Chapter 40 Leveraging Technology Options for Financial Inclusion in India

Shalu Chopra

VES Institute of Technology, India

Rajeev Dwivedi

Institute of Management Technology, India

Arun Mohan Sherry

Institute of Management Technology, India

ABSTRACT

Financial services have a ubiquitous need however the urban rich have easy and universal access with wider options, compared to the low-income group who are forced to accept informal, expensive and riskier means to fulfill their financial needs.

The demand and supply of financial services for the poor is imbalanced, with supply being acutely constrained by lack of viability and sustainability of current business models. Technology and IT has a pivotal role in making financial inclusion a viable reality. Technology, including information technology can enable lowering costs by increasing automation, enhancing efficiency, enabling scaling up through uniformity, consistency and security. Multiple technology choices are available to financial service providers but few have been proven yet. This paper examines technology options at the front end and back-end in detail with a critique of alternatives available for financial inclusion in Indian context.INTRODUCTION

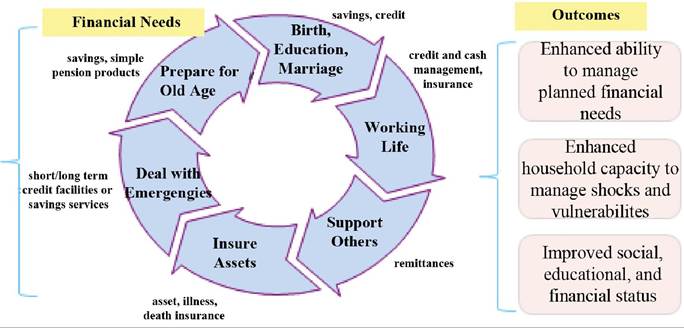

Access to financial services (in the form of savings, credit, insurance, remittance or welfare payments) is a fundamental tool for managing a family’s well being and productive capacity, to smooth expenditure when inflows are erratic, to build surplus when the demand for expenditures is heavy (school fees, marriages, buying farm equipment) or to protect against emergencies. However only one-

DOI: 10.4018∕978-1-4666-6268-1.ch040

quarter of financial households have any form of savings with formal banking institutions (Adams, et al., 2008). The following Figure 1 depicts how finances help a person at every stage of his life. It not only improves person’s social, educational and financial status, also provides capacity to manage shocks and vulnerabilities at any point of time in life (Singha & Gayithri, 2012; Borghoff, 2011; Ravi, et.

al., 2011; Zhang, 2011). According to the World Bank (2009), getting financial services to.

Figure 1. Financial needs (Microsave)

rural people is the biggest challenge in the quest for broad -based financial inclusion.

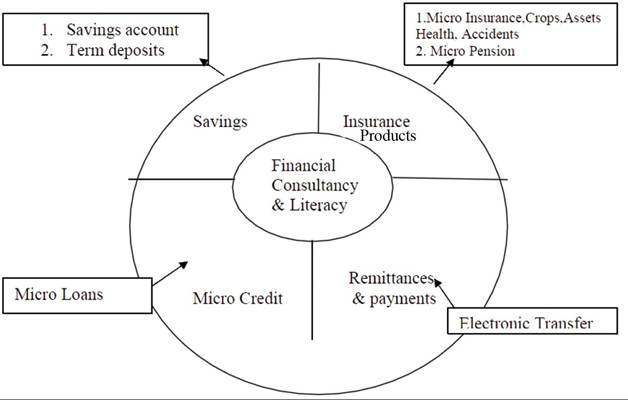

According to the “Transact” the national forum for financial inclusion “Financial Inclusion is a state in which all people have access to appropriate, desired financial products and services in order to manage their money effectively.” It is achieved by financial literacy and financial capability on the part of the consumer and financial access on the part of product, services and active suppliers.” The following Figure 2 depicts the Components (Savings, Micro credit, Insurance and Remittance) of Financial inclusion.

Several studies have demonstrated that there is considerable demand for financial inclusion by the under-banked and unbanked provided these services address specific consumer needs such as ease and proximity of access, security, low-value high-volume transactions, and financial services that offer value better than existing informal alternatives and integrate into the livelihoods, such as entrapping income during harvesting and enabling access during festive seasons or emergency needs (World Bank, 2008; Balmer, et al., 2005). They also have a willingness to pay reasonable charges to avail these services (Cheney, 2008). Given the few and expensive alternatives for financial services that poor have, they are willing to pay a price based on perceived value and cost of existing alternatives likes loan sharks, money lenders or informal savings with high risk.

Figure 2. Components of financial inclusion (Karmakar, 2010)

Key influencers of demand and willingness to pay are demographics, literacy levels, socialdynamics, local enablers and inhibitors, availability of informal and alternate channels (together with their cost and convenience), adaptability to change, comfort with technology, and other exogenous and endogenous factors (Affleck & Mellor, 2006).

Out of the 428 million deposit accounts in India only 30% are in rural areas. With a rural population of 741.6 million, the rural penetration of bank is as low as 18%. Even where access to banking is available the transaction cost of savings in India is as high as 10% for the rural people (Group Savings and Loans Associations: Impact Study, 2010).

Banks usually target customers with regular and stable incomes, like salaried employees and well established businesses. This is efficient and profitable as most of these clients conduct high value and less frequent transactions, resulting in lower operating costs (Chakrabarty, 2006). Banks service most customers from branches, while facilitating few transactions outside the branch premises, through ATMs (cash withdrawal and deposit), internet and mobile banking (cheque book request, bill payments, funds transfers, and balance enquiries).Banking is currently costly and labour intensive for all concerned.

Due to high cost of delivery and small average size of the transactions, it is not profitable business for banks to set up shop to cater for the poor people (Chakrabarty, 2006). As a consequence a large segment has remained financially excluded.

But, the situation is gradually changing and increasingly several organisations including Banks, Mobile Network Operators (MNOs), Technology Service Providers, Business Correspondents (BC’s) and large agent networks are recognizing that there is considerable potential at the bottom of the pyramid (Wilcox, 2011; 2015). They understand that getting low income segments into the regular financial sector is beneficial both for the people belonging to this segment and the financial institutions.

Widespread penetration of mobile technologies and their integration with banking infrastructure has enabled banking services outreach in a low cost and more efficient manner through mobiles phones (Suoranta & Mattila, 2004). Advances in biometrics and its integration with Point of Transaction (POT) terminals has enabled substitution of bank personnel by technology, supported by less qualified agents and business correspondents, enhancing security and lowering costs (Davis, & Owens, 2009; World Bank, 2008).

The policy environment too has evolved considerably. Using a mix of loose and tight regulations and taking a controlling, direction setting or mentoring approach, it has provided suitable incentives and disincentives to promote financial inclusion. Policy enablers such as extending outreach through third party agents and agent network managers or business correspondents have been promoted by the Reserve Bank of India (RBI, 2009; 2010).

Today a wide range of technologies are available that can address requirements for financial inclusion in parts.

LITERATURE REVIEW

Financial Inclusion has been on the agenda of several institutions around the world. Across the developed countries, access to financial services is largely ubiquitous; there is an abundance of cash and credit on demand, from multiple channels, and 24 hours a day. But in developing countries the situation is very different; approximately 88 percent population is excluded from access to the formal financial system (Richard, et al, 2009).

A mix of gratuitous and market-led approaches has been tried in various geographies. Migration of poor to urban environment for better and steady wages is quite common in developing countries. This leads to the first and second generation migrants usually remitting money back to their split families.

In Kenya, M-PESA from Safaricom (a leading telecom operator) has leveraged this need to achieve significant take-up using mobile technology. It launched the Sambaza product that allows subscribers to send small amounts of airtime value across the network to others and pay utility bills.

In Brazil, Utility and other payments including welfare payments have been tapped by large banks using branchless banking methods. Initially started and incentivised by the state for social and welfare payouts (Saeed, et. al., 2012), the services gradually scaled and became mainstream financial services.

Philippines is pioneer in enabling financial services through mobile phones.

Products like Smart Money and GCASH have enabled large amount of money transfers between urban, rural areas and overseas, leveraging the distribution advantages of Mobile Network Operators (MNOs). Countries like Sudan, Ghana and South Africa have adopted mobile technology for inclusive finance. Latin American countries like Uruguay, Paraguay, Argentina, Venezuela and Colombia started with a huge success. As a result several mobile financial products have emerged for e.g. Tigo cash in Ghana, Pago Movi in Peru, Nipper n Mexico and Oi in Brazil.Tigo Cash in Ghana is a mobile financial services product that allows people to use mobile phone as a mobile account. It provides an affordable, fast, convenient and safe way to send and receive money, buy airtime credit, pay for goods and services using a mobile phone anywhere in Ghana (Okyere, Gloria, & Kwamena, 2011). Customers can deposit and withdraw money from their mobile phone with any one of authorized Tigo Cash Agents. They are not required to hold a bank account to use the service. There are a few easy steps to begin sending money with Tigo Cash:

• Customers have to first sign up for the service at a Tigo Cash Agent or a Tigo Service Center by providing their picture ID for proof.

• After the account is activated, customers can deposit cash into the account - for free!

• With money in their account, the customer can use their Tigo mobile phone to send money, buy airtime credit or pay bills at anytime, from anywhere and to anyone in Ghana.

• To withdraw money from their account, the customer can visit a Tigo Cash Agent or a Tigo Service Center.

• Transaction cost involved in mobile banking is very low as compared to traditional banking. (It is US $ 0.50 as compared to US$ 2.5).

TECHNOLOGY OPTIONS

AT THE FRONT END

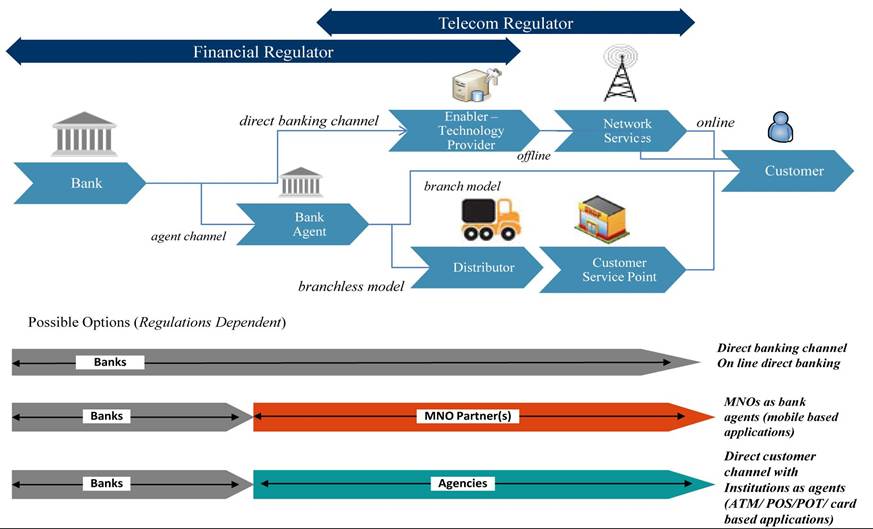

People can access financial services either through a brick and mortar model (which is branch based) or through an ICT model (which is branchless). Figure 3 depicts the technology options for the branchless model.

There are three possible ways of doing this:1. Online Direct Banking (PC/Internet Banking)

2. ATM/Mobile ATM/Point of Terminal (POS/ POT) and Smart Card Based

3. Mobile Banking (USSD, SMS, STK, IVR Technology based Financial Services)

Figure 3. Branchless banking model (Microsave)

Anybody (urban/rural) can access financial services using online Direct Banking provided the person has Personal Computer and Internet facility. This is very popular among urbanized.

ATM/Mobile ATM/Point of Terminal (POS/ POT) and Card Based technology revolutionized banking sector around 30 years ago. Initially, ATMs were bulky, expensive and difficult to maintain and replenish. Their deployment was delayed for over 20 years in many countries like Africa, India due to the cost, inadequate telecommunications and electricity supply. Now the scenario has changed due to improvement in technology, Financial institutions have started deploying POS/ POT devices, Mobile ATMs in rural locations that often provide the same functionality as ATM at a fraction of the cost (Ketley, 2009). Banks have also started interoperability (using Bank A’s card on Bank B’s ATM) and this has reduced the operational cost dramatically. In some countries commercial banks have migrated all of their customers to electronic channels, using debit cards at ATM and POS devices. The cost of implementing plastic cards has reduced dramatically in recent times so this seems to be much cheaper option, but processing takes little bit more time as daily transaction has to be uploaded offline at the banking server site (Davis & Owens, 2009).

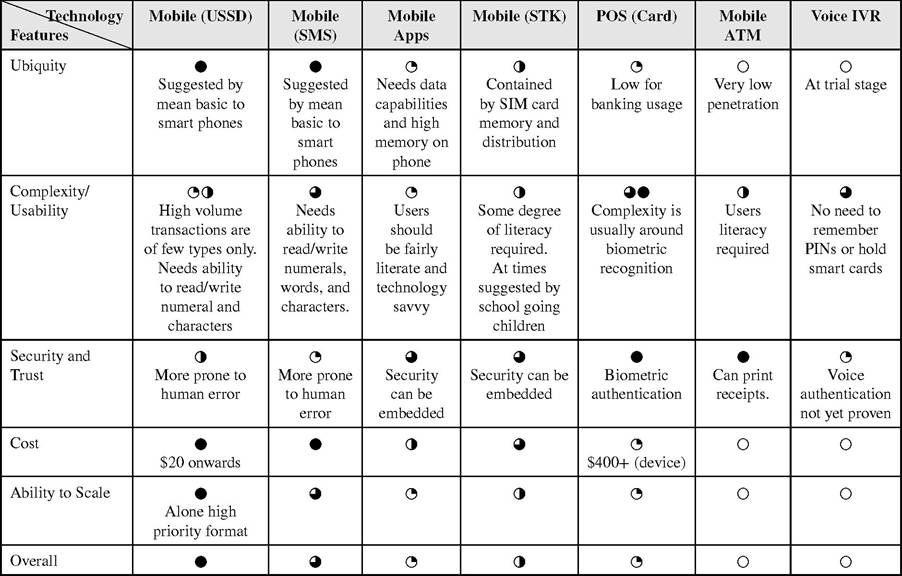

Mobile Technology based Financial Services can also be accessed using mobile phones with STK (SIM Tool Kit), SMS (Short Message Service), USSD (Unstructured Supplemental Service Data), Mobile App and through IVR (Interactive Voice Response) mechanism.

Mobile Phones with SIM Tool Kit (STK) is a very popular option being used in developing countries (Kumar & Mino, 2011). Mobile Phones with USSD (Unstructured Supplementary Service Data) are based on communication technology that is used to send text between a mobile phone and an application program in the network. It is very much similar to Short Messaging Service (SMS). Each type requires customers to remember codes to initiate transactions e.g. USSD requires the format typically in a set of * numbers and a # (like * 140* 12345678#) to initiate a query. USSD transactions are session based as compared to SMS and because of this property it is very popular in banking applications as the customer can immediately see his/her transaction happening (Soni, 2010).

For Mobile Banking user should be fairly literate and techno savvy so in order to provide appropriate training mobile financial service providers are developing simple step by step guide with mobile screen shots to ensure that the customer and agents can easily process transactions.

Voice IVR is at a very trial stage. Using this technology there is no need to remember PIN or hold smart cards. Authentication is based on user’s voice.

Table 1 shows the various technology options available today in Indian context and their comparison (in terms of ubiquity, complexity, secu- rity/trust, cost, scalability) in enabling financial inclusion at scale.

Mobile USSD and SMS based applications are most ubiquitous as most of the mobile handsets (low end to high end) support this. But they are not easy to use as the customer has to remember the specific codes for each and every transaction. But, now a days to deal with m-banking, m-commerce providers are providing users with quick reference guides to assist them in remembering the codes for various transactions. Security/ reliability in USSD applications is quiet high as MNOs offer most reliable communication format whereas Voice (IVR) and SMS are at second and third level. Mobile STK is very user friendly

Table 1. Comparison of mobile technology options and their potential in enabling financial inclusion at scale

•OOHigh, Medium, Low scores

option for customers but uploading STK menu becomes sometimes unreliable (especially on low end phones). POS based mobile machines and Mobile ATMs are less complex from usage point of view as an agent can be deployed at the village centre/Kiosk which can help novice users to perform transactions.

Voice IVR is comparatively easy to use but their cost is high as compared to mobile USSD and Mobile SMS based applications and security, ability to scale is also major concern as it is at a very trial stage. Overall, Mobile SMS and USSD based applications take high score.

Many other innovations are in early stages and few of them might evolve and achieve scale to benefit the cause of financial inclusion. UIDAI’s Aadhar project (Aadhar, UIDAI) is using fingerprint and iris recognition technologies to rollout unique identification for 700 million people in India. This has the potential of addressing the severe challenges associated with identification of individuals for financial services. Interbank mobile payment system (IMPS), a service developed by NPCI offers instant interbank electronic fund transfer through mobile on 24x7 basis. Mobile ATMs are being adopted by several institutions and undergoing constant innovation. RFID and NFC based technologies integrated with mobile technologies are evolving.

TECHNOLOGY OPTIONS

AT THE BACK END

As law mandates, any transaction on an account involving cash has to be made within the physical premises of the bank. The Reserve Bank of India has permitted the appointment of Business correspondents to accept deposits or make cash payments on behalf of banks provided it is updated at the banking site within 24 hours time frame. So with the help of modern information technology and managerial capabilities of business correspondents, banking functionalities can be easily extended to remote regions and transaction data can be uploaded at the banking site either online or offline.

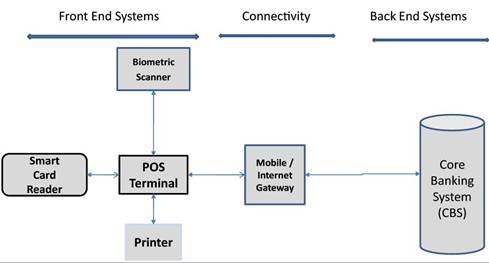

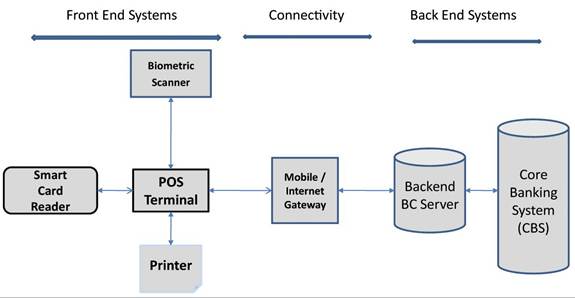

In case of online BC’s system is directly connected to the Banking site and in case of offline the data is stored temporarily at the BC’s Backend Server and later on (may be at the end of the day) it is transported to the Core Banking System (CBS). Based on these it can be Tier 2 (Figure 4) (when no storage server is needed, financial data directly being transferred to CBS) or Tier 3 (Figure 5) Architecture (in case of offline, when storage server is needed to store transactions temporarily).

No-one technology has emerged that can be best suited for the purpose. Few technology options at the front end and back end hold the promise of

Figure 4. Tier 2 architecture for back-end processing (on-line with direct integration through service providers)

Figure 5. Tier 3 architecture for back-end processing (off-line with indirect integration though service providers)

enabling. Technologies will also need continuous improvement and innovation to meet the demand of more complex products and to keep pace with growing business.

CASE STUDY

As a result of strong will of Government and after realizing the great potential of mobile technology to provide efficient low cost services at the bottom of pyramid, several public sector banks like State Bank of India, Union Bank of India, Axis Bank, Andhra Bank, Punjab National Bank (list is too long..) have set up or are in the process of setting up mobile phone based micro banks. Even telecom providers such as Bharti, Airtel, Vodafone and reliance Communications have tied up with banks to extend their mobile remittance services to rural areas (Davis & Owens, 2009). Several technology firms such as Ekgaon Technologies and Spanco systems have also stepped up to offer mobile banking tools.

Eko India Financial Services Pvt. Ltd. is another business correspondent (BC) financial service, for State Bank of India (SBI) and ICICI Bank, India’s top two largest banks, and provides no-frills bank accounts and deposit, withdrawal and remittance services to customers (nearly 80% of whom are migrants or the unbanked section of the population) through mobile banking. They have seen a rapid growth in mobile transaction volumes in select corridors (New Delhi - Bihar) after launching domestic remittance product “Tat- kal” from SBI. Eko enables customers to conduct financial transaction at a neighbourhood retailer by leveraging USSD technology while providing the security of a commercial bank

Technology companies FINO and A Little World (ALW) are also using the Business Correspondent (BC) model to deliver NREGA wages and pensions in several districts of Andhra Pradesh. Before processing payments, FINO/ALW collect fingerprint and other KYC data from each beneficiary. Payments are delivered on behalf of banks by local agents using a biometric enabled transaction processing (POS) device. FINO/ALW provide smartcards to each beneficiary. They have witnessed huge volumes of pro-active client enrolments and EBT transaction by rural beneficiaries receiving social payments - employment wages (NREGA) or old age pension funds.

FINO uses Tatkaal smart-card based product for remittance purposes. They provide end to end technology solutions like flexible saving schemes, loans, insurance, remittances using Biometric identification enabled hand held devices and mobile handsets, facilitating transactions at the customers’ doorstep through agents.They have also enabled cashless and paperless insurance processing to effectively reach at the bottom of pyramid customers.

ALW is India’s first domestic payment system with specific focus on reaching out to masses with lowest available communication infrastructure. The main technology focus of ALW is on biometrics based ID, RFID smart cards, and NFC (Near Field Communication) mobile phones.

MAJOR LEARNINGS

Today a wide range of technologies are available that can address requirements for financial inclusion in parts. But no -one technology has emerged that can be best suited for the purpose. These options co-exist in various forms with limited standardization, challenges in terms of achieving interoperability, critical mass and higher costs. Recognising client needs, their context, drivers and influencer’s and building financial services strategy on these is critical for succeeding in the long run. Technology can be a major enabler or handicap. The major attributes that an appropriate technology needs to have are (Hoffmann, 2006):

• Suitable: A key driver for choice of technology is suitability to the business model - clients, agents, products offered, policy compliance. No one size fits all and a technology working well in one context or environment might be a misfit for a similar purpose in another environment. Philippines’s GCASH and SMART find menu driven formats to have proven very user friendly, whereas due to illiteracy reasons, but these had limited uptake in India. Eko (Bharathan & Bhargava, 2010) has instead found USSD to be more promising. A combination of mobile and POS/ card based with bio-metric authentication solutions might work better in fulfilling the unique needs for certain demographics. Cost Effective: Technology constitutes a large component of cost of delivery of financial services and hence extremely important to be managed well. USSD & SMS formats exhibit the promise of being more cost-effective, provided other considerations like usability, security, reliability are met. MNOs prefer SIM based solutions, which apart from being more cost-effective; allow market differentiation and client “stickiness/retention” also through walled- garden approach (Mobee Bank, 2008). Secure: Security needs to be viewed from two perspectives (a) technology security and (b) human ignorance or negligence. Technology has evolved considerably and offers reasonable secure and idiot-proof solutions, provided the right processes in place. POS with biometrics has worked out better where authentication becomes vital, as with government payments. In South Africa a bank using USSD2 has not faced a single case of fraud vis-a-vis ATM and POT which can be hacked more easily (Stone & Grossman, 2009). Economies with lower literacy levels face the challenge of client ignorance or negligence. Needing assistance to fulfill financial transactions they end up disclosing PINs and passwords.

Proven and Scalable: Scalability is a key consideration as market demands can be unpredictable and institutions struggle to respond (GSM Association, 2010). Technology and processes often limit the much-needed and rapid scale-up or down. Telenor witnessed a demand of 2.0 million clients within weeks of launch of service. Adopting proven technologies can mitigate these risks with the added advantage of lower costs driven by the benefits of volumes and scale. Several institutions and technol-

ogy providers are experimenting with completely new technologies which are nascent and yet to be proven at any scale.

• Longevity: Every technology has a shelflife and eventually becomes obsolescent or is succeeded by the next generation. With 3G and 4G networks growing rapidly and a strong emphasis on http with Java and Android handsets, there is a great scope for USSD, SMS and STK based applications. MNOs have greater flexibility and deeper pockets to drive the technology decisions.

Investing in skill and capacity building to enable financial and technology illiteracy, overcoming language barriers, developing selling and servicing skills, managing risks, establishing controls and ensuring compliance are the other major challenges.

CONCLUSION

Technology has a major role to play in not only financial inclusion but inclusive growth of the excluded. Over the years technology evolution has enabled overcoming several handicaps and challenges which previously prevented financial services to be extended far and wide. Enabling low-value high-volume transactions to be made possible, lowering capital expenditure and operating costs, automation of processes, enhancing security and reliability, safeguarding consumers and enhancing trust, enhancing service levels are some of the factors that technology interventions have helped improve. However there is no technology silver bullet that can be a panacea for all challenges. Front and back-end technologies have provided solutions to many issues nevertheless these have been island solutions addressing issues in silos but not comprehensively. Innovations around a more comprehensive framework are still underway and might lead to a more holistic solution in times to come.

REFERENCES

Adams, N., Johnson, G., Matejic, P., Murray, C., Toufexis, N., & Whatley, J. (2008). Households below average income: An analysis of the income distribution. London, UK: Department for Work and Pensions.

Affleck, A., & Mellor, M. (2006). Community development finance: A neo-market. Journal of Social Policy, 35(2), 319. doi:10.1017/ S0047279405009542

GSM Association. (2010). Mobile signatures whitepaper: Best practises.

Balmer, N., Pleasence, P., Buck, A., & Walker,

H. C. (2005). Worried sick: The experience of debt problems and their relationship with health, illness. Social Policy and Society, 5(1), 39-51. doi:10.1017/S147474640500271X

Bharathan, V., & Bhargava, S. (2009). How inclusion centred financial infrastructure can change the lives of 300 million Indians. The EKo series on Financial Inclusion, India.

Bharathan, V., & Bhargava, S. (2010). Anti money laundering and combating the financing of terrorism. The EKo series on Financial Inclusion, India.

Borghoff, T. (2011). The globalisation of firms as a social evolutionary process. [IJABIM]. International Journal of Asian Business and Information Management, 2(2), 18-33. doi:10.4018/ jabim.2011040102

Chakrabarty, K. C. (2006). Financial inclusion concepts, issues and roadmap. India: IDRB.

Cheney, J. S. (2008). An examination of mobile banking and mobile payments: Building adoption as experience goods. Philadelphia, PA: Federal Reserve Bank of Philadelphia.

Cirasino, M., & Jose, A. (2009). Measuring payment systen development. World Bank Group, Access Finance. I(27).

Clark, A., Forter, A., & Reynolds, F. (2005). Banking the unbanked - a snapshot.

Davis, B., & Owens, J. (2009). POS vs. mobile phone as a channel for m-banking. India: Microsave.

Hannig, A., & Jansen. (2010). Financial inclusion and financial stability: Current policy issues. Asian Development Bank Institute ADBI Working Series, No. 259.

Heyer, A., & Mas, I. (2010). Seekingfertile grounds for mobile money. Lydian Payments Journal.

Hoffmann, J. (2006). Issues in mobile banking - Implementation choices. Microsave (Market-led solutions for financial services). India.

ICICI Bank’s Strategy. (n.d.). ICICI Bank’s strategy for promotion of financial inclusion.

Ketley, R. (2009). Does mobile banking require a card. India: Micro Save.

Kumar, K., & Mino (2011). Five business case insights on mobile money. CGAP - Consulative Group to Assist the Poor. Learning from local action developing national solutions. Toynbee Hall.

Mas, I. (2008). Being able to make (small) deposits and payments, anywhere. CGAP - Consulative Group to Assist the Poor.

Mas, I. (2009). The economics of branchless banking. MIT Press Journals INNOVATIONS, 4(2), 75. doi:10.1162/itgg.2009.4.2.57

Mas, I., &Siedek, H.(2009). Banking through networks of retail agents. Consulative Group to Assist the poor

Mas, I., & Radcliffe, D. (2010). Mobile payments go viral: M-PESA in Kenya. Consulative Group to Assist the Poor.

Matthews, B. H., Musoke, C., & Green, C. (2010). Group savings and loans associations: Impact study. DAI.

Mobee Bank. (2008). A complete mobile banking solution. Manam Infotech, India. http://manam- tech.com/

Mukesh, & Wright, G. (2009). Interbank mobile payment system: Will it catalyse financial inclusion? Microsave, India.

Nelson, J., Ishikawa, E., & Geaneotes, A. (2009). Developing inclusive business models: A review of Coca-Cola’s manual distribution centers in Ethiopia and Tanzania. Harvard Kennedy School.

Nyangosi, R., Arora, J. S., & Singh, S. (2009). The evolution of e-banking: A study of Indian and Kenyan technology awareness. International Journal of Electronic Finance, 3(2), 149-165. doi:10.1504/IJEF.2009.026357

Okyere, N. Y. D., Gloria, K. Q. A., & Kwamena, M. N. (2011). The effect of marketing communications on the sales performance of Ghana Telecom. International Journal of Marketing Studies, 3(4). doi:10.5539/ijms.v3n4p50

Ravi, S. P., Jain, R. K., & Song, W. (2011). IT outsourcing strategies: The case of Indian banking sector. [IJABIM]. International Journal of Asian Business and Information Management, 2(3), 27-39.

RBI. (2009-2010). Report on trend and progress of banking in India. Reserve Bank Of India.

Roman, P. B. (2009). Mobile phone/branchless banking andfinancial inclusion in the Philippines. World Bank, ISBN Number: 978-0-8213-7754-3, 2009.

Saeed, S., Rohde, M., & Wulf, V. (2012). IT for social activists: A study of world social forum 2006 organizing process. [IJABIM]. International Journal of Asian Business and Information Management, 3(2), 62-73. doi:10.4018/ jabim.2012040106

Shahid, Q. (2010). Understanding branchless banking business models -international experiences. CGAP- Consulative Group to Assist the Poor.

Singha, R., & Gayithri, K. (2012). Government policy and performance: A study of the Indian engineering industry. [IJABIM]. International Journal of Asian Business and Information Management, 3(2), 10-22. doi:10.4018/jabim.2012040102

Soni, P. (2010). M-payment between banks using SMS [Point of View]. Proceedings of the IEEE, 98(6), 905. doi:10.1109/JPR0C.2010.2047216

Stone, R., Grossman, J., Breul, P., Carpio, A., & Cabello, M. (2009). Trade in financial services: Mobile banking in Southern Africa. The World Bank Mozambique.

Suoranta, M., & Mattila, M. (2004). Mobile banking and consumer behaviour: New insights into the diffusion pattern. Journal of Financial Services Marketing.

TRAI. (2010). The Indian telecom services performance indicators. Telecom Regulatory Authority of India.

Venkatesh, V., Morris, M. G., Davis, F. D., & Davis, G. B. (2003). User acceptance of information technology: Toward a unified view. Management Information Systems Quarterly, 27, 478.

Wilcox, H. (2011-2015). Mobile money transfers & remittances: Markets, forecasts & vendor strategies. Juniper Research

World Bank. (2008). Banking the poor: Measuring banking access in 54 economies. Washington, DC. doi: 10.1596/978-0-8213-7754-3

Yang, J. (2007). New issues and challenges facing e-banking in rural areas: An empirical study. International Journal Electronic Finance, 1(3).

Zhang, X. (2011). Social loafing in distributed organization: An empirical study. [IJABIM]. International Journal of Asian Business and Information Management, 2(4), 44-60. doi: 10.4018/ jabim.2011100105

This work was previously published in International Journal of Asian Business and Information Management (IJABIM), 4(1); edited by Patricia Ordonez de Pablos, pages 10-20, copyright 2013 by IGI Publishing (an imprint of IGI Global).

740