Chapter 28 ICT Infrastructure Framework for Microfinance Institutions and Banks in Pakistan: An Optimized Approach

Sadiq Shahbaz Ali

Shaheed Zulfikar Ali Bhutto Institute of Science and Technology, Pakistan

M. N. A. Khan

Shaheed Zulfikar Ali Bhutto Institute of Science and Technology, Pakistan

ABSTRACT

Information and communication technology (ICT) can be termed as a reagent for the microfinance sector.

It has contributed significantly for the growth of this sector, which is clearly depicted from the reviewed literature as well as the market evaluation. The paper analyzes the impact of technological advancements within the microfinance industry from academic as well as practitioner’s point of view. The true advantage of that advancement in the technology is yet to be realized by this sector. The paper proposed that ICT components on an optimized approach can be beneficial for a new as well as an experienced microfinance player for the efficient and cost effective delivery of its services to the masses without any major hindrance.1. INTRODUCTION

The ICT infrastructure framework for microfinance institutions can be seen in two perspec- tives-global and local.

1.1. Global Perspective

ICT is an enabler and catalyst of economic and social development in the third-world nations

DOI: 10.4018∕978-1-4666-6268-1.ch028

(Dewan & Riggins, 2005). At the global level, United Nations (UN) and the World Bank are consorting with government and non-government institutions of the less resourceful and developing countries to promote ICT with the target of bringing them up to a certain conventional level in technology by making the requisite grant funds available to promote economic development (Kauffman & Rigging, 2010). This objective is perceived in the United Nation’s commitment towards the global development. One of UN’s goals is to create a harmonized global platform for development (Kauffman & Rigging, 2010).

This includes liaising with the private and public sector for the provision of benefits of information and communication technologies (Kauffman & Rigging, 2010)..

Microfinance services have emerged as an effective and responsive mechanism for the economic development in the last couple of decades. Microfinance can be defined as “the availability of financial services to unbanked or poor or lower income clients or lesser privileged sector of the society” (Ledgerwood, 2000). Microfinance institutions give small loans to such clients who are not being provided any services from conventional sector and are willing to opt it for setting up their own business. This sector provides the services like loans, savings mobilization, remittance, insurance and capacity building for business setup. The Nobel peace prize laureate and the founder of Grameen Foundation brought the industry into limelight. There are about four billion unbanked people around the world which is more than two third of the population of low and middle income developing countries around the world (2010). Conventional financial institutions such as commercial bank are still unable to reach poor population, because of high cost for constructing and sustaining the branch network.

Microfinance Providers (MFPs) i.e., microfinance institutions (MFIs) and microfinance banks (MFBs) are considered as the best apparatus for alleviating poverty, as it helps reduce risk and increase income of the poor household. Several MFIs were converted into the full-fledged microfinance banks over a period of time. This transition has never been easy for such institutions to become a regulated b ank under the supervision of the regulatory body of that country. The conventional banks are also looking into the feasibility to venture into this market as well. These types of conventional players are entering into the microfinance sector with diverse ICT background and facilities.

ICT is being stimulated as a technological instrument to help MFIs being placed at a better position in a modest environment.

ICT has been recognized as a preferred investment within the banking industry, especially in the conventional sector. Operational efficiency, risk analyzing and controlling/mitigation, getting new customers and retention of existing customers has been enhanced significantly through the use of ICT. The MFIs have followed the same pattern to remain buoyant to compete in the banking sector. The use of ICT by conventional lending institutions and MFIs is driving the closeness and coordination between the two sectors of the banking arena. This is also dictating MFIs/MFBs into an economically more competitive business domain. The third-party websites such as the Consultative Group to Assist the Poor (www.cgap.org), Microfinance Information Exchange (MIX Market, www.mixmarket. org) and Banking With The Poor (www.bwtp. org), which creates healthy competition among MFIs for technological advancements, consultant pools, real success stories, strategy guidance and donor funds. This gives the benefit to bring more efficiency and performance in the overall business key indicators. Whether the ICT has provided an edge to the overall microfinance sector or not, is it really competitive to the conventional sector and has certainly raised the standard of the sector.1.2. Local Perspective (Pakistan)

The microfinance is a specific sector within the banking industry that functions through the provisions set out in the microfinance ordinance approved by the State Bank of Pakistan. The industry is focused to serve the specific impoverished segment of the society which is un-served by the commercial banking. This sector provides the services like loans, savings mobilization, remittance, insurance and capacity building of clients for business setup. The conventional banking has flourished quite a lot in Pakistan from the technological aspects covering core banking solutions, communication and infrastructure in the last decade or so. Usually, the conventional banks are provided with the deep pockets to make huge investments in the technology area, but this is not the case of the microfinance banks.

The concept of microfinance is relatively new and emerging in Pakistan. The State Bank of Pakistan states its mission in this regard as “Transformation of microfinance into a dynamic and integrated industry through the provision of services to unbanked population within a regulatory and governance framework” (2011). The industry has its own challenges and issues, which are of varied nature and quite different from the conventional banking industry. The good aspect is that it is provided with certain platform/forums like Financial Inclusion Program (www.sbp.org. pk) and Pakistan Microfinance Network (http:// www.microfinanceconnect.info) to assist in the technological areas, so that it helps the industry in a better way. Those forums help the microfinance banks and institutions to build their capacity by sharing the mutual experiences in an organized manner. The innovation in a technological area with coordination to business addresses all these challenges in a better way.

Pakistan is the fifth largest country in terms of using mobile phone services. There are around 95 million mobile users, including the remote mountainous areas (like Gilgit, Baltistan) and there are 26 million banking accounts within the country which indicate inherent potential for mobile banking in Pakistan (2010). The prominent MFIs working in Pakistan are (Ahmed, 2006):

• Khushali Bank;

• Kashf Microfinance Bank;

• NRSP Microfinance Bank;

• Bank of Khyber;

• The First Microfinance Bank Ltd.;

• Orangi Pilot Project (OPP);

• Sungi development Foundation;

• Taraqee Foundation MFI;

• Thardeep MFI;

• Rozgar Microfinance Bank;

• Tameer Microfinance Bank;

• Asasa MFI;

• Pak Oman Microfinance Bank;

• Waseela Microfinance Bank.

To expand financial system access and usage, the innovation in the institutional processes and technology is a requisite program to opt for. To reduce the capital expenditure cost, the microfinance institutions are moving towards the adoption of latest technologies like virtualization, cloud computing, outsourcing model and managed services, as this approach requires less upfront investment for them.

Mobile phone technology and agent network (2011) help reduce the operational cost and increase banking footprint. Indeed, inadequate research has been made under the ICT influence over the microfinance sector. This paper is an attempt to extend the work carried out by Robert Kauffman and Frederick Riggins (2011) in the microfinance sector. Rest of the paper is organized as follows: Section 2 provides a literature survey about the ICT advancements in different areas of the microfinance sector which have set the lasting impressions. These imprints were also replicated in a more or less the same manner in other parts of the world. Section 3 elaborates the key findings; Section 4 covers our proposed framework that has been developed based on the usage of ICT advancements. Section 5 explains components of the proposed framework. Section 6 delineates a case study based discussion and, finally, we conclude in the last section.2. LITERATURE REVIEW

Ahmed (2006) discussed the importance of ICT for microfinance institutions and highlighted the difficulties in getting the right technology because of certain issues like human-resource skills, suitable core banking application, business process diversity, geographical outreach, vendor capacity and higher cost of solutions. The author presented a strategy comprising a) strong IT department, b) short term Core Microfinance Application, and c) long term Core Microfinance Application to address all the areas of business, including the alternate delivery channels. The research focus in this area is on the importance of the Core Microfinance Application which is a backbone of any institution for all kinds of transactional flow. The right selection of the solution by keeping in mind the future vision of the organization and cost-benefit analysis could place an organization in a better position to go on with the market pace.

Robert et al. (2010) identify the challenges faced by the microfinance institutions as: efficiency in operations, risk mitigation, financial sustainability and growth.

These areas can be better addressed by the help of right selection of technologies. The authors emphasize the impacts of IT in better economic development and efforts to cover the digital gap. The microfinance technology ecosystem can be developed with the integration of the ICT drivers, stakeholders including the customers, microfinance institution, donors, regulatory bodies and the microfinance industry as a whole. The focus is on the effective coordination of all the stakeholders to reap the benefits of the ICT. In view of this, it is imperative to understand in detail the influence of ICT facilities at the donor, MFI, customer and the microfinance industry. The specific weightage has been assigned to the usage of Internet banking and mobile banking, which can produce benefits to the sector by reducing the distances and proving facility to the customers of the far-flung areas.Malia et al. (2011) examine factors that positively influence users to adopt latest banking services, which are technology-driven, i.e., Internet banking, phone banking and auto-teller machine (ATM). Such an approach necessitates a technology acceptance model to support the usage of these services by the customers due to factors like trust, perceived ease of usage, reliable connectivity and best service quality. These services are provided with better quality, and customers can rely on them based on their own convenience. The technology has particular leverage to the banking sector for swift and reliable execution of all types of transactions.

Nobert et al. (2011) provide the ICT roadmap for the future based on; user access, availability of ICT services, user expectations and future projects. The roadmap basically guides the development of such applications and services which can serve the current needs as well as the forthcoming expectations to some extent. However, the applications should be developed keeping in view of the scalability, usability and flexibility aspects in mind. Contrary to that, such applications would not be able to keep up the pace of business opportunities and development.

Victor etal. (2012) recommend a service-based Mobile Collection System in order to establish a better system with no redundancy, lower error probability and lesser fraud rate. The system shows that not all of dependable attributes are satisfied to the same degree. Reliability, confidentiality and safety have the highest degree level; availability and integrity share the medium degree level; and maintainability has the lowest degree level. So, using the mobile technology could add a value to it and provide a convenience to the customer to avoid the commuting time and cost required to physically visit the bank branch.

Parikh (2006) discusses three important aspects faced by the rural microfinance service providers, which are: remote clients data exchange, data processing for the institutional and the payment system to distant rural areas. The abovementioned three challenges can be amicably addressed to a great extent through adopting the following procedures:

• The usage of handheld technologies/device to collect the data;

• Provision of a strong microfinance banking application for centralized and quick processing;

• Introducing the electronic banking, i.e., ATM for collection and delivery.

The benefits achieved from the introduction of these services are far-reaching and can bring long-term sustainability to the sector.

Vikas etal. (2011) observe that mobile penetration, the ease of usage of voice interface and reasonable acceptability of mobile related technologies, all bring us to the convergence of mobility and innovative collaboration technologies that can help in crafting a system for the masses. A system is proposed that uses voice as medium to reach the larger population and crosses the thick layer of illiteracy and establishes an effective interaction with the MFI. This reduces the cost to a considerable extent without compromising any information and also enforces the active participation of the illiterate sector of the unbanked population, which in itself is a remarkable achievement. The voice medium is the best medium to approach that segment of the society as a certain kind of transactions can be carried out through it.

Nabila et al. (2010) provided an account of the influence of IT-related technologies over the work efficiency, risk management and customer relationship, which proved to be quite positive. By the efficacious implementation of ICT based services, the work efficiency along with the customer experience can be enhanced notably. In order to make it more effective, the user awareness level should also be improved.

Eduardo et al. (2008) discussed a particular model of correspondent banking, which created an ICT based business edifice for banks to downscale financial services out ofthe conventional branches such as small retail shops, supermarkets, mobile franchises, drugstores, post offices, and so on. This concept is known as the branchless banking which has revolutionized the banking sector in general and microfinance sector in particular. The upfront cost for the MFI/MFB to set up a branch premise has reduced to a considerable extent and using the other mediums benefited a lot. The writer has also focused upon the use of point of sale machines, ATMs and other handheld devices to do the microfinance-related transaction in the correspondence banking model.

Radhika et al. (2008) explain that the underlying principle behind ICT in gaining importance in developmental projects is that it contributes considerably to the accretion in human wellness by enabling economically and socially marginalized sections of the society to exercise their right of choice through enriched community participation. In this context, the authors present the concept of digital ecosystems for using ICT as a means of information delivery to the masses. A digital mechanism describes an ICT enabled network that displays associative and autopoietic properties capable of self-sustenance and of expansion through heightened inclusion and growth.

Saket et al. (2006) explain that credit risk assessment system can be carried out using the mobile technology, and this can be done by sending officers into the field to get the approval for processing of micro loans. This approach can reduce the commuting time for the officer to execute such a process in the office.

Parikh (2005) presents a mechanism in which the cell phone camera is used to scan all the documents, which are subsequently transmitted to the central repository for further processing. This mechanism can be used in the developing world to support the existing manual document submission process. This can really benefit the microfinance industry as the loan office can fill the data while in the field and then submit it through the mobile which will be processed accordingly at the central site.

Adeel et al. (2010) elaborate that the technological innovation can be attractive when it is combined with measures to support learning and community building. Outsourcing is one of the better aspects to be used by the MFI/MFB as making huge upfront technological investments are quite expensive. There is enough room to use the ICT for the empowerment and education of customers within the microfinance sector as it would help uplift the standard of life among the masses.

The financial inclusion (Olga et al., 2010) in numerous parts around the world has been made on the basis of technology enabled branchless banking services. This service is increasing the spectrum for the provision of microfinance banking services to the customers near to their doorstep. Not only, the customers are facilitated, but it also reduces the operational expense of the microfinance provider. The technology is instrumental in providing better and cheap access to the customers.

The technology has changed the face of the microfinance sector (Jaijit & Richa, 2007) especially reaching out to the masses and enhancing the scalability and sustainability of it. Rao et al. (2010) examined the impact of a different framework on the use of the mobile services and felt the need of having uniformity across the board.

3. KEY FINDINGS

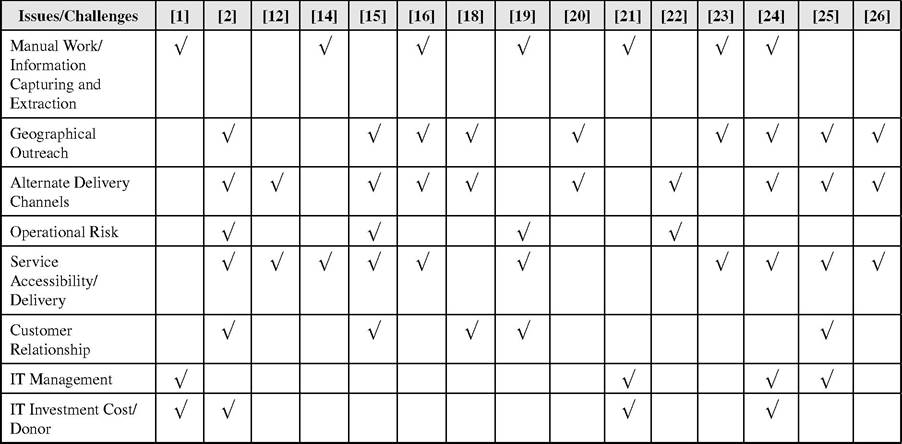

During the literature review, we observed a number of issues and challenges being faced by the microfinance sector that encompasses both the global as well local perspective. The key challenges viz-a- viz the cited literatures are highlighted in Table 1.

To conduct this research, besides undergoing an extensive literature review, we visited central and regional offices of the different microfinance institutions and banks. From the practitioners’ angle, the participation from the key stakeholders is essential for undertaking any research study. Therefore, in this study, the practitioners were involved by interviewing representatives (through physical visits or over the voice) from Branch Operations, Business, Risk Management and IT departments. The challenges pinpointed by the practitioners help us to formulate an appropriate IT response to overcome these challenges.

The ICT solutions for some of the major areas viz-a-viz the challenges identified during the study are highlighted in Table 2. Table 2 also highlights the suggested tool, techniques and solutions for those challenges.

Table 1. Issues/challenges w.r.t. microfinance sector

Table 2. Solutions (ICT/non-ICT) against issues/challenges*

| IssuesZChallenges | Solutions (ICT or Non-ICT) |

| Manual Work/Information Capturing and Extraction | Centralized Core Microfinance Application, Mobile Applications, Other applications like office automation and collaboration |

| Geographical outreach | Branchless Banking, Outsourcing Model, Handheld Technology (Mobile, POS, PDA) |

| Alternate Delivery Channels | Automated Branches, Branchless Banking Units, Internet, Phone, Mobile, ATM |

| Operational Risk | Better controls through Centralized Core Microfinance Application, Document Scan through Handheld devices (Mobile, PDA) |

| Service Accessibility/Delivery | Mobile Technology linked with Centralized Core Microfinance Application |

| Customer Relationship | Customer Relationship Management Application |

| ICT Management | Outsourcing Mechanism, Virtualization of resources, Cloud Computing, Shared Services, Managed Services |

| ICT Investment Cost/Donor | Active Donors (World Bank, Asian Development Bank and other State Driven Banks and International Financial Institutions) available for funding of ICT projects provided that it place major impact over the microfinance sector |

*(The institutions considered from the practitioners’ angle include: Khushali Bank, Kashf Microfinance Bank, Asasa MFI, The First Microfinance Bank Ltd, NRSP Microfinance Bank - Interviews were conducted either through physical visit or over the voice)

Some of the solutions discussed in Table 2 are being practiced by the microfinance banks and institutions and have been proven to be beneficial to the industry to a considerable extent as they can help make it a more viable, promising and financially sustainable sector.

3. GUIDING PRINCIPLES: PROPOSED ICT FRAMEWORK

The challenge is an opportunity in disguise, which provides a direction for growth, expansion, efficiency and sustainability. Based on the academic and practitioners’ angle and keeping in view the challenges and opportunities along with the availability of ICT solutions, we propose an ICT framework for microfinance institutions and banks. This is a logical framework as the components suggested are not only archetypes for a new microfinance operator, but it can also help enhance the overall functional efficiency of an experienced one as well. This will help the institutions to devise their ICT strategy keeping in view the past practices and the new techniques to be adopted. The institutions need not to re-invent the wheel as they can adopt the components in a phase-wise approach as per their own business strategy.

The proposed framework is divided into two major components: IT Management and IT Services. The “IT Management” component is linked to the management of the overall IT infrastructure covering all the relevant areas while “IT Services” is the area which will provide the specific services which are the need of the business. It will also serve as an enabler of business through the use of IT infrastructure.

The approaches which are best suitable for the microfinance sector (to be adopted) have been mentioned against each component. The proposed approaches are basically the way for managing or monitoring the respective component. Three main approaches have been identified i.e., in-house management (management within the Institute), outsourcing (management by a service providing company) and third-party piggybacking (using the existing infrastructure of any other key player).

3.1. Outsourcing

In this case, the specific part of the IT infrastructure is being taken care of or maintained by an outside specialized company or group having a service level agreement in place for the continued availability of that service for the client (MFI).

3.2. In-House Management

In this case, the specific section of the IT infrastructure is being developed or serviced or maintained by the owner (MFI) itself.

3.3. Third-Party Piggy Backing

In this case, the specific part of the IT infrastructure owned by a third-party company (who is specialized to do it) which is being used by the institution (MFI). In this case, the client needed not to place its own infrastructure instead using that of service providers at a certain cost on an agreed formula.

Table 3 shows the identified ICT domains having their respective components; and the approaches to be adopted in the implementation of those components.

4. COMPONENTS AND ITS ASSOCIATED APPROACH

Table 4 provides a detailed overview about the component together with d its approach that should be adopted for its effective implementation.

A mix and match of these can be adopted for specific type of MFI as it varies from institution to institution. Nowadays, the availability of such vendors/service providers to offer the services are quite good for MFI’s who cannot make such huge upfront investments in the IT domain.

5. USAGE IN LOCAL ENVIRONMENT: A CASE STUDY-BASED DISCUSSION

Based on the above work, we carried out an exercise to check an important aspect of the above-mentioned components, i.e., application software for business operations, which is also called as the Core Microfinance Application. This usage clearly depicts that the local environment is needs to follow the best practices and standard frameworks which are essential to stay

Table 3. ICT framework components with its preferred approaches

| ICT Domains | Components | Approach |

| IT Management | Asset Management (hardware and software) | Outsourcing |

| Human resource Management | Outsourcing | |

| Data/Information Management | In-house management | |

| Information security Management | In-house management | |

| Maintenance/Warranty services | Outsourcing | |

| Information systems development management | Outsourcing | |

| Network management (Communication links) | Outsourcing | |

| Web services Management | Outsourcing | |

| IT Services | Office automation | In-house management |

| Application software for business operations | In-house management | |

| Internal and External Communication | In-house management | |

| Outreach and expansion | Third-Party piggybacking | |

| Online services | In-house management | |

| ATM/POS/Handheld services | Third-Party piggybacking |

Table 4. Descriptive information against the components

| Component | Approach | Descriptive Information |

| Asset Management (hardware and software) | Outsourcing | It is an administrative cost (with respect to management of hardware and software assets) and overhead to the business, hence, it should be handed over to a third- party. |

| Human resource Management (HR) | Outsourcing | Instead of managing the whole HR within the organization, it should be outsourced to avoid the cumbersome process of hiring and firing manpower. |

| Data/Information Management | In-house management | As information/data is the critical part of any organization so it should be managed by the organization itself for all kind of reporting to stakeholders and regulators. |

| Information security Management | In-house management | The organization is the custodian of its data, so it should have absolute control over the right information for the right person and need to be managed within the organization. |

| Maintenance/Warranty services | Outsourcing | It is an administrative cost, so proper service level agreements (SLA) should be maintained with the vendors to provide all the maintenance related activities. |

| Information systems development management | Outsourcing | Proper SLA should be maintained with the vendors to provide the information systems development related activities. |

| Network management (Communication links) | Outsourcing | It is an administrative cost; therefore, proper SLA should be maintained with the vendors for the availability of communication/network links at the desired level of the organization. |

| Web services Management | Outsourcing | Being an administrative cost, proper SLA should be maintained with the vendors to provide the web related services. |

| Office automation | In-house management | Adopt open source technologies and manage it within the house to have control over the sharing of data/information. |

| Application software for business operations | In-house management | As it pertains to the information/data relevant to the organization, so it should be managed in-house and SLA should be in placed with the vendor for any changes or further developments in the system. In addition, it should be centralized for better management and control. |

| Internal and External Communication | In-house management | Prefer to adopt the open source technologies and it needs to be managed within house to have control over the sharing of data/information. |

| Outreach and expansion | Third-Party piggybacking | The footprint of the institution can be taken up to any level by the adoption of piggyback model for getting the benefits of agents or branches network of other institutions like post offices, mobile franchises, etc. |

| Online services | In-house management | As information/data is the critical part of any organization, so it should be managed by the organization itself for all kinds of online services by the effective coordination of different functions. |

| ATM/POS/Handheld services | Third-Party piggybacking | In this case, the institution can tie up with any other bigger banking player having strong presence in the country to use their ATM/POS network and can introduce its services through it. |

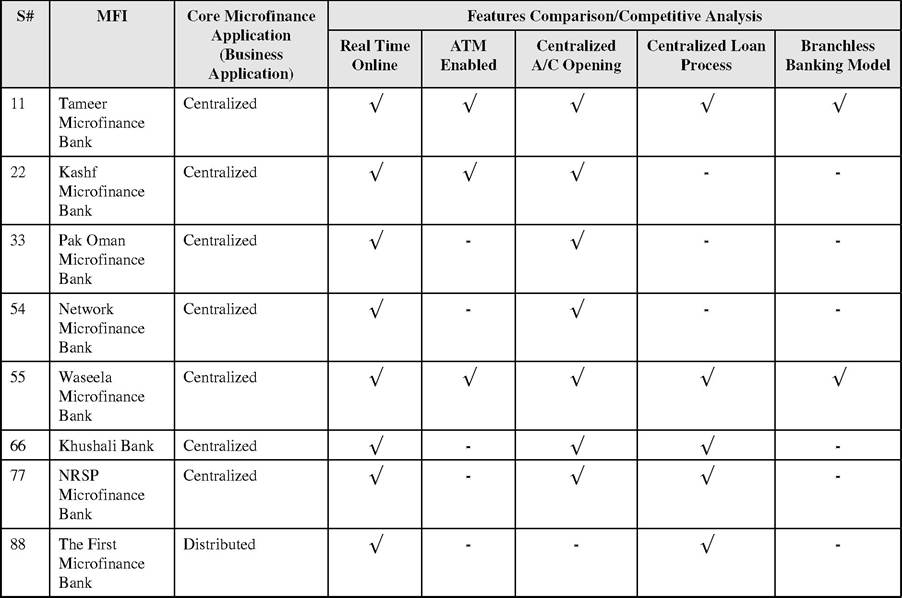

competitive in the market. Table 5 highlights the core microfinance applications being used by the different MFIs/MFBs in Pakistan.

This is one of the validations carried out against one of the main components within the ICT framework which shows that the sector in local environment is moving in the right direction for the adoption of such trends, which are expected to produce numerous advantages.

The placement of centralized Core Microfinance Application is the backbone of the IT infrastructure as most of the other services can only be opted once they are placed on strong footings. As the institutions that have such components in place can move forward to provide for better services to their customers by using different distribution channels as technology is facilitating the businesses to achieve their objectives.

Table 5. Usage of Core Microfinance Application and its advantages

The proposed ICT logical framework was developed on the basis of data obtained from academic and practitioner resources. The approach against each component is a real driver for those components as it can guide an institution to opt for it as evident from the research. The adoption of right approach is critical as all the remaining things really depend on it. The proposed approach could benefit the organizations in a number of ways as it is extracted from the aforementioned components from certain pertinent angles such as: a) Wider geographical access to customers, b) Low transactional cost, c) Less capital expenditure cost,

d) Better customer relationship and satisfaction,

e) Reduced administrative efforts, and f) Focused approach towards business.

7. CONCLUSION AND FUTURE WORK

This paper focuses on the influence of ICT on different areas of the microfinance sector. We have tried to include the practitioners’ angle from the local microfinance sector into the proposed framework. Thus, this research covers both the angles which are quite aligned with each other and indicate that the local industry in Pakistan is also on the footpath of international market to follow the ICT advancement and its benefits.

ICT has become an enabler to the business for the launch of innovative products and services for the under-served segments of the society. The components along with the specified approach can be taken as an ICT roadmap or guidance tool for the new or experienced microfinance players to give leverage to the business. We have validated one of the components from the local environment, which clearly indicates its direction towards the adoption of centralized microfinance application. Further, it is also suggested that the local market should take the benefit of the ICT practices and approaches being followed globally. These practices are basically facilitating the functioning of these microfinance institutions and banks to enhance their performance in terms of efficiency and business goals.

Based on the above work, a new dimension is available for further work as well i.e., development of a consortium for getting the true benefit of that technological advancement. The need for that consortium is because of high cost technological facilities and resources which is a quite difficult ask for the banks/institutions in the microfinance sector.

REFERENCES

Adeel, M., Nett, B., & Wulf, V. (2010). Innovating the field level of microfinance: A Pakistan case study. In Proceedings of the 4th ACM/IEEE International Conference on Information and Communication Techologies and Development.

Agarwal, V., Desai, V., Kapoor, S., Kumaraguru, P., & Mittal, S. (2011). Enhancing the rural self help group - Bank linkage program. In Proceedings of the International Conference on Service Operations, Logistics, and Informatics (SOLI).

Ahmed, A. (2006). Management information system for microfinance. Retrieved December 10, 2012, from http:///www.bwtp.org pp

Armendariz de Aghion, B., & Morduch, J. (2005). The economics of microfinance. Cambridge, MA: MIT Press.

Azim, M., Ali, A., & Sattar, J. (2011). Factors influencing adoption of information technology based banking services: A case study of Pakistan. Frontiers of Information Technology 2011.

Banking with the poor. (n.d.). Retrieved December 10, 2012, from http://www.bwtp.org

Bhattacharya, J., & Singla, R. (2007). Microfinance - A technical framework for cross border credit in India. In Proceedings of the International Conference on Theory and Practice of Electronic Governance (ICEGOV-2007).

Branchless Banking Newsletter, S. B. P. (2012). State bank of Pakistan, Development finance group. Retrieved December 10, 2012, from http:// www.sbp.org.pk

Dewan, S., & Riggins, F. J. (2005). The digital divide: Current and future research directions. Journal of the Association for Information Systems, 6(9), 298-336.

Diniz, E. H., Pozzebon, M., Jayo, M., & Araujo, E. (2008). The role of information and communication technologies (ict) in improving microcredit: The case of correspondent banking in Brazil. In Proceedings of the Portland International Center for Management of Engineering and Technology-2008 Coference.

Financial Inclusionfor the poor. (n.d.). Retrieved December 10, 2012, from http://www.cgap.org

Jawadi, N., Jawadi, F., & Ziane, Y. (2010). Information and communication technologies contribution to microfinance institutions performance: An empirical investigation of developing and emerging financial markets. In Proceedings of the 2nd IEEE International Conference on Information Management and Engineering.

Jere, N. R., Thinyane, M., & Terzoli, A. (2011). Development of an ICT road map for eservices in rural areas. In Proceedings of ITU Kaleidoscope 2011: The Fully Networked Human? - Innovations for Future Networks and Services (K-2011). Kauffman, R. J., & Rigging, F. J. (2010). Research direction on the role and impact of ICT in microfinance. In Proceedings of the 43rd Hawaii International Conference on System Sciences (pp. 238-242).

Ledgerwood, J. (2000). Microfinance handbook: An institutional and financial perspective. Washington, DC: World Bank.

Morawczynski, O., Hutchful, D., & Rangaswamy,

N. (2010). The bank account is not enough: examining strategies for financial inclusion in India. In Proceedings of the 4th IEEE/ACM Conference on Information and Communication Technologies and International Development (ICTD 2010).

Pakistan branchless banking conference. (2010). Retrieved December 10, 2012, from http://www. sbp.org.pk/MFD/pbbc/Salim-Raza.pdf

Parikh, T. S. (2005). Using mobile phones for secure, distributed document processing in developing world. IEEE CS and IEEE ComSoc. doi:10.1109/MPRV.2005.43

Parikh, T. S. (2006). Rural microfinance service delivery gaps, inefficiencies and emerging solutions. In Proceedings of the International Conference on Information and Communication Technologies and Development (ICTD-2006).

Parikh, T. S., & Lazowska, E. D. (2006). Designing an architecture for delivering mobile information services to the rural developing world. In Proceedings of the 15 th International Conference on World Wide Web (WWW-2006).

Rajagopalan, R., & Sarkar, R. (2008). A digital ecosystem approach to using ICT for sustainable development in communities. In Proceedings of the International Conference on Digital Ecosystems and Technologies (DEST-2008).

Rao, K. V., Ramamritham, K., & Sonar, R. M. (2010). Examining the viability of mixed framework for evaluating mobile services impact in rural India. In Proceedings of the International Conference on Information and Communication Technologies and Development (ICTD-2010).

Sathe, S. K., & Desai, U. B. (2006). Cell phone based microcredit risk assessment using fuzzy clustering. In Proceedings of the International Conference on Information and Communication Technologies and Development (ICTD-2006).

Singh, R., Bhar, C., & Sen, M. (2012). Data flow diagram for developing DSS on fund management of Indian microfinance institutions. In Proceedings of the International Conference on Recent Advances in Information Technology (RAIT-2012).

Strategic framework for sustainable framework in Pakistan, state bank of Pakistan, microfinance department. (2011). Retrieved December 10, 2012, from http://www.sbp.org.pk

Taylor, S., & Todd, P. A. (1995). Understanding information technology usage: A test of competing models. Information Systems Research, 6(2), 144-176. doi:10.1287/isre.6.2.144

Utomo, V., & Hidayat, A. (2012). Dependable service-based application for micro finance: Case study in mobile collection system for Bank Sahabat Purba Danarta. In Proceedings of the International Conference on Cloud Computing and Social Networking (ICCCSN).

Yunus, M. (2007). Banker to the poor: Microlending and the battle against world poverty. New York, NY: Public Affairs.

This work was previously published in International Journal of Online Marketing (IJOM), 3(2); edited by Hatem El-Gohary, pages 75-86, copyright 2013 by IGI Publishing (an imprint of IGI Global).

544