Chapter 35 Banks and People in the Development Process: A District-Level Analysis of the Banking Habits in India

Atanu Sengupta

Burdwan University, India

Sanjoy De

Burdwan University, India

ABSTRACT

Economic development is crucially an end product of mobilizing dormant savings into the fragrance of a new life - what is commonly called as investment.

Banks play a crucial role in this channelization. In an underdeveloped economy like India, there are many traditional avenues of savings (such as gold, land, livestock, real estate, and so on). There may be many motives why people opt for traditional avenues rather than formal banking. The traditional avenues are believed to be more trustworthy and down to earth. The strict rules and stereotyped functioning of the formal banks can make them uncomfortable to the people in the underdeveloped areas. Thus, a huge fund in India is caught in the web of informal banking streams. This chapter seeks to understand how far and to what extent these changes have occurred in India. First, the authors consider a case study from rural India that depicts disparate banking behavior of rural populace. Next, they use district level data on banking habits across all the states of India. The authors first note the pattern and distribution of banking habits of people across the subcontinent. They then try to assess the reasons behind such discrepancy.Introduction

Traditional macro economic theory asserts that the key to economic development is the availability of savings. An improvement in savings would release funds that can be invested. In all our stan

dard theories, the synchronization between saving and investment is automatic. In the neo-classical approach, the problem of investible fund is not put forth. In the Keynesian model, the matching between saving and investment is essential. But, this is only in the aggregative sense. Keynesian equilibrium is determined when demand for investible funds matches the supply, i.e.

saving. What these models safely assume is the working of a well-structured banking system, wherein the supply of investible funds is automatically directed towards its demand.DOI: 10.4018/978-1-4666-6268-1.ch035

.

In the modern economy households save while companies invest. It is certainly important that the aggregate saving equates aggregate investment as argued by the Keynesians. But this is half the story. Successful investment requires the collection of disparate savings of the families and its channelization to the investors. In modern parlance, we can designate it as a co-ordination problem. Text book macroeconomics does away with this co-ordination problem by assuming the functioning of a well-established banking system.

The problem became serious when the economists began to study the underdeveloped world. There, more often than not, savings are scattered and often in various static or ‘unusable’ forms (such as gold, properties of the religious institutions, land etc). This view of co-ordination failure is not new to the thinkers outside the hallowed boundary of economics. Francois Bernier was a French traveler who visited India during the reign of the Mughal emperor Aurangazeb. He was of the view that average Indians were very rich. Even a peasant woman used to wear earrings. But, there were little investing activities. People used to bury their valuable treasures under the earth. Thus they lost any chance of being invested and creating income and wealth.

This problem is still prevalent in the current Indian milieu. Lack of or absence of formal saving practices is still there in the country. Huge amount of money are still being saved informally. This huge informal saving is actually belittling the opportunity of capital and wealth creation. It is in turn hampering economic development in the country. In order to spread the banking services to the hitherto uncharted territories as well as to channelize the informal and unused savings in the country to the formal routes, the RBI is now vociferously preaching for ‘financial inclusion’.

In our paper we will try to decipher the reasons behind the lack of co-ordination in the country between savings and investment. In other words, we will try to find out the reasons behind lack of or absence of formal saving or institutional savings habits in the country. We will attempt to unravel the micro level indicators that have any bearing on the formal saving habits or the banking habits of the people in the country.

The paper is divided into 4 sections. Section 2 discusses a case study of disparate banking behavior. Next we consider the basic data that is used in the study as well as the methodology in section 3. The next section takes account of the analytics of disparate savings behavior. In section 5 we conclude.

2. CASE STUDY

In line with our scheme of things, here we incorporate a case study. The case study is based on a socio-economic study conducted by the Post Graduate students of the University of Burdwan in a cultivable area in Bolpur in Birbhum district during February 2013. The study is based on the data collected from 306 households coming from different villages within the Sian Muluk of Bolpur, Srineketan block.

The villagers in this are engaged in various types of semi-skilled and unskilled jobs. This includes working in agriculture, unskilled non-farm labor service, various types of petty businesses, services and others. Among the women there are many who remain as housewives. These people are not all of homogeneous categories. Out of the families surveyed, about 39% are above the official poverty line while 61% are below the poverty line (Table 1).

However, once we come to their source of loans, 16.81% depend on banks. This means about 83% of the total sampled households depend on

Table 1. Economic profile of the households surveyed

| No of Households | Percentage of Households | |

| APL | 119 | 38.89 |

| BPL | 187 | 61.11 |

| Total | 306 | 100 |

Source: A socio-economic survey conducted by the Department of Economics, Burdwan University

various sources of non-bank credit.

Among these sources, 0.88% comes from post office and 4.42% from panchayat. This roughly amounts to 5.3% from official sources. Among the remaining 78%, roughly 30% depends on moneylenders, 30% on chit funds and micro-finance and 7% from other sources (Table 2).Chit funds are unofficial loaning and depositing agencies in rural and semi-urban West Bengal. Originally, the word chit comes from ‘sheet of paper’. These are formed by an agreement between individuals who form Rotating Savings and Credit Institutions (ROSCAs).1 Each individual saves a fixed amount in the common pool during each month or at some common interval of time. A lottery is made at each meeting to decide who will receive the entire pooled amount as loan for a certain specified period. The person is liable to pay the money back and the pot is again distributed.

However, the chit funds have expanded its role beyond the legal limits of ROSCAs, as specified by the SEBI. In rural Bengal, these unauthorized chit funds play a substantial role in the informal market. They attract huge deposits by alluring a high rate of interest. They also charge a high rate on interest on the loan given by them.

The question arises as to why the residents in rural and semi-urban areas depend so heavily on non-bank institutions. In our case study we found at least three main reasons for this.

The first reason is the easy accessibility of these loans. Most of the loans are so small that commercial bankers would not feel profitable to release them. Our data shows that about 97% of the loans are of less than or equal to Rs 50,000 only. Again, 52% of the loans amounts to less than or equal to Rs 10,000. There are loans even below Rs 1000 (about 8%). It is clear that no commercial bank would offer this small amount of loan (Tables 3 and 4). Added with this, is the fact that a huge amount of loan is disbursed without any collateral (63.16%).

Personal acquaintance, informal bonding etc. are more important to obtain a loan than collateral.

In the rural and semi-urban areas, even the middle and rich families might not be able to procure collateral in the appropriate form as required by the formal loaning agency.The third important aspect of informal loan is its flexibility. In many cases, the purpose for which the loan is taken and its actual use are in complete contrast with one another. For example, though only 4.23% of the borrowers state agriculture as the purpose of taking out the loan, the actual utilization of the loan for agricultural purpose is roughly 39%. Similarly, the amorphous other categories (that mostly includes expenditures on societal duties such as marriage of sisters, daughters etc.) accounts to only 7.62% as the declared purpose for loans, which actualizes to 24%. Faced with uncertainties, the rural and semi-urban families often have to re-orient their expenditure plans. Such re-orientation requires flexibility in

Table 2. Source of loans

| Money Lenders | Chit Funds | Panchayat | Self-Help Group | Post Office | Bank | Relatives | Land Lords |

| 30.08% | 30.08% | 4.42% | 10.61% | 0.88% | 16.81% | 6.19% | 0.88% |

Source: A socio-economic survey conducted by the Department of Economics, Burdwan University

Table 3. Amount of loans

| Amount of Loans | Percentage of Households |

| Rs 0 - Rs 1000 | 7.64 |

| Rs 1001- Rs 5000 | 19.50 |

| Rs 5001 - Rs 10,000 | 32.20 |

| Rs 10001-Rs 50,000 | 37.28 |

| Rs 50,001-Rs 4.50 lakh | 3.38 |

Source: A socio-economic survey conducted by the Department of Economics, Burdwan University

Table 4.

Loan with Collateral/no Collateral| Loan with Collateral | Loan with no Collateral |

| 36.84% | 63.16% |

Source: A socio-economic survey conducted by the Department of Economics, Burdwan University

loan use that is not possible in the formal sector (Tables 5 and 6).

Thus our case study reveals that it is not merely income that determines the use of formal banking. There are many advantages in the use of informal sources. These sources are flexible, easily accessible and somewhat non-structured. In many cases, when there is an urgent need of loans, the households have to depend on the informal sources for their only avenue. Many of these informal sources are a part and parcel of their lives. They meet these agents in their day to day activities of life. They believe them and depend upon them. Sometimes, they form social ties with the informal lenders. Formal loans, on the other hand, are a world apart. Unless the formal sector finds some innovative ways to attract the borrowers and the savers, the hope of financial inclusion will remain a distant dream.

3. SOME SALIENT FEATURES OF THE DATA USED AND METHODOLOGY

The empirical analysis requires data on various aspects of the saving behavior of people. Some of these can be gathered from the amenities data of the Indian census 2001. Another and more important source is the District Level Household and Facility Survey data of 2007-08 (DLHS 3). Both these data give the district level features. These two sets of data are combined together for our purpose.

From census 2001, we gather data on the total number of households availing banking services for 581 districts in India, coming from 34 states and union territories. We find out the proportion of households availing banking services in each of the 581 districts that we selected. In our study, we refer the proportion of households availing banking services as the dependent variable and we refer it as ‘bank’ in our study. We try to find out how ‘bank’ depends upon various other factors. From the census data, we get number of households according to the usage of various durable goods such as radio, transistor; television; telephone; bicycle; scooter, motor cycle, moped; car, jeep, van; and none of the specified assets. Finding the proportion of households who hold none of the specified assets and subtracting the proportion from one for each district, we derive an estimate of ‘assets’. It is anticipated that ‘assets’ and ‘bank’ are positively correlated. In other words, increased asset holding should require higher banking practices by the people.

Table 5. Purpose of loan

| Agriculture | Livestock Purchase | Durable Asset Creation | Education | Medical Purposes | Trade | Other Activities |

| 4.23% | 16.94% | 24.57% | 12.75% | 25.42% | 8.47% | 7.62% |

Source: A socio-economic survey conducted by the Department of Economics, Burdwan University

Table 6. Actual utilization of the loans

| Agriculture | Livestock Purchase | Durable Asset Creation | Education | Medical Purposes | Trade | Other Activities |

| 39.08% | 6.89% | 1.15% | 3.45% | 16.09% | 9.19% | 24.15% |

Source: A socio-economic survey conducted by the Department of Economics, Burdwan University

We have also used the District Level Household and Facility data of 2007-08 (DLHS 3) for our study. DLHS is a wonderful effort by the Ministry of Health and Family Welfare and the survey was conducted by the International Institute of Population Sciences. For this survey data was collected from over 0.72 million households cutting across 28 states and 6 union territories.

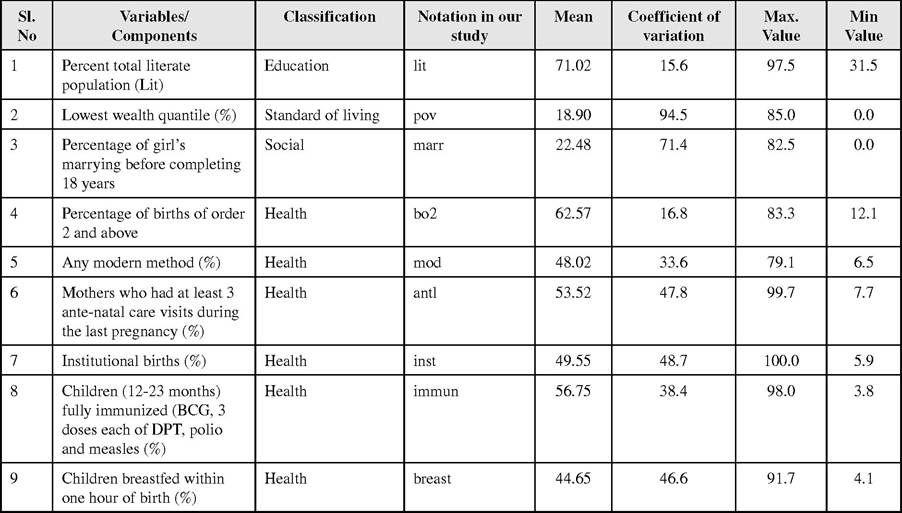

The survey was conducted on the basis of 17 parameters that include education, living standard and health. In our study, we have used data on 9 parameters. The parameters that are used in our study are presented in Table 7.

A careful look at the table brings out some important features of the data. For two variables - ‘pov’ and ‘marr’, the variability is more than 70%. Higher CV in the variable ‘pov’ implies widespread disparity in income of the people in the country. Higher variation in ‘marr’ implies a wide asymmetry in the development of social consciousness among the women.

In all other variables - ‘lit’, ‘bo2’, ‘mod’, ‘antl’, ‘inst’, ‘immun’, ‘breast’ - the variability is below 50%. Lowest variability is observed in the variable ‘lit’. It means that there have not been any significant fluctuations in the literacy level across different areas in the country. In ‘bo2’ also, there has not been any significant variation. A moderately higher degree of variation has been observed in the variables - ‘mod’, ‘anti’, ‘inst’, ‘immun’ and ‘breast’.

Table 7. Survey parameters in DLHS 3

Since the variable ‘bank’ is truncated at zero, the ordinary least squares will yield inconsistent results. For this we have to resort to the Tobit analysis. The variable ‘bank’ is a censored variable. This is not observable for families with no banking habits. The Tobit methodology is useful here.

However, before the Tobit regression, we used step regression technique to identify factors that are most relevant for the analysis. The step regression technique is a useful tool to combat the problem of multi-collinearity so common in the cross-sectional analysis. The variables are selected according to the improvement in the F- value. The set of independent variables may change from one regression to another depending upon the criteria of rejection by the step technique.

4. EMPIRICAL ANALYTICS OF THE DISPARATE SAVINGS BEHAVIOR

The variable that we identify as constituting the formal saving propensity is the ‘bank’. It is noted that there are a number of factors on which ‘bank’ depends. Firstly, ‘bank’ has correlation with the earning and wealth profile of families. Wealthier the family, higher should be the formal saving propensity. However, this text-bookish relationship between the earning capacity and the dependent variable ‘bank’ needs to be taken with a pinch of salt. Improvement of the family earning propensity increases the capacity to use formal banking system. However, there is no guarantee that the formal system will be used.

In a traditional society, there are numerous avenues of savings, most of them are informal in character. A potential saver has the option to choose between these various available avenues. In many cases, the potential savers may have an inherent distrust for the formal bankers. This distrust may be due to part-fear or due to part-bad experience in the past. The inflexibility of the formal banking system and its various requirements makes it less lucrative. For example, in order to save in the formal system, a potential saver has to devote both time and money. Informal options are available at his doorstep. Normally, formal banking system operates within a stipulated time. Most of its activities are limited within that time. On the contrary, informal sectors are more flexible. If I want to deposit money at the stroke of midnight, it is almost impossible to avail a formal bank. However, it is far easier if I approach an informal bank. Loan disbursement policies of the formal banks are more structured and generalized. On the other hand, informal loans are tailor-made to the recipient’s demand. Added to this, is the personal ties with the informal bankers that makes it seem more reliable2

Thus the relationship between the saving propensity in the formal sector has to be mediated through a number of variables. Many of them reflect the quality of life and awareness towards the modern system. We have considered 8 such variables (‘lit’, ‘marr’, ‘bo2’, ‘mod’, ‘antl’, ‘inst’, ‘immun’, ‘breast’). Two other important variables are ‘assets’ and ‘pov’. In order to find out the relationship, we have considered 3 types of regression. These regressions are based on the distinction between the variables ‘pov’ and ‘assets’. ‘Pov’ measures the percentage of families who are below the destitute levels. ‘Assets’ on the other hand refers to the measure of durable goods purchased by the households (such as bi-cycle, scooter, TV etc). These two variables should have different levels of influence. The variable ‘assets’ is directly related to ‘bank’ because of loan requirement for building up assets. ‘Pov’ on the other hand, relates to ‘bank’ through an improvement in the saving capacity of the families. We have considered 3 types of regression. In the first regression, both ‘pov’ and ‘assets’ are used allowing the step to choose among them. In the second regression, we used only ‘pov’. In the third regression, we used only ‘assets’.

The first regression retains both ‘pov’ and ‘assets’ within the regression. Both of them have the required signs (positive for ‘assets’ and negative for ‘pov’) and are significantly related to ‘bank’. This implies that both these variables are important in explaining the formal saving propensity of the families. Among the lifestyle variables, all are significant and have the required signs. ‘Lit’ is positively related to ‘bank’, implying a beneficial effect of awareness. More aware a family is of the formal saving avenues, the greater will be the willingness to save in formal avenues. ‘Mod’ has a positive relation with ‘bank’, implying a general improvement in awareness and the intensity to formal savings. However, ‘bo2’ has a positive sign. Here, the third factor of wealth may be very vital. Given the literacy level, richer families have larger number of children and higher propensity to save in the formal sector. Relationship between ‘breast’ and formal saving propensity is similarly explained. In the so-called rich families, there is a negative tendency towards breast feeding the child.

In all, our first Tobit regression has satisfied more or less all the anticipated relationships that we have hoped it to confer to us. Now we look to our next regression. Here the regression has been done by omitting the variable ‘assets’. Here the additional variables that have entered in our Tobit regression are ‘marr’, ‘inst’ and ‘immun’. The variable that has not come into the analysis is ‘pov’. Other variables (‘lit’, ‘bo2’, ‘mod’, ‘breast’) that came in explaining the relationship remained same with same signs. The variable ‘marr’ reflects the percentage of girl’s marrying before entering the adulthood. Higher value of this variable ‘marr’, symbolizes social stigma and prevalence of male dominance. This actually stems from lack of literacy, mainly lack of female literacy and lack of social awareness. So, it is quite likely that higher the value of ‘marr’, lower will be the inclination towards formal banking activities. The variable ‘inst’ is positively related to ‘bank’. Higher percentage of institutional birth implies more awareness towards health as well as faith towards institutional set up. Availability of institutional health facilities in nearby area is also very important in determining the percentage of institutional birth. It is needless to say, an area with higher institutional birth, should also show same kind of institutional affinity in regard to savings behavior also. This unquestionably explains the positive relationship between ‘inst’ and formal saving behavior. ‘Immun’ has also quite evidently positive relationship with formal banking habits. Higher percentage of children having immunization indicates higher health and social awareness among the parents. They are also likely to be more conscious and aware of the formal banking system. So, in the second Tobit regression analysis also, all the anticipated relationships have been supported. Now we enter into the third Tobit regression where we omitted the variable ‘pov’.

If we omit the variable ‘pov’, then the variables that come in explaining the relationship with formal saving behavior with various factors are ‘ marr’, ‘bo2’, ‘inst’, ‘immun’ and ‘breast’. The direction of relationship with bank and these variables does not show any peculiarity. The same kind of relationships (negative for ‘marr’ & ‘breast’ and positive for ‘bo2’, ‘inst’ and ‘immun’) appear in this Tobit regression also. The same explanations that we gave earlier for these variables hold here too.

5. CONCLUSION

The paper considers the banking behavior of people in an under developed economy like India. In the age of financial inclusion, a huge section of the populace is still outside the formal banking system. Unlike the common concept, poverty is not always the main reason behind this disparate saving behavior. Various types of informal outlets provide easy and cheap access to loan and savings. They are flexible and provide on the door services. It is often difficult for the formal sector to compete with this. Unless intelligent uses of

Table 8. OLS Results of Determinants of ‘bank’ when both ‘pov’ and ‘assets’ are included

| Variable Name | Estimated Co-Efficient | T-Ratio |

| ST | -0.14716E-02 | -2.526 |

| LIT | 0.16627 | 3.226 |

| POV | -0.92075E-01 | -2.584 |

| BO2 | 0.15096 | 2.852 |

| MOD | 0.27003 | 7.707 |

| BREAST | -0.98238E-01 | -3.563 |

| ASSETS | 0.47740 | 14.28 |

| CONSTANT | -0.21607 | -3.492 |

Table 9. Tobit Result of Determinants of ‘bank’ when both ‘pov’ and ‘assets’ are included

| Variable Name | Normalized Co-Efficient | T-Ratio |

| ST | -0.12942E-01 | bgcolor=white>-2.3563|

| LIT | 1.4423 | 2.9555 |

| POV | -0.85170 | -2.5363 |

| BO2 | 1.3573 | 2.7210 |

| MOD | 2.6073 | 7.7114 |

| BREAST | -0.94660 | -3.6331 |

| ASSETS | 4.5548 | 13.325 |

| CONSTANT | -2.0253 | -3.4682 |

| BANK | 9.3230 | 33.670 |

Table 11. Tobit Results of Determinants of ‘bank’ when the variable ‘assets’ is omitted

| Variable Name | Normalized Co-Efficient | T-Ratio |

| ST | -0.46654E-01 | -7.3117 |

| LIT | 1.8766 | 3.7866 |

| MARR | -1.0632 | -2.8229 |

| BO2 | 1.7671 | 3.4757 |

| MOD | 1.6967 | 4.8523 |

| INST | 1.4921 | 4.7649 |

| IMMUN | 0.80005 | 3.0380 |

| BREAST | -1.9117 | -7.2195 |

| CONSTANT | 0.30659 | 0.58749 |

| BANK | 8.4304 | 34.082 |

Table 12. OLS Results of Determinants of ‘bank’ when the variable ‘pov’ is omitted

| Variable Name | Estimated Co-Efficient | T-Ratio |

| ST | -0.63073E-02 | -5.698 |

| MARR | -0.19985 | -3.274 |

| BO2 | 0.23925 | 2.535 |

| INST | 0.27551 | 5.390 |

| IMMUN | 0.12754 | 2.816 |

| BREAST | -0.18645 | -3.944 |

| CONSTANT | 0.22075 | 2.781 |

Table 10. OLSResults of Determinants of ‘bank’ when the variable ‘assets’ is omitted

| Variable Name | Estimated Co-Efficient | T-Ratio |

| ST | -0.55108E-02 | -7.452 |

| DT | 0.11654E-02 | 2.882 |

| LIT | 0.23048 | 3.965 |

| MARR | -0.13547 | -3.065 |

| BO2 | 0.16747 | 2.786 |

| MOD | 0.20028 | 4.889 |

| INST | 0.16360 | 4.418 |

| IMMUN | 0.10579 | 3.373 |

| BREAST | -0.21486 | -6.925 |

| CONSTANT | 0.36704E-01 | 0.6126 |

Table 13. Tobit Results of Determinants of ‘bank’ when the variable ‘pov’ is omitted

| Variable Name | Normalized Co-Efficient | T-Ratio |

| ST | -0.33104 | -1.3619 |

| LIT | 2.6003 | -0.29403 |

| BO2 | -0.20116 | -0.29403 |

| MOD | 2.3425 | 5.2435 |

| BREAST | -1.6029 | -4.3349 |

| ASSETS | 0.30461 | 1.2534 |

| CONSTANT | 0.85285 | 1.2346 |

| BANK | 7.3620 | 23.694 |

banking instruments are facilitated, it might become impossible for the formal sector to tap these sources and a huge wastage of internal savings can’t be prevented. Instead of being locked in the informal cup-boards, informal savings should be diverted to the investible activities of the land. Only then the tall talks of financial inclusion can be fruitful (Tables 8 through 13).

REFERENCES

Amemiya, T. (1973). Regression analysis when the dependent variable is truncated normal. Econo- metrica, 41(6), 997-1016. doi:10.2307/1914031

Banerjee, A., & Duflo, E. (2011). Poor economics: A radical rethinking of the way to fight global poverty. New York: Public Affairs.

Besley, T., Coate, S., & Loury, G. (1993). The economics of rotating savings and credit associations. The American Economic Review, 83, 792-810.

Stuart, R. (2000). The poor & their money. Delhi: Oxford University Press.

ENDNOTES

1 Besley & Loury, (1993) have given a detailed analysis regarding the economics of ROSCAs.

2 A similar analysis has been made by Banerjee & Duflo, (2001), Poor Economics: A Radical Rethinking of the Way to Fight Global Poverty with regard to the informal health sector in Rajasthan. In spite of the competence, people opt for informal health services even when the formal health services facilities are cheap and standardized. Patients feel easy with the informal doctors with whom they can communicate more easily. To them, formal doctors are a world apart, who does not understand their language, tend to undermine them and live in a superior complex.

This work was previously published in Handbook of Research on Strategic Business Infrastructure Development and Contemporary Issues in Finance, edited by Nilanjan Ray and Kaushik Chakraborty, pages 12-21, copyright 2014 by Business Science Reference (an imprint of IGI Global).

670

More on the topic Chapter 35 Banks and People in the Development Process: A District-Level Analysis of the Banking Habits in India:

- Nutrition is a dynamic process to supply adequate nourishment for survival, growth and development, repair and creation of future reserves.

- Accreditation is a voluntary process that provides a means to demonstrate a level of quality.

- REGIONAL DEVELOPMENT AND INVESTMENT BANKS

- CONSEQUENCES FOR THE DESIGN OF THE INITIATION PROCESS

- Bureaucracy in the development process

- Malcolm Fraser had likely been drinking, although at the inquest his wife attested that he ‘was not of drunken habits’.

- Religious life at the popular level

- What Were the Banks Doing?

- Section 6 Emerging Trends

- Financial Constraints and High Level of R&D