Chapter 73 Innovation in Business Models of Banks in Europe: Towards a Methodological Approach

Konstantinos Liakeas

University of the Aegean, Greece

Anastasia Constantelou

University of the Aegean, Greece

ABSTRACT

Since the end of the 1990s, the introduction of Internet technology to the mainstream technologies used in businesses led to the expectation of pure Internet enterprises that might eliminate physical presence to one or more points in the value chain.

A sequence of failures managed to resize those expectations and led most firms to just expose routine back end systems transactions through the Internet without a clear focus on relationship building or an integrated cross-channel sales approach. Despite the structural changes to the business level strategy that the Internet may have brought to firms in many industries, business practices in banking have not really evolved. This is because banks perceived Internet-based innovation as an investment opportunity that could raise spatial and temporal constraints much like ATMs had done in the past, without actually changing the value proposition of the business model or the strategic options of financial institutions. This chapter argues that the degree to which financial institutions have actually infused innovation into their traditional business model has been negligible and aims to set out a scene for the study of the evolution of strategy and business models of banks in the Internet era.INTRODUCTION

The introduction of internet technology to the mainstream technologies used in businesses, led to the expectation of pure internet enterprises that might eliminate physical presence to one or more points in the value chain. Especially in the cases

DOI: 10.4018/978-1-4666-6268-1.ch073

of non-tangible goods or in cases where parts of the value chain could become dematerialized - like money transactions, telecommunications spectrum, software or music - expectations were really high and in some cases business plans were justified based on these expectations in order to support such e-businesses (for example, pure ebank entities like Egg1).

A sequence of failures managed to resize those expectations and led most firms to just expose routine back end systems transactions through the internet without a clear focus on relationship building or an integrated cross-channel sales approach. This resizing of expectations2 led in certain cases to a mismatch between the initial decision for an additional revenue stream that would result from shifting business online, and the actual multi-channel approach that was finally adopted. In the banking sector, in particular, this was especially obvious in cases where e-business was implemented through an additional channel and not as a pure e-bank entity..

Although in certain industries (ICT, retail commerce etc.) internet technology has led to a differentiation in the business level strategy and business models, in the bulk of the traditional banking sector business practices have not really evolved. Despite the structural changes (to business level strategy or business model) that internet may have caused to firms in most industries, the banking sector seems the least affected. Most banking institutions perceived Internet-based innovation as an investment opportunity and funded businesses that based their business models on these technologies. However, as this chapter argues the degree to which these institutions have actually infused innovation into their business models has been so far negligible. This initial perception has been our primary stimulus for an in-depth investigation into the ways in which the strategy and the business models of banking institutions appear to have evolved in the Internet era.

Our starting hypothesis in this chapter is that, in this changing environment, incumbent banks opted to push their existing business models to the extreme - underestimating in many cases lending risk (Nellis, McCaffery, & Hutchinson, 2000) - than to investigate the opportunities offered in the provision of higher value products and services.

The latter stem out of the observable deconstruction of banks’ traditional value-chain activities and the revision of their current approach in conducting business. This chapter aims to function as a provocative first attempt to explore the validity of the aforementioned hypothesis. To do so, it develops an analytical framework that allows for an in-depth investigation into the evolution of business models surrounding the operation of commercial banks in Europe over the last decade.The chapter does not aspire to unfold a fully- fleshed theoretical framework regarding the complexity of the dynamics shaping the banking industry in the Internet era. Rather, drawing upon observed industry trends, it uses a methodological approach that allows for the measurement of the “behavior” of an organization, that is the initiatives stemming from its business plan, the processes, and the performance metrics used to plan and realize its business model. To this end, the aim here is to go one step further and develop an operational tool that can guide future work in the identification of innovation in the business models and business level strategy of commercial banks during the first years of the Internet era.

The structure of the chapter is as follows: the following Section Two summarizes briefly the main arguments found in the literature regarding the impact of Information Technology (IT), and of the Internet in particular, on the banking industry and the subsequent emergence of new business models in the banking sector. Section Three presents the theoretical elements upon which a conceptual framework is built for the study of the behavior of incumbent banks in the networked era. This conceptual framework guides the empirical investigation in the subsequent Section Four of the main hypothesis stated at the beginning of the chapter. The Concluding Section summarizes the main arguments posed and proposes directions for further research.

INFORMATION TECHNOLOGY AND THE INTERNET IN BANKING: A REVIEW AND SOME PENDING ISSUES

In the current electronic environment, Information Technology (IT) has been seen as a dominant element in organizations’ competitiveness and growth.

In the banking industry, in particular, IT has been the backbone of all multilateral Business- to-Business (B2B) and Business-to-Customer (B2C) financial transactions. Banking institutions have been pioneers in the adoption of IT-based innovations, such as electronic markets, clearinghouses, and multilateral trading facilities. Banks also use IT and the Internet as a strategic weapon to face competition in the consumer markets by developing services such as e-banking, that offer them the possibility to enhance their relationships with customers (Marine, 2013).Several studies discuss IT in banking in terms of strategy- technology alignment that can potentially lead to organizational growth and development. For example, previous studies have focused on several strategic issues such as the internal and external factors (e.g. government regulation, costs, technology platforms, competition, etc) that influence the development of e-banking strategies (Smith, 2006); the strategies for the successful implementation and development of multichannel banking services (Gurau, 2005); the assessment of the level of banks’ readiness for providing e-banking services (Huang, Huang, Zhao, & Huang, 2004); the role of technological aspects and IT employees’ capabilities in creating value for banking firms (Lin, 2007); and the internal organizational critical success factors in e-banking adoption by banking institutions (Shah & Siddiqui, 2006). Another strand in the literature has been looking at consumers’ perspective, their acceptance of e-banking technologies and the factors that seem to affect their evaluation of e-banking trustworthiness and their subsequent adoption behavior (Tan & Teo, 2000; Yap, Wong, Loh, & Bak, 2010). For example, studies in this area address the issue of trust and the confidence that can be cultivated among customers about the security and integrity of their transactions as a particularly influential factor. Last, but not least, the measurement of the impact of e-banking in terms of business value creation has been also attracted researchers’ attention over the last decade (Stamoulis, Panagiotis, & Drakoulis, 2002).

Still, amidst these technologically deterministic approaches of IT research in banking, there are other approaches that take a longer and more strategic perspective (Li, 2001; Alt & Puschmann, 2012; Marine, 2013). These approaches seek to assess the extent to which, and the particular ways in which, the adoption of IT and the Internet shake the mere foundations of the banking industry causing a major disruption in the operation of the traditional business model of banks, which has been based on process integration, service bundling, scale economies, and the monopolization of distribution channels (Li, 2001).

Initially, the deployment of the Internet by banking institutions in their routine procedures and practices was more seen as a cost-cutting and distribution-extending mechanism, which could further enhance the existing vertically integrated and consolidated banking model. It could do so, as the cost of processing a transaction over the Internet was significantly lower than the cost of handling it over the counter, whereas the convenience of having Internet banking available anytime and anywhere allowed banks to extend their distribution network using cheaper and more convenient solutions. In parallel, another trend made its appearance: that of the unbundling of the banking services and the re-intermediation of the traditional value chain of banking activities by third party, non-bank-related newcomers, who specialize on specific niche activities (Li, 2001). As a first example of this unbundling of the value chain, one could refer to the new actors that entered the market, such as Pay Pal and VeriSign, which started their businesses by offering payment transaction and security management facilities between business and consumers. More recent examples of similar nature and scope include services such the collaboration of Google, Citibank and Mastercard to establish a mobile payment system, Vodafone’s plan to provide a banking infrastructure for Africa and Facebook’s engangement into developing “Facebook Credits” (Alt & Puschmann 2012).

Over a decade ago, Li (2001) made a first attempt to conceptualize the complex picture in Internet banking in the UK by identifying eight such prevalent models. These ranged from more conservative ones, which treated the Internet as merely a “new distribution channel,” to more revolutionary ones like those of “brand-stretching,” where non-bank players with established brand name were using the Internet to serve banking services to selected customers; and “pure-play new entrants,” which have been experimenting with entirely new business models. Li concluded that:

.if [incumbent] banks do not proactively reinvent the industry by adopting new strategies, new entrants will increasingly take away profitable businesses from them by leveraging the potential of the Internet and other new technologies. By then, not only will strategic opportunities have been lost, but many existing banks may have no choice but to change or die (Li, 2001:320).

A decade later, a similar observation is made by Marine (2013). He sees IT developments interfering in the traditional business model of banks pushing them to choose between what he calls “transaction banking” and “relationship banking.”3 The former relates more to the banks’ traditional business model of reaping the benefits of scale and scope in standardized operations, whereas the latter places an emphasis on the redesign of business processes and on the exploitation and strengthening of relationships with customers. In this respect, his analysis concludes that:

...the future structure of the banking industry is blurred. On the one hand, large universal banks would focus on IT-driven economies of scale and scope in transaction banking activities. On the other hand, small, customer-focused banks should use IT developments to further cultivate relationship ties with their customers (p.93).

This chapter argues that the degree to which incumbent banks have actually got accustomed to these new opportunities and challenges by infusing innovation into their traditional business model has been negligible. The value proposition of the business model of most incumbent banking institutions has not changed much and is still based on what they know to do best: reaping the benefits of process integration and service bundling. A typical example of the extent to which the business practices of incumbent banks have remained unchanged comes from the U.S. There, the biggest retailers Wal-Mart and Home Depot have applied for banking licenses. Also major players in the auto making industry (VW, BMW) have already completed this process4. These new actors enter the banking market with new IT-based business models. This is not surprising since banking is essentially an information intensive sector which trades information-based products and services that can be accessed from a variety of Internet-enabled devices. It is obvious that financial institutions themselves could provide “white label” products and services to these organizations but have either decided not to do so or keep postponing such a shift in their business model. Beyond that, banks have not yet started to offer as a service the skill set that they have seen enterprises from other industries developing internally. Skills like capital management, transaction platform design deployment and management5 are examples of core competencies that financial institutions could provide as white label services. Although certain brands from nonbanking industries may have had the gravity to develop this know how internally, there are others that either do not have the capacity to follow the same approach or choose to focus on developing their core competences, i.e. the production and distribution of goods and services.

The changes in the financial payments landscape with the implementation of the Single European Payments Area (SEPA)6, provide an additional basis that will further enhance the opportunities for new non-banking organizations to provide payment services intercepting this commission generating activity that until now has been carried out exclusively by banks. This interception, beyond the obvious reduction of operating income, will deprive banks from data related to the transactional behavior of their clients, as well as from opportunities for cross-selling and up-selling. Almost in parallel, regulatory changes in the financial sector like the implementation of the single market programme7 has further boosted cross border competition.

In the banking literature, (and especially the part that refers to commercial banks), the evolution of banking operations has often been examined through a series of events like crisis, rescues, mergers and regulation. Evolution has been observed in relation to economic growth through capital mobilization and credit creation. This chapter looks at the evolution in banking from a different perspective: that of business model innovation. The key role of business models in the evolutions linked to ICTs and the corresponding innovative strategies (Chesbrough, 2006; Teece, 2009) was pointed out in the literature a few years ago (Mahadevan, 2000) and has been gradually defined and refined from a strategic perspective (Zott and Amitt, 2008). Of particular interest is the application of this concept to the evolution of incumbent commercial banks. The next sections propose a framework for identifying business model innovation in traditional banks.

TOWARDS A CONCEPTUAL FRAMEWORK FOR IDENTIFYING BUSINESS MODEL INNOVATION IN BANKING

Defining a Business Model

Strategy is a broad term. In the context of this chapter, we use it to denote the process of selecting the environment within which a company is positioned, as well as the process of selecting the company’s long term goals and the way to achieve them within this environment. In particular we refer to the content of strategy at the business level (De Wit and Meyer, 2010). That is the level where functional units of the firm (sales, marketing etc.) aggregate to an autonomous entity and cater for specific products or services. Beyond the business level, firms may aggregate to groups that operate within a corporate level strategy. At a higher level, network level strategy guides the course of a firm within the value network that it operates in.

In order for a firm to meet its objectives in the strategically selected business environment, a value proposition must be formed using the available resources to address the needs of selected customer segments. This subset of business level strategy that focuses upon the value the firm delivers to its customers using its resources is of core importance as it is the system that implements strategy. This system has been named “Business System” (De Wit and Meyer, 2010, pp.168) or “Business Model” (Johnson, Christensen, and Kagermann, 2008). A more transaction-oriented definition of the business model concept is the following: “The business model can be defined as ‘the structure, content, and governance of transactions’ between the focal firm and its exchange partners”(Amit and Zott, 2001, pp. 511). Alternatively, a value-oriented definition of the concept of business model is the following (Osterwalder and Pigneur, 2010, pp.14) “A business model describes the rationale of how an organization creates, delivers and captures value.” Internet technology facilitated multiplication of options regarding resources, partners, customer segments, value propositions, therefore the significance of the business model construct increased to the point of it being considered as an autonomous concept.

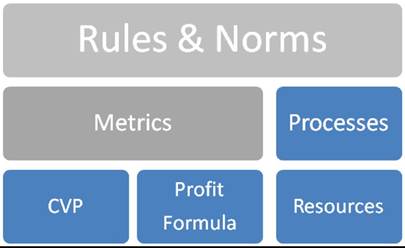

Johnson, Christensen, and Kagermann (2008) provide a structural perspective to the business model definition. They identify the concept as consisting of the following key elements:

1. The Customer Value Proposition: A suitable product-service combination to address a real need of selected customer segments.

2. The Profit Generation Model: A monetary view of the value creation mechanism considering the revenue generation concept, the cost structure (direct, overheads, economies of scale), etc.

3. Key Resources: People, know how, partners, marketing and corporate communication, channels etc. Whatever is needed to deliver the Customer Value Proposition.

4. Key Processes: The processes that -using the key resources available- will deliver the Customer Value Proposition in a measureable, scalable, and manageable way.

This approach regarding the structure of the business model, enriched with rules and metrics as the connecting tissue for the system to work, is depicted in Figure 1 (Johnson, 2010).

Business Model Innovation

The concept of Innovation covers a wide range of activities from discovery and invention to development and commercialization. Innovation is usually perceived as the end offering (the final form of product or service) and as being tightly coupled with some sort of technological novelty. Innovation in the business model is defined after Conway and Steward (2009, pp. 14) as “novelty in the drivers of an organization’s activities or strategy.” For the purpose of analysis in this chapter, we seek to identify elements that prompt either to architectural or to component level innovation at the business model or the business level strategy of commercial retail banks during the last 15 years.

As an example of business model evolution within the banking domain one could consider the way the scope of banks has changed over time. Capital mobilization has been the initial value proposition of financial institutions since ancient and medieval times. Main resources were own funds -and in time deposits-, processes and rules handling operational and credit risk. Profit was generated by interest on loans. Currency exchange and fund transfers reformed the value proposition allowing for regional specialization in production of goods. This additional value proposition allowed for additional commissions reforming the traditional revenue scheme and adding operational risk which then affected the cost scheme.(Grossman, 2010).

In this vein, one may consider whether the regulatory obligation of financial institutions to reserve capital constitutes an evolution of their business model. This is because it definitely affects their cost structure both directly and indirectly in the form of opportunity cost as the reserved capital cannot be used for investments or for funding loans. The approach adopted in this chapter is that whatever

Figure 1. The Four Boxes business modelframework

Adaptedfrom Johnson (2010, pp.24)

does not affect the value proposition of banking institutions towards their customers and business partners will not be considered as innovation in their business model evolution.

Operationalising Strategy:

The Delta Model

The attempt to study evolution of strategy and business models of financial institutions involves a number of challenges. Strategy frameworks (at least the dominant ones like M. Porter’s Competitive Advantage or the Resource Based View of the firm) are conceptually useful when used to define the competitive positioning of an organization but difficult to be applied in practice. More than often, the process of identifying the strategy of a particular organization ends up as an intuitive exercise. What is more, the term “business model” is often broadly defined making the boundaries with the concept of strategy quite obscure.

In most cases, the strategy and business models of organizations are not explicitly documented beyond a mission statement. Of course there are a number of reasons that justify the lack of a complete strategy statement. Evolution of business as a series of reactions to environmental changes gives the impression of a preconceived strategy (Andrews, 1987). However even if strategy is not clearly articulated it can be deducted from the “behavior” of the organization, where “behavior” refers to the initiatives stemming from the business plan, the processes, and the performance metrics used to plan and realize its business model.

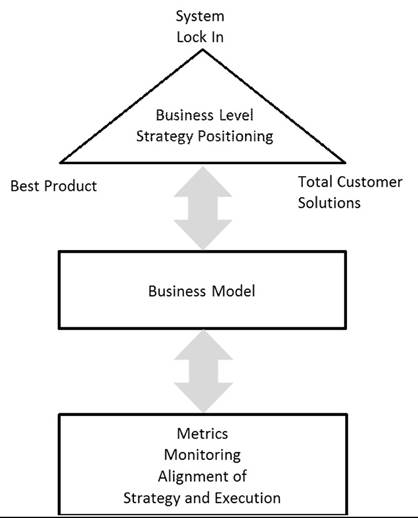

The review of the various strategic frameworks that could be more useful in identify business level strategy paved the way to the Delta Model (Hax & Wilde, 2001), a recent framework developed as a complement to existing ones. The main characteristic of this framework is that beyond the new elements at the conceptual level, it ties the strategic positioning at the business strategy level with the business model through which this positioning is realized. It also uses metrics as sensors to monitor the alignment of strategy to its implementation. The Delta Model provides a framework that allows an organization to position its business level strategy on a hypothetical triangle according to where its focus lays on regarding its products, its customers, and its complementors (firms that deliver products and services that enhance the organization’s product and service portfolio) within its business environment.

As already indicated, this framework was developed in order to complement existing strategy frameworks that relied more on the mechanism of competition, whereas the Delta Model puts an emphasis on bonding with customers and complementors. The framework has three major components which are the following:

The “Triangle,” which is a comprehensive representation of three distinct strategic options at the level of business strategy, namely:

Best Product: This refers to the traditional strategic options for most companies that pursue success either by offering low cost products or services, or by seeking product differentiation strategies. Examples of companies seeking to achieve product differentiation are Google Inc. which seeks to offer distinct features to its products, and BMW, which has a hard to establish corporate image.

Total Customer Solutions: This is an option that can be realized either by offering a complete spectrum of products and services that satisfy customer needs through integration beyond discount bundling (e.g. Amazon), or by adding value to the daily routine of customer operations (e.g. GE, Xerox) or by redefining customer experience in a way that encompasses the timeline from customer acquisition till the end of life of the purchased product or service (e.g. General Motors, Saturn).

◦ System Lock In: This option can be achieved either through the use of proprietary standards (as Intel and Oracle do), or as an exchange after achieving a critical mass of customers (e.g. eBay), or by raising barriers to entry to competitors (e.g. Coca Cola, and WalMart through its opt for rural locations).

The business model structure, which in the context of this framework is comprised of the initiatives and the processes needed to realize the selected strategic positioning. These initiatives are grouped in the term Strategic Agenda and the processes in the term Adaptive Processes and cover the areas of :

Defining and offering a Customer Value Proposition called Customer Targeting in the context of the framework.

Defining and operating the cost infrastructure called Operational Effectiveness in the context of the framework.

Defining and operating the revenue infrastructure called Innovation in the context of the framework.

Metrics, which monitor the alignment of the selected strategic positioning with its implementation through the Strategic Agenda and the Adaptive Processes. The framework stresses the inefficiency of using averages as the main aggregate metric and the need to use more elaborate aggregate metrics as well as the need for granular metrics.

A conceptual representation of the Delta Model is presented in Figure 2.

The Delta model provides a way to map the strategic positioning of a firm on the triangle and

identify its evolution over time. Moreover, through the use of metrics it supports the relation between the business level strategy and its realization at the level of the business model. Therefore it supports the identification and mapping on the triangle of the strategy actually executed, which may or may not match to the initially selected strategic positioning.

From Static to Dynamic Approach in Strategy Evolution: The Business Model Canvas

Identifying the strategy and the business model of an organization over specific periods of time is one thing. The ability to identify its evolution over time is another. Throughout the description of the Delta Model by Hax and Wilde (2001), the term business model is used interchangeably with the term strategic option. It implies the group of processes that span across a company’s Operational Effectiveness, Customer Targeting and Innovation. This approach, although fits the purpose of the Delta Model framework, is not suitable for studying how a business model evolves over time. In order to identify evolution in the design and content of the business model (the ‘what’ question) and not just in its application to the operation of the organization through the processes adopted, (the ‘how’ question), another two-dimensional representation of the concept would be more appropriate. The in-depth review of the literature over measures that could be used for the operationalisation of busines s model evolution over time led us to the concept of the “business model canvas” as defined by Osterwalder & Pigneur (2010).

Figure 2. Conceptual representation of the Delta model

Adapted from Hax and Wilde (2001)

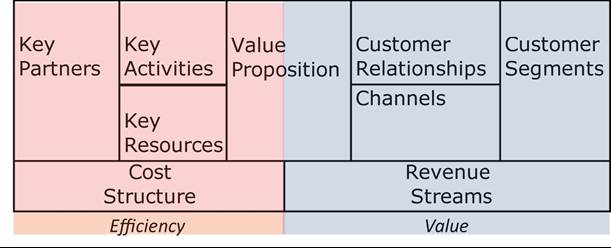

In this concept, the business model construct is broken down into nine elements altogether, namely:

1. The key partners of the company,

2. The key activities,

3. The key resources used for the realisation of activities,

4. The company’s value proposition,

5. The relationships with its customers,

6. The channels through which it establishes presence in the market,

7. The customer segments it serves,

8. Its cost structure, and finally

9. Its revenues streams.

Being a more granular approach to the Four Boxes Business Model Framework discussed above, it is more suitable for the identification of innovation in certain elements of the business model. The concept of business model canvas is built on the assumption that the goal of an organization is to serve specific customer segments through value propositions designed to identify and solve problems as well as to address the needs of these segments. In order to achieve this goal, relationships have to be developed with customer segments and partnerships with external contractors have to be established. In this context, resources are utilized to perform the necessary activities in order to deliver the value proposition to the customer segments through selected channels. All the phases prior to the delivery of the value proposition result in costs and the delivery phase produces revenues. It depends on the business level strategic positioning and the related business model design what the financial goal of the bottom line (net profit, break even etc.) eventually is. This description is depicted in Figure 3.

Figure 3. The main elements of the business model canvas

Business Model Generation, ©Osterwalder & Pigneur (2010). This material is reproduced with permission of John Wiley and Sons, Inc.

Putting it All Together

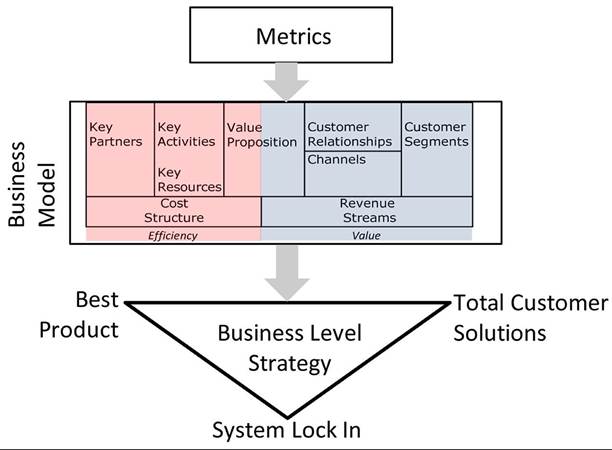

In order to identify a business model’s evolution over time a hybrid approach is adopted which utilizes components from both the aforementioned frameworks. In particular, the business model construct included in the Delta Model is replaced by the more analytical Business Model Canvas. This hybrid framework, will be fed with actual metrics used over time by banking organizations that correspond to the elements of the business model canvas. Depending on the emphasis put on distinct parts of the canvas and on the relationship between the parts, innovation at the level of business model and subsequently at the business level strategy is identified. This is all portrayed in Figure 4. Apart from relying on two complementary frameworks, the novelty of this approach is its inverted direction: the down-arrow figure suggests that using the metrics and allocating them to the appropriate modules of the business model canvas one can characterize the actual behavior of a firm and identify the business model used as well as its business level strategy, as defined by the Delta Model..

APPLYING THE FRAMEWORK TO TEST BUSINESS

MODEL EVOLUTION IN THE BANKING SECTOR

The approach described above has been operationalised in a real case in order to test its validity. The metrics used to feed the model assess the performance of the retail network of a Greek bank at three distinct points in time (2003, 2005 and 2011). It is important to stress that the actual figures do not matter in the context of this paper. It is the nature of the metrics that characterizes the business model and business level strategy actually implemented.

In addition to the metrics provided by the retail network MIS team of a major Greek bank, two interviews with experts were conducted which sought for the opinions of interviewees about the elements of the business model canvas. During these interviews, the retail network business plans were reviewed in order to extract information not directly evident through the metrics. Table 1 presents the metrics collected by the banking

Figure 4. The down arrow approach

Table 1. Mapping of2003 performance metrics to the business model canvas elements

| Value Proposition | As it is obvious from the performance metrics the value proposition is the provision of credit and funds management. Bancassurance offering is emerging. Performance assessment is 100% product based. 8 |

| Revenue | |

| Customer Segments | Professionals running their own business. |

| Affluent customers with over a 100.000ˆ funds under management. | |

| Employees. | |

| Customer Relationships | Cross Selling Ratio. |

| Channels | Own channels such as branch network sales force and Open24 sales force. Phone and internet for commission producing transactions. |

| Retailers (car, appliances, etc.) providing credit. | |

| Revenue Streams | Interest margin, transaction commissions and insurance premiums. |

| Cost | |

| Key Partners | Retailers as additional credit delivery channels. |

| Key Activities | Provide credit aiming at market growth and streamline operations |

| Key Resources | Branch network, unified IT infrastructure, capital from funds under management. |

| Cost Structure | All retail network operating costs are allocated to branches and combined with the revenues per branch form the branch profitability. |

institution which can be mapped into the Business Model Canvas components.

From a business level strategy standpoint, the metrics used to assess the company’s performance in 2003 as well as the interviews held with experts led to an assessment of the company’s strategic focus as being on the Best Product positioning (see Figure 5).

During the interviews, the concept of credit risk mitigation seemed to emerge in the 2005 business plans. Customer service and customer satisfaction concepts also surfaced. However the

Figure 5. Strategic positioning of the Greek bank in 2003

emphasis, as it appears in the metrics used to assess performance was still on volumes and on how to mitigate the saturation at the credit market. The mapping of the 2005 metrics to the Business Model canvas is shown in Table 2.

From a business level strategy standpoint the assessment leads again to a Best Product strategic positioning (see Figure 6).

In the specific bank selected for the case study, a strategic initiative had taken place in 2009 in order to refocus the organization towards a customer centric approach. With the support of a strategy consulting firm the financial institution was aiming to change its structure from pure product oriented, replacing the product oriented business units with customer segment oriented business. Still, despite this effort, the metrics used in 2011, 2 years after this initiative, were still product-oriented although the emphasis was on controlling the costs than on generating profits. Table 3 maps the 2011 performance metrics to the Business Model Canvas.

Figure 6. Strategic positioning of the Greek bank in 2005

Table 2. Mapping of2005 performance metrics to the business model canvas elements

| Value Proposition | As in 2003, the value proposition is provision of credit and funds management. Bank assurance volume is important as well. Performance assessment is still 100% product based. |

| Revenue | |

| Customer Segments | Small Businesses have replaced the initial Professionals segment extending the concept of those running their own business |

| Affluent customers with over a 100.000ˆ funds under management remain a core segment. | |

| Mass retail has extended the Employees segment of 2003 | |

| Customer Relationships | The only metric is still Cross Selling Ratio |

| Channels | Same as in 2003. Own channels such as branch network sales force and Open24 sales force. Phone and internet for commission producing transactions. |

| Retailers (car, appliances, etc.) providing credit | |

| Revenue Streams | Interest margin, transaction commissions and insurance premiums remain the sources of revenue |

| Cost | |

| Key Partners | As retail credit remains the main pillar of the value proposition still retailers act as additional credit delivery channels |

| Key Activities | As the credit market becomes saturated the main activities shift to customer attraction, up selling, cross selling and anti attrition |

| Key Resources | Extension of branch network, customer service training and tools for operational efficiency |

| Cost Structure | No change in this element. Still all retail network operating costs are allocated to branches and combined with the revenues per branch, form the branch profitability |

It is obvious that the bank was trying to conform to changes occurring in the external environment. The disengagement between the metrics and the customer-centric business redesign is obvious, confirming the Delta Model’s attempt to mitigate and align strategy to its execution. Still, in the business model theme, the shift from provision of credit to the defensive position of restructuring credit does not constitute innovation in the value proposition. Therefore in this particular case although there are changes in the elements of the business model as a reaction to the environmental changes, the main theme of delivering value to the customers has not changed.

From a business level strategy standpoint neither the business plans nor the metrics used, could prove a shift of the strategic positioning of the company from Best Product to Total Customer Solutions or to System Lock-In. In the span of 8 years for the particular case the strategic positioning remained Best Product (see Figure 7).

CONCLUDING REMARKS

Starting with an overview of the basics of IT research in the banking industry, and in the light of the increasing use of IT and the Internet by both established actors and newcomers in the sector, this chapter dealt specifically with business model

Figure 7. Strategic positioning of the Greek bank in 2011

Table 3. Mapping of 2011 performance metrics to the business model canvas elements

| Value Proposition | Credit restructuring. Performance assessment is still 100% product based. |

| Revenue | |

| Customer Segments | Small Business has replaced the initial Professionals segment extending the concept of those running their own business |

| Affluent customers with over a 100.000ˆ funds under management remain a core segment. | |

| Mass retail has extended the Employees segment of 2003 | |

| Customer Relationships | The only metric is still Cross Selling Ratio |

| Channels | Open 24 is out of the picture. Branch network is resized. Phone and internet remain sources for commission producing transactions. Retailers still provide credit but pre-credit control is tighter. |

| Retailers (car, appliances, etc.) providing credit | |

| Revenue Streams | As credit risk increases and funds are insufficient, emphasis shifts on insurance premiums and transaction commissions still contribute to revenue |

| Cost | |

| Key Partners | As retail credit recedes, the role of retailers as additional credit delivery channels is not as important |

| Key Activities | Credit restructuring and securing outstanding balances |

| Key Resources | Branch staff |

| Cost Structure | Loan provisions heavily affect the profitability of the branches |

innovation in traditional banks. A framework was built which could support the monitoring of evolution of incumbent firms’ business models through the use of metrics collected at the business level. To put the framework to the test, it was fed with metrics used to monitor the performance of a retail bank network over the last 8 years. This made possible the examination of the evolution of the customer value proposition (the core business model element) as well as of the strategic positioning of the bank. The empirical application of methodology indicated that, at this level, no significant changes to the business model were identified.

As this is an ongoing research, the conceptual framework presented can be further fine-tuned. Future research could produce a more extensive list of parameters that could include explicit as well as implicit metrics that go beyond the retail branch network domain to the rest of the commercial bank activities. Additionally, further research could enhance our understanding as to the ways in which banks view innovations like Peer-to-Peer lending and financial management platforms that have developed outside of the banking industry. Last but not least, the validity of this framework depends to a significant extent upon the proper design of information systems that bear the collection and processing of metrics and, as a result can support the short- and long-term operation of banking institutions. In this regard, information systems’ design and performance represents a necessary condition for the further testing and use of this framework.

REFERENCES

Alt, R., & Puschmann, T. (2012). The rise of customer-oriented banking - Electronic markets are paving the way for change in the financial industry. Electronic Markets, 22, 203-215. doi:10.1007/s12525-012-0106-2

Amit, R., & Zott, C. (2001). Special issue: Strategic entrepreneurship: Entrepreneurial strategies for wealth creation. Strategic Management Journal, 22(6-7), 493-520. doi:10.1002/smj.187

Andrews, K. (1987). The concept of corporate strategy. New York, NY: McGraw-Hill.

Chesbrough, H., Vanhaverbeke, W., & West, J. (Eds.). (2006). Researching a new paradigm. Oxford, UK: Oxford University Press.

Conway, S., & Steward, F. (2009). Managing and shaping innovation. Oxford, UK: Oxford University Press.

De Wit, B., & Meyer, R. (n.d.). Strategy process, content, process an international perspective. Andover, UK. South-Western Cengange Learning.

Forrester Research. (2006). Retailers get into banking, so what for banks? Retrieved May 25, 2011 from http://www.forrester.com/rb/Research/ retailers_get_into_banking%3B_so_what_for/q/ id/39805/t/2?src=40959pdf

Grossman, S. (2010). Unsettled account. Princeton, NJ: Princeton University Press.

Gurau, C. (2005). ICT strategies for development: Implementing multichannel banking in Romania. Information Technology for Development, 11(4), 343-362. doi:10.1002/itdj.20024

Hax, A., & Wilde, D. (2001). The delta project. New York: Palgrave Macmillan. doi:10.1057/9780230288089

Huang, J., Huang, W., Zhao, C., & Huang, H. (2004). An e-readiness assessment framework and two field studies. Communications of the Association for Information Systems, 14(19), 364-386.

Johnson, M. (2010). Seizing the white space: Business model innovation for growth and renewal. Boston: Harvard Business Press.

Johnson, M., Christensen, C., & Kagermann, H. (2008). Reinventing your business model. Boston: Harvard Business Press.

Li, F. (2001). The internet and the deconstruction of the integrated banking model. British Journal of Management, 12, 307-322. doi:10.1111/1467- 8551.00212

Lin, B.-W. (2007). Information technology capability and value creation: Evidence from the US banking industry. Technology in Society, 29, 93-106. doi:10.1016/j.techsoc.2006.10.003

Mahadevan, B. (2000). Business models for internet based e-commerce - An anatomy. California Management Review, 42(4), 55-69. doi:10.2307/41166053

Marine, M. (2013). Banks and information technology: Marketability vs. relationships. Electronic Commerce Research, 13, 71-101. doi:10.1007/ s10660-013-9107-2

Nellis, J., McCaffery, K., & Hutchinson, R. (2000). Strategic challenges for the European banking industry in the new millennium. International Journal of Bank Marketing, 18(2), 53-63. doi:10.1108/02652320010322967

Osterwalder, A., & Pigneur, Y. (2010). Business model generation. West Sussex, UK: Wiley.

Shah, M. H., & Siddiqui, F. A. (2006). Organisational critical success factors in adoption of e-banking at the Woolwich bank. International Journal of Information Management, 26, 442-456. doi:10.1016/j.ijinfomgt.2006.08.003

Smith, A. (2006). Aspects of strategic forces affecting online banking. Services Marketing Quarterly, 28(2), 79-97. doi:10.1300/J396v28n02_05

Stamoulis, D., Panagiotis, K., & Drakoulis, M. (2002). An approach and model for assessing the business value of e-banking distribution channels: Evaluation as communication. International Journal ofInformation Management, 22, 247-261. doi:10.1016/S0268-4012(02)00011-7

Tan, M., & Teo, T. (2000). Factors influencing the adoption of electronic banking. Journal of the Association for Information Systems, 1(5), 1-42.

Teece, D. (2010). Business models, business strategy and innovation. Long Range Planning, 43(2-3), 143-462. doi:10.1016/j.lrp.2009.07.003

Yap, K., Wong, D., Loh, C., & Bak, R. (2010). Offline and online banking - Where to draw the line when building trust in e-banking? International Journal of Bank Marketing, 28(1), 27-46. doi:10.1108/02652321011013571

Zott, C., Amit, R., & Massa, L. (2011). The business model: Recent developments and future research. Journal of Management, 20(10), 1-25.

KEY TERMS AND DEFINITIONS

Business Model: A concept that describes the general approach an organization has adopted to go about and organise its business in order to create value for its customers and generate revenue.

Business Model Canvas: A conceptual framework that operationalises the business model concept by breaking it down into nine distinct areas, each of which deals with specific aspects of an organization’s internal and external resources and activities.

Business Model Innovation: A radical or incremental change in the operation, organization, or product offering of an organization that affects the value proposition to its customers and business partners.

Delta Model: A conceptual framework in the field of strategy that links the business level strategy of an organization to a set of initiatives and processes used to realize its strategic positioning and proposes metrics to monitor the alignment of strategy with its implementation.

ENDNOTES

www.egg.com founded 1998 out of Prudential’s banking arm and survived the dot.com burst (unlike other efforts like First-e) due to its flexible low cost infrastructure and low cost credit card offering. Today owned by Citibank, it still remains a pure e-bank which means it is only possible to operate an Egg account over the internet, or via their call center.

In the case of the banking industry, this is exemplified by the following statement from a Datamonitor report published in April 20 2001 “The mass desertion from traditional banks to online players that was so hyped just a year ago has failed to materialize. Instead, the traditional banks have realized that online is the way to go - as part of a multi-channel distribution strategy,” available at http://www.datamonitor.com/store/ News/barclays_a_big_bank_and_a_big_ ebank?productid=FA7222E3-9BB9-48E7- 8C54-88817B822F53 (last accessed March 2013).

By transaction banking, Marine refers to activities with a one-time focus on a single customer which are scalable and can easily be replicated for transactions with many customers. Relationship banking, on the other hand, is defined “as bank activities that rely on often proprietary, customer-specific information, obtained through multiple in-

teractions with the same customer over time and/or across products. Such information is predominantly soft in nature (i.e., difficult to quantify) and therefore proprietary to the bank, reusable, and costly to produce” (Marine, 2013, pp. 73).

Forrester July 10 2006 “Retailers Get Into Banking; So What for banks?” Transaction platforms: systems and processes used for payments, billing, customer service, credit and debit card issuing and management as well as other streamlined and commoditized assets http://www.ecb.int/paym/pol/sepa/html/ index.en.html

The Second Banking Directive effective from January 1st 1993, established the mechanisms of home-country control, single licence and mutual recognition in order to create a European financial area with the free provision of financial services.

The term Bancassurance denotes the provision of banking and insurance products and services through the same distribution channel to the same customer segment.

This work was previously published in Approaches and Processes for Managing the Economics of Information Systems, edited by Theodosios Tsiakis, Theodoros Kargidis, and Panagiotis Katsaros, pages 363-378, copyright 2014 by Business Science Reference (an imprint of IGI Global).