Chapter 65 An Empirical Investigation on Credit Card Adoption in Indi

G.

H. Varaprasad

National Institute of Technology Calicut, India

Kailas Sree Chandran

St.Thomas Institute for Science and Technology, India

R. Sridharan

National Institute of Technology Calicut, India

Anandakuttan B.

UnnithanIndian Institute of Management, India

ABSTRACT

In India, the credit card usage as well as the penetration has been found to be very low compared to that of debit cards. Though banks offer the best of the services, still there are apprehensions about the risks involved in using a credit card in India. Hence, this study investigates the customer’s adoption behavior of credit cards and determines the factors which influence the acceptance among Indian customers. Many studies have been reported in the literature to analyze the customer’s adoption behavior of online banking, Automated Teller Machines, e-shopping etc. But, there are not many studies that analyze the adoption behavior of credit cards. In this study, an empirical model that includes ten behavioral factors has been proposed. Along with the main determinants identified from the literature, two new parameters such as perceived benefits and self-esteem have been included in the model. The analysis of the model reveals that factors such as perceived usefulness, perceived ease of use, perceived risk, relative advantage, perceived trust, social influence and perceived benefits have been found to be the main determinants of credit cards adoption in India. The findings are of great use primarily for the banks which are planning to offer credit cards, and for already existing banks to focus on the gaps.

INTRODUCTION

Services are central parts of developed economies which are growing in numbers, varieties and complexities (Geczy et al., 2010). Banking sector is the potential sector which has a vibrant growth. The revolutionary advancements in the

banking sector brought a dramatic change in the banking operations over the past two decades.

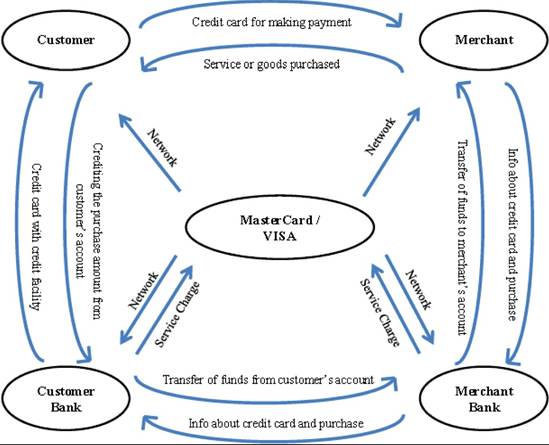

With an increasingly competitive global market, cost, quality, and technology leadership are no longer sufficient for businesses to secure competitive advantage (Ryan, 2012). With the advancement in technologies, banks started offering innovative products and services to secure the competitive advantage. Credit cards have emerged as the most widely used means of financial transactions. These plastic cards have become the best solution for those who do not have money at present, but want to fulfill their needs. Debit cards, credit cards, Automated Teller Machine (ATM) cards, shopping cards etc. are examples of plastic cards. Depending on the type of application, their utility also varies. Credit card is a vital payment tool for bank customers globally. The working mechanism of a credit card has been illustrated in Figure 1.DOI: 10.4018/978-1-4666-6268-1.ch065

.

It is evident from the mechanism that customer, merchant, network and bank are all equally responsible for a smooth and hasslefree credit card transaction. In India, Visa and MasterCard are the main players in credit cards who provide the network. According to the latest bulletin of Reserve Bank of India (Feb 2012), there are over 180 lakhs of valid credit cards in circulation.

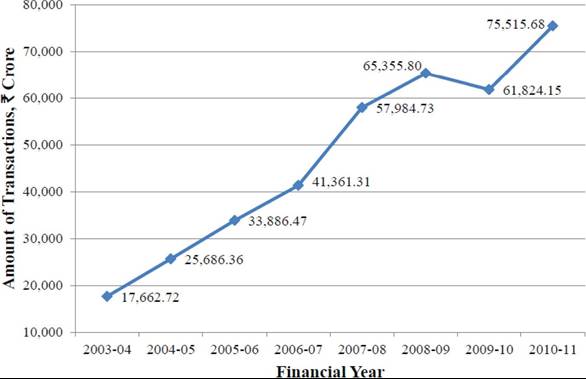

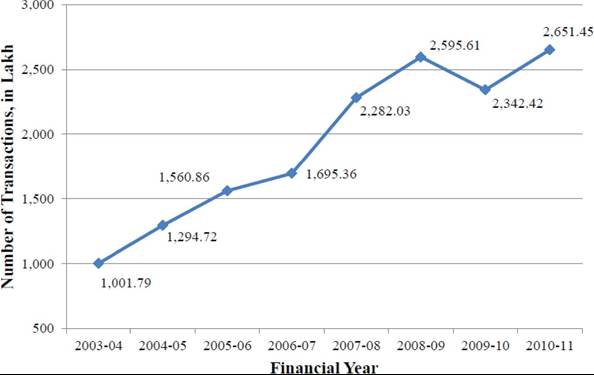

Figures 2 and Figure 3 give an overview of the status of credit card usage in India.

The Banks in India that offer credit card facility to its customers are Axis Bank, Bank of Baroda,

Canara Bank, Corporation Bank, HDFC, ICICI Bank, Indian Overseas Bank, Kotak Mahindra, Punjab National Bank, State Bank of India, Syndicate Bank, Union Bank of India, Vijaya Bank. The major foreign banks offering credit card services in India are ABN Amro, American Express, ANZ, Barclays Bank, Citibank, Diners Club, HSBC, Royal Bank of Scotland, Standard Chartered. Despite these many banks offering credit cards in India, still the credit card penetration is less than 10% of the total bank customers of India. Hence, this encourages the researchers to explore the possible impediments to the credit card adoption in India.

Therefore, the main objective of this behavioral study is to explore the major determinants which influence the adoption of credit cards among Indian customers. Based on a review of the relevant literature, an empirical model has been proposed with two new factors; perceived benefits and self esteem. This empirical model has been analyzed using various statistical methods. Different hypotheses were tested to find the behavioral factors which affect the adoption and acceptance of credit cards among IndianFigure 1. Working mechanism of credit cards

Figure 2. Total amounts of transactions using credit cards

Figure 3. Total number of credit card transactions

customers. The rest of the paper is organized as follows. First, we deal with the review of the relevant literature. Then we go on to outline the proposed research model and the hypotheses. Afterwards we describe the salient aspects of data collection. Then we provide data analysis and results. Followed by managerial implications and the conclusion.

LITERATURE REVIEW

Based on the behavioral theories, many studies have been reported in the literature to analyze the adoption and acceptance of new information systems. Similar kind of studies have also been conducted in banking sector related to the adoption of online banking, debit cards, mobile banking, credit cards etc. Moore and Benbasat (1991) had found the relative advantage and compatibility are relevant with respect to technology innovations. They have integrated diffusion of innovations and theory of reasoned action models to predict utilization of information technology by end-users. Many studies have found the effect of income in credit card usage. The various studies on credit cards from the literature have been summarized in Tablet.

Kaynak et al. (1995) exposed the preference of lower and middle income consumer’s on credit features over the service features, such as security and convenience. Kalakota and Whinston (1996) posit the nature of small-value transactions using credit cards. According to them, credit cards were not appropriate for small-value transactions compared to other forms of electronic payment system. The effect of low annual fee among consumers of Hong Kong was analyzed by Chan (1997). He found the importance of this factor in adopting credit cards. Lee and Hogarthe (1999) revealed that most of the customers in general are unaware of how to use a credit card and this unawareness has caused the customers to reject the credit card which led to a decline in the credit card market.

Venkatesh and Davis (2000) have introduced the construct social influence to predict the adoption of internet. They proposed a modified technology acceptance model (TAM) in their study. Studies conducted by Hsieh (2001) and Chou et al. (2004) indicate that credit cards are the most frequently used form of e-payment. They compared different e-payment systems and found the nature of usage of different systems. The influence of social status in adopting new mobile services was explained by Teo and Pok (2003). According to Wang et al. (2003), perceived ease of use was also a significant antecedent of the behavioral intention to use credit cards. Goyal (2004), found that supplementary services would promote credit card use and could help in reducing risk perception of customers towards using credit cards. Sun and Wu (2004) revealed the usage difference of credit cards among rural and urban population of China. Pin and Lin (2005) found a significant direct relationship between perceived financial cost and behavioral intention to use mobile banking. Amin (2008), examined that perceived usefulness, perceived ease of use, perceived credibility and the amount of information as the important determinants to predict customers’ intentions to use mobile credit card.

A study by Gan et al. (2008) found the effect of age and gender in the adoption of credit card. The findings in the study by Phau and Woo (2008) revealed that compulsive buyers perceived money as a symbol of power and prestige. They were more likely to use credit cards as compared to non-compulsive buyers. Dalia et al. (2009) suggested that perceived ease-of-use was the strongest predictor of intentions to continued usage of credit cards services in Egypt. Liu (2009) found that awareness about reward points could improve consumers’ attitude and credit card use behavior. Lee (2009) studied about the factors influencing the adoption of credit cards. He found perceived risk and perceived benefit to have a positive influence on the adoption. He also found a positive influence of perceived usefulness in the adoption. Yoon (2010) revealed that ease of use, demographic variables and perceived usefulness does not have a significant influence on customer satisfaction. Zafar (2010), examined life style to have a positive influence towards credit cards use while other factors like self-esteem, time consciousness, peer group pressure, exposure to advertisement and gregariousness were found to be insignificant. Wang et al. (2011) found self-control, self-esteem, self-efficacy, deferring gratification, internal locus of control and impulsiveness to have an influence on credit card usage. In a study on early adopters of credit cards in the Chinese context, Worthington et al. (2011), examined that perceived ease of use, self esteem, knowledge about the new product will have a positive effect on the adoption of credit cards. Convenience, customization, security/ privacy, web appearance and entertainment value were the key characteristics of e-retail environment impacting e-satisfaction of online purchase (Kim et al., 2011). Khare et al. (2012) found use, convenience and status to have an influence on credit card adoption.Table 1. Summary of factors considered in various studies on credit cards

| Author and Year | Country | Factors Considered/Investigated |

| Kaynak et al. (1995) | Turkey | Age and income |

| Chan (1997) | Hong Kong | Income and changes in education system |

| Goyal (2004) | India | Supplementary services promote credit cards usage and helps to reduce risk |

| Sun and Wu (2004) | China | differences in rural and urban population |

| Gan et al. (2008) | Singapore | Age and gender |

| Willis and Worthington (2006) | China | Status symbol |

| Amin (2007) | Malaysia | Perceived usefulness, perceived ease of use, credibility and amount of information |

| Phau and Woo (2008) | Australia | Power and prestige |

| Wickramasinghe and Gurugamage (2009) | Srilanka | Status symbol |

| Foscht et al. (2010) | Italy | payment mode and personal characteristics |

| Wang et al. (2011) | China | self-control, self-efficacy, deferring gratification, internal locus of control and impulsiveness |

| Worthington et al. (2011) | China | Perceived ease of use, self esteem, new product adoption, knowledgeable |

| Khare et al. (2012) | India | Use, convenience and status attributes |

In the present research, two new constructs perceived benefits and self-esteem have been introduced. The utilization of the traditional theoretical models with minor modifications and variety of analyses in the Indian context makes this study unique. This study focuses on individual perspective and proposes to identify factors that influence adoption and use of credit c ards in India.

RESEARCH MODEL

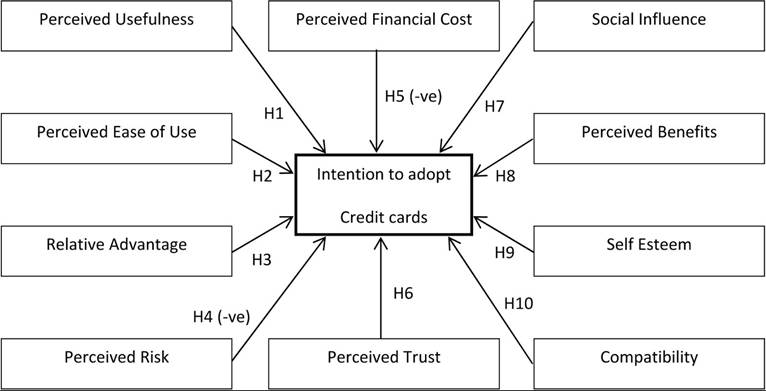

Based on the literature review, the crucial factors which influence the attitude towards credit card adoption have been identified as perceived usefulness, perceived ease of use, perceived risk, relative advantage, perceived financial cost, social influence, self esteem, compatibility, perceived benefits and perceived trust. An empirical model has been proposed as shown in Figure 4 and the following hypotheses have been formulated and tested.

FORMULATION OF HYPOTHESES

Perceived Usefulness

Technology Acceptance Model (TAM) proposed by (Davis et al., 1989) posits that perceived usefulness (PU) is a significant factor affecting acceptance of an information system. Davis et al., 1989 define PU as the degree to which a person believes that using a particular system would enhance his or her job performance. In simple words, PU is defined as, the usefulness of credit cards perceived by the customer. If a person doesn’t have money in his/her wallet or his/her account, he/she can still make a purchase/payment using his/her credit card. The customer can even use the credit card to withdraw money from any ATM. So, the customer expects some enhanced performance in his/her banking activities when he/she uses credit card. Thus, the following hypothesis has been formulated:

Figure 4. Proposed model

H1: Perceived usefulness will have a positive effect on the adoption of credit cards.

Perceived Ease of Use

Davis et al. (1989) define Perceived Ease of Use (PEOU) as the degree to which a person believes that using a particular system would be free of effort. According to TAM, perceived ease of use is a maj or factor that affects acceptance of information system. If the procedure of making a credit card transaction is easy to learn and less complex, then the user would be more comfortable in making transactions using credit cards and it motivates him to adopt it. So, the perception of ease of use may affect the intention to adopt credit cards. This leads to the following hypothesis:

H2: Perceived ease of use will have a positive effect on the adoption of credit cards.

Compatibility

Compatibility is defined as degree to which an innovation is perceived as consistent with the existing values, past experiences and needs of potential adopters (Rogers, 1983). The more compatible the innovation is, the more likely that users will adopt it. In this research, the compatibility of credit cards in small shops and outside the country, relationship between credit cards and the users’ life style etc. are investigated. Thus, the following hypothesis has been proposed:

H3: Compatibility will have a positive effect on the adoption of credit cards.

Relative Advantage

The rate of adoption is positively related to relative advantage of any innovation (Rogers, 1983). According to Rogers (1983), relative advantage is the degree to which an innovation is perceived as being better than the idea it supersedes. Here, the advantage of credit cards over other forms of money is considered. While traveling abroad, credit cards can be used for making payments. Compared to cash, credit cards are easy to carry and hassle free as they are just plastic cards. So, these advantages can influence the adoption of credit cards. This leads to the following hypothesis:

H4: Relative Advantage will have a positive effect on the adoption of Credit Cards.

Perceived Risk (PR)

Bauer (1960) introduced the concept called perceived risk. In credit card context, perceived risk may be associated with the financial loss as a result of using the services. The lack of security and privacy are the main concerns of risk. In this study, perceived risk focuses on users’ concerns about fraud, unprotected transactions, reliability of the merchant etc. The following hypothesis has been formulated:

H5: Perceived risk will have a negative effect on the behavioral intention to use credit cards.

Social Influence

Social influence (SI) is defined as the degree to which an individual’s emotions and feelings are affected by others in using an innovation (Venkatesh & Morris, 2000). SI simply means the influence of friends, relative and the society in one’s decision. Bank users will perceive credit cards to be useful when they see colleagues, friends and family members use it and get a recommendation of using it from them. The adoption of a new technology can be affected by this social influence. Thus, the following hypothesis has been tested:

H6: Social Influence will have a positive effect on the adoption of credit cards.

Perceived Trust (PT)

Trust is defined as the willingness to rely on an exchange partner in whom one has confidence on the other party (Moorman et al., 1992). The base of credit card system itself is the mutual trust between different parties. The customer trusts the merchant, the merchant trusts the merchant bank and the merchant bank trusts the customer bank. So, trust has a big influence in the credit card system and the adoption also depends on the trust of customer on this system. Thus, the following hypothesis has been formulated:

H7: Perceived trust will have a positive effect on the adoption of credit cards.

Perceived Benefits

Customers are very much interested in the benefits offered by the services before actually using the services. Perceived benefits are the add on benefits offered at free of cost to the customers along with the core services. Many banks offer rewards and benefits packages to their credit card holders. The offerings include enhanced product warranties at no cost, free membership in elite clubs, and points which may be redeemed for cash, products, or airline tickets etc. These benefits are provided to attract new customers and also to retain the existing credit card holders. In this research, perceived benefits (PB) focus on users’ interest in reward points, special offers and discount coupons which they get while making credit card transactions. These benefits may influence the bank users in adopting credit cards and thus, the following hypothesis has been tested:

H8: Perceived benefits will have a positive effect on the adoption of credit cards.

Self Esteem (SE)

Self esteem is a term used in psychology to reflect a person’s overall evaluation or appraisal of his or her own worth. Some individuals consider credit cards as a status symbol. A few individuals make purchase using credit cards just to show off. Studies conducted by Willis (2006) in China and Wickramasinghe (2009) in Srilanka suggest that status symbol has an effect in the adoption of credit cards. Zafar et al. (2010) had developed a model to identify the psychographic factors that influence the consumer attitudes toward using credit cards in Malaysia. Hence, self-esteem has been considered as a factor in the behavioral intention to adopt credit cards. This leads to the following hypothesis:

H9: Self esteem will have a positive effect on the adoption of credit cards.

Perceived Financial Cost

Perceived financial cost (PFC) is defined as the extent to which a person believes that using credit cards will cost money to the individual. Mathieson et al. (2001) suggests that perceived financial resources are a significant antecedent of the behavioral intention to use an information system. In order to own and possess a credit card one has to pay a certain amount in the form of processing fee apart from the fixed annually fee. Also, the defaulters are summoned with a huge fine for a delayed payment of credit amount. Hence, the customers would have a negative perception of these financial charges and these perceived financial charges can have a negative impact on the adoption of credit cards. Therefore, the following hypothesis has been tested:

H10: Perceived financial cost will have a negative effect on the adoption of credit cards.

DATA COLLECTION

The data for this study has been collected by means of a survey instrument. The sample consists of corporate professionals working in IT companies and faculty of different IITs, IIMs and NITs. 950 credit card holders participated in the survey and 640 were completely filled and valid for analysis leading to a response rate of 67%. This results in a sample that is well distributed in terms of demographics. In the questionnaire, a five point Likert scale ranging from strongly agree to strongly disagree are used as a basis to know the respondent’s views. The questionnaire consists of questions that are related to demographic information, the possible factors affecting the acceptance of credit card usage. The questionnaire has been developed and tested with a focus group consisting of banking professionals. Before proceeding with the main survey, the questionnaire was validated through pre-testing. This resulted in an error-free final questionnaire. The focus groups verified that the hypotheses developed might be the crucial factors in explaining the adoption of credit cards. Based on the feedback from the focus group and from the pilot study, some of the questionnaire items were dropped and some items were added and the wordings of some of the questions have been changed to improve clarity. Items have been jumbled in a random order to avoid the stereotype and biasness. The intention to use credit cards has been chosen as the dependent variable in the model. In this study it is assumed that there is no interaction effect among the independent variables.

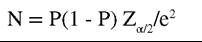

SAMPLE SIZE DETERMINATION

The data for this study has been collected only from credit card holders. The sample size was determined using the general formula for finding the sample size of an infinite population. If the total population is more than 50000, it can be assumed as infinite population (Maria, 2006):  where, N is the sample size required, P represents the percentage of proportion of credit card holders among bank users in India. According to RBI Bulletin (November 2011), 9.11% of bank users are credit card holders. A 5% tolerable error (e) is desired with 95% reliability. While the error is equal to 0.05, Z=1.96. Thus, the sample required has been obtained as 128. In the actual study, the sample size is chosen as almost six times the required sample size so that the resultant sample represents the entire population.

where, N is the sample size required, P represents the percentage of proportion of credit card holders among bank users in India. According to RBI Bulletin (November 2011), 9.11% of bank users are credit card holders. A 5% tolerable error (e) is desired with 95% reliability. While the error is equal to 0.05, Z=1.96. Thus, the sample required has been obtained as 128. In the actual study, the sample size is chosen as almost six times the required sample size so that the resultant sample represents the entire population.

DATA ANALYSIS AND RESULTS

The data was analysed using SPSS version 16.0 (statistical package for social sciences). The demographic profile of the respondents is shown in Table 2. From Table 2, it is found that 40.5% of the respondents are in the age group 26-35 years, 88% of the respondents are male, 40.6% of the respondents are post graduates, 42.2% of the

Table 2. Descriptive statistics of respondent’s demographics

| Profile | Description | Percentage |

| Gender | Male | 88 |

| Female | 12 | |

| Age | 18-25 | 38.1 |

| 26-35 | 40.5 | |

| 36-45 | 12 | |

| 46-55 | 5.9 | |

| 56-65 | 3.4 | |

| >65 | bgcolor=white>0.2||

| Education | Pre Degree | 2 |

| Degree | 40.6 | |

| P.G | 25.2 | |

| Research/Doctoral | 25 | |

| Diploma/Technical | 7.2 | |

| Annual Income | '1.6-3 lakhs | 15.5 |

| '3-5 lakhs | 31.4 | |

| '5-8 lakhs | 33 | |

| '8-10 lakhs | 8 | |

| '>10 lakhs | 12.2 | |

| Occupation | Student | 9.4 |

| Faculty/Teacher | 32.8 | |

| Professional/Officer | 42.2 | |

| Technician | 1.1 | |

| Business | 2.5 | |

| Retired | 1.3 | |

| Others | 10.8 | |

| Area | Rural | 11 |

| Urban | 89 |

respondents are professionals/officers, 31.4% of the respondents are in the income range Rs.3Lakhs - 5Lakhs. The credit card usage patterns of the Indian customers are shown in Table 3.

Reliability Analysis has been carried out by calculating the values of Cronbach’s alpha. Nunnally (1978) recommends the value of Cronbach's alpha to be at least 0.7 to show high internal consistency. In the present study, the Cronbach’s alpha value of the factor perceived financial cost has been found to be lower than the recommended value. Hence, this factor has not been dropped for the further analyses. Rest all factors have been found to have a higher Cronbach Alpha value higher than the recommended value, which shows a high internal consistency of the measures. Construct reliability of the factors are obtained as shown in Table 4:

A confirmatory factor analysis has been conducted on the items comprising perceived usefulness, perceived ease of use, perceived risk, relative advantage, self esteem, social influence, compatibility, perceived benefits, perceived trust and intention to use. The Kaiser criteria of eigen values greater than 1 has been used to determine the initial number of factors to retain. The Kaiser- Meyer-Olkin (KMO) measure was 0.873. From the Bartlett’s sphericity test the value of chi-square is found to be 26380 with a significance of 0.000. Hence, the constructs have been found to be valid.

Table 3. Attitude of credit card usage

| Attitude of Usage | Description | Percentage |

| Frequency of credit card usage in a month | 15 times | 9.5 |

| Minimum amount of transaction | '100 | 19 |

| '100-500 | 39 | |

| '500-1000 | 42 | |

| Maximum amount of transaction | ' 1,00,000 | 0.0 |

Table 4. Cronbach’s alpha values

| Factor | Cronbach’s Alpha |

| Perceived Usefulness | 0.840 |

| Perceived Ease of Use | 0.838 |

| Compatibility | 0.805 |

| Relative Advantage | 0.828 |

| Perceived Risk | 0.946 |

| Social Influence | 0.901 |

| Perceived Trust | 0.860 |

| Self Esteem | 0.793 |

| Perceived Benefits | 0.907 |

| Perceived Financial Cost | 0.600 |

| Intention to Adopt | 0.700 |

Multi-regression analyses are performed to test the hypotheses and to examine the associations among the constructs. The results have been reported in Tables 5 through Table 6

A linear multiple regression analysis has been carried out on the proposed model, where intention to use is the dependent variable and perceived usefulness, perceived ease of use, perceived risk, relative advantage, self esteem, social influence,

Table 5. Regression model

| Model | R2 | Adjusted R2 | Standard Error of Estimate |

| 1 | 0.722 | 0.718 | 0.38106 |

Independent Variables: perceived risk, perceived ease of use, self esteem, social influence, relative advantage, compatibility, perceived benefits, perceived trust, perceived usefulness

Dependent Variable: intention to adopt

compatibility, perceived benefits, perceived trust are the independent variables. From the ANOVA result shown in Table 6, it is evident that the model applied is significantly good enough in predicting the outcome variable. From the results of regression analysis shown in Table 5 it is found that, the coefficient of determination R2 is 0.722. This means that 72.2% of the variability in the dependent variable (i.e. intention to use credit cards) can be explained by the independent variables such as perceived usefulness, perceived ease of use, perceived risk, relative advantage, self esteem, social influence, compatibility, perceived benefits, and perceived trust. The R2 value and the adjusted R2 value are very close which implies that the model includes only the factors that are significant, i.e., the model is not over specified.

Hence, the multiple regression equation is:

Intention to use credit cards = 0.137 - 0.079*Per- ceived usefulness + 0.691 *Perceived ease of use + 0.036*Compatibility - 0.076*Relative advantage +0.109 *Perceived risk + 0.117*Social influence + 0.191*Perceived trust - 0.073* Perceived benefits + 0.036 * Self esteem

According to the hypothesis H1, perceived usefulness will have a positive effect on the intention to use credit cards. The findings from Table 7 perceived usefulness is found to be statistically significant at 0.05 level (β = -0.102, p = 0.018). Thus, the hypothesis H1 has been supported. This suggests that the bank customers perceive credit cards to be useful.

The hypothesis H2 states that perceived ease of use will have a positive effect on the behavioral

Table 6. ANOVA result

| Model | Sum of Squares | Degrees of Freedom | Mean Square | F | P-Value |

| Regression | 237.901 | bgcolor=white>926.433 | 182.042 | 0.000a | |

| Residual | 91.479 | 630 | 0.145 | ||

| Total | 329.380 | 639 |

Table 7. Regression result

| Model | Unstandardized Coefficients | Standardized Coefficients | t | P-value | |

| B | Standard Error | Beta | |||

| (Constant) | 0.137 | 0.126 | 1.090 | 0.276 | |

| Perceived usefulness | -0.079 | 0.034 | -0.102 | -2.364 | 0.018 |

| Perceived ease of use | 0.691 | 0.027 | 0.772 | 25.833 | 0.000 |

| Compatibility | 0.036 | 0.020 | 0.040 | 1.829 | 0.068 |

| Relative advantage | -0.076 | 0.022 | -0.087 | -3.388 | 0.001 |

| Perceived Risk | 0.109 | 0.032 | 0.145 | 3.440 | 0.001 |

| Social Influence | 0.117 | 0.029 | 0.113 | 4.026 | 0.000 |

| Perceived Trust | 0.191 | 0.030 | 0.179 | 6.290 | 0.000 |

| Perceived Benefits | -0.073 | 0.023 | -0.105 | -3.186 | 0.002 |

| Self Esteem | 0.036 | 0.021 | 0.044 | 1.744 | 0.082 |

intention to use credit cards. Table 7 that perceived ease of use is found to be statistically significant at 0.05 level (β = 0.772, p = 0.000). Thus, the hypothesis H2 is supported. This suggests that the bank customers perceive credit cards as easy to use.

According to the hypothesis H3 compatibility will have a positive effect on the behavioral intention to use credit cards. It is found from Table 7 that compatibility is statistically insignificant at 0.05 level (β = 0.040, p = 0.068). Thus, the Hypothesis H3 is negated. This means that the bank customers are not finding credit c ards transactions to be compatible. In India, other than big shopping malls, not many retailers accept credit cards. The credit card system is not yet so significant in small shops and also among the general public. Hence, respondents might have felt credit cards to be incompatible.

The hypothesis H4 states that relative advantage will have a positive effect on the behavioural intention to use credit cards. The findings from Table 7 shows that relative advantage is statistically significant at 0.05 level (β = -0.087, p = 0.001). Thus, the hypothesis H4 is supported. This means that bank customers are perceiving credit card transactions to be relatively advantageous than the traditional banking.

Hypothesis H5 states that perceived risk will have a negative effect on behavioral intention to adopt credit cards. It is observed from Table 7 that perceived risk is statistically significant at 0.05 level (β = 0.145, p = 0.001). H5 is therefore negated. The possible reason for the failure of the hypothesis may be because of the efforts taken by banks in making the credit card transactions more secure.

The hypothesis H6 states that social influence will have a positive effect on behavioral intention to adopt credit cards. Table 7 reveals that social influence is found to be statistically significant at 0.05 level (β = 0.113, p = 0.000). Thus, the hypothesis H6 is supported.

The hypothesis H7 states that perceived trust will have a positive effect on the behavioral intention to use credit cards. Table 7 that perceived trust is found to be statistically significant at 0.05 level (β = 0.179, p = 0.000). Thus, the hypothesis H7 is supported. This suggests that the bank customers trust the credit card system.

According to the hypothesis H8 perceived benefits will have a positive effect on the behavioral intention to use credit cards. It is found from Table 7 that perceived benefits is statistically significant at 0.05 level (β = -0.105, p = 0.002). Thus, the Hypothesis H8 is supported. This means that the bank customers are adopting and using the credit cards for the perceived benefits.

According to the hypothesis H9 self esteem will have a positive effect on the behavioral intention to use credit cards. It is found from Table 7 that self esteem is statistically insignificant at 0.05 level (β = 0.044, p = 0.082). Thus, the Hypothesis H9 is negated.

In summary, out of the nine hypotheses, seven were found to be statistically significant in this empirical study. The hypotheses H3, H5 and H9 have been rejected. Rejection of hypothesis H5 reveals that perceived risk has a positive effect on credit cards adoption.

From the model testing, it is understood that out of the two new factors considered, only one has shown a positive effect on the adoption. It is apparent, but confusing that in India, people use credit cards as a status symbol as hinted by the focus group interviews. However, from this study, it is evident that there is no effect of self esteem on the adoption of credit cards. The other factor proposed by the focus groups was perceived benefits. The focus group interviews opined that customers like to adopt or use credit cards for the benefits it offers and the same has been proved from this study.

In India, not many retailers accept credit cards. The credit card system is not yet so significant in small shops. Hence, respondents might have felt credit cards to be incompatible with their lifestyle. This is one of the reasons for the non-adoption of credit cards in India.

Security issues are the major concerns when it comes to financial matters. Because of various frauds, credit cards have been perceived to be risk prone in India. But, from this study, it is apparent that the trend is slowly changing and this is a good sign for the banking sector.

MANAGERIAL IMPLICATIONS

The findings of this study are particularly important for banks to concentrate on the problem areas to attract more customers and to help decide how to allocate resources to retain and expand their customer base. They can concentrate on those factors which are really influencing the bank users in adopting credit cards. The outcome ofthe study can be used to formulate new market strategies to increase the customer base of the credit card market. Based on demographics results, 90% of the card users are from urban sector. But, it does not mean customers in rural sectors are not willing to use credit cards. Educating all segments of the market is highly recommended as statistics show that the credit card penetration is only 9.1%. Therefore, financial institutions as well as government need to seriously think of educating the general public to see that everyone adopts the credit cards, which in turn helps the government to boost up the economy. The positive influence of perceived usefulness and perceived ease of use in the adoption can be exploited by the credit card issuing banks in framing or modifying the transaction procedures and services. Demirkan and Spohrer (2010) Agility and innovation are essential for survival in today’s business world. Banks and financial institutions should add more useful features and services to credit cards and they should simplify the procedures in making a credit card transactions.

In addition, the nation’s culture also plays a major role in the adoption of new advanced technologies. In the Indian context, power distance, and uncertainty avoidance have been found to be the main dimensions of culture apart from individualism versus collectivism, and masculinity versus femininity (Hofstede, 2001). With the modifications in the proposed research model and incorporating culture as an external variable, this study may be generalised universally.

In all major industrialized countries, the service sector is the largest economic segment maintaining the highest growth rate (Kett, 2011). In India, credit card is still a grape vine for the people who are in the middle and lower income groups. The credit cards are issued to only those whose monthly income is a minimum of Rs.10000 to 15000/-. The bank customers are denied a credit card on the basis of economic back ground. Though the customers have an urge to own a credit card, their economic conditions and the bank’s stringent conditions do not allow them to adopt credit cards.

The ability to design innovative services is an important capability for organizations in the 21st century (Schindlholzer et al., 2011). Banks need to strive hard to educate the general public by campaigning and creating awareness about the credit card system and the benefits it offers. Also, integrating products and services into customized solutions can help firms to gain competitive advantage (Bonnemeier et al., 2010; Burianek et al., 2011). Apart from banks, it is the responsibility of the government also to see that the credit card system flourishes in the Indian market. The stronger the nation’s credit card system, the stronger is the country’s economy. The evil of black money can be completely culminated at all levels with a fool proof credit card system. Therefore, the government should play a major role in implementing the credit card system throughout the country, and this will help in the adoption of credit cards in India.

CONCLUSION

The results support the view that perceived ease of use and perceived usefulness are the predicting variables in the intention to adopt. Both of them have positive influence along with the determinants such as relative advantage, social influence, perceived trust and perceived benefits. But, compatibility and self esteem are found to have negative influence on the adoption of credit cards. Interestingly, customers are not finding the credit card transactions to be risky. This could be because of the efforts of financial institutions to see that the credit card transactions are well protected with a high level of security. The introduction of chip based credit cards and instant short message service (SMS) to the customer upon any transaction helps to enhance the level of security in the transactions. Therefore, because of these security features, customers might be feeling the credit card transactions to be non-risky.

Since the data for the present study has been collected using online survey, the customers who are not familiar with computers and internet have been ignored in this study. The results pertain to only the credit card holders of public sector banks in India and hence the results may not be generalized.

A study on private sector banks and next generation banks could be an area for further research. Also, a comparison of the nationalized banks and private sector banks could be an ideal area for further research. Another area of research could be a study on the satisfaction levels of the customers of public sector banks.

ACKNOWLEDGMENT

The authors express their sincere thanks to the referees and the editor for their valuable comments which have helped to bring this paper to the present form.

REFERENCES

Ahmed, Z. U., Ismail, I., Sohail, M. S., Tabsh, I., & Alias, H. (2010). Malaysian consumers’ credit card usage behavior. Asia Pacific Journal of Marketing and Logistics, 22(4), 528-544. doi:10.1108/13555851011090547

Amin, H. (2008). Factors affecting the intentions of customers in Malaysia to use mobile phone credit cards. Management Research News, 31(7), 493-503. doi:10.1108/01409170810876062

Bauer, R. A. (1960). Consumer behavior as risktaking. In R. S. Hancock (Ed.), Dynamic marketing for a changing world (pp. 389-398). Chicago, IL: American Marketing Association.

Bonnemeier, S., Reichwald, R., & Burianek, F. (2010). Pricing integrated customer solutions: A process-oriented perspective on value appropriation. International Journal of Service Science, Management, Engineering, and Technology, 1(3), 1-16. doi:10.4018/jssmet.2010070101

Burianek, F., Bonnemeier, S., & Reichwald, R. (2011). Creating effective customer solutions: A process-oriented perspective. International Journal of Service Science, Management, Engineering, and Technology, 2(1), 15-29. doi:10.4018/ jssmet.2011010102

Chan, R. Y. (1997). Demographic and attitudinal differences between active and inactive credit card holders - the case of Hong Kong. International Journal of Bank Marketing, 15(4), 117-125. doi:10.1108/02652329710189375

Chou, Y., Lee, C., & Chung, J. (2004). Understanding m-commerce payment systems through the analytic hierarchy process. Journal of Business Research, 57(12), 1423-1430. doi:10.1016/ S0148-2963(02)00432-0

Davis, F. D. (1989). Perceived usefulness, perceived ease of use, and user acceptance of information technology. Management Information Systems Quarterly, 13(3), 319-339. doi:10.2307/249008

Demirkan, H., & Spohrer, J. C. (2010). Servitized enterprises for distributed collaborative commerce. International Journal of Service Science, Management, Engineering, and Technology, 1(1), 68-81. doi:10.4018/jssmet.2010010105

El-Kasheir, D., Ashour, A. S., & Yacout, O. M. (2009). Factors affecting continued usage of credit cards among Egyptian customers. Communications of theIBIMA, 9,252-263. ISSN: 1943-7765.

Foscht, T., Maloles, C. III, Swoboda, B., & Chia, S. L. (2010). Debit and credit card usage and satisfaction: who uses which and why - evidence from Austria. International Journal of Bank Marketing, 28(2), 150-165. doi:10.1108/02652321011018332

Gan, L. L., Maysami, R. C., & Koh, H. C. (2008). Singapore credit cardholders: Ownership, usage patterns, and perceptions. Journal of Services Marketing, 22(4), 267-279. doi:10.1108/08876040810881678

Geczy, P., Izumi, N., Hasida, K., Eto, K., & Mori, A. (2010). Interaction-based foundation of services. International Journal of Service Science, Management, Engineering, and Technology, 3(3), 1-11. doi:10.4018/jssmet.2012070101

Goyal, A. (2004). Role of supplementary services in the purchase of credit card services in India. Asia Pacific Journal of Marketing and Logistics, 16(4), 36-51. doi:10.1108/13555850410765258

Hofstede, G. (2001). Culture’s consequences: Comparing values, behaviors, institutions, and organizations across nations. Thousand Oaks, CA: Sage Publications.

Hsieh, C. (2001). E-commerce payment systems: Critical issues and management strategies. Human Systems Management, 20(2), 131-138.

Kalakota, R., & Whinston, A. B. (1996). Frontiers of electronic commerce. Boston, MA: Addison Wesley.

Kaynak, E., Kucukemiroglu, O., & Ozmen, A. (1995). Correlates of credit card acceptance and usage in an advanced developing Middle Eastern country. Journal of Services Marketing, 9(40), 52-63. doi:10.1108/08876049510094496

Kett, H. (2011). a business model approach for service engineering in the internet of services. International Journal of Service Science, Management, Engineering, and Technology, 2(4), 1-8. doi:10.4018/IJSSMET.2011100101

Khare, A., Khare, A., & Singh, S. (2012). Factors affecting credit card use in India. Asia Pacific Journal of Marketing and Logistics, 2(2), 236-256. doi:10.1108/13555851211218048

Kim, J., Kim, M., & Kandampully, J. (2011). The impact of e-retail environment characteristics on e-satisfaction and purchase intent. International Journal of Service Science, Management, Engineering, and Technology, 2(3), 1-19. doi:10.4018/ jssmet.2011070101

Lee, J., & Hogarthe, J. (1999). The price of money: Consumers’ understanding of APRs and contract interest rates. Journal of Public Policy & Marketing, 18(1), 66-76.

Lee, M. (2009). Factors influencing the adoption of credit cards: An integration of TAM and TPB with perceived risk and perceived benefit. Electronic Commerce Research and Applications, 8(3), 130-141. doi:10.1016/j.elerap.2008.11.006

Liu, M. K. (2009). Do credit card redemption reward programs work in China? An empirical study. Journal of Consumer Marketing, 26(6), 404-413. doi:10.1108/07363760910988229

Luarn, P., & Lin, H.-H. (2005). Toward an understanding of the behavioral intention to use mobile banking. Computers in Human Behavior, 21(6), 873-891. doi:10.1016/j.chb.2004.03.003

Mathieson, K., Peacock, E., & Chin, W. W. (2001). Extending the technology acceptance model: The influence of perceived user resources. The Data Basefor Advances in Information Systems, 32(3), 86-112. doi:10.1145/506724.506730

Mavri, M., & Ioannou, G. (2006). Consumers’ perspectives on online banking services. International Journal of Consumer Studies, 30(6), 552-560. doi:10.1111/j.1470-6431.2006.00541.x

Moore, G. C., & Benbasat, I. (1991). Development of an instrument to measure the perceptions of adopting an information technology innovation. Information Systems Research, 2(3), 192-222. doi:10.1287/isre.2.3.192

Moorman, C., Zaltman, G., & Deshpande", R. (1992). Relationships between providers and users of market research: The dynamics of trust within and between organizations. JMR, Journal of Marketing Research, 29(3), 314-328. doi:10.2307/3172742

Nunnally, J., & Bernstein, I. H. (1978). Psychometric theory (3rd ed.). New York, NY: McGraw Hill.

Phau, I., & Woo, C. (2008). Understanding compulsive buying tendencies among young Australians: The roles of money attitude and credit card usage. Journal of Marketing Intelligence & Planning, 26(5), 441-460. doi:10.1108/02634500810894307

Rogers, M. (1983). Diffusion of innovations. New York, NY: The Free Press.

Ryan, L. (2012). An investigation of product service system models. International Journal of Service Science, Management, Engineering, and Technology, 3(2), 35-49. doi:10.4018/jss- met.2012040103

Schindlholzer, B., Uebernickel, F., & Brenner, W. (2011). A method for the management of service innovation projects in mature organizations. International Journal of Service Science, Management, Engineering, and Technology, 2(4), 25-41. doi:10.4018/IJSSMET.2011100104

Sun, T., & Wu, G. (2004). Consumption patterns of Chinese urban and rural consumers. Journal of Consumer Marketing, 21(4), 245-253. doi:10.1108/07363760410542156

Teo, T. S. H., & Pok, S. H. (2003). Adoption of WAP-enabled mobile phones among Internet users. The International Journal of Management Science, 31(6), 483-498.

Venkatesh, V., & Morris. (2000). Why don’t men ever stop to ask for directions ? Gender, social influence, and their role in technology acceptance and usage behavior. Management Information Systems Quarterly, 24(1), 115-139. doi: 10.2307/32509 81

Venkatesh, V., & Davis, F. D. (2000). A theoretical extension of the technology acceptance model: Four longitudinal field studies. Management Science, 46(2), 186-204. doi:10.1287/ mnsc.46.2.186.11926

Wang, L., Lu, W., & Malhotra, N. K. (2011). Demographics, attitude, personality and credit card features correlate with credit card debt: A view from China. Journal of Economic Psychology, 32(1), 179-193. doi:10.1016/j.joep.2010.11.006 Wang, Y. S., Wang, Y. M., Lin, H. H., & Tang, T. I. (2003). Determinants of user acceptance of credit cards: An empirical study. International Journal of Service Industry Management, 14(5), 501-519. doi:10.1108/09564230310500192

Wickramasinghe, V., & Gurugamage, A. (2009). Consumer credit card ownership and usage practices: Empirical evidence from Sri Lanka. International Journal of Consumer Studies, 33(4), 436-447. doi:10.1111/j.1470-6431.2009.00779.x

Willis, M., & Worthington, S. (2006). Foreign credit cards in China: To adapt or not to adapt? Journal of Asia-Pacific Business, 7(3), 45-77. doi:10.1300/J098v07n03_04

Worthington, S., Thompson, F. M., & Stewart, D. B. (2011). Credit cards in a Chinese cultural context-the young, affluent Chinese as early adopters. Journal of Retailing and Consumer Services, 18(6), 534-541. doi:10.1016/j.jretcon- ser.2011.07.003

Yoon, C. (2010). Antecedents of customer satisfaction with online banking in China: The effects of experience. Computers in Human Behavior, 26(6), 1296-1304. doi:10.1016/j.chb.2010.04.001

This work was previously published in International Journal of Service Science, Management, Engineering, and Technology (IJSSMET), 4(1); edited by Ghazy Assassa and Ahmad Taher Azar, pages 13-29, copyright 2013 by IGI Publishing (an imprint of IGI Global).