Chapter 36 Customers' Perspectives of Internet Banking Adoption in Developing Economies

G. Varaprasad

National Institute of Technology Calicut, India

R. Sridharan

National Institute of Technology Calicut, India

Anandakuttan B. Unnithan

Indian Institute of Management Kozhikode, India

ABSTRACT

The competition in the banking sector has increased dramatically from the past decade.

This increased competition environment in the financial service sector has resulted in the development and utilization of alternative delivery channels. The advancements and revolutions in the communication and information technology have changed the functional scenario of the banking sector significantly. Internet banking is a novel delivery channel of banking and has been found to be an optional channel for the traditional banking because of the savings in time, money and effort. Banks have become more and more competitive to meet the customers demand for ease of use, functionality, relative advantage, greater accessibility and the best of the services at a lower price. The objective of this study is to investigate the factors which influence the adoption of Internet banking adoption in private sector banks of India. Factors such as perceived usefulness, perceived ease of use, perceived risk, relative advantage and trialability have been found to be the determinants of Internet banking in the previous studies. A new variable called conspicuousness has been introduced in the present study. Such a study has not been reported in the literature in the Indian context. A model has been proposed and tested using various statistical techniques. The findings are of great use primarily for the banks which are planning to offer Internet banking services, and for already existing banks to focus on the gaps. This research article provides valuable insights into the underlying contextual factors of Internet banking behavior for researchers and practitioners. The outcome of the study can be used to formulate new marketing strategies to increase the customer base of Internet banking market.DOI: 10.4018∕978-1-4666-6268-1.ch036

.

INTRODUCTION

Businesses in the developing economies are highly reliant on information technology and communications to compete in the global market. Banks started relying on information technology and communications to penetrate the existing markets and to enter new segments. Globalization has resulted in foreign banks expanding their businesses across the world. The arrival of foreign banks into the Indian market with the latest information technology based services has pressed the Indian banks to follow the latest technologies in banking to counter the threat of competition. The arrival of foreign banks followed by an increase in the number of private banks has resulted in a stiff competition among the banks, to provide the best of the services to the esteemed customers. The Indian banking sector is going through a series of innovations in its operational aspects. With the growing demand for convenience products and services, banks are striving hard to maintain the equilibrium. The economic fluctuations in the markets may result in positive and negative shocks to the banks Nathan et al. (2010). These external shocks for the banks may be inevitable if the business and funding models are faulty Aidan et al. (2008). Fadzlan (2010) empirically finds that foreign banks have higher technical efficiency compared to their domestic bank counterparts. According to Jagdish et al. (2011) organizations have been investing heavily in building information links with their suppliers and buyers to reduce costs and lead times to improve the timely customized delivery of products and services. B anks are trying to differentiate their products and services to gain an advantage over their competitors, by trying to offer services at customer’s home. Even mobiles service providers have a large spectrum of financial service offerings to attract new customers and to also to retain the existing.

Today, bank consumers round the globe are looking for the ease and convenience of online banking to take care of their financial needs. People are being comforted by the newer methods and technologies of accessing the Internet to check the status of their finances by the click of a mouse. Internet has egressed as a convenient delivery channel for these service providers Arpan et al. (2012). The recent and rapid developments in communications and information technology have brought unprecedented change in the lives of the people as well for banks. Internet has touched almost all aspects of human lives including the way we live, shop, entertain and interact. With this rapid development in communication and information technology, various activities are handled electronically from the home or workplace. In fact, Internet is a global phenomenon, making both time and distance irrelevant. Gordian et al. (2011) states that service industries started investing in information technology to bring cost savings in their operations. It has emerged as a convenient channel for many service providers. Therefore, Internet definitely tries to influence the way people save and invest. The financial service providers, from the developed countries have been using Internet as a channel to deliver their services more effectively and efficiently. Internet banking is defined as the delivery of banking services to customers through the Internet Chi et al. (2007). Majority of the service providers from the developing countries started reaping the benefits by using Internet as a service channel. The adoption of agile technologies and methodologies by the managers made the information system, qualitative and foolproof Kenneth et al. (2010). The financial institutions use information technology as a tool to grant loans and maintain records of individuals and enterprises that have been evaluated as credible Tarik et al (2009). Tero et al. (2004) define Internet banking as the Internet protocol through which customers can use different banking services ranging from bill payment to making investments.

The costs of information technology appear to have a stronger positive impact on bank performance when there are greater environmental changes Abbas et al., (2012). Ruiliang et al. (2012) examines that, it is very much essential for banks to share the information between the online and traditional retailers for a profitable e-business. Internet banking is the tool which allows consumers to do the banking transactions from the comfort of a home with the help of an Internet connection. Internet banking uses more traditional technologies such as personal computers and Internet in order to pay bills, transfer funds and obtain account information Mavri (2006). The amazing characteristic of Internet banking is allowing the customers to manage their own accounts. The customer can monitor and control his finance such as money transfers, utility bill payments, fixed deposits etc from home with the help of Internet (Mukherjee and Nath, 2003). The benefits of Internet banking are vivid which add value to customers’ satisfaction in terms of quality of services as well to gain competitive edge over the competitors. Managing and integrating the financial data of the consumers globally is a major concern for banks as the data is spread worldwide. The diffusion of latest technology, computers and growth of Internet make customers crave for varieties of services and more of convenience.The diffusion of innovations model proposed by Rogers (1962) includes five characteristics such as relative advantage, compatibility, complexity, observability, trialability which influences the consumer acceptance of new products or services. The rate of adoption of innovation depends on the complexity of the innovation, the more complex is the innovation, the lower is its rate of adoption (Tornatzky and Klein, 1982). According to Black et al. (2001), it would take more time for the diffusion of innovations if the service is complicated and difficult to understand. These have given rise to the need for such a study on Internet banking in the Indian context.

Though numerous studies have been conducted on this topic before, still this research is not superfluous because Internet banking is a very vivacious in today’s scenario and hence it needs to be constantly updated and studied. This paper seeks further to understand the development of Internet banking in the Indian context through an investigation of the factors that influence customers’ acceptance of Internet banking services. Only the private sector banks of India have been considered in the present study. Intention to use Internet banking services has been taken as the dependent variable in the present study. This research reports the findings in the consumer adoption of Internet baking in India and also finds out the factors which influence the adoption of these services.The rest of the paper is organized as follows. Section 2 deals with the review of the relevant literature. Section 3 outlines the proposed research model and the hypotheses. Section 4 describes the salient aspects of data collection. Section 5 provides data analysis and results. Section 6 presents conclusions.

LITERATURE REVIEW

A significant number of studies do exist in the literature about Internet banking, but not many exist in the Indian context. Internet banking has gained a significant popularity in the recent past and hence there is a need of contributing to the literature on Internet banking. The literature about Internet banking is reviewed and summarized in this section. Internet banking channel has been found out to be the cheapest delivery channel for delivering the banking products and services once established (Sathye, 1999). The lack of awareness about the benefits offered by Internet banking services and security concerns have been found out to be the impediments for the adoption of Internet banking services by consumers. The objective of Internet banking is to provide financial services to consumers round the clock from any remote location across the globe. Hence, in order to be successful in providing these services, banks are keen to understand the reasons for adoption of Internet banking services.

This has led to the enormous research in the field of banking. Recent literature on banking industry reveals that several researchers have investigated the adoption of Internet banking. It has been proved that Internet banking channel is the cheapest delivery channel for banking products once established. Cost savings, time and freedom from place have been found to be the main reasons for the acceptance of Internet banking (Black et al., 2002). Several studies indicate that perceived usefulness and perceived ease of use are the crucial factors for any innovation or technology acceptance which was adopted from the technology acceptance model proposed by Davis (1989). Perceived usefulness has been defined as the degree to which a person believes that using a particular system would enhance his/her job performance (Davis, 1989). Whereas perceived ease of use is the degree to which a person believes that using a system would be free of effort Davis (1989).Kolodinsky et al. (2004) investigated the effect of the factors such as relative advantage, complexity, compatibility, observability, risk tolerance, and product involvement on adoption. Customers comprehend Internet banking transactions to be risky and more prone to fraud as there is a monetary value involved. Therefore, perceived risk has been found to be one of the major factors which hinder the acceptance of Internet banking (Sathye, 1999; Tan and Teo, 2000). Perceived risk may include financial, physical, or social risks which are associated with trying an innovation (Polatoglu et. al. 2001). Bauer (1960) defines perceived risk as the risk involved in any action of a consumer that will produce consequences, which cannot be anticipated with certainty, and some of them are likely to be unpleasant. Walker et al. (2002) state that customers are worried that technology based service delivery systems will not work as expected. If the level of willingness to take risk exceeds the level of perceived risk only then consumers adopt Internet banking services. The opportunity to try an innovation is an effective way of reducing perceived risk and hence may lead to adoption of the innovation. According to Rogers (1983), consumers might adopt an innovation if they are given the opportunity to try the innovation. Gerrard et. al. (2003) defines trialability as the degree to which an innovation may be experimented with on a limited basis. Tan and Teo (2000) suggest that by trying a technology users feel more comfortable with the innovation and are more likely to adopt it.

Ndubisi and Sinti (2006) linked compatibility, complexity, trialability and risk to Internet banking adoption. The above factors supported the Internet banking adoption along with the moderating variables such as education, exposure to IT and usage frequency. Relative advantage has been found to be an important element in the adoption of Internet banking. It is often referred to as convenience, cost, time and effort savings with a decrease of discomfort in the adoption of an innovation (Rogers, 1983). Internet banking has been found to be hassle free and more advantageous compared to other banking options. (Black et al., 2001). Derrick (2012), consumers consider not only the relative advantage afforded by currently available products, but also the relative advantage expected from future generation products. It is presumed that a consumer who perceived Internet banking to advantageous over other banking options would adopt the services. Guriting and Ndubisi (2006) found perceived usefulness and perceived ease of use as the strong determinants of behavioural intention to adopt online banking. A high visibilty of the Internet banking services in the media is termed as conspicuousness which has been derived from the model of diffusion of innovation (Rogers, 1983). Rogers (1983) considers visibility as observability and later Moore and Benbasat (1991) redefine it as two constructs namely visibility and result demonstrability. But, Black et al., (2001) find that a simple visibilty has no effect on the adoption of any innovation. In the present research, a new construct called conspicuousness which means a high level of visibility has been introduced. The utilization of the traditional theoretical models with minor modifications and variety of analyses in the Indian context makes this study unique. This study focuses on individual perspective and proposes to identify factors that influence adoption and use of Internet banking services by customers of private sector banks in India.

AN OVERVIEW OF BEHAVIOURAL THEORIES OF ADOPTION

The behavioural theories that have achieved popularity in the study of technology adoption behaviour are discussed below.

1. Theory of Reasoned Action (TRA): Proposed by Ajzen and Fishbein (1975) explains and predicts the determinants of intended behaviour of individuals.

2. Technology Acceptance Model (TAM): Proposed by Davis (1989) to address, why users adopt or decline information technology.

3. Theory of Planned Behaviour (TBP): Developed by Ajzen (1991) by adding a new construct - perceived behavioural control to TRA.

1. Theory of Reasoned Action

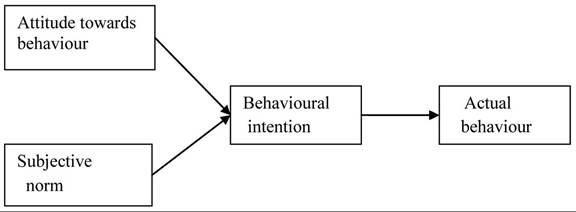

In this theory, a person’s attitude towards behaviour consists of a belief that particular behaviour leads to a certain outcome and an evaluation of the outcome of that behaviour. If the outcome seems beneficial to the individual, he or she may then intend to or actually participate in a particular behaviour. Subjective norm is a person’s perception of what others around them believe that the individual should do. That is, whether or not a person participates or intends to participate in any behaviour is influenced strongly by the people around them. The behavioural intention is affected by the attitude towards behaviour and subjective norm as shown in Figure 1.

2. Technology Acceptance Model

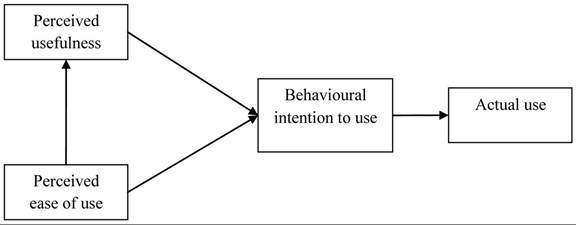

The technology acceptance model (TAM) developed by Davis (1989) was adapted from TRA (Fishbein & Ajzen, 1975). The objective of TAM is to provide an explanation of user’s acceptance and usage behaviour across a variety of end-user computing technologies (Davis, 1989; Davis et al., 1989). Among other technology acceptance and diffusion models, TAM is arguably the approach most widely accepted and used by information system researchers. TAM postulated that user acceptance of a new technology is determined by their behavioural intention to use the system, which can be explained jointly by user’s perception about the technology’s usefulness and attitude towards the technology use. Attitude is jointly influenced by two behavioural beliefs, perceived usefulness and perceived ease of use as shown in Figure 2.

Davis (1989) defines perceived usefulness as the degree to which a person believes that using a particular system will enhance his or her perfor-

Figure 1. Theory of reasoned action (Source: Fishbein and Ajzen, 1975; Ajzen, 1980)

Figure 2. Technology acceptance model (Source: Davis, 1989)

mance, while the perceived ease of use is defined as the extent to which a person believes that using a particular system is free of effort.

3. Theory of Planned Behaviour

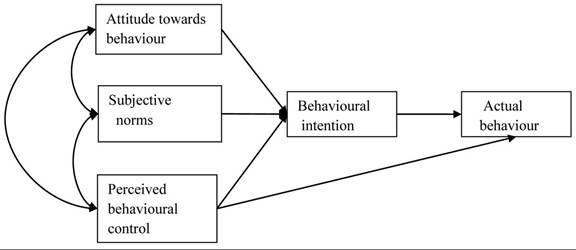

Theory of planned behaviour is the successor of theory of reasoned action proposed by Ajzen and Fishbein (1975, 1980). This succession was the result of the discovery that behaviour appeared to be not 100% voluntary and under control. This resulted in the addition of perceived behavioural control and this theory was called the theory of planned behaviour. TRA has been successfully applied to predict behaviour and intention in a variety of domains. Despite strong predictability of TRA, it became problematic as most of the researchers found subjective norms on behavioural intention to be insignificant, while some other authors found the opposite. Hence, a new construct has been added to the theory of reasoned action. In combination, the attitude towards the behaviour, subjective norm, and perception of behavioural control, leads to the formation of a behavioural intention as shown in Figure 3.

PROPOSED RESEARCH MODEL

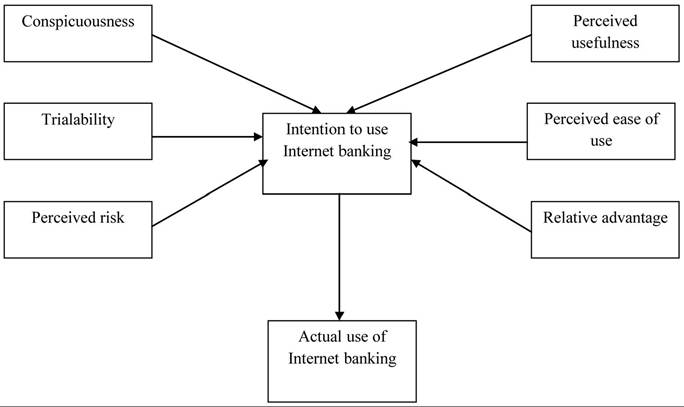

From the literature review and the various behavioural theories of adoption, the crucial factors for the adoption of Internet banking services have been identified as perceived usefulness, perceived ease of use, perceived risk, relative advantage, trialability, and conspicuousness. The following hypotheses have been formulated and tested. Figure 4 illustrates the proposed research model.

Figure 3. Theory of planned behaviour (Source: Ajzen, 1991)

Figure 4. Proposed research model

Dependent Variable: Intention to Adopt or use Internet Banking

The dependent variable is the intention to use or adopt Internet banking services. Ajzen (1991) predicted behavioural intentions by using attitudes, subj ective norms and perceived behavioural control. The more favourable the attitude and subjective norm with respect to behaviour, and the greater the perceived behavioural control, the stronger should be an individual’s intention to perform the behaviour under consideration (Ajzen, 1991).

Independent Variables: The independent variables in the study are perceived usefulness, perceived ease of use, perceived risk, relative advantage, trialability and conspicuousness.

Research Work in Brief: The sequential process involved in this research work is enumerated as given:

Formulation of Hypotheses Data collection and Validation Hypothesis Testing using Statistical Analyses

Formulation of Hypotheses

Perceived Usefulness (PU)

Davis (1989) defines PU as the degree to which a person believes that using a particular system would enhance his or her job performance. From the technology acceptance model proposed by Davis (1989), it is evident that PU is a significant factor affecting acceptance of an information system. Further, from the prior studies on Internet and Internet banking, perceived usefulness has been found to be an important determinant in the adoption of Internet banking services. So, in the context of Internet banking, perceived usefulness may be explained as performing the banking tasks anytime and from any location. Therefore, the following hypothesis has been tested:

H1: Perceived usefulness will have a positive effect on the intention to use Internet banking.

Perceived Ease of Use (PEOU)

Davis (1989) defines PEOU as the degree to which a person believes that using a system would be free of effort. From the technology acceptance model, PEOU is a major factor which affects the acceptance of information system (Davis et. al., 1989). In the context of Internet banking, perceived ease of use may be explained as using a system which is perceived to be easier to use than the conventional one. A significant number of studies suggested that perceived ease of use influences intention (Agarwal and Prasad, 1997). Thus, the following hypothesis has been proposed:

H2: Perceived ease of use will have a positive effect on the behavioral intention to use Internet banking.

Perceived Risk

Perceived risk, in the context of Internet banking may be associated with the financial loss as a result of using the services or with the electronic delivery channel. Black et. al. (2001) analyzed perceived risk in terms of risk of error and the level of security. A large number of studies have found that perceived risk is one of the maj or factors affecting user adoption of Internet banking. Thus, the following hypothesis has been formulated:

H3: Perceived risk will have a negative effect on the behavioral intention to use Internet banking.

Relative Advantage

Rogers (1962) defines relative advantage as the degree to which an innovation is perceived as being better than the idea it supersedes. Relative advantage in the context of Internet banking may be explained as allowing customers to access their bank accounts from any location and at any time of the day in contrary to the traditional banking. Tornatzky et. al. (1982) finds relative advantage to be an important factor in determining the adoption of new innovations. Also, a large number of studies have found relative advantage as a crucial factor in the adoption of Internet banking. This leads to the following hypothesis:

H4: Relative advantage will have a positive effect on the behavioural intention to use Internet banking.

Trialability

According to Rogers (1983), consumers might adopt an innovation if they are given the opportunity to try the innovation. Gerrard et al. (2003) define trialability as the degree to which an innovation may be experimented with on a limited basis. In the context of Internet banking, trialability can be viewed as the ability to access one’s own account and carrying out the banking transactions on a trial basis preferably at bank premises with the help of bank personnel who will be able to demonstrate how it works and the benefits it offers. This reduces the fear of adopting Internet banking services and encourages the potential customers to adopt it. Thus, the following hypothesis has been tested:

H5: Trialability will have a positive effect on behavioral intention to adopt Internet banking.

Conspicuousness

Conspicuousness can be defined as high visibility. It can be viewed as the coverage of Internet banking in the media i.e. attracting the attention of the society. With such an exposure of Internet banking, potential customers could gain knowledge about the services and its benefits. If such information about the services and benefits can be shared with friends and colleagues, then there is a chance of adoption. Thus, the following hypothesis has been tested:

H6: Conspicuousness will have a positive effect on behavioral intention to adopt Internet banking.

Data Collection

In this research, questionnaire has been used as a data collection tool to meet the objectives framed. The data for this study has been collected by means of a survey conducted in a metropolitan city in India, with the help of a questionnaire. The design of the questionnaire is to be taken care in all aspects such as instructions, appearance, order and an expression of appreciation for the help rendered by the respondent in filling up the questionnaire. A five point Likert scale ranging from strongly agree to strongly disagree are used as a basis to know the respondent’s views in the present research.

Filled in questionnaires were obtained from three different locations i.e., colleges, corporate offices and banks. This results in a sample that is well distributed in terms of demographics. Convenience sampling has been used in this present study on Internet banking.

A total of 450 questionnaire forms were delivered to the customers of private sector banks, out of which 347 filled in forms were received giving a response rate of 77 percent. After careful screening and scrutiny, questionnaire with incomplete and vague responses were discarded and were not included in the analysis. The questionnaire consists of questions that are related to demographic information, the possible factors affecting the acceptance of Internet banking and the use of Internet banking services.

The questionnaire has been developed and tested with a focus group consisting of banking professionals. The focus group verified that the hypotheses developed might be the affective factors in explaining the adoption of Internet banking. Based on the feedback from the focus group, the questionnaire was modified. Before proceeding with the main study, a pilot study is conducted. A pilot study is a survey on a small scale as a trial prior to the main survey that tests the questionnaire. To refine the questionnaire, it is required to conduct a pilot survey. Poorly designed questionnaire leads to the collection of inappropriate or inaccurate data. Hence, it is not proper to assume that questions in the questionnaire are perfectly and accurately framed at the first attempt itself. Based on the feedback from the pilot study, the inappropriate and unclear items are dropped; the wordings of some of the questions have been changed to improve clarity and new items added. After making amendments, the new version is re-tested. After the completion of pilot study and focus group interviews, the questionnaire is assumed to be free from all sorts of errors and ambiguities.

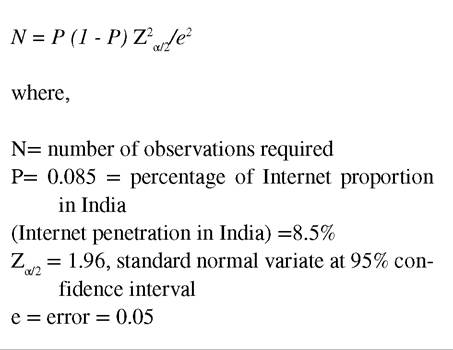

The sample size is calculated using the following general formula.

Thus, the sample required has been obtained as 119. In the actual study, the sample size is chosen as almost thrice the required sample size so that the resultant sample represents the entire population.

RESULTS AND ANALYSES

The data was edited, coded and analysed using Statistical Package for the Social Sciences-SPSS 16.0 for windows. All the statistical analyses have been performed using SPSS. The demographic profile of the respondents is shown in Table 1.

From Table 1, it is found that 41.9% of the respondents are in the age group 26-35 years,

Table 1. Characteristics of the sample

| Variable | Frequency | Percentage | |

| Gender | Male | 247 | 71.2 |

| Female | 100 | 28.8 | |

| Age | 18 - 25 | 145 | 41.9 |

| 26 - 35 | 138 | 39.8 | |

| 36 - 45 | 46 | 13.3 | |

| 46 - 55 | 9 | 2.3 | |

| 56-65 | 9 | 2.6 | |

| Education | Pre-degree | 2 | 0.6 |

| Degree | 137 | 39.5 | |

| Post Graduation | 140 | 40.3 | |

| Research | 25 | 7.2 | |

| Diploma | 43 | 12.4 | |

| Occupation | Student | 20 | 5.8 |

| Faculty | 39 | 11.2 | |

| Professional | 226 | 65.1 | |

| Supervisor | 8 | 2.3 | |

| Technician | 6 | 1.7 | |

| Business | 22 | 6.3 | |

| Retired | 26 | 7.5 | |

| Income (Rs./-) | < 1.6 Lakhs | 38 | 11 |

| 1.6 - 3 Lakhs | 85 | 24.5 | |

| 3 - 5 Lakhs | 130 | 37.5 | |

| 5 - 8 Lakhs | 62 | 17.9 | |

| 8 - 10 Lakhs | 15 | 4.3 | |

| > 10 Lakhs | 17 | 4.9 | |

| Internet usage | 1 - 2 Years | 16 | 4.6 |

| 2 - 3 Years | 27 | 7.8 | |

| 3 - 5 Years | 87 | 25.1 | |

| 5 - 7 Years | 92 | 26.5 | |

| > 7 Years | 125 | 36 |

71.2% of the respondents are male, 40.3% of the respondents are post graduates, 65.1% of the respondents are professionals/officers, 37.5% ofthe respondents are in the income range Rs.3 Lakhs - 5 Lakhs and 36% of the respondents have been using Internet for more than 7 years.

Reliability Analysis has been carried out to check the internal consistency of items. In order to use the measurement scales it is important that the reliability as well as the validity needs to be demonstrated. Hence, the construct reliability has been tested using the index of Cronbach’s alpha. Nunnally (1978) recommends the value of Cronbach’s alpha to be at least 0.7 to show high internal consistency. Cronbach’s alpha values of the factors are shown in Table 2.

In the present study, the Cronbach’s alpha values of all the factors have been found to be higher than the recommended value which shows a high internal consistency of the measures.

Validity is arguably the most important criteria for the quality of a test. It refers to whether or the test measures what it claims to measure. In this study, factor analysis is employed to establish the construct validity. Before proceeding with the factor analysis, Kaiser-Meyer-Olkin (KMO) and Bartlett’s sphericity tests have been performed to find the appropriateness of data for factor analysis. The Kaiser-Meyer-Olkin (KMO) measure more than 0.7 indicates that it is appropriate to use factor analysis. A confirmatory factor analysis has been conducted on the items comprising perceived usefulness, perceived ease of use, perceived risk, relative advantage, trialability, conspicuousness and intention to use. The Kaiser criteria of eigen values greater than 1 has been used to determine the initial number of factors to retain. The Kaiser-

Table 2. Cronbach alpha values

| Factor | Cronbach Alpha Value |

| Perceived usefulness | 0.854 |

| 0.883 | |

| Perceived risk | 0.810 |

| Relative advantage | 0.931 |

| Trialability | 0.778 |

| Conspicuousness | 0.833 |

| Intention to adopt/use (dependent variable) | 0.837 |

Meyer-Olkin (KMO) measure was 0.833. From the Bartlett’s sphericity test, the value of chi-square is found to be 7251 with a significance of 0.000. Hence, the constructs have been found to be valid.

Multi-regression analyses are performed to test the hypotheses and to examine the associations among the constructs. The results have been reported in Tables 3, 4 and 5.

A linear multiple regression analysis has been carried out on the proposed model, where intention to use is the dependent variable and perceived usefulness, perceived ease of use, perceived risk, relative advantage, trialability and conspicuousness are the independent variables. From the ANOVA result shown in Table 4, it is

Table 3. Regression model

| Model | R2 | Adjusted R2 | Standard Error of the Estimate |

| 1 | 0.645 | 0.639 | 0.66406 |

evident that the model applied is significantly good enough in predicting the outcome variable. It can be observed that the p-value is statistically significant and the value of F computed is well above the F critical value at 95 percent level of confidence. Hence, the null hypothesis that there is no relationship between the dependent and independent variables is rejected. Therefore, it is concluded that there is a relationship between the dependent and independent variables.

From the results of regression analysis shown in Table 3 it is found that the coefficient of determination R2 is 0.645. This means that 64.5% of the variability in the dependent variable (i.e., intention to use Internet banking) can be explained by the independent variables such as perceived usefulness, perceived ease of use, perceived risk, relative advantage, trialability and conspicuousness. The R2 value and the adjusted R2 value are very close which implies that the model includes only the factors that are significant, i.e., the model is not over specified.

Table 4. ANOVA results

| Model | Sum of Squares | df | Mean Square | F | Sig. |

| Regression | 272.766 | 6 | 45.461 | 103.092 | 0.000 |

| Residual | 149.932 | 340 | 0.441 | ||

| Total | 422.698 | 346 |

Table 5. Regression results

| Model | Unstandardized Coefficients | Standardized Coefficients | t | Sig. | |

| B | Std. Error | Beta | |||

| (Constant) | 0.070 | 0.268 | 0.263 | 0.793 | |

| Perceived usefulness | 0.504 | 0.059 | 0.423 | 8.490 | 0.000 |

| Perceived ease of use | -0.084 | 0.040 | -0.069 | -2.126 | 0.034 |

| Perceived risk | -0.044 | 0.042 | -0.034 | -1.030 | 0.304 |

| Relative advantage | 0.261 | 0.061 | 0.229 | 4.248 | 0.000 |

| Trialability | -0.031 | 0.048 | -0.021 | -0.638 | 0.524 |

| Conspicuousness | 0.277 | 0.057 | 0.248 | 4.887 | 0.000 |

Hence, the multiple regression equation is obtained as follows:

Intention to use Internet banking services =

0. 070 + 0.504*Perceived usefulness - 0.084 * Perceived ease of use - 0.044*Perceived risk + 0.261*Relative advantage -0.031*Trialability + 0.277*Conspicuousness

According to the hypothesis H1, perceived usefulness will have a positive effect on the intention to use Internet banking. From Table 5, perceived usefulness is found to be statistically significant at 0.05 level (β = 0.423, p = 0.000). Thus, the hypothesis H1 has been supported. This suggests that the bank customers perceive Internet banking to be useful.

The hypothesis H2 states that perceived ease of use will have a positive effect on the behavioral intention to use Internet banking. Table 5 reveals that perceived ease of use is found to be statistically significant at 0.05 level (β = -0.069, p = 0.034). Thus, the hypothesis H2 is supported. This suggests that the bank customers perceive Internet banking as easy to use.

According to the hypothesis H3, perceived risk will have a negative effect on the behavioral intention to use Internet banking. It is found from Table 5 that perceived risk is statistically insignificant at 0.05 level (β = -0.034, p = 0.304). Thus, the Hypothesis H3 is negated. This means that the bank customers are not finding Internet banking transactions to be risky. This may be because of the efforts taken by banks in making the Internet transaction more secure.

The hypothesis H4 states that relative advantage will have a positive effect on the behavioural intention to use Internet banking. The findings from Table 5 show that relative advantage is statistically significant at 0.05 level (β = 0.229, p = 0.000). Thus, the hypothesis H4 is supported. This means that bank customers are perceiving Internet transactions to be relatively advantageous than the traditional banking.

Hypothesis H5 states that trialability will have a positive effect on behavioral intention to adopt Internet banking. It is observed from Table 5 that trialability is statistically insignificant at 0.05 level (β = -0.021, p = 0.524). H5 is therefore negated. The possible reason for the failure of the hypothesis is lack of support from the banks to offer the services on a trial basis.

The hypothesis H6 states that conspicuousness will have a positive effect on behavioral intention to adopt Internet banking. Table 5 reveals that conspicuousness is found to be statistically significant at 0.05 level (β = 0.248, p = 0.000). Thus, the hypothesis H6 is supported. This means that the higher the visibility of the banks services in the public media, the higher would be the rate of adoption.

In summary, out of the six hypotheses, four were found to be statistically significant in this empirical study. Rejection of hypothesis H3 reveals that perceived risk has a positive effect on Internet banking. Hence, only one hypothesis H5 is rejected. The factors perceived usefulness, relative advantage and conspicuousness have been found to have a very strong relationship with intention to adopt Internet banking services.

CONCLUSION AND FUTURE RESEARCH DIRECTIONS

Information technology services are considered as the key drivers for the rapid changes globally. Internet banking is the most recent and innovative service which is the new trend among the consumers. In India, Internet banking is an uprising banking service and has not been widely accepted by customers because of various reasons. Many banks are striving hard to provide the best Internet banking services to their customers. It is important for bank managers to frame their problems appropriately and address them in a proper manner. Otherwise, the problems poorly addressed may create more problems and take longer time to fix in the long run (John, 2010). Hence, it is of prime importance for bank managers to identify the factors that influence the adoption of these services. The aim of this paper is to investigate the significant factors which influence the consumer’s adoption of Internet banking services. The results of this study show that perceived usefulness, perceived ease of use, perceived risk, relative advantage, and conspicuousness are the important determinants of Internet banking adoption. The findings clearly state that the factors which were discarded in the prior studies have shown a significant influence in the Indian context in this present study. This might be a result of the cultural and perceptual differences. As such, there is still room for further investigation into the adoption of Internet banking in India. We could investigate our research model in different time periods and make comparisons, thus providing more insight into the phenomenon of Internet banking adoption. Only private sector banks have been covered in the present study. An investigation of the consumer adoption of Internet banking services offered by public sector banks can be carried out. Further, a comparison of both public sector and private sector banks is an extensive area for future research. Also, a study on the perspectives of corporate banking customers can be an ideal work for future. Banks cannot presume that consumers are homogenous in terms of the attitudes and behaviors. Hence, research into the demographic and socio-economic factors is extremely important in enabling financial service providers to target specific segments of the customer base. The findings of this study are particularly important for banks to concentrate on the problem areas to attract more customers and to help decide how to allocate resources to retain and expand their customer base. Banks also need to concentrate on those factors which are really influencing the bank users in adopting Internet banking. With an increase in the penetration rate of Internet banking, the work force required in the banks and transaction costs can be reduced significantly. This research article provides valuable insights into the underlying contextual factors of Internet banking behavior for researchers and practitioners. The outcome of the study can be used to formulate new marketing strategies to increase the customer base of Internet banking market. Hence, banks should consider the importance of these factors for designing, implementing, maintaining and promoting their products and services.

ACKNOWLEDGMENT

The authors express their sincere thanks to the referees and the editor for their valuable comments which have helped to bring this chapter to the present form.

REFERENCES

Abbas, K., Mohammad, A. A., Marzyeh, M. G., & Masoud, A. M. (2012). Investigating the effects of information technology investment on bank performance: Considering the role of environmental dynamism and strategy. International Journal of Applied Decision Sciences, 5(1), 32-46. doi:10.1504/IJADS.2012.044945

Agarwal, R., & Prasad, J. (1997). The role of innovation characteristics and perceived voluntariness in the acceptance of information technologies. Decision Sciences, 28(3), 557-582. doi:10.1111/j.1540-5915.1997.tb01322.x

Aidan, O., & Francisco, J. S. A. (2008). Information and intertemporal decision processes in banking: The run on Northern Rock. International Journal of Applied Decision Sciences, 1(4), 359-396. doi:10.1504/IJADS.2008.022976

Ajzen, I. (1991). The theory of planned behavior. Organizational Behavior and Human Decision Processes, 50(2), 179-211. doi:10.1016/0749- 5978(91)90020-T

Ajzen, I., & Fishbein, M. (1980). Understanding attitudes & predicting social behavior. Englewood Cliffs, NJ: Prentice-Hall.

Arpan, K. K., & Priyal, S. (2012). A model for bundling mobile value added services using neural networks. International Journal of Applied Decision Sciences, 5(1), 47-63. doi:10.1504/ IJADS.2012.044946

Bauer, R. A. (1960). Consumer behavior as risktaking. In R. S. Hancock (Ed.), Dynamic marketing for a changing world. Chicago: American Marketing Association.

Black, N. J., Lockett, A., Ennew, C., Winkl- hofer, H., & McKechnie, S. (2002). Modelling consumer choice of distribution channels: An illustration from financial services. International Journal of Bank Marketing, 20(4), 161-173. doi:10.1108/02652320210432945

Black, N. J., Lockett, A., Winklhofer, H., & En- new, C. (2001). The adoption of Internet financial services: A qualitative study. International Journal of Retail and Distribution Management, 29(8), 390-398. doi:10.1108/09590550110397033

Chi, S. Y., Grant, K., & Edgar, D. (2007). Factors affecting the adoption of Internet banking in Hong Kong - Implications for the banking sector. International Journal of Information Management, 27(5), 336-351. doi:10.1016/j. ijinfomgt.2007.03.002

Davis, F. D. (1989). Perceived usefulness, perceived ease of use, and user acceptance of information technology. Management Information Systems Quarterly, 13(3), 319-339. doi:10.2307/249008

Derrick, S. B. (2012). Consumer purchase decisions under asymmetrical rates of technological advance and price decline. International Journal of Strategic Decision Sciences, 3(2), 20-30. doi:10.4018/jsds.2012040102

Fadzlan, S. (2010). The evolution of Malaysian banking sectorls efficiency during financial duress: consequences, concerns, and policy implications. International Journal of Applied Decision Sciences, 3(4), 366-389. doi:10.1504/ IJADS.2010.036852

Gerrard, P., & Cunningham, J. B. (2003). The diffusion of Internet banking among Singapore consumers. International Journal of Bank Marketing, 21(1), 16-28. doi:10.1108/02652320310457776

Gordian, A. N., Bay, A., & Yongtao, H. (2011). A worldwide study of the impacts of information technology on healthcare costs. International Journal of Applied Decision Sciences, 4(2), 95128. doi:10.1504/IJADS.2011.039514

Guriting, P., & Ndubisi, N. O. (2006). Borneo Internet banking: Evaluating customer perceptions and behavioural intention. Management Research News, 29(1/2), 6-15. doi:10.1108/01409170610645402

Jagdish, P., & Navneet, V. (2011). Cost framework for evaluation of information technology alternatives in supply chain. International Journal of Strategic Decision Sciences, 2(1), 66-84. doi:10.4018/jsds.2011010104

John, D. (2010). Management theory: A systems perspective on understanding management practice and management behavior. International Journal of Strategic Decision Sciences, 1(3), 33-48. doi:10.4018/jsds.2010070103

Kenneth, E. K., Sue, K., & Julie, E. K. (2010). The impact of agile methodologies on the quality of information systems: Factors shaping strategic adoption of agile practices. International Journal of Strategic Decision Sciences, 1(1), 41-56. doi:10.4018/jsds.2010103003

Kolodinsky, J. M., Hogarth, J. M., & Hilgert, M. A. (2004). The adoption of electronic banking technologies by US consumers. International Journal of Bank Marketing, 22(4), 238-259. doi:10.1108/02652320410542536

Mattila, M., Karjaluoto, H., & Pento, T. (2003). Internet banking adoption among mature customers: early majority or laggards? Journal of Services Marketing, 17(5), 514-528. doi:10.1108/08876040310486294

Mavri, M., & Ioannou, G. (2006). Consumer perspectives on internet banking services. International Journal of Consumer Studies, 30(6), 552-560. doi:10.1111∕j.1470-6431.2006.00541.x

Moore, G. C., & Benbasat, I. (1991). Development of an instrument to measure the perceptions of adopting an information technology innovation. Information Systems Research, 2(3), 192-222. doi:10.1287/isre.2.3.192

Mukherjee, A., & Nath, P. (2003). A model of trust in Internet relationship banking. International Journal of Bank Marketing, 21(1), 5-15. doi:10.1108/02652320310457767

Nathan, L. J., & Khelifa, M. (2010). Testing for overreaction and return continuations in stock price index returns. International Journal of Strategic Decision Sciences, 1(2), 93-112. doi:10.4018/ jsds.2010040105

Ndubisi, N. O., & Sinti, Q. (2006). Consumer attitudes, system’s characteristics and internet banking adoption in Malaysia. Management Research News, 29(1/2), 16-27. doi:10.1108/01409170610645411

Nunnally, J., & Bernstein, I. H. (1994). Psychometric theory (3rd ed.). New York: McGraw Hill.

Petrus, G., & Nelson, O. N. (2006). Borneo internet banking: Evaluating customer perceptions and behavioural intention. Management Research News, 29(1), 6-15.

Polatoglu, V. N., & Ekin, S. (2001). An empirical investigation of Turkish consumers’ acceptance of internet banking services. International Journal of Bank Marketing, 19(4), 156-165. doi:10.1108/02652320110392527

Rogers, E. M. (1983). Diffusion of innovations. New York: The Free Press.

Ruiliang, Y., John, W., & Bin, Z. (2012). Is information sharing profitable in e-business age? International Journal of Applied Decision Sciences, 5(1), 1-10. doi:10.1504/IJADS.2012.044943

Sathye, M. (1999). Adoption ofinternet banking by Australian consumers: An empirical investigation. International Journal of Bank Marketing, 17(7), 324-334. doi:10.1108/02652329910305689

Tan, M., & Teo, S. H. (2000). Factors influencing the adoption of Internet banking. Journal of the Association for Information Systems, 1(5), 1-44.

Tarik, A., Hafsa, L., Samir, A., & Ali, D. (2009). A benchmark based AHP model for credit evaluation. International Journal of Applied Decision Sciences, 2(2), 151-166. doi:10.1504/ IJADS.2009.026550

Tero, P., Kari, P., Heikki, K., & Seppo, P. (2004). Consumer acceptance of online banking: An extension of the technology acceptance model. Internet Research, 14(3), 224-235. doi:10.1108/10662240410542652

Tornatzky, L. G., & Katherine, J. K. (1982). Innovation characteristics and innovation adoption implementation: A meta analysis of findings. IEEE Transactions on Engineering Management, 29(1), 28-43. doi:10.1109/TEM.1982.6447463

Walker, R. H., & Johnson, L. W. (2006). Why consumers use and do not use technology-enabled services. Journal of Services Marketing, 20(2), 125-135. doi:10.1108/08876040610657057

This work was previously published in Analytical Approaches to Strategic Decision-Making, edited by Madjid Tavana, pages 191-205, copyright 2014 by Business Science Reference (an imprint of IGI Global).