Chapter 29 ICT Investments and Management for Organizations

Georgios N. Angelou University of Macedonia, Greece

Anastasios A. Economides

University of Macedonia, Greece

ABSTRACT

Developing the Information and Communication Technologies (ICT) strategy that supports the overall organization ,s business strategy is critical for generating business value.

Recognizing the inadequacy of traditional quantitative cost-benefits analysis for evaluating and managing ICT investments, researchers suggest multi-criteria analysis, integrating quantitative and qualitative modeling. This chapter introduces the Balance Scorecard (BS) decision analysis framework and combines it with Real Options (ROs) analysis, in a qualitative and quantitative perspective, for modeling the business flexibility as well as for evaluating and controlling the ICT investments strategy. The multi-criteria ROs modeling applies to all perspectives of the BS framework providing a holistic decision-making model for ICT business.INTRODUCTION

In a competitive business environment, it is necessary for organizations to take advantage of every opportunity to reduce cost, improve quality and provide service. Information and communication technologies (ICT) constitute a strategic asset for organizations. Organizations rely on ICT for both their technology infrastructure and their specific applications to conduct their core business. ICT markets all over the world recently have been, and still are, undergoing drastic changes, fuelled my market reforms and technological progress. Organizations find ICT compelling due to improved customer satisfaction, reduce operations cost, increased organizational productivity, and rapid application development.

The valuation and management of ICT business activities is a challenging task because it is characterized by high-level uncertainty and tangible and intangible effects.

Gomez et al. (2010) argued that it is not sufficient to focus on the easily measurable tangible and quantifiable benefits of ICT. They motivated that the intangible benefits of ICT on development such as empowerment, self esteem and social cohesion are more important from a developmental perspective. In addition, Zehir et al. (2010) analyzed the relationship between information technology (IT) investment level, IT usage, IT perception, IT at decision making process, future orientation, technology orientation and firm performance in the comprehensive competitive environment.The findings of their study showed that IT investments are vital component of firm performance and if firms manage IT investments successfully, they will enhance firm performance.DOI: 10.4018/978-1-4666-6268-1.ch029

.

Also, Lin et al. (2007) examined the relationship between the levels of IT maturity and the use of IT investment evaluation and benefits realization methodologies via case studies and survey in the service sector. The findings indicated that IT maturity has a positive impact on the adoption of IT investment evaluation and benefits realization approaches. In risk management perspective, Otim et al.(2012) examined the effect that investments in information technology (IT) have on downside risk profiles of companies that made public announcements of their investments in technology. They found evidence that IT investments and their timing influence organizational downside risk. In addition, transformational and informational IT investments lead to a reduction in downside risk only if they lead to strategic IT investments in the industry.

In overall, although a vast array of methodologies for ICT investments evaluation present in the literature, some argued that a multi-perspective or integrated approach is needed combining specific decision analysis techniques, such as Delphi and Analytic Hierarchy Process (Azadeh et al., 2009; Gunasekaran et al., 2006).

ICT investments should consider operational, management and strategic perspectives.

Particular, ICT investments in operational management are related to processes that embody the execution of tasks comprising the activities of an organization’s value chain. Investments in the area of management may include processes and activities related to the administration, allocation and control of resources within the organization. Also, investments in strategic perspective could include processes such as planning, forecasting and strategy implementation.In parallel, ICT can have four distinct but complimentary effects on business evaluation. It is through the following four effects on business processes that ICT creates value. First, automotive effects refer to the efficiency perspective of value coming from the role of ICT as a capital asset being substituted for labor, deriving productivity improvement, and cost reductions. Second, Information effects are related to ICT capacity of collect, store, process, and disseminate information. Following these effects, business value (i.e. Return on Investment) accrues from improved decision quality, and enhanced organizational effectiveness. Third, transformative effects refer to the value of business process reengineering and redesigned organizational structures. Finally, growth effects are related to organizations core business expansion in other business fields based on existing ICT infrastructure indicating growth business opportunities.

The aforementioned analysis concerns quantitative and qualitative measures and applies to organization’s internal processes, customers, overall economic and growth business perspectives.

The valuation of ICT investments and the management of their implementation and exploitation require multi-attribute analysis adopting multicriteria analysis and combination of quantitative and qualitative measures.

This work discusses all these issues and includes them in a multi-attribute perspective providing a holistic methodology and model for ICT investments managements for business strategy formulation, evaluation and implementation.

It adopts the balance scorecard (BS) technique and combines it with real options (ROs). The proposed analysis provides a better understanding, for an organization, of the ICT investments strategy formulation, the risks and the various qualitative factors inherent in such investments, enabling these investments to be deployed more optimum and valued with higher accuracy.The main contributions of this chapter are the following:

• Adoption of the BS for strategy formulation, evaluation and implementation monitoring under ROs analysis,

• Introduction of quantitative and qualitative analysis adopting ROs,

• Risk management and the organizations flexibility modeling to implement and exploit such investment activities.

The aim is to the define strategy for ICT investments, analyze and evaluate it in a multiattribute perspective and find the business deployment that achieves a balance, for organizations, between risk control, investment’s flexibility exploitations and performance maximization.

The rest of the chapter is organized as follows. In Section 2, we provide background of the involved techniques. In Section 3, we provide the proposed methodology and model. In Sections 4, we discuss suggest possible future research. Finally, in Section 5 we conclude.

BACKGROUND OF THE PROPOSED TECHNIQUES

Balance Score Card

The Balanced Score Card was introduced in the late 1980s and early 1990s as a method to help companies manage their increasingly complex and multi-faceted business environments. It was developed by Kaplan and Norton as a framework that helps top management to select a set of measures that provide an integrated look at a company (Kaplan and Norton, 1992).

They suggest four perspectives.

1. The financial scorecard contains the traditional financial performance measures. The company should set financial goals and select a limited set of financial measures.

2. The customer scorecard deals with the question ‘‘how do customers see us?’’ Again, goals are set and measures are selected.

3. The internal business scorecard provides goals and measures concerning the internal operations. The underlying question here is ‘‘What should we excel at?’’.

4. The fourth scorecard deals with the innovation and learning perspective. Can we continue to improve and create value?

Each perspective can be explained by a key question with which it is associated. The answers to each key question become the objectives associated with that perspective, and performance is then judged by the progress to achieving these objectives. There is an explicit causal relationship between the perspectives: good performance in the Learning and Growth objectives generally drives improvements in the Internal Business Process objectives, which should improve the organization in the eyes of the customer, which ultimately leads to improved financial results.

Though there are four basic perspectives proposed, it is important to understand that these perspectives reflect a unique organizational strategy.

Objectives, Measures, and Initiatives

Objectives are desired outcomes. The progress toward attaining an objective is gauged by one or more measures. As with perspectives, there are causal relationships between objectives. In fact, the causal relationship is defined by dependencies among objectives. So, it is critical to set measurable, strategically relevant, consistent, time-delineated objectives (Bloomfield, 2002).

Measures are the indicators of how a business is performing relative to its strategic objectives. Measures, or metrics, are quantifiable performance statements (Milis and Mercken, 2004). As such, they must be:

• Relevant to the objective and strategy.

• Placed in context of a target to be reached in an identified time frame.

• Capable of being trended.

• Owned by a designated person or group who has the ability to impact those measures.

An organization is likely to have a variety of types of measures. Some will be calculated from underlying data.

Others will be aggregated index measures that assign different weights to multiple contributing measures. Some are frequently measured and others may only be measured on a quarterly or annual basis.It is important to balance lagging indicators- which includes most financial measures-with leading indicators-areas where good performance will lead to improved results in the future.

It is also important to balance internal measures, such as cost reduction, injury incident rates, and training programs, with external measures like market share, supplier performance, and customer satisfaction.

Finally, initiative is a change process, activity or project designed to achieve one or more objectives. The initiative is what will move a measure toward its target value. Initiatives, projects may be large or small in scope.

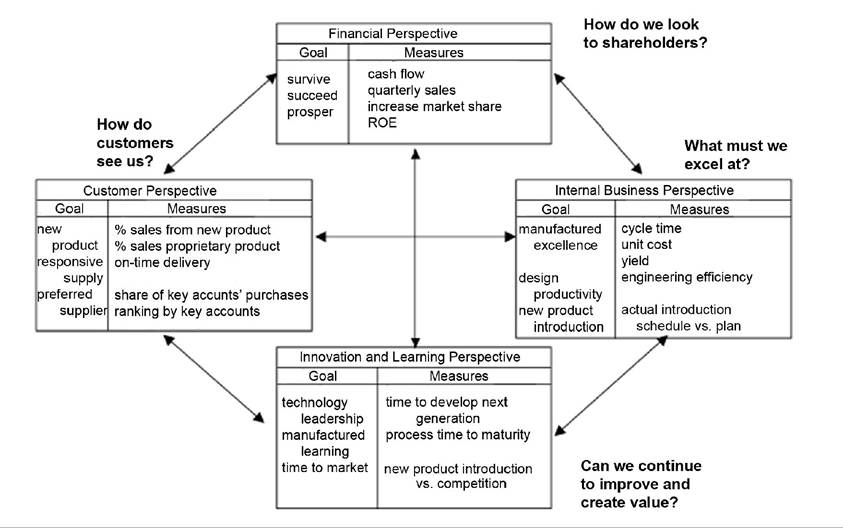

To illustrate the use of the BS, Kaplan and Norton (1992) presented an interesting example (Figure 1). An IT-company used the balanced scorecard framework to select a number of metrics and to set a number of targets for top management.

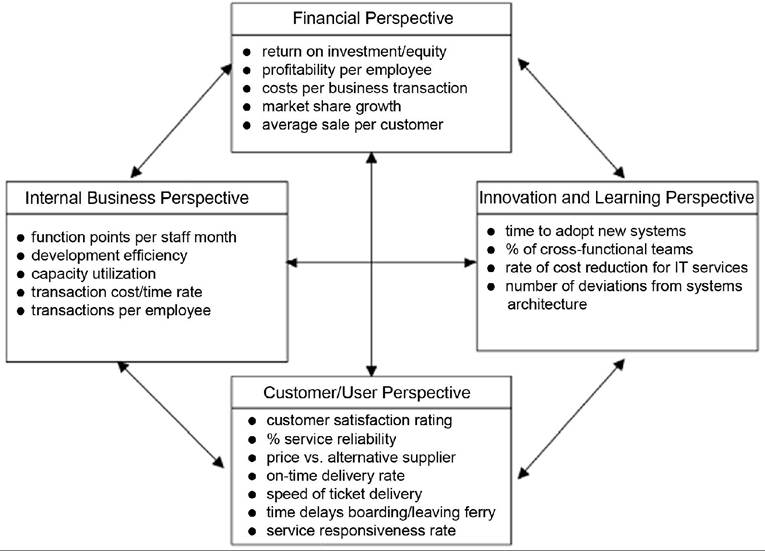

It is relative easy to formulate the BS framework to the needs of ICT business evaluation and implementation. Willcocks and Lester (1994) presented an ICT-company that used the BS framework to select a number of metrics and to set a number of targets for top management (Figure 2).

Figure 1. Example of the balanced Scorecardframeworkfor an ICT company (Kaplan and Norton, 1992)

When looking at this method more closely, one can conclude that this framework is a mixture of (traditional) quantitative decision analysis methods and new evaluation methods. In particular, the (traditional) finance based evaluation techniques are not abandoned (financial perspective) but are combined with qualitative analysis (Willcocks and Lester, 1994; Kaplan and Norton, 1992).

The B S encourages a shift from financial based evaluation techniques to strategy and vision. This is as a result of the BS need for substantially more input from the top management than does the traditional techniques. Traditional techniques in most cases are designed and overseen by financial experts (Kaplan and Norton, 1992). The BS forces management to take a broad view on ICT investments. This is one of the main advantages of this method. Another advantage is that many different evaluation techniques can be integrated into the framework. A further advantage is that the framework can be used for the feasibility evaluation as well as for the follow up and ex-post evaluation.

In this chapter, the aforementioned perspectives are enhanced by adopting the ROs philosophy. ROs constitute mainly a quantitative technique; however, the need for their integration with qualitative analysis has been already discussed in the literature (Angelou and Economides, 2008, 2009, 2013).

Real Options

An option gives its holder the right, but not the obligation, to buy (call option) or sell (put option) an underlying asset in the future. Financial options are options on financial assets (e.g. an option to buy 1000 shares of Nokia S.A. at the pre-agreed price 10 ˆ per share on January 2015). The ROs approach is the extension of the options concept to real assets (Trigeorgis, 1996). For example, a telecommunication investment can be viewed as an option to exchange the cost of the specific investment for the benefits resulting from this investment. An investment embeds a RO when it offers to the management the opportunity to take some future action (such as abandoning, deferring or expanding the investment) in response to events occurring within the firm and its business environment (Trigeorgis, 1996).

Figure 2. ICTperformance indicators example (Willcocks and Lester, 1994)

Trigeorgis (1996) provided an in-depth review and examples on different real options. Lee et al. (2009) established a dynamic model under real options analysis to analyze the optimal timing decision of IT investments when the output price for firms is stochastic and benefits of IT investments are arisen from the increasing output price, increasing sale, and cost savings. They found that increasing (decreasing) price volatility will delay (advance) the timing of IT investments. Increasing IT investments, however, may not delay the timing of IT investments. In addition, the decreasing (increasing) efficiency and increasing (decreasing) depreciation of IT investments will delay (advance) the timing of IT investments. Also, Benaroch et al. (2006) focusing on IT projects argued that managerial intuition ought to be supplemented with the use of formal real option models, which allow for better quantitative insights into which risk mitigations to pursue and combine in order to effectively address the risks most worth controlling. For more practical issues the reader is referred to Mun (2002). Finally, Angelou and Economides (2005) provided an extended survey of ROs applications in real life ICT investments.

Real Options Limitations and Need for Quantitative and Qualitative Analysis

In business practice, several conceptual and practical issues emerge when trying to use options theory as proposed in the current ICT literature. It is accepted that all ROs models provide approximate valuations of ROs values (Renkema, 1999).

Existing models for ROs valuation assume a certain distribution of the resulting cash flows, based on an efficient market. However, this is rarely the case in the context of investments in the ICT business field, which is known for its uncertain and unpredictable conditions. It has also been recognized that finance-oriented option valuation models are too complex for managerial decision-making practice, when real life business conditions are considered (Fichman et al., 2005). In particular, after the liberalization of the telecommunication market, the required competition modeling has increased the complexity of existing options models. It is very difficult for senior managers to accurately estimate the parameters of a statistical distribution of outcomes and mainly volatility since they do not really have a “gut feel” for the estimation of the volatility, even though they understand its technical definition as a statistic. Options theory in its present state does provide a conceptual decision framework to evaluate technology investments but, in many cases, cannot be considered as a fully operational tool for management. If it is expected that practitioners and senior managers will resist the use of formal options pricing models, then the qualitative option valuation can be an alternative analysis process. This is based more on the intuition of decision makers and forecasting for risks profiles, and less on sharply quantified prediction for parameters used in the formal options models.

Overall, these issues suggest that even quantified ROs analysis could produce only approximate valuations, which in some cases can cause serious mistakes in investment decisions (Fichman et al., 2005). For these reasons, although ROs enhance quantitative financial analysis, by modeling investment flexibility, they also require a wider view of qualitative perspective.

Hence, a multi-criteria decision analysis framework can be extended including typical tangible factors from financial perspective and intangible ones from qualitative ROs thinking. This framework is built based on the BS technique, adopting the later as the strategy definition, evaluation and implementation decision taken tool.

THE PROPOSED MODELMETHODOLOGY

Here, a methodology is presented that helps to address the question:

How do we define and implement the firm’s business strategy, in the ICTfield, in such a way so that to minimize the risks and increase the performance?

The proposed models contain both tangible and intangible perspectives. The current chapter introduces the BS framework. BS provides to the firms’ upper management the ability to define business strategy, performance indicators, as well as evaluate the business.

The proposed steps are the following:

1. Define the strategy (using the BS).

2. Evaluate the strategy (build ROs philosophy on BS framework).

3. Implement the strategy.

4. Monitor and correct the strategy.

This chapter focuses mainly on the first two steps providing the overall framework of combining the ROs philosophy with the BS technique.

Define the Strategy

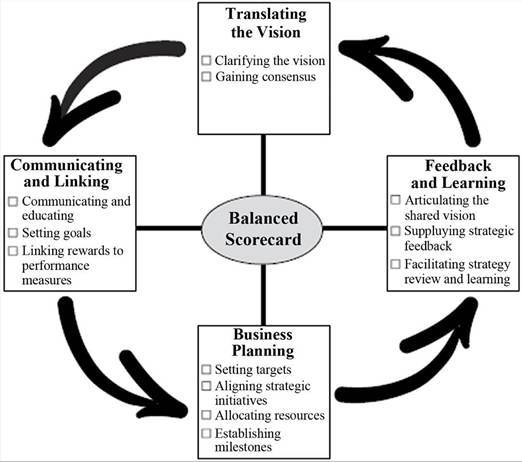

Particularly, there exist four processes in using the BS for defining and managing the ICT business strategy (Figure 3). The first process is to translate the vision of the firm. It helps managers to build a consensus around the firms’ vision and strategy. The second process is to communicate the managers’ strategy up and down of the firm’s structure and link it to the departmental and individual objectives. The third process is the business planning based on quantitative and qualitative analysis enabling the firms to integrate financial results with intangible pay offs. Finally, the fourth process is the learning by the implementation of the strategy and the reformulation of it during this period. All the aforementioned processes may be implemented around the BS framework (Kaplan and Norton, 2007).

Figure 3. Defining and managing strategy in ICT business, (Kaplan and Norton, 2007)

Evaluate the Strategy using the BS Enhanced by ROS Philosophy

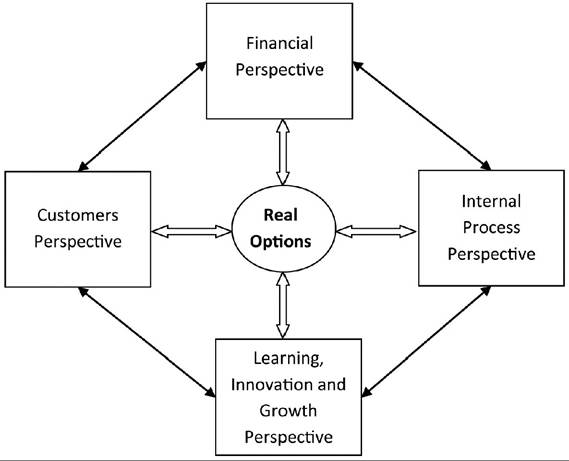

The target is to evaluate the strategy adopting various implementation alternatives. In particular, the ROs philosophy is applied to the four perspectives of BS adopting specific characteristics of ROs, either quantitative or qualitative (Figure 4).

Financial Perspective

As with the traditional methodologies, measuring needs financial data. However, the critical point is that the current emphasis on financials leads to the “unbalanced” situation with regard to other perspectives. Timely and accurate funding data will always be a priority, and managers will do whatever necessary to provide it. In fact, often there is more than enough handling and processing of financial data. There is perhaps a need to include additional financial-related data, such as risk assessment and cost-benefit data, in this category.

The financial perspective evaluates how a company is meeting though financial measures. For the valuation of financial perspective we may adopt traditional accounting techniques such as Net Present Value (NPV), Return on Investment (ROI) and Internal Rate of Return (IIR), or even the Expanded Net Present Value (ENPV), which is the business value as estimated by the quantitative ROs analysis (Trigeorgis, 1996).

Learning, Innovation, and Growth Perspective

This perspective includes employee training and corporate cultural attitudes related to both individual and corporate self-improvement. In the current climate of rapid technological change, it is becoming necessary for knowledge workers to be in a continuous learning mode. The importance of learning and growth has to be considered. Metrics can be put into place to guide managers in focusing training funds where they can help the most. In any case, learning and growth constitute the essential foundation for success of any knowledge-worker organization.

Figure 4. Evaluating and implementing business strategy by applying ROs to four BS perspectives

In addition to the aforementioned operational perspective, growth may concern with business knowledge and adoption of new business options based on this specific knowledge. This last is the core idea of the ROs philosophy in strategic perspective, and these growth options may be estimated under quantitative and qualitative perspective (Angelou and Economides, 2009).

Internal Process Perspective

This perspective refers to internal business processes focusing mainly on the operational and management level. Internal process may refer to ICT projects implementation and mainly to ICT systems exploitation. Metrics based on this perspective allow the managers to know how well their business is running, and whether its products and services conform to customer requirements and fulfills the mission. These metrics have to be carefully designed by those who know these processes most intimately. Considering that the business missions are unique and specialized, this definition can not entirely be developed by outside consultants.

In addition to the strategic management process, two kinds of business processes may be identified: 1) mission-oriented processes and ICT systems supported, and 2) support processes and ICT support systems. Mission-oriented processes and systems are business-related special functions, and many unique problems are encountered in these processes. The support processes are more repetitive in nature, and hence easier to measure and benchmark using generic metrics.

Customers Perspective

Recent management philosophy has shown an increasing realization of the importance of “customer focus” and “customer satisfaction” in any business. These are leading indicators: if customers are not satisfied, they will eventually find other suppliers that will meet their needs. Thus, poor performance on these indicators is a red flag of future decline, even though the current financial picture may look good. In order to develop metrics for customer satisfaction, the firm should analyze its customers in terms of their characteristics and the types of processes for which the firm provides its product or service to those customer groups.

For the evaluation and policy implementation of the specified strategy, Angelou and Economides (2008, 2009) proposed ROs under a multi-criteria analysis. In the following, some general guidelines are provided, while the interest reader is referred to the afore mentioned works.

ROs Multi-Criteria Analysis

Furthermore, intangible factors are difficult, if not impossible, to quantify in absolute monetary terms, but they are still important to the decision making process. Particularly, ROs analysis itself brings to the “surface” a number of factors that cannot be quantified, at least easily, by existing ROs models and methodologies. Fichman et al. (2005) called them potential pitfalls of option thinking for risk management and investment evaluation. We integrated some of them in our analysis, in order to achieve a balance between risk control achieved by options adoption and other issues influencing the overall investment’s deployment strategy and limit the options thinking applicability.

Among others, not all investments can be divided into stages implementing stage and expand options. Sometimes a firm should consider an investment as a whole entity, such as when external funds must be raised or when co-investment from other parties is required. Another issue is that stakeholders may prefer all at once funding to obtain maximum control of the investment and have so more time to get a troubled investment back on track before facing a next track of justification. We introduce this possibility in our analysis by considering the intangible factor “CapabilityInterest of staging the investment” (CSI).

In ROs literature, investment opportunities that are known in advance, based on initial infrastructure investments, are treated as growth options, while for the estimation of their values compound option models are utilized. However, in reality, telecommunication growth investment opportunities can be hardly defined during the decision phase (Benaroch, 2002). For this reason, we model qualitatively the existence of growth investment opportunities, which are based on investments in previous phases of a firm’s business activity and cannot be defined quantitatively in advance.

Concerning growth options, the main challenge is the difficulty of estimating their values (due to ambiguity of future cash flows) and uncertainty about the appropriate value for option model parameters. We name this intangible option factor as no clarified growth options (NCO). Also, building in option to abandon or contract operation may concern intangible costs related to credibility and morale. We model this possibility by the intangible factor cost of scaling down operation (CSO). Finally, a potential pitfall of switch-use option is that it can add extra time and expense to the development of the initial information communication technology platform in order to change from shadow to real option. Creating this option (making it real) usually involves making the ICT platform more generic and modular in order to let higher flexibility, experiencing however higher cost. We model this issue as intangible factor named cost of systems flexibility-modularity (CSF).

Internal processes efficiency and customers’ satisfaction are strongly related risks inherent to ICT systems implementation and running. ROs have been already applied for ICT projects risk management. Risk management strategies are oriented towards identifying different types of risks, assessing their relative importance for the project, and implementing strategies for managing risks (Kumar, 2002). Risk management actions can be viewed as being of two types. The first type is oriented towards reducing the degree of risk; for example, a major source of uncertainty in IT projects is the uncertainty regarding the scope or specifications of the project. This can be partially resolved by interviewing multiple stakeholders. However, since risk cannot be completely eliminated, a second type of strategy, oriented towards hedging risks is important. Risk hedging strategies are insurance-like ones oriented towards minimizing the negative impact of risk, when the associated uncertainty is resolved over time. For example, specification uncertainty in ICT projects may be due to uncertain business conditions that may be resolved as the project progresses. ICT risks can be placed into three categories (Benaroch, 2002; Brautigam and Esche, 2002).

• Firm-specific risks: Are due to uncertain endogenous factors (endogenous or technical uncertainty). They could be the result of uncertainty regarding the ability of the firm to fully fund a long-term capital-intensive investment, the adequacy of the firm’s development capabilities to a target investment, the fit of the target application with various organizational units, etc. These factors affect the ability of the investing firm to successfully realize an investment opportunity.

• Competition risks: Are the result of uncertainty about whether a competitor will make a preemptive move, or simply copy the investment and improve on it. These risks give rise to the possibility that the investing firm might loss part or all of the investment opportunity.

• Market risks: Are due to uncertain exogenous factors that affect every firm considering the same investment (exogenous or market-related uncertainty). These risks could be the result of uncertainty about customer demand and prices for the products or services, a target investment yields, potential regulatory changes, unproven capabilities of a target technology, the emergence of a cheaper or superior substitute technology, and so on. These factors can affect the ability of the investing firm to obtain the payoffs expected from a realized investment opportunity.

Research on technology investment’s evaluation and risk management recognizes that the ROs thinking emphasizes the sources of risks inherent in such investments and contributes to risk control.

For controlling these risks managers can adopt a number of investment modes:

Defer investment: To learn about risk in the investment recognition stage. If we don’t know how serious some risk is, the option to defer investment permits learning about the risk by acquiring information passively (observe competitor moves, review emerging ITs, monitor regulatory actions, etc.) or actively (conduct market surveys, lobby for regulatory changes, etc.). Such learning-by-waiting helps to resolve market risk, competition risk, and organizational risk. Apparently, the greater the risk, the more learning can take place, and the more valuable is the deferral option.

Partial investment: With active risk exploration in the building stage. If we don’t know how serious some risk is, investing on a smaller scale permits to actively explore it. Three options facilitate learning- by-doing, that is, enable gathering information about the firm’s technological and organizational ability to realize the investment successfully. The option to stage investment supports learning via a sequential development effort, and the options to pilot and prototype support learning through the production of a scaled down operational investment. The last two options compress the investment lifecycle, thus allowing to learn early how competitors, customers, regulatory bodies and internal parties will react to the investment initiative. Put another way, these options permit market risk, development risk and organizational risk to be transferred to earlier parts of the full scaled investment lifecycle. Similarly, the stage option divides the investment realization effort into parts, thus permitting to transfer risk across parts within the building stage. For example, implementing the riskiest parts of the realization effort as early as possible helps to reveal up-front whether the entire realization effort can be completed successfully (e.g., within schedule and budget).

Full investment with reduction of the expected monetary impact of risk in the building and operation stages: Here, options help to lower the value consequences of risk and/or the probability of its occurrence. An example of the former is the option to lease development resources, which protects against development and market risks by allowing to kill an investment in midstream and save the residual cost of investment resources. A way to lower the probability of risk occurrence is the option to outsource development. This option lowers the risk of development failure by subcontracting (part or all of) the realization effort to a third party that has the necessary development capabilities and experience. In essence, both these options permit transferring risk (partially or fully) to a third party.

Dis-investment/Re-investment with risk avoidance in the operation stage: If we accept the fact that some risk cannot be actively controlled, two options offer contingency plans for the case it will occur. The option to abandon operations allows redirecting resources if competition, market or organizational risks materialize. The option to alter scale allows contracting (partially disinvest) or expanding (reinvest) the operational investment in response to unfolding market and organizational uncertainties.

Based on the logic of these investment modes, the mapping of specific risks to specific options that control them can be refined to fit any class of IT investments. Examples of ROs thinking in the basis of the aforementioned investment modes are provided by Benaroch (2002) and Angelou and Economides (2007). Particularly, they apply ROs thinking based on the aforementioned investment modes for analyzing information technology investment opportunities. ROs analysis can control different sources of risks existing in the various stages of the investment life-cycle.

Strategy Matrix Presentation

The strategy matrix may be a useful visualization and summarization tool. It displays objectives, measures, targets, and initiatives in one table. The strategy matrix can point to areas where scorecard elements might be out of balance. For example, there may be a cluster of initiatives around one objective, while other objectives have no supporting initiatives. This can be useful when prioritizing spending for projects. Typically, the strategy matrix will reflect a strategic theme, so one matrix is prepared for each theme. Table 1 presents an example of BS template formulation including ROs philosophy.

Evaluate and Implement Strategy

For the evaluation of the defined strategies multicriteria decision analysis ROs models may be adopted such as provided in Angelou and Econo- mides (2009) work.

Monitor and Correct Strategy

During the implementation of the selected strategy there is a continuous monitoring for comparing for the defined measures, (i.e. performance indicators) the ex ante and ex post data analysis.

In overall, the aforementioned analysis can be summarized as following:

Summary

The proposed methodology involves four main steps that must be repeated over time as more information is collected concerning the overall business environment. These steps help to optimally configure, evaluate before, during and after implementation the business strategy under the information set available initially, but as time passes they must be re-applied in case that some risks get resolved or new risks surface. In particular, the formulation of the BS is the first main step. Implementation of the scorecard generally begins at the corporate level, but is useful at all levels of an organization. The scorecard is not only an executive information system for corporate management but should form the basis for promoting behavioral change in the organization to conform with the vision and strategy. Often this means pushing the scorecard methodology down through the organisation. Analytically, the proposed steps are given in Table 2.

DISCUSSION AND FUTURE TRENDS

Business vision translation to more practical aspects concluding to specific strategy actions is the first step for defining business strategy, not only in ICT field but in overall business generally. This work proposes BS for connecting organizations vision to specific business stragegy. BS provides

Table 1. Example strategy matrix under ROS analysis

| Strategy Formulation Example Combining BS and ROs | |||||

| Objective | Measure | Target | Initiative (action) | ROs analysis - Implementation Policy | |

| Financial | Increase profitability | Expanded Net Present Value (Trigeorgis, 1996) | > 2 Mˆ year 1 > 5 Mˆ year 3 | New Projects implementation | Quantitative ROs analysis (Angelou and Economides, 2009) |

| Avg. # of days to breakeven | < 180 days year 1 < 130 days year 3 | Operations review and new monitoring systems implementation | Quantitative ROs analysis (Angelou and Economides, 2009) | ||

| Increase sales | Revenue per customer | > $ X year 1 > $ Y year 3 | Self-service checkout pilot | Quantitative ROs analysis (Angelou and Economides, 2009) | |

| Customers | Domination in the market | Avg. # daily new customers | > X in first 6 mos., > Y in first year, > Z by year 3 | Local marketing/Web portal implementation for customers support. | Multicriteria ROs (Angelou and Economides, 2009) |

| Avg. ˆ customer purchase | > $ X year 1 > $ Y year 3 | ||||

| Internal Processes | Increase customers support processes efficiency | Days lag between new customers applications and finally customers connection | < 30 days year 1 < 10 days year 3 | GIS system integration with Enterprise Resources Planning (ERP) | Multicriteria ROs (Angelou and Economides, 2009) |

| Improve procurement processes efficiency | % of procurements outsite from yearly procurement program | < 30% year 1 < 10% year 3 | Web-based procurement process | Multicriteria ROs (Angelou and Economides, 2009) | |

| Learning & Growth | Use business intelligence systems | % eligible employees trained | >90% year 1 >99% year 2 | In-house system training | Multicriteria ROs (Angelou and Economides, 2009) |

| Integrated knowledge management | # projects documents included | < 10 year 1 < 20 year 2 < 40 year 3 | Corporate data warehouse system | ||

Table 2. The steps in the proposed analysis

| Identify Vision | Create a Balanced Scorecard: You have to identify a vision. Where is the organization going? |

| Identify Perspectives | By identifying strategies you tell how you will get there. Define perspectives, which means you have to ask what do we have to do well in each perspective. |

| Identify Performance Indicators | Identify the Performance Indicators - when enough is enough, and when not. Thereafter ask how do we measure that everything is going the expected way? |

| Identify Strategies Alternatives | Define alternatives to be analyzed under ROs multicriteria analysis. |

| Evaluate Strategies Alternatives | Now it is necessary think of the evaluation of your Scorecard under. multicriteria ROs analysis. Consider how do secure that the right things are measured? |

| Implement Selected Strategy - Create Action Plans | Based on this work you should create action plans and plan reporting and operation of the Scorecard. |

| Follow Up and Manage | Monitor strategy implementation and take corrective ations |

a framework in four perspectives crossing through operation, management and strategic level of the organization. It may include both quantitative and qualitative analysis. This work combines this framework with ROs philosophy for defining, evaluating and implementing business strategy by exploiting business flexibility. In particular, business flexibility may concern investment time, deployment scale, and products characteristics in a way that the involved uncertainties become more clear and being at least partially resolved.

ROs support managers to evaluate and manage risky ICT investments. Also, senior finance executives are becoming increasingly aware of the need to view major risky capital investments as options.

ROs have already applied in the literature for investment management and evaluation of ICT investments. In practice managers identify risks and formulate strategies that can control these risks in the most efficient way. These strategies may contain option analysis and the target is to map options to risks and find the optimum combination of them in order to achieve the optimal value for the investment opportunity. However, the option analysis experiences criticism concerning the need for the parameters quantification of the option models. The issue becomes even more complicated in ICT markets. Particularly, after the markets liberalization competition intensity has been increased dramatically and the players are usually so many that oligopoly models are becoming very complicated to be used in practice. Hence, the quantitative analysis of competition influence in telecom investment opportunities is a very difficult task that requires high-level of mathematical modeling and high number of assumptions while managers and practisians quite often do not “feel comfortable” to adopt it.

Instead, we provide qualitative option thinking. The proposed analysis requires from the management and business analysts to recognize qualitatively the options, during the lifecycle of an investment opportunity that can at least partially control specific risks. Sometimes deferring an investment may be optimum, while some other times the immediate implementation is the best solution adopting afterwards a step-wise deployment strategy during building and operation period. In our analysis, we are not only based on qualitative option thinking but also integrate financial tangible and intangible factors coming by both the nature of the telecommunication investments and the options analysis itself.

However, ROs are not a tool for defining strategy in a common methodological decision analysis “platform.” For this purpose, BS technique is adopted for translating the vision to specific strategy.

The proposed framework seem quite generic. If can be also applied in information technology (IT) service management (e.g. ITIL) and IT governance (e.g. Cobit). Particularly, they deal with issues such as how to provide a good service at the good price. People combine these approaches to the maturity concept. Indeed, one can map ITIL process onto the perspective of the standard IT Balanced Scorecard (BSC) as presented below (Mingay and Bittinger, 2002).

IT BSC Business Contribution:

◦ Financial Management

IT BSC User Orientation:

◦ Service Level Management

◦ Availability Management

◦ Continuity Management

◦ Incident Management

◦ Financial Management

IT BSC Operational Excellence:

◦ Problem Management

◦ Service Level Management

◦ Change Management

◦ Service Level Management IT BSC Future Orientation:

Service Level Management Capacity Management Change Management Financial Management

CONCLUSION

There is a large consensus among academics and practitioners that ICT investments should be carefully justified, measured and controlled. The fact that most decisions on ICT investments are still taken by the financial department might add to the choice for these traditional techniques. Nevertheless, serious doubts about the fitness of these techniques in an ICT environment arise. ICT investments have special characteristics (high risk, large proportion of intangible/hidden costs and benefits) which makes the use of these techniques very difficult and the reliability of the outcome most uncertain. This work suggests using a multi-layer evaluation process or an evaluation process derived from the balanced scorecard for the appraisal of ICT investment projects. Particular, the current work provides a decision analysis framework, based on BS and ROs integration, for defining, evaluating and implementing ICT business strategy adopting quantitative and qualitative analysis. It is the first time in the literature, to our knowledge, where BS and ROs are combined in a common framework of analysis offering a multicriteria strategy definition and evaluation model. A limitation of the proposed work is the lack of real world application. In addition, it can be further analyzed based on more ICT factors related.

REFERENCES

Angelou, G., & Economides, A. (2005). Flexible ICT investements analysis using real options. International Journal of Technology. Policy and Management, 5(2), 146-166.

Angelou, G., & Economides, A. (2007). E-learning investment risk management. Information Resources Management Journal, 20(4), 80-104. doi:10.4018/irmj.2007100106

Angelou, G., & Economides, A. (2008). A decision analysis framework for prioritizing a portfolio of ICT infrastructure projects. IEEE Transactions on Engineering Management, 55(3), 479-495. doi:10.1109/TEM.2008.922649

Angelou, G., & Economides, A. (2009). A multicriteria game theory and real options model for irreversible ICT investment decisions. Telecommunication Policy Journal, 33, 686-705. doi:10.1016/j.telpol.2009.07.005

Angelou, G., & Economides, A. (2013). Broadband business by utilities infrastructure exploitation: A multistage competition model. Telecommunications Policy, 37, 63-79. doi:10.1016/j. telpol.2012.07.009

Azadeh, A., Keramati, A., & Jafary Songhori, M. (2009). An integrated Delphi/VAHP/DEA framework for evaluation of information tech- nology/information system (IT/IS) investments. International Journal of Advanced Manufacturing Technology. doi:10.1007/s00170-009-2047-2

Benaroch, M. (2002). Managing information technology investment risk: A real options perspective. Journal of Management Information Systems, 19(2), 43-84.

Benaroch, M., Lichtenstein, Y., & Robinson, K. (2006). Real options in information technology risk management: An empirical validation of risk-option relationships. MIS Q., 30(4), 827-864.

Bloomfield, C. (2002). Bringing the balanced scorecard to life: The Microsoft balanced scorecardframework (White Paper). Insightformation, Inc.

Brautigam, J., & Esche, C. (2003). Uncertainty as a key value driver of real options. In Proceedings of 7th Annual Real Options Conference. IEEE.

Fichman, R., Keil, M., & Tiwans, A. (2005). Beyond valuation: Option thinking in IT project management. California Management Review, 47(2), 74-95. doi:10.2307/41166296

Gomez, R., Pather, S., & Peninsula, C. (2010). ICT evaluation: Are we asking the right questions? Paper presented at International Development Informatics Conference. Cape Town, South Africa.

Gunasekaran, A., Ngai, E. W. T., & McGaughey, R. E. (2006). Information technology and systems justification: A review for research and applications. European Journal of Operational Research, 173(3), 957-983. doi:10.1016/j.ejor.2005.06.002

Kaplan, R., & Norton, D. (1992, January-February). The balanced scorecard: measures that drive performance. Harvard Business Review, 71-80. PMID:10119714

Kaplan, R., & Norton, D. (2007, July-August). Using the balanced scorecard as a strategic management system. Harvard Business Review. PMID:17286078

Lee, K., Shyu, D., & Dai, M. (2009). The valuation of information technology investments by real options analysis. Review of Pacific Basin Financial Markets and Policies, 12, 611. doi:10.1142/ S0219091509001770

Lin, C., Huang, Y., & Cheng, M. (2007). The adoption of IS/IT investment evaluation and benefits realization methodologies in service organizations: IT maturity paths and framework. Contemporary Management Research Pages, 3(2), 173-194.

Mingay, S., & Bittinger, S. (2002). Combine CobiT and ITIL for powerful IT governance (Research Note, TG-16-1849). Washington, DC: Gartner.

Mun, J. (2002). Real options analysis: Tools and techniques for valuing strategic investments and decisions. New York: Wiley Finance.

Otim, S., Dow, K., Grover, V., & Wong, J. (2012). The impact of information technology investments on downside risk of the firm: alternative measurement of the business value of IT. Journal of Management Information Systems, 29(1), 159-194. doi:10.2753/MIS0742-1222290105

Renkema, T. (1999). The IT value quest: How to capture the business value of IT-based infrastructure. New York: John Wiley & Sons, Ltd.

Trigeorgis, L. (1996). Real options: Managerial flexibility and strategy in resource allocation. Cambridge, MA: The MIT Press.

Willcocks, L., & Lester, S. (1994). Evaluating the feasibility of information systems investments: Recent UK evidence and new approaches. In Information management: The evaluation of information systems investments. London: Chapman & Hall. doi:10.1007/978-1-4899-3208-2_3

Zehir, C., Muceldili, B., Akyuz, B., & Celep, A. (2010). The impact of information technology investments on firms performance in national and multinational companies. Journal of Global Strategic Management, 7, 143-154.

KEY TERMS AND DEFINITIONS

Balance Score Card: The balanced scorecard (BSC) is a strategy performance management tool - a semi-standard structured report, supported by design methods and automation tools, that can be used by managers to keep track of the execution of activities by the staff within their control and to monitor the consequences arising from these actions.

Investment Cost: The amount of money spent for the investment, investment expenditure required to exercise the option (cost of converting the investment opportunity into the option’s underlying asset, i.e. the operational project).

Multi-Criteria Business Analysis: Analysis of business under multicriteria perspective for finding the optimal deployment strategy and estimating its overall performance.

Real Option: It is the extension of financial options concept to real assets.

Risk Management: The process of identifying different types of risks, assessing their relative importance for the project, and implementing strategies for managing risk.

This work was previously published in Approaches and Processes for Managing the Economics of Information Systems, edited by Theodosios Tsiakis, Theodoros Kargidis, and Panagiotis Katsaros, pages 91-107, copyright 2014 by Business Science Reference (an imprint of IGI Global).