsen & Hufbauer, 2011, p. 2). For these reasons, many companies, mostly large multinational corporations, gave up or suspended their FDI projects. In many countries privatization was also stopped, e.g., Sweden, Kuwait, France, Mexico. Massive capital withdrawals were observed, and profits were repatriated instead of being reinvested. This trend was common and visible in many industries, starting from the extracting industry up to manufacturing and services.

The actual financial crisis emphasized the flexibility of the developing and transition economies to the current global economic situation (Carp, 2012, p. 39). The increased volume of FDI at the beginning of the crisis was reduced in 2008 by 16%, and in 2009 by about 21%. Clear changes could be noted in the hierarchy of beneficiaries and investors, mainly by raising the relative weight held by investors in developing and transition countries.

In 2012 FDI volume decreased by almost 1/5. The deepest drops were reported for developed economies, mainly in the EU. Declines were recorded in 22 out of 38 developed economies, including 16 European economies. FDI in this group dropped by 32%, to the lowest level in ten years. Almost all industries suffered from the crisis. The smallest declines were recorded in the manufacturing sector (food processing, tobacco, pharmaceuticals) and services for business, communication, transport, and logistics.

In 2012, for the first time ever the developing economies absorbed more FDI than developed countries. Nine developing economies and two transition economies ranked among the 20 largest recipients of FDI in the world (WIR, 2013). Among developing regions, FDI inflows to developing Asian countries fell by 6.7% as a result of decreases across major economies, including China, Hong Kong, India, the Republic of Korea, Saudi Arabia and Turkey. However, 2012 inflows to Asia are still high, accounting for 58% of FDI flows to developing countries. FDI to Latin America and the Caribbean decreased only slightly, by 2.2 per cent in 2012, and amounted to over 240 bn USD. Africa was a region that saw FDI inflows rise in 2012 to about USD 50 bn. Slightly smaller FDI inflows were experienced by the transition economies of South-East Europe and the Commonwealth of Independent States.

The global ranking of the largest FDI investors shows that investors from developing and transition economies have become very active in recent years and are willingly seeking new investment locations in the world. In 2012 two developing countries now rank among the five largest foreign investors in the world, with China was the world’s third largest investor, after the United States and Japan.

FDI Inflow Dynamics in the Visegrad Group Countries

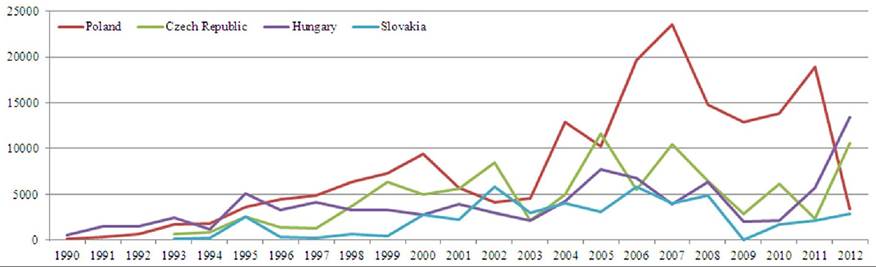

Since the beginning of the 1990s, when the Visegrad Group countries opened up their economies, investors have been showing increasing interest in locating FDI in their territories. The Czech Republic, Poland, Slovakia, and Hungary are economically much further advanced than the majority of Central and East European countries.3 They were the first to launch systemic transformations and one of their top priorities in modernizing their economies was to attract as many operators with foreign capital as possible, and the highest possible volume of FDI (Figure 2).

Figure 2. Inward FDIflows to Visegrad Group countries, annually 1990-2012 (mln USD)

Source: UNCTADStat

In the first years of transformation, Hungary received the most FDI, due to its more attractive legal framework compared to the other countries in the Group. Hungary was also the first to involve foreign investors to a great extent in the privatization process (Sass & Kalotay, 2012, p. 1). On top of that, labour was inexpensive in Hungary and the government was able to offer extremely attractive investment incentives. FDI inflow to other V4 countries, mainly to Poland, started when foreign operators were allowed to participate in privatization. Moreover, radical reforms and the size of the Polish market rapidly increased Poland’s attractiveness. Since 1996 Poland has systematically attracted more foreign capital than the remaining three countries and, with the exception of two years, regularly received the largest share of FDI inflows.

On the other hand, the Czech Republic and Hungary recorded declines in FDI inflows in mid- 1990s. In the Czech Republic this was caused by foreign exchange crisis in 1996. Little FDI inflow was yet noticeable in the Slovak territory until 1998 (with the exception of 1995). This was because the government had engaged in efforts to build the so-called Slovak capital community and refused to open Slovakia to foreign investment (Kucharcikova, 2013, p. 3). In the 1990s FDI volume in the countries of the Visegrad Group was also influenced by the competition of their economies, which had just started transformation, and the Russian crisis of 1998.

Nevertheless, in the period 1990-1999 the Czech Republic, Hungary, and Poland accounted for cumulated FDI inflows amounting to 79% of total FDI into Central and Eastern Europe. In the years 1995-2001 Poland was the single absolute largest recipient of inward FDI, with the Czech Republic being the next absolute largest recipient in all of the Central and Eastern Europe. However, Poland was far from being the most FDI-intensive host economy when nominal FDI flows are deflated by nominal GDP levels (Globerman, Shapiro & Tang, 2004, p. 7).

Data on the dynamics of annual FDI inflow to the countries of the Visegrad Group confirms the increased interest of foreign investors after they joined the EU. This indicates their competitive position improved as a result of EU accession. In Poland, the higher FDI volume was also the effect of lowering the fiscal burden of the corporate income tax, which encouraged investors to declare higher profits in their branches in Poland. While Poland was, as already mentioned, clearly the leader in the region, it should be noted that in 2002 and 2005 the Czech Republic attracted the most capital invested in the Visegrad Group.

Slovakia attracted the least FDI compared to other countries in the Group during the entire transformation period, with the exception of the years 1995, 2000 and2002. The main reasons were political developments in Slovakia, legislative barriers to entry, and a weak business environment (Fifekova & Hardy, 2010, p. 9). After 1999, FDI inflow intensified, but once the maj or privatization projects had taken place, it slowed down again.

In the second half of the first decade of the 21st century Poland was receiving the majority of investment capital in the CEE countries. The record-breaking year was 2007, when the inflow of foreign capital in Poland reached USD 23.5 bn. This was almost 80% higher than in2004, and over 15% higher than in 2006. In 2008 FDI in Poland dropped by over 37% compared to the preceding year, reflecting the trends on the global market. Such a substantial decrease in investment in Poland could suggest a deep regression with respect to the investment attractiveness of the country. We need to stress, however, that this happened a year after Poland’s FDI record-breaking result recorded in 2007, i.e. just before global economic crisis.

The negative impact of the crisis was overcome in Poland in 2011, but in 2012 FDI recorded a dramatic drop by over 82% compared to the previous year. This result was largely influenced by the scale of capital in transit,4 which in 2012 increased sevenfold globally. Disregarding capital in transit, Poland’s FDI inflow in 2012 would reflect the negative impact of crisis, but it would not be such a steep decline.

Since 2008 other Visegrad Group countries have also experienced serious consequences of the global recession. In Hungary reinvestment was significantly reduced, and other capital flows were negative as a result of the increase in reverse borrowings within companies and debt repayment from Hungarian branches to parent companies. FDI flows to Hungary were especially hard hit by the crisis years of 2009 and 2010, both in absolute terms and relative to flows to other countries, such as Poland and the Czech Republic. The 2011-2012 dataset indicates an increase in FDI inflows, however, according to Hungarian National Bank this is mainly due to a large capital in transit flow. A similar situation took place in the Czech Republic, where FDI increased four times in 2012 compared to 2011.

Summing up, since the beginning of transformation until 2012 almost 44% of all FDI directed to Visegrad Group countries was located in Poland, over 23% in the Czech Republic, over 21% in Hungary, and 11% in Slovakia. However, the value of FDI per capita has definitely been the highest in the Czech Republic throughout the entire period of 1990-2012.

Investors’ Geographic Origin

In analyzing the directions from which FDI flows into the Visegrad Group countries, initial stress should be paid to the very strong economic and trade ties of the region with other EU member states, in particular with the Economic and Monetary Union member states, (euro area, also known as the Eurozone). On average, about 70% of inward FDI in Poland, the Czech Republic, Slovakia, and Hungary comes from the euro area member states. The Baltic States are an exception in Central and Eastern Europe in this respect, as investments originating from euro area represent not more than 35% of the total incoming FDI. Becoming dependent upon one area, even an economically advanced region, may also have negative consequences. They may be particularly painful in times of economic crisis (Bialek, 2012).

Having stated the above, we may also note some differences in the origin of foreign capital in the form of FDI reaching the countries of the Visegrad Group. This is the outcome of the various determinants of investors’ interest, which have been summarily outlined in the first part of the Chapter.

The Czech economy offers a highly advanced technical infrastructure, skilled labour and a functioning market economy particularly strongly linked with the so-called “old” EU member states, also referred to as the EU-15. But strong trade relationships with the euro area slowed down economic growth in the Czech Republic in recent years. The authorities are trying to counteract the situation by improving Czech’s investment attractiveness by offering a wide array of incentives.

In the period 1993-2011 cumulated FDI inflow into Czech Republic was estimated at over EUR 77 bn. As of 31 December 2011, by the country of origin, the biggest share of foreign capital in the Czech economy originated from the Netherlands (27.4%), Germany (14.9%), and Austria (13.2%). Countries whose total outward FDI exceeded CZK 100 bn (approximately EUR 3.6 bn) also include Luxembourg, France, and Switzerland. The total share of EU-originating FDI investment amounted to 87.6%, with almost 92.5% from Europe in the broadest sense of the term. Hence only 7.5% of foreign capital investment was owned by investors from outside the Old Continent, mainly from the United States and Japan (Foreign Direct Investment in 2011, 2013).

In recent years Hungary has faced serious economic problems. The financial crisis had a strong impact upon the economic performance of the country. Cumulated FDI value at the end of 2011 was about EUR 70 bn. Over 70% originated from the EU, including about 22% from Germany. Similarly to all EU member states, investors from other countries of the Community, in particular from Germany, the Netherlands, Austria, Luxembourg, and France dominated FDI inflow to Hungary. Operators from outside of the EU also represented a substantial share, mainly those from the United States and, to a smaller extent, from South Korea and Japan.

The presence of investors from Central America is also an important aspect in Hungary. That might be the consequence of Hungarian investments in the region in previous years. In Hungary there are, e.g. investors from the construction (Cemex) and automotive (Nemak) industries. Hungary’s investment attractiveness was clearly enhanced by a variety of investment incentives addressed mainly to these industries. Besides direct subsidies and allowances, companies were attracted by industrial parks. In Hungary there are more than 200 such parks (Sass, Kalotay, 2012; Central Bank of Hungary, 2013).

Slovakia, despite being one of the smallest countries of Central and Eastern Europe, efficiently and quickly managed to cope with economic crisis. It provides a relatively attractive alternative to foreign investors with its low costs, investment incentives, and organizational support of the public administration. No doubt Slovakia’s membership in the euro area (since 2009) is also an advantage in the eyes of investors.

Cumulated FDI value for Slovakia in 2011 was almost EUR 40 bn. Data of the Slovak Investment and Trade development Agency (SARIO) indicates that FDI investment was distributed rather equally across the regions. With respect to the country of capital origin, the period 2002-2012 was clearly dominated by German investments (17%). Substantial shares were also recorded for investment projects from other EU member states (Denmark 6%, France 5%, United Kingdom 5%, the Netherlands 4%, Spain 4%, and Belgium 4%). Slovakia became also the location of non-EU capital, in particular from South Korea (12%) and from the United States (7%) (SARIO, 2012).

Considering its area, GDP, population and resources, Poland is the biggest economy in the Central and East European region. Its successful transformation, large domestic market, relatively low cost of a highly skilled workforce and management staff, and rich catalogue of incentives make Poland the unquestionable leader in attracting and maintaining FDI in the region. The value of cumulated FDI inflow to Poland in the years 1994-2011 exceeded EUR 139 bn.

From the point of view of invested capital, the Netherlands is at the top of the list of foreign investors in Poland. The value of cumulated Dutch investment at the end of 2011 was EUR 26.8 bn. Subsequent runners-up are investors from Germany (EUR 20.4 bn), France (EUR 18.7 bn), Luxembourg (EUR 13.1bn), and the U.S. (EUR 9.3 bn) (Biaiek, 2012).

In 2011 the largest FDI flow originated from Luxembourg (EUR4,542 mln), Spain (EUR 4,318 mln), Germany (EUR 3,592 mln), and Sweden (EUR 2,617 mln). There were also cases of divestment, i.e. investors’ withdrawals from Poland. These investors were mostly Irish (EUR -2,946 mln) and Swiss (EUR -2,424 mln) (NBP, 2012).

Structure of FDI Flows

As was the case with the origin of capital, the structure of FDI flows to the Visegrad Group countries is similar throughout the group. In all the countries investors from the automotive, electronics, and machinery industries played an important role. However, more in-depth analysis of FDI inflows to individual countries of the Group reveals some differences and specializations in the host countries.

In Poland, like in other Visegrad Group countries, firms with foreign capital are gaining in importance in the economy. Today it is hard to imagine many sectors of the economy without foreign investors, with their knowledge, organization, technology, and capital. This is clearly visible in automotive industry, and in electronics and domestic appliances.

In 2011 there were almost 25,000 economic entities with foreign capital operating in Poland, nearly 8% more than in 2010. In terms of legal arrangements, the group was dominated by limited liability companies (93.1%). Joint stock companies ranked second, but their share was only 3.8%. In 2011 more than 1,500 new entities were established (approximately 200 more than in the preceding year). The majority of new businesses dealt with trade and repairs of motor vehicles (440). New projects were mostly greenfield investments (80%).

From the point of view of the size of the businesses invested in, more than 84% were small firms (up to 49 employees), including 66% micro-businesses (employing up to 9 people). The smallest group, less than 5%, was comprised of big companies (employing over 250 people). The majority of businesses (almost 2/3) dealt with the trade and repair of motor vehicles (28.0%), industrial processing (20.1%), the real estate market (9.5%), and construction (9.2%). At the end of 2011 companies with foreign capital employed 1,566,500 people, an increase of 3.2% more compared to 2010.

In 2011, as many as 10,108 companies with foreign capital exported their products or goods and materials. They represented 40.6% ofthe total number of businesses with foreign capital (41.1% in 2010). Exports to the parent company or to related entities in a capital holding or in a group of companies to which a given entity belongs (so called intra-group exports) accounted for 41.7% of total exports by these companies in 2011 (a decline of 5.6%). Exports to parent companies or related entities prevailed among the manufacturing entities - 83.8%.

In 2011 as many as 46.1% of businesses with foreign capital reported outlays for the purchase of fixed assets in Poland (47.7% in 2010). Their value was PLN 73,704.4 mln, an increase of 19.6% compared to the same value for 2010. The largest amounts were invested by businesses in the manufacturing sector (35.1% of outlays for fixed assets made by all entities with foreign capital), companies dealing with trade and repair of motor vehicles (11.6%), and information and communication (10.4%) (GUS, 2012).

Many foreign investors operating in Poland represent leading multinational corporations. The scope of this publication does not allow to list even a small portion of the largest ones. By way of example however we will mention Amcor Ltd, Strabag, Toyota, France Telecom, Hutchinson, Dell, Peugeot, BSH Bosch und Siemens Hausger- ate, IBM, Metro Group AG, Siemens, Volkswagen, FIAT, Indesit, Fujitsu, and Philips (PAIiIZ, 2013).

The two recent decades witnessed a major change in FDI structure in Hungary. At the beginning of the 1990s, direct investments focused predominantly on manufacturing. Then the importance of this sector gradually decreased. In 2000 its share was still significant and accounted for 47% of all FDI in Hungary. The role of manufacturing continued to decrease to the level oscillating around 25% in 2009, then increased to 30% in 2010. Transport and electric engineering were the most important investment destinations within the manufacturing sector. On the other hand, services have gained in importance in the structure of FDI in Hungary over the last 20 years, in particular wholesale and retail trade, repairs, real estate, IT and business services.

The largest investment projects in Hungary can be divided into two groups. The first includes affiliates of multinational corporations, such as Audi, Nokia, GE, Samsung, Philips, E.ON, Deutsche Telekom (M-Telekom), and Fibria Cellulose. The second group consists of former Hungarian state- owned enterprises privatized through public offers on the stock exchange, where at present a number of majority shareholders are foreign investors, e.g. MOL, OTP Bank, and Richter.

Some sectors of the Hungarian economy, especially manufacturing and services, are dominated by entities with foreign capital. When it comes to vehicles, Hungary is the host country for such renowned global corporations as Japanese Suzuki and German Audi. In 2012 a new plant of German automotive-holding Daimler AG launched production in Hungary. Other automotive corporations, such as American General Motors’ and German Opel, specializing in spare parts, also enjoy a substantial share in the Hungarian market. It is also worth mentioning top class German manufacturers of vehicle systems, such as Knorr-Bremse (braking systems) or Robert Bosch (spare parts and accessories).

In Hungary there are also many global leaders in the electronics industry, e.g. American National Instruments, Jabil, and GE, Flextronics from Singapore, Foxconn from Taiwan, Dutch Philips, South-Korean Samsung, German Siemens, and Finnish Nokia.

Leaders in the service sector comprise multinational financial and telecommunication corporations. An example may be MKB bank, with German BayerischeLandesbank as its major shareholder, and CIB Bank owned by Italian IntesaSanpaoloSpA. On the telecommunications market in Hungary one may find, e.g., M-Telekom owned by the German giant Deutsche Telekom and an affiliate of Norwegian Telenor. Operators with foreign capital also have a big share in Hungarian retail trade, with the leading corporations in this area including French Auchan, Cora from Belgium, British Tesco, and German Lidl (Sass, Kolotay, 2012).

In Slovakia the majority of FDI was attracted by the automotive industry, with plants opened by Volkswagen, KIA Motors, and PSA Peugeot Citroen. Investors from the electronics industry are also interested in Slovakia. It is a host country for FDI by Sony, Samsung, Panasonic, and AU Optronics.

Foreign investors have also located their capital in other industries in the Slovak economy, e.g. in machine-building and chemical industries and in telecommunication services. The list of key foreign investors in Slovakia should be supplemented with e.g. U.S. Steel, Whirlpool, IBM, HP, DELL, Siemens, Alcatel, Foxconn, and Soitron (Bialek, 2012, SARIO, 2012).

Currently in the Czech Republic there are more than 173,000 businesses with foreign capital. Like in other Visegrad Group countries, the first period after transformation was dominated by investments in manufacturing. Modernization of the economy, upgrading of infrastructure, and human resource development have turned the Czech Republic into an attractive investment location also for services and R&D centres.

According to the Investment and Business Development Agency (CzechInvest), there are at least several industries in the Czech economy where FDI inflows are constantly increasing. As has been mentioned, knowledge-based industries and advanced technologies are among them. These are mostly telecommunication, business support services, aviation, the automotive industry, machine engineering, equipment and tools, natural sciences, electric engineering and electronics, renewable energy, and nanotechnologies.

Among the over 173,000 businesses with foreign capital in the Czech Republic, the biggest companies are ABB, Continental, DANONE, Ford, Panasonic, Nestle, IBM, DHL, Astra Zeneca, Rockwell, Procter & Gamble, Renault, Siemens, Lufthansa, Honeywell, and Volkswagen (Czech- Invest, 2013; Czech National Bank, 2013).

INVESTMENT ATTRACTIVENESS

Assessment in the Light of Selected Rankings

When analyzing the results of leading international rankings, we may conclude that over the last several years, including the times of crisis and economic downturn, Visegrad Group countries have remained an attractive investment location.

According to The Global Competitiveness Report 2012-20135 Poland and Hungary are in transition from economies driven by increasing productivity to innovation-driven economies. The Czech Republic and Slovakia are considered innovation-driven economies. (The Global Competitiveness Report 2012-2013, 2012, p. 10). Between 2004-2012 only Poland markedly improved in the Global Competitiveness Index ranking from 60 to 41, Czech Republic remained stable (+1). Slovakia (-28) and Hungary (-21) lost substantially. From among the countries of the Visegrad Group, the highest ranking positions in the competitiveness ranking6 in 2012-2013 are occupied by the Czech Republic and Poland, 39th and 41st respectively, while Hungary and Slovakia rank 60th and 71st respectively (The Global Competitiveness Report 2012-2013, 2012, p. 14). This means the economic transformation has brought concrete measurable results, as these countries have managed to achieve higher efficiency in many industries and improve the investment attractiveness of the region. At present, the areas where FDI is expected in these countries are creative industries, strategic services, and R&D.

When analyzing the factors determining the intensity of FDI inflow to Central and Eastern Europe in the years 1996-2010, Mateev & Tsekov (2012) demonstrate that the primary advantages of these countries are low taxes (Czech Republic) and the competitive cost of labour (Slovakia). However, individual countries differ in geopolitical, economic, and cultural terms, hence there are factors which distinguish them from one another, and methods of attracting foreign capital by offering, e.g. well developed infrastructure or establishing special economic zones.

According to the World Bank's Doing Business 2013 report the “economies in Central and Eastern Europe have received large inflows of FDI over the past couple of decades because they are seen as entry points into the huge European market and also because they have relatively well-educated labour forces.” (2013, p. 49). Macroeconomic forecasts suggest Central Europe will continue to be the fastest growing region in the European Union. Another advantage of these countries consists in their skilful combination of emerging markets with the stability of developed economies.

Studies by Ernst & Young show that, in the opinion of 49% of interviewed investors, in the years to come Central and Eastern Europe will be the most attractive investment spot globally. (E&Y attractiveness survey, Europe, 2013, p. 8). Investors even ranked CEE ahead of Brazil, Russia and India. Countries of the Visegrad Group are the most popular among the countries of the CEE region. Stability, predictability, and a well educated labour force are the location selection criteria most often taken into consideration in the times of recovery. Half of interviewed multinationals also pointed to the cost of labour as a basic element of investment decisions. In this area as well the Visegrad Group countries, despite increases in salaries and wages, remain attractive to foreign investors. It suffices to say that annual wages in Poland, Hungary and the Czech Republic remain, on average, half of those in Germany, France or the UK (Eurostat, July 2013).

According to E&Y, in 2012 Poland and the Czech Republic combined accounted for 5.8% of all FDI projects globally (2013, p. 15). In addition, Poland was the top improver globally, according to the World Bank’s Doing Business 2013 report, because it has won attention as the fastest growing EU member since 2008, and benefits from a skilled native and migrant workforce. (Doing Business 2013, 2013).

Poland is also a leader according to UNCTAD when it comes to investment attractiveness. Its major competitive advantages are a large and rapidly developing internal market, an educated and flexible workforce, stable banking system, access to international local markets, and the availability of suppliers and partners. Most probably the above mentioned factors gave Poland, as the only member of the Visegrad Group, a place in the group of the top 15 attractive FDI locations in recent years. (World Investment Report, 2010, 2011, 2012, 2013).

Poland is also the only country among the Visegrad Group members included in the basket of 25 countries covered by the FDI Confidence Index.7 It occupied its highest ranking position, sixth, in 2010, while in 2012 and 2013 ranked 23rd and 19th, respectively (2013, p. 3). The report by A.T. Kearney stresses that Poland is particularly strong in automotive components and vehicle assembly, and is seeing increased activity around its newly built highways. Besides, Poland “is also seeing more knowledge-centered investments, thanks to a large student population, a breadth of language talent, and an EU grant scheme to support such investments” (A.T. Kearney 2013 FDI Confidence Index, 2013, p. 22).

The Visegrad Group countries also occupy high positions in the ranking published in 2013 by Foreign Policy magazine. Its B aseline Profitability Index (BPI) is intended to be an overall guide for all foreign investors and is based on three factors: asset growth, preservation of value, and repatriation of capital. In the BPI ranking Poland is 18th among the most attractive countries in which to invest, while the Czech Republic ranks 22nd, Slovakia 28th, and Hungary 37th.

System of Investment Incentives

The system of investment incentives in place significantly impacts the investment climate in a given economy. It also contributes to increased attractiveness of the host country. Support is most often coordinated by a specialized agency and includes all sorts of tax allowances, favourable settlement rules for investment projects, and also direct subsidies for investors.

Although foreign investors often perceive the CEE as a single area, the countries in the region differ rather substantially with respect to their economic accomplishments, FDI absorption capacity, and their approaches to investment incentives (all of course in line with the EU acquis communautaire). Poland and the Czech Republic can be proud of their successes in attracting foreign capital. In the period 2000-2012 cumulated FDI inflow into both countries was the highest in the CEE; it exceeded USD 154 bn in Poland and USD 82 bn in the Czech Republic.

The whole Central and East European region is situated in the centre of the pan-European market, and each of the four countries of the Visegrad Group has its own particular geographical mer- its.8 Considering not only the location but, first of all, market determinants, Poland is very well positioned, having definitely the biggest market in the region. It is also economically stable, with a good availability of workforce. However, conditions for running a business in Poland are assessed lower than in the remaining Visegrad Group countries. The Czech Republic has the best air transport connections in the region. The advantages offered by Hungary include a relatively well-developed infrastructure and high quality of human resources. In Slovakia costs are the lowest and it may become the primary destination of service investments. All countries of Visegrad Group constantly improve their business environment and investors may expect direct support from local and regional authorities.

Poland also offers a wide range of incentives for FDI proj ects. Investors may benefit from multiannual support programs, subsidies, real estate tax allowances, or special economic zones. The Ministry of Economy manages a special program9 designed to enhance innovation and competitiveness in the Polish economy. Its main aim is attracting and supporting FDI in sectors referred to by the OECD as hi-tech sectors.10 Support is offered only to investors who plan to invest in the following priority industries: automotive, electronics, aviation, biotechnology, modern services, and R&D. The system provides investment support for the cost of creating new jobs (non-refundable employment subsidies) and eligible costs of the new investment (non-refundable investment subsidies).

In Poland there are also 14 special economic zones, and several dozen technology and industrial parks. The latter have become a popular tool for supporting local and regional development through entrepreneurship and innovation support schemes, which establish the framework for cooperation between public administration, businesses, and research centres. Finally, Poland is the largest beneficiary of EU structural funds from among the countries of Central and Eastern Europe. Its cohesion policy budget for the years 2007-2013 exceeded EUR 67 bn. Currently, ongoing discussions concern the new financial perspective for 2014-2020. A major part will be dedicated to companies, with the Polish Information and Foreign Investment Agency (PIFIA), together with local and regional authorities, entrusted with the task of seeking and supporting foreign investors. All these institutions should provide concrete and coherent information to allow an investor to tailor his or her position to ensure that he or she receives the maximum amount of incentives available.

Foreign investors are attracted to the Czech Republic by a rich offer of financial incentives financed with public resources. Investment projects are supported by the Czech government via the CzechInvest agency, and (similar to other EU member states) the assistance may not exceed the amount specified in the regional map of State aid intensity. The ceiling depends on the region where an investment project is taking place. A large portion of the assistance is directed to manufacturing projects. Support consists in, e.g., granting full or partial tax allowances (up to five years of full corporate tax relief for newly established legal entities, and partial corporate tax relief for the expansion of existing production), subsidizing new jobs (up to 2,000 EUR annually for each newly created job), subsidies for training and retraining, and also site support (transferring public land at a favourable price). Incentives are also available for developing export-oriented industries representing high value added.

Since July 2012, when the Act on Investment Incentives was amended, State aid has been expanded to cover technology centres and business support services. Support is available for investment in research, development, and innovation (technology centres) and strategic services centres. The latter are units dealing with selected operations by companies, closely linked with IT technologies and having clear international orientation, e.g., IT software development centres or expert and task-specific ICT centres. On top of that, the Ministry of Industry and Trade launched the program Entrepreneurship and Innovation, which covers 15 various assistance programs and offers, e.g., non-refundable subsidies, preferential loans and guarantees. Similarly to Poland, the Czech Republic receives structural funds under the EU cohesion policy.

In Hungary there are also some instruments providing incentives to investors. These include all sorts of cash subsidies, tax allowances (including 80% reduction of the corporate income tax), low-interest loans, and land available either free of charge or at reduced prices. The main types of cash incentives related to investments focus on the delivery of an investment project (e.g. purchasing assets, construction works, etc.), creating new jobs and training employees. The Hungarian Government provides a negotiation-based “VIP” subsidy opportunity for investments greater than EUR 10 million with a fixed number of newly created jobs, depending on the purpose and location of the investment. There is also the possibility to subsidize a project from available EU Funds.

In Hungary, priority is given to FDI aimed at the development of the economy, employment, transport, human resources, health and wellness services, environment and energy, public services and the regions. Investors may choose from more than 200 industrial parks, which facilitate the establishment and operation of a business, and offer the support of local authorities, tax allowances, and preferential conditions.

The typical services specifically provided by industrial parks in Hungary include: the provision of basic infrastructure for production (e.g. energy, water and waste-water treatment facilities) and a wide range of other quality services (e.g. banking services, customs administration, consultancy, security guards and office services).The institution entrusted with the task of promoting foreign investment and bilateral trade, as well as assisting EU integration-oriented development of SMEs, is the Hungarian Investment and Trade Agency (HITA).

The last on our list of analyzed countries, Slovakia, also offers a transparent system of incentives. State aid and investment incentives vary and depend on four categories of projects that can be supported: industrial production, technological centres, shared service centres, and tourism. Support is available to investors starting new businesses as well as to those expanding existing initiatives. For each category of projects, there are specific conditions which must be met in order to apply for investment incentives. Incentives consist of, e.g. subsidizing the acquisition of material and immaterial assets, income tax relief, a contribution for new jobs created, and transfer or exchange of real property at a price lower than the general asset value. State aid is available up to 50% of investment and the minimum invested amount depends on the unemployment rate in a given location (it can be even as much as EUR 14 mln).

Recently Slovakia initiated support for the R&D sector by offering a wide array of public subsidies, incentives and programs which have encouraged many investors to transfer their technology and research centres to Slovakia. The first contact point for investors is SARIO. Among its many responsibilities, the most important deal with providing investors with initial information and assistance with their investment.

Special Economic Zones as a Tool to Attract Foreign Investors

Special economic zones, or so-called free trade zones, operate in several countries in Central and Eastern Europe (Romania, Estonia, Latvia, and Lithuania). From among the Visegrad Group countries they operate only in Poland. For this reason below we shall discuss the specificity of Polish special economic zones. Special economic zones (SEZs) are one of many tools designed to attract foreign investors and increase the investment attractiveness of the host country or region

Pursuant to Polish law, a special economic zone is an uninhabited, distinguished territory, where businesses may operate on terms laid down in the law (Ustawa, 1994). A zone may be established to stimulate economic development of a part of the country’s territory, in particular by (Ustawa, 1994, Art. 3):

1. Developing specific areas of business activity,

2. Developing new technical and technological solutions and the application thereof in the national economy,

3. Developing exports,

4. Increasing the competitiveness of products and services,

5. Utilizing existing industrial assets and economic infrastructure,

6. Creating new jobs,

7. Utilizing available natural resources in a sustainable and environmentally friendly way.

At present in Poland there are 14 SEZs. As of the end of June 2012, almost 1,500 permits were issued to operators to run businesses in these zones. These entrepreneurs invested almost PLN 82 bn (approximately EUR 20 bn) and employed more than 240,000 people. The main incentives for locating a business in a SEZ include preferential operational terms, developed investment plots, and qualified staff (Special Economic Zones, 2012).

Preferential terms mean the availability of State aid. In the case of SEZs, State aid may be granted in accordance with regulations which specify its allowable intensity for a given area. The aid takes the form of corporate income tax allowance and real estate tax allowances. Allowances and relief are available to entrepreneurs up to 2020 when, pursuant to the amended Act on SEZs, the zones will cease to exist under the current arrangements.

Recent years have witnessed the stabilization and further development of SEZs in Poland. In 2011, 188 permits were issued, an increase of 6% compared to 2010. The most permits were issued in the Kostrzyn-Slubice and Lodz SEZs - 22 each. With respect to investment outlays, in 2011 a slight decrease was recorded (by 3%) compared to the preceding year. Statistics were better for the labour market. In 2011 the number of people employed in SEZs exceeded 240,000 and increased by 7% compared to 2010. In absolute numbers, the zone in Katowice has the highest employment (ca. 48,500), followed by the SEZ in Walbrzych (ca. 31,200), Tarnobrzeg (ca. 28,700), and Lodz (ca. 24,800).

Special economic zones are open to both domestic and foreign investment projects. Ministry of Economy data shows that entities with foreign capital play an important role as sources of investment expenditure in all of the 14 special economic zones. As at 31 December 2010, the total investment outlays amounted to over PLN 73 bn (approx. EUR 17.3 bn), and only 17.3% consisted of Polish capital. In the group of foreign investors, German businesses accounted for the largest share of investment. By the end of 2010 it reached almost PLN 12 bn (approx. EUR 3 bn), i.e., 16.3% of total investment outlays in all the 14 zones. In terms of value, the largest investments were recorded in the Legnica and Lodz Special economic zones. German investors were followed by American (11.5%), Japanese (9.7%), Dutch (9.5%), and Italian (8.5%) business entities. In all the SEZs, the share of EU-based capital was ca. 44% (Ministry of Economy, 2010).

It is worth stressing that SEZs in Poland score high against other similar zones in the world. In the ranking of FDI Magazine, which lists the 50 top special economic zones in the world, five were SEZs from Poland: the SEZ in Katowice ranked 11th, in Lodz 18th, in Walbrzych 22nd, in Pomorska 35th, and in Starachowice 37th. The ranking was dominated by SEZs from the Middle East (23 out of 50), mainly from United Arab Emirates (14), although the zones from Central and Eastern Europe were also noted. They were recognized mostly for good quality infrastructure and well developed networks (www.fdiintelli- gence.com, 2013).

Special economic zones seem to be a specific location advantage of Poland compared to other Central and Eastern Europe countries, including the Visegrad Group countries. The operational scale and legal framework offered to investors in Poland have not been reproduced in any other country in the CEE region. Slightly similar arrangements, although on a smaller scale, are available only in Lithuania and Latvia. Estonia and Romania offer access to selected duty free areas. Neither in Bulgaria nor in any other Visegrad Group country can we find specific areas that operate similarly to SEZs. This does not mean, of course, that those countries do not have any investors’ support schemes involving State aid. On the contrary, as has been mentioned above, e.g., Czechs grant tax allowances depending on the region and volume of investment expenditure.

Investment Barriers