Chapter 72 XBRL: A New Global Paradigm for Business Financial Reporting

Chunhui Liu

University of Winnipeg, Canada

ABSTRACT

Ranked as one of top ten technologies for accounting and auditing professionals, extensible Business Reporting Language (XBRL) is a freely available, open, and global standard language for exchanging business financial information digitally.

XBRL holds the greatest promise for building a global standard that is pledged to enhance the accuracy, reliability, efficiency, accessibility and availability of electronic communication of business financial data. This paper sets out to provide a review of literature to lend insights into our understanding of XBRL adoption, implementation, and value realization assessment. A comprehensive review uncovers four sub-themes of research in XBRL adoption: perceived benefits of XBRL adoption; organizational readiness; external pressure; and XBRL adoption. Research challenges for future research are highlighted.INTRODUCTION

The persistent rise of high profile corporate accounting scandals in recent years highlights the urgency for more effective corporate financial reporting that is informative, credible, and readily accessible to regulators, investors, and other stakeholders (Lester, 2007). As an evolving information technology for web-based financial reporting (Doolin & Troshani, 2007), eXtensible Business Reporting Language (XBRL) holds the greatest promise for building a global standard

that is pledged to enhance the accuracy, reliability, efficiency, accessibility and availability of electronic communication of business financial data (Baldwin et al, 2006; Lester, 2007; Stantial, 2007; Vasarhelyi et al., 2012; Willis, 2005; Yoon et al, 2011). Initiated in 1998 by the AICPA, and now administered by a global consortium, XBRL streamlines the preparation of financial statements both internally and externally (Taylor & Dzuranin, 2010).

XBRL is considered an important enabler of corporate transparency (Apostolou & Nanopoulos, 2009; Bonson et al., 2010; Debreceny et al., 2011; Ionescu, 2011; Roohani et al., 2009) and an example of breakthrough value adding accounting information technology (Alles et al., 2008).DOI: 10.4018∕978-1-4666-6268-1.ch072

.

XBRL is an information technology that provides an identifying tag for business information such as total sales to create an unambiguous way to identify and compare information of one company to another (Hoitash et al, 2006). Selfdescribing markups or tags provide notations to contents of a document and thus allow the search and extraction of desired information by purpose-built computer programs without downloading an entire document (Jones & Willis, 2003; Vasarhelyi et al., 2012). XBRL tags are defined and organized using a systematic classification scheme called a taxonomy that defines financial reporting concepts and their relationships as per specific legislation or standards (Deshmukh, 2004; Lester, 2007; Strader, 2007). Files with tagged financial information are called XBRL instance documents (Janvrin & Mascha, 2010). XBRL tags can be applied to financial statements after they are generated or implemented directly into an accounting information system (Vasarhelyi et al., 2012). By separating content from format, XBRL benefits all members of the financial information supply chain by making information exchangeable between different applications and systems and easy to extract, search, and reuse by users (Jensen & Xiao, 2001). The computer readable and searchable XBRL-tagged document will lead to a fundamental revolution in financial reporting as users like investors and analysts can download not only the traditional financial report but also consistent representations of the data that were combined and aggregated to create that report (Hannon, 2002; Plumlee & Plumlee, 2008). It’s also perceived as a useful IT productivity tool by auditors (Chironna & Zwikker, 2011; Janvrin et al., 2008).

The American Institute of Certified Public Accountants has ranked XBRL as one of top ten technologies for accounting and auditing professionals (Peng & Chang, 2010).XBRL facilitates the automated production and consumption of large volumes of business performance information by combining the immediacy and reach of the Web with the ability of information consumers to incorporate corporate information directly into their data warehouses and decision models (Debreceny et al. 2010). Because of such expected benefits (Bovee et al., 2005), XBRL is quickly becoming the reporting standard for financial information worldwide (Taylor & Dzuranin, 2010). Many countries such as Australia, Chile, China, Denmark, Germany, India, Israel, Italy, Japan, Luxemburg, Singapore, Spain, South Korea, the United Kingdom, and the United States have started mandating XBRL adoption (O’Kelly 2010; Srivastava & Kogan 2010; Yoon et al. 2011). Regulators in manyjurisdictions such as Canadian Securities Administrators are still assessing the costs and benefits from XBRL adoption.

Given the rising interest in XBRL assessment and implementation among academics, financial statement preparers and regulators (Janvrin & Mascha, 2010), this article reviews extent research into XBRL technology to reveal key theories, key findings and key challenges. This paper is organized as follows. The next section presents a brief overview of our research methodology in conducting this review. It’s followed by a review of literature that includes XBRL as a central variable in the study. The paper concludes with a summary of findings and highlights unresolved challenges for future research.

RESEARCH METHODOLOGY

A search of the key word “XBRL” is conducted with ABI/Inform, Business Source Premier, and Science Direct (Elsevier) databases. The bibliographies of key articles are further checked to ensure that other articles are not overlooked. Finally, every issue of leading journals in information systems and accounting information systems is searched since 1998 for appropriate literature.

The search is limited by choosing articles from peer-reviewed academic journals. Articles that merely mention XBRL as a recent technology are removed from the sample.LITERATURE REVIEW

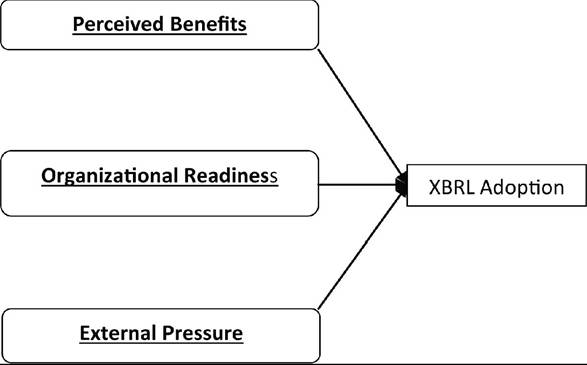

137 articles from 57 peer-reviewed academic journals have been reviewed. Three major themes are observed: XBRL adoption, implementation, and value realization assessment. XBRL adoption research theme is broken into four sub-themes as per the Iacovou et al. (1995) model: perceived benefits; organizational readiness; external pressure; and XBRL adoption. The literature review is provided next. Then, challenges for future research will be discussed.

Major Theme 1: XBRL Adoption

The adoption of innovations such as XBRL often results from a mixture of pull and push influences (Warren, 2004). Many theories have tried to identify drivers in the decision to adopt a new technology. Theory of reasoned action (TRA) (Fishbein & Ajzen, 1975) asserts that individual behavior such as technology adoption is driven by intentions, which are a function of an individual’s attitude. Based on TRA, technology acceptance model (TAM), an information systems theory, proposes that users’ attitude toward adopting a new technology is influenced by the perceived usefulness and perceived ease-of-use of the technology (Davis et al., 1989). Theory of planned behavior (TPB) (Ajzen, 1991) extends TRA and posits that the immediate antecedent of a given behavior is the intent to perform it and that the intent can be predicted by three conceptually independent determinants of intention: attitude, subjective norms, and perceived behavioral control. Decomposed TPB incorporates perceived usefulness and ease of use from TAM as mediating variables for the attitude construct in TPB (Taylor & Todd, 1995). In addition to these models at the individual level, models have been developed for understanding IT adoption at the firm level. For example, the technology, organization, and environment (TOE) framework (Tornatzky & Fleischer, 1990) identifies technological, organizational, and environment contexts as influential in a firm’s adoption of an IT.

Iacovou et al. (1995) combine technological and organizational context factors to reflect organizational readiness and add perceived benefits as an additional critical factor (Oliveira & Martins, 2011). As per the Iacovou et al. (1995) model, XBRL adoption research theme is broken into four sub-themes: perceived benefits; organizational readiness; external pressure; and XBRL adoption as depicted in Figure 1.Sub-Theme 1: Perceived Benefits

Common to TRA, TAM, TPB, and the Iacovou et al. (1995) model is the belief that perceived benefit or usefulness of a technology contributes to attitude formation toward the adoption of a technology. In face of the growing interest in online business reporting and XBRL, research tends to have a means/ends focus which tells us what the technology can do and the potential benefits that will be derived (Williams et al., 2006).

XBRL is expected to improve digital financial information quality and prevent the financial chicanery present in accounting scandals (Seetharaman et al., 2005). Researchers (Apostolou & Nanopoulos, 2009; Bonson et al. (2010); Debreceny et al., 2011; Florescu & Tudor, 2009; Graziano, 2002; Ionescu, 2011; Roohani et al., 2009) believe that XBRL will provide financial executives with the critical ability to provide the transparency required by recent governance regulation. Bizarro and Garcia (2010) think that XBRL can improve internal control as the machine-readable XBRL eliminates manual intervention such as rekeying of data or manipulation via a spread sheet with associated labor costs and possibility for error.

Figure 1. XBRL adoption research themes as per the Iacovou et al. (1995) model

Uniquely identifying each line item on the financial statement and tagging the method of accounting used, XBRL standardizes current financial reporting data to resolve comparability issues resulted from different naming conventions, accounting policies, or account aggregation levels (Vasarhelyi et al., 2012).

XBRL is expected to benefit the preparer of financial information. XBRL is expected to facilitate real-time reporting, continuous auditing, and rapid and versatile preparation of business information to facilitate reliable and accurate data reporting (Cunningham, 2005; Dye, 2010; Estebanez et al., 2010; Gray & Miller, 2009; McGuire et al., 2006; Pitre, 2007; Rezaee et al., 2001; Rezaee & Turner, 2005; Roohani, 2003; Toshani, 2007; Vasarhelyi et al., 2010; Willis, 2005). Internal incentives to voluntarily file financial statements in the XBRL format include reduced costs of compiling and reporting financial information due to streamline reporting process, reduced disparities between firms in disclosure level and content to gain easier access to capital markets, reduced cost of capital, improved corporate governance, and reduced cost for tax filing (Gray et al., 1995; Hannon, 2006; Hodgson et al., 2011; Malhotra & Garritt 2004; Matherne & Coffin, 2001; Premuros & Bhat- tacharya, 2008). Thomson and Iyer (2011) believe in XBRL’s ability to improve risk management and sustainability reporting. In addition, XBRL can be a significant tool in the move towards the adoption of International Financial Reporting Standards (Alley & James, 2005; Liu, 2011; Liu et al., 2011b). Result demonstrability is another perceived benefit of XBRL adoption. Signaling good or improved firm performance is often a major motivation for firm voluntary disclosures (Dye, 1985; Lang & Lundholm, 1993; Miller, 2002; Verrecchia, 2001). Researchers (Callaghan & Nehmer, 2009; Hodge et al., 2004; Premuros & Bhattacharya, 2008) find significant relation between corporate governance level and firms’ decision to voluntarily adopt XBRL for signaling purpose. Early adopters of XBRL filing expect to be rewarded for their efforts in increased transparency through an increased share price and market capitalization by differentiating themselves from late movers (Sledgianowski et al., 2010) and improving credit agency rating evaluations (Premuros & Bhattacharya, 2008).

Besides probable benefits to firms filing with XBRL technology, XBRL is also expected to benefit information users such as investors, auditors, analysts, and regulators. Bartlett (2010) states that XBRL has the potential to increase the speed and usability of financial information by minimizing transcription costs and logistic challenges related to real-time evaluation of firms’ periodic filings. Wallace (2001) thinks that by reducing the time spent on data gathering which can now be automated with data in XBRL format, lenders can price and monitor their risks more effectively. As XBRL tags make searching through financial statements easier than ever (B aldwin & Trinkle, 2011; Hunton & McEwen, 1997; Rezaee et al., 2001; Teo et al., 2003), Quinlan (2010) says that XBRL will make it easier for analysts to identify the best-performing stocks, for executives to monitor competitors, and for regulators to identify potential problems in a company’s financial data. Weber (2003) believes that XBRL reduces the costs associated with getting and analyzing information from businesses by eliminating incompatible reporting formats. Ball (2007) and Kull et al. (2007) indicate that XBRL can also be relevant to federal financial management in reconciling intra-governmental activities and balances between federal agencies, improving consolidated financial statements, and improving business-to-government reporting. Moreover, advanced technology like XBRL preserves the ability of the taxing jurisdictions to achieve economic objectives and to address the unique circumstances of the state and local government through the use of a flexible sales tax system (Wells, 2009). Therefore, proponents believe that XBRL benefits all members of the financial information supply chain (Jensen & Xiao, 2001). Pinsker and Wheeler (2009)'s survey of 61 MBA students as proxies for nonprofessional investors reveals a generally positive perceptions of net benefits from using XBRL.

Sub-Theme 2: Organizational Readiness

Organizational readiness measures the level of resources necessary for realizing the perceived benefits of a technology (Iacovou et al., 1995). Organizational readiness or capability behaves both as a source of competitive advantage and as a constraint of changes (Liu et al., 2008). Organizational-capability theorists and resource- based-view theorists believe that innovations are adopted when they help the organization to utilize its unique capabilities and resources to realize value (Liu et al., 2008).

Financial resources are important for organizational readiness. The U.S. SEC estimates that the direct costs to a company submitting its first interactive data financial statements with XBRL with block-text footnotes and schedules could average $40,510 with an upper bound of $82,220 while the costs for subsequent block-text filings could average $13,450 with an upper bound of $21,340 (Sledgianowski et al., 2010). The level of cost and resources necessary to prepare XBRL filings vary significantly, from several thousand dollars at smaller companies to $500,000 at largest filers (Malonza, 2011).

In addition to budget constraint, Teo et al. (2006) reveal that unresolved technical issues and lack of IT expertise can inhibit a firm’s readiness for an IT. High degree of change and difficulties associated with XBRL generate uncertainty and risk (Doolin & Troshani 2010; Li & Pinsker 2005). Recent studies of early XBRL adoption reveal that XBRL, as an unproven technology, has yet to be fine-tuned (Liu & Yao, 2012). XBRL specification is being developed by a global non-profit consortium and still going through changes which necessitate costly redevelopments and disrupt normal reporting process (Doolin & Troshani, 2007; Nicolaou et al., 2003). Locke and Lowe (2007) point out that the governance of the XBRL consortium such as the requirement for paid membership and a focus on transacting business at physical conferences and meetings may create a barrier to participation for XBRL to fully benefit from the open source model. Researchers have contributed to uncovering design issues in XBRL specifications. The empirical study by Cong (2008) shows that a company’s inherent characteristics such as industry, sales and inventory position play significant roles in the selection of financial statement formats and henceforth certain degree of flexibility should be allowed for the choice of financial statement formats in the XBRL design. Such flexibility decreases comparability of documents for information processing and evaluation and increases search cost (Boritz & No 2008; Debreceny et al. 2005). In addition, the XBRL community is trying to overcome information integration barrier resulted from XBRL data taxonomies presented in a format that is not readily transferable to or integral with standard data warehousing schemata through XBRL for General Ledger (Cohen, 2009; Haseqawa et al., 2004; Spies, 2010). Because raw XBRL data are not intended for human consumption, the ease of use associated with XBRL must be derived from XBRL-enabled analysis and parsing software (Vasarhelyi et al., 2012). Many XBRL software packages are difficult and time-consuming to use and demand high level of XBRL and accounting knowledge (Janvrin & No, 2012). Easy-to-use applications must be developed for mainstream users to benefit from XBRL (Vasarhelyi et al., 2012).

Besides unresolved technical issues, lack of expertise can inhibit a firm’s readiness for XBRL adoption. Surveys of accountants, auditors, and financial executives reveal a significant lack of XBRL knowledge (Abdullah et al. 2008; Aguilar, 2008; Bizarro & Garcia, 2010; Bonson 2001; Cuneo, 2002; Filipek, 2007; Hannon, 2004; Pin- sker, 2003; Said, 2011). Debreceny et al. (2011) analyze extensions made in a subset of XBRL filings made to the SEC between April 2009 and June 2010 to find forty percent of extensions to be unnecessary due to the availability of semantically equivalent elements in U.S. Generally Accepted Accounting Principles (GAAP) taxonomy. They also find twenty one percent of extensions to be aggregated or disaggregated existing elements and thirty percent of extensions for new concepts to be variants of existing elements. A better understanding of XBRL taxonomy could have reduced the need for such unnecessary extensions and improved the comparability of reported information tremendously. Lack of XBRL knowledge/expertise limits self-efficacy and perceived behavioral control among accountants and hinders many organizations from considering XBRL adoption (Alles & Gray, 2012).

XBRL is among the least frequently covered topics in accounting programs’ curricula (Badua, 2008; Rezaee et al., 2006). In response to this challenge, cases, exercises, and illustrations have been developed to train students and practitioners on XBRL (Capozzoli & Farewell, 2010; Debreceny & Farewell, 2010a, 2010b; Naumann, 2004; Peng & Chang, 2010; Phillips et al., 2008; Taylor & Dzuranin, 2010; Tribunella & Tribunella, 2010; White Jr., 2010b). Bartley et al. (2011) reveal that the use of a voluntary filing program (VFP) such as the U.S. VFP offers an effective learning experience to identify and solve unanticipated issues because a reduction in errors in XBRL documents over time is identified in the U.S. VFP. Therefore, more XBRL training and practice through programs such as VFP may be necessary to improve knowledge readiness among firms.

Both unresolved technical issues and lack of expertise can inhibit a firm’s readiness because they increase the risk of errors in creating XBRL documents (Debreceny et al., 2005; Bartley et al., 2010). Bovee et al. (2002) reveal significant variations of quality across financial statements and industries among firms using the year 2000 version ofXBRL taxonomy. Boritz and No (2008) find two-thirds of the XBRL instance documents in the SEC’s Voluntary Filing Program to contain inconsistencies and errors. Boritz and No (2009) find several problem areas such as redundant elements, inconsistent labels, missing totals, and misspellings in XBRL-rendered documents. Debreceny et al. (2010) examine SEC XBRL filings up to 1 September 2009 to uncover an average of 1.8 errors per filing in a U.S. XBRL

filing sample, which has median error of $9.1 million per filing with the maximum exceeding $7 billion. Bartley et al. (2011) examine errors in the XBRL Form 10-K documents in the U.S. Voluntary Filing Program (VFP) for fiscal 2006 and 2008 to find a reduction in errors in XBRL documents over time but a persistence of errors in the third year of VFP.

Despite evidence of errors in XBRL implementation, no requirement has been set up for independent assurance of the XBRL version of financial statements in any regulatory filings around the world (Boritz & No, 2009; Gray & Miller, 2009; Plumlee & Plumlee, 2008; White Jr., 2010a). Attestation on the financial statements does not currently apply to the process of creating XBRL documents, so it is unclear what criteria would be used in an XBRL environment by auditors or others as they provide assurance (Plumlee & Plumlee, 2008). Current XBRL guidelines require only a match of the XBRL-based documents to the paper filing and may not be effective in the paradigm shift from a paper-centric to a data-centric focus resulted from XBRL adoption (Plumlee & Plumlee, 2008). Where legal protection of outside investors is weak, the uncertainty and errors associated with XBRL adoption can be especially salient without requirement for independent assurance (Li & Pinsker, 2005). XBRL statements must be made less error-prone before information preparers and organizations can have stronger readiness for XBRL adoption (Vasarhelyi et al., 2012).

Sub-Theme 3: External Pressure

External pressure refers to influences from the organizational environment (Iacovou et al., 1995). Institutional theory posits that organizations are subject to external influences such as institutional pressures or promotions that cause them to be similar to others in their environment to gain legitimacy, which allows them to secure resources and support for survival (Liu et al., 2008). Institutional pressures may arise from three major sources: coercive (pressures exerted on organizations by other organizations upon which they are dependent for scarce and important resources), mimetic (the pressures to imitate similar other organizations that are successful), and normative pressures (pressures from professionalization) (Liu et al., 2008).

Novel technologies are more likely to be adopted when they are adopted by other organizations (Haveman, 1993). Mimetic pressure is found to play a role in voluntary adoption of XBRL as firms voluntarily submit information in XBRL to acquire a company image as being among pioneers in technology (Ponte et al., 2009). However, the rate of voluntary adoption is sometimes considered to be disappointing when compared with the early predictions made for XBRL’s success (Keeling & Domingo, 2004; Topazio, 2008). For example, in Australia, a critical mass of both XBRL adopters and suppliers of is lacking (Troshani & Rao, 2007). Such a lack of salience among local XBRL stakeholders highlights the importance of normative pressures for XBRL diffusion (Troshani & Doolin, 2007).

Normative pressures and promotions have played an important role in XBRL diffusion to date. Many accountants and researchers have contributed to promoting XBRL. Researhers (Barnabe, 2003; Garthwaite, 2000; Jones & Willis, 2003) introduce XBRL as an eXtensible Markup Language (XML) based language for business reporting which is platform independent and software independent. Lester (2007) promotes XBRL technology as “the business reporting equivalent of bar coding.” Research on perceived benefits of XBRL mentioned in sub-theme 1 demonstrates a collective effort of members of the accounting profession to define and promote XBRL so that legitimacy for occupational autonomy can be strengthened with improved corporate financial reporting that is informative, credible, and readily accessible to regulators, investors, and other stakeholders.

In addition to mimetic and normative pressures, coercive pressures have played a key role in XBRL adoption. Charles Hoffman, the founding father of XBRL, recognizes that a lot of the use of XBRL has been regulator driven (Wenger et al., 2011) due to the clear benefits for regulators and governments in allowing data to be filed once and used and shared in many ways by multiple agencies (Fisher, 2008). Many countries have mandated XBRL as the format for reporting financial information (Taylor & Dzuranin, 2010). Most respondents in the study of Janvrin and No (2010) report the primary motivation for XBRL implementation in the U.S. to be the Securities and Exchange Commission (SEC) mandate. Besides institutional pressures from governmental mandate and regulations, institutional promotions also play a key role in XBRL diffusion. For example, Standard Business Reporting (SBR) program, an Australian Government initiative to reduce the business-to-government reporting burden, has been a key actor providing a specific social setting for the emerging XBRL standard in Australia (Troshani & Lymer, 2010).

Sub-Theme 4: XBRL Adoption

Because of limited organizational readiness due to unresolved technical issues and lack of knowledge/expertise, a lot of the use of XBRL has been regulator driven (Wenger et al., 2011). Due to the perceived benefits of XBRL, many XBRL jurisdictions have indicated an intention to allow voluntary business financial information filing with XBRL while XBRL jurisdictions such as Belgium, Chile, China, Denmark, Germany, India, Israel, Japan, Luxembourg, Singapore, South Korea, Spain, United Kingdom and United States have solidified their adoption intention by mandating XBRL adoption. Bartley et al. (2011), Coffin (2001b), Cohen et al. (2005), Deshmukh (2004), and Rezaee et al. (2001) provide a timeline for XBRL adoption.

Major Theme 2: XBRL Implementation

Janvrin and No (2012) suggest four major phases for XBRL implementation: planning; tagging financial items and creating taxonomy extensions; validating, reviewing and rendering XBRL-related documents; and auditing and issuing XBRL documents. At the planning phase, after knowledge about XBRL and regulatory requirements is obtained, an implementation team is set up to develop an implementation plan. The interviews conducted by Williams et al. (2006) indicate that making sense of, and implementing emerging XBRL metadata standards for business reporting are challenging for organizations. Approximately three months are needed to learn XBRL and the related software among voluntary adopters surveyed in a recent study (Choi et al., 2008). Proper XBRL training and learning are critical for proper XBRL implementation and compliance to XBRL taxonomies (Debreceny et al., 2005; Williams et al., 2006). Support from top management is also critical as it has been found to be the most crucial factor in information technology implementation (Wang & Chen, 2006). Interviews with accountants responsible for XBRL implementation in U.S. reveal that top management commitment is necessary to align XBRL with the existing financial reporting process, to allocate appropriate resources, to align incentives, and to monitor progress (Janvrin & No, 2012; Sharma & Yetton, 2003). At the second phase, the firm chooses the appropriate standard taxonomy based on XBRL knowledge, maps financial items to tags in the taxonomy or creates a new tag by extending the taxonomy, and generates an instance document. At the third phase, validation tests and other internal control mechanisms are conducted to ensure the compliance of XBRL documents to XBRL specifications and regulatory requirements. In an ideal situation, the firm requests its auditor to provide assurance on XBRL documents at the last phase.

Unfortunately, independent audit assurance for XBRL documents is not yet required.

Gianluca Garbellotto (2009), current chair of XBRL global ledger working group, suggests that organizations can consider the following three implementation options for tagging items: a bolt-on option by tagging financial statements at the end of the reporting process to convert the statements to XBRL format; a built-in option by integrating XBRL mapping capability within accounting information systems across the firm’s value chain as part of the reporting process with the help of a conversion software; or an embedded option by standardizing the internal reporting process by embedding it in ERP applications and ledgers. A survey of voluntary adopters of XBRL in U.S. reveals that some early adopters purchase XBRL financial statement conversion software while others outsource the XBRL project with their vendors performing the conversion (Choi et al, 2008). Creating XBRL documents through either XBRL financial statement conversion software or outsourcing at the end of the accounting cycle does not utilize the full potential of XBRL within a company (Wenger et al., 2011). Such implementation methods are expected to evolve so that XBRL tags are incorporated into accounting software and ERP systems to become part of the process of creating financial reports in the beginning of the accounting cycle (Plumlee & Plumlee, 2008). A recent survey reveals that many companies that previously outsourced their XBRL conversion have begun to bring the process in-house by integrating XBRL into their normal reporting processes (Howell, 2012; Sin- nett, 2011). Major software vendors have started to embed XBRL into ERP applications (Mascha et al., 2009). Effort is also made to use XBRL to supplement internal control procedures (Argyrou & Andreev, 2011).

In addition, Chang and Jarvenpaa (2005) highlight the importance ofbroad collaborations across groups of stakeholders in the financial reporting supply chain in the development and implementation of XBRL. Fahy et al (2009)'s case study of an XBRL-enabled inter-organizational system concludes that the co-operative approach to inter- organizational systems (IOS) is likely to be more suited to the implementation of XBRL-enabled systems for financial information supply chains than the “hub and spoke” model characteristic of IOS in other industries (Montazemi & Irani, 2009).

Global implementation of XBRL is also affected by national cultural values. Accounting is contingent on national culture (Alexander, 2011; Ionascu et al., 2011). Information is interpreted through cultural lenses (Bhagat et al., 2002). Research (Downing et al., 2003; Katz & Townsend, 2000; Sia et al., 2011) demonstrates that cultural differences impact firm operations and IT use. Liu et al. (2011b) illustrate that national cultural dimensions matter in XBRL implementation. Take Hof- stede’s (1980, 1983, & 2001) cultural dimensions for instance. Hofstede’s cultural dimensions are one of the most widely studied cultural frameworks (Lim, Leung, Sia, & Lee, 2004). This framework depicts culture along the dimensions of power distance (the extent to which a culture accepts unequal power distribution), uncertainty avoidance (the extent to which people feel threatened by uncertain situations), individualism-collectivism (the extent of ties people hold beyond those of the nuclear family and the degree to which a culture supports individual or collective achievement), masculinity-femininity (the extent to which people are tough and concerned about material success), and long-or short-term-orientation (the extent of orientation toward future vs. past and present). Potential influences of such national cultural value dimensions on successful implementation of XBRL are provided in Table 1.

Major Theme 3: XBRL Value Realization Assessment

Coffin (2001a) believes that XBRL implementation can ultimately impact 90% of what accountants do. Brown and Willis (2003) argue that XBRL

Table 1. Examples of national cultural dimensions and their potential influences

| Cultural Dimensions | XBRL Key Success Factors | Potential Influences |

| Power distance | Collaboration (Chang & Jarvenpaa, 2005; Fahy et al., 2009) | Mejias et al. (1996) and Tan et al. (1998) find a positive association between high power distance and group consensus and collaboration. |

| Uncertainty avoidance | Effort to learn XBRL (Williams et al., 2006) | Hwang (2005) reveals that uncertainty avoidance encourages firms to provide training that enhances perceived ease of use.. |

| Individualism | Compliance with XBRL taxonomies (Debreceny et al., 2005) | Milberg et al. (1995) find that countries rated higher in individualism tend to have less government involvement in regulation and thus higher level of resistance to regulatory mandate. |

| Masculinity | Collaboration (Chang & Jarvenpaa, 2005; Fahy et al., 2009) | Quaddus and Tung (2002) show that people with high masculinity tend to generate more conflict than collaboration. |

| Long-term orientation | Effort to learn XBRL (Williams et al., 2006) | Hofstede and Bond (1988) posit that people of long-term time orientation are more comfortable with sacrificing now such as spending time to learn a new technology. |

systems will revolutionize the corporate reporting supply chain. Notwithstanding the anticipated impact of XBRL, its actual value realization is yet to be assessed. A weak link between information technology (IT) and value, an ‘IT productivity paradox’, has been identified in previous IT value realization research (Hitt & Brynjolfsson, 1996; Sircar et al., 2000). Further investigations (Im et al., 2001; Kivijarvi & Saarinen, 1995; Yao et al., 2010) into such a paradox find that investment in information systems such as XBRL may take some time before its value can be fully realized. The need for XBRL value realization assessment has been identified (Richards & Tower, 2004) because economic justification for XBRL disclosure is an important issue to regulators, the investing community, and participating companies (Debreceny et al., 2005).

Positive impact has been identified among preparers of XBRL documents. Pinsker and Li (2008)'s interview reveals that XBRL can lead to a reduction of 30% of bookkeeping staff in some companies and reduce the time needed to generate financial statements tremendously. John Stantial, assistant controller at United Technologies Corp. reports that XBRL usage reduces the cost and time of external reporting processes by more than 20 percent (Willis & Sinnett, 2008).

Positive impact has also been revealed among users of XBRL documents. Fahy et al (2009)’s case study reveals that XBRL-enabled systems can significantly reduce the burden of data discovery and processing for regulated firms, facilitate new forms of value creating activity such as returning benchmarking data to the market, and shape new regulatory policies by facilitating higher levels of process transparency. Hodge et al. (2004) find that XBRL helps nonprofessional financial statement users to acquire and integrate related financial statement and footnote information in making investment decisions. Hunton and McEwen (1997) find that directive information search strategy enabled by XBRL is associated with accurate analysts forecast. Yoon et al. (2011) find a significant negative association between XBRL adoption and information asymmetry in the Korean stock market, implying that XBRL adoption may lead to the reduction of information asymmetry in South Korea. Kim et al. (2012) show that that XBRL disclosure under the SEC mandate increases information efficiency and decreases return volatility.

Nevertheless, contingency theory entails that accounting information systems and technologies are an important part of the fabric of organizational life and need to be evaluated in their wider environmental context (Cheung & Burn, 1994; Otley, 1980). Assessment of value realization of a technology, hence, depends on the fit between technology integration and contingent factors (Nicolaou, 2000). According to Karimi and Konsynski (1991), differences in business environments, availability of resources, technological and regulatory environments must be taken into consideration as soon as a technology crosses national boundaries. Though an empirical examination of firms listed in U.S. reveals that the mandatory XBRL adoption has led to a significant improvement to both the quantity and quality of information, as measured by analyst following and forecast accuracy (Liu et al., in press), Liu and Yao (2011) and Liu et al. (2013) disclose that the uncertainty related to XBRL, such as information errors, has decreased analysts’ forecast accuracy and increased cost of capital among Chinese firms in an economy with weak public information on listed firms. Though Yoon et al. (2011) find a significant negative association between XBRL adoption and information asymmetry in the Korean stock market, Blankespoor et al. (2012) find a significant positive relation between XBRL adoption and information asymmetry in the U.S. Such empirical evidence of differences in value realization from XBRL adoption in different nations implies that contextual differences across nations such as cultural differences (Liu et al., 2011a) play an important role as influential contingent factors. Potential influences and challenges from global contextual factors are summarized in Table 2. These factors should be considered when assessing value realization from XBRL across nations.

CONCLUDING COMMENTS

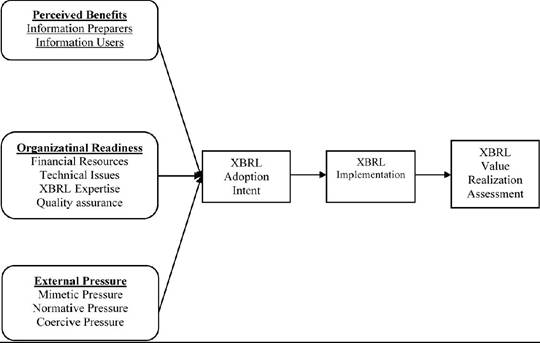

B ased on the number and variety of articles dealing with some aspects of XBRL, there appears to be strong interest in XBRL, the technology believed to bring forth a new paradigm of business financial reporting. Key themes covered in extant literature include perceived benefits; organizational readiness; external pressure; XBRL adoption; XBRL implementation; and value realization assessment as depicted in Figure 2.

Table 2. Potential challenges to value realization from XBRL as a global standard

| Contextual Differences | Potential Challenges |

| Different accounting standards | The proliferation of a multitude of accounting principles and standards across nations necessitates the need for flexibility in creating taxonomy extensions (Bonson et al., 2009; Piechocki et al., 2009). The development and diffusion of global accounting standards as a unique foundation for XBRL taxonomies are essential to achieve global standardization and comparability (Bonson et al., 2009). |

| Different XBRL regulations | Different speed of XBRL mandate across nations (Srivastava & Kogan 2010) undermines its value realization in terms of financial statement comparability of firms from different countries. |

| Different auditing practices | Despite evidence of errors in XBRL documents, no requirement has been set up for independent assurance of the XBRL version of financial statements in any regulatory filings around the world (Gray & Miller, 2009). Different auditing practices across nations leave the reliability and accuracy of XBRL documents of different countries in the dark. A solution is yet to be sought for a unified standard for assurance of XBRL documents. |

| Different financial regulatory environments | Financial regulatory structure affects accounting information quality (Han et al., 2010; Leuz et al., 2003). The uncertainty associated with XBRL is especially salient for firms in economies with weak public information on listed firms (Li & Pinsker, 2005). |

| Different national cultures | Different cultural values can contribute to remarkably different usage of information and communication technology in various nations of the world (Bagchi & Kirs, 2009) because cultural differences among nations may result in different views of the relevance, applicability and value of XBRL (Liu et al. 2011b). |

Much research has contributed to a better understanding of XBRL adoption. Research analyzing the costs and benefits of XBRL filing is important to both potential preparers and users of XBRL (Debreceny et al., 2005). Many believe that benefits will outweigh the cost to convert (Bonson, 2001). Perceived benefits include improved transparency due to streamline reporting process, improved corporate governance and internal control, reduced cost of capital, improved credit agency rating evaluations to adopting firms, improved search and analysis by business information users, and improved business-to-government reporting process. Though the perceived benefits contribute to positive attitude toward XBRL adoption, organizational readiness is relatively weak due to unresolved technical issues, unresolved assurance and security issues, varying speeds of adoption across countries and industries, and lack of internal organizational resources such as XBRL knowledge among accountants and financial experts. Much of XBRL adoption is regulator driven through external pressure.

XBRL implementation can take four major phases with three options for tagging items. Top management support, financial resources, XBRL expertise, and collaborations are among key success factors for XBRL implementation. In addition, national cultural values can play an important role in global implementation of XBRL.

Though XBRL diffusion is at an early stage, some impact has been identified by empirical studies. XBRL-enabled systems are found to significantly reduce the burden of data discovery, processing, and integration for decision making purposes. Significant relation has been identified between XBRL and information asymmetry, analyst forecast accuracy and cost of capital. Some contradictory findings highlight the importance of evaluating XBRL impact in light of contingent factors such as cultural accounting, auditing, and financial regulatory contexts.

As Table 3 indicates, the majority of extant research is based on conceptual and qualitative analysis. Quantitative analyses are conducted less than thirty percent in the reviewed literature. As the availability of archival data increases with broader adoption of XBRL, more quantitative analyses may be conducted to shed light on the impact, implementation, and value realization assessment of XBRL diffusion.

Figure 2. Overview of XBRL research

Table 3. A summary of XBRL research method

| Methodology | Usage |

| Archival Data Analysis | 20% |

| Case Study | 4% |

| Experiment | 3% |

| Interview | 6% |

| Qualitative Analysis | 65% |

| Survey | 2% |

SUGGESTIONS FOR FUTURE RESEARCH

Our conclusion reveals that the investigation of XBRL is still at an early stage. Further research is necessary to unravel the full potential of XBRL. Debreceny and Gray (2001) lay out potential areas of research incorporating: new taxonomies; XBRL front end to database accounting; XBRL-based financial statement assurance; intelligent agents; human/computer interface for XBRL reports; standard development process, adoption incentives, global adoption; and formal ontologies. Though progress has been made in these areas of research, much is still unexplored. For example, development of a suite of new taxonomies incorporating current XBRL standard taxonomies is needed to reduce the need for taxonomy extensions, to improve comparability of tagged information, and to better meet the need for business reporting and tax reporting (Brands, 2011; Monterio, 2011). The development and diffusion of global accounting standards as a unique foundation for XBRL taxonomies are essential to achieve global standardization and comparability (Bonson et al., 2009). Research is yet to overcome information integration barrier to embed XBRL in ERP systems and the management control systems (Grabski et al., 2011). Further research is necessary to set up appropriate assurance policies on XBRL-based reporting (Srivastava & Kogan, 2010; Wright et al., 2008). The future prospects of XBRL-based reporting precipitate an entirely new set of needs for assurance at the account level (Alles et al., 2002) to allow investment analysts to disaggregate financial statements more easily (Elliott, 2002). Since available tools and systems are inadequate to identify errors in the XBRL filing (Malonza, 2011), reliable tools need to be developed to review the XBRL files effectively (Boritz & No, 2005; Bovee et al., 2005). Developing XBRL as a global standard calls for the development of interoperable XBRL taxonomies under various GAAPs and a better understanding of the role environmental factors such as national cultures and financial regulatory environments play in XBRL diffusion. More research is imperative in establishing effective ways to incorporate XBRL in the accounting curriculum and to train accounting professionals and financial experts. Additional research is necessary to reveal contingent factors such as organizational, cultural, or financial regulatory factors influencing value realization from XBRL adoption and to uncover a better picture of real impact of XBRL on information preparers and users.

ACKNOWLEDGMENT

The author is indebted to Editor-in-Chief Choon Ling Sia and two anonymous reviewers for their numerous guidance, enlightening comments, and helpful suggestions.

REFERENCES

Abdullah, A., Khadaroo, I., & Shaikh, J. M. (2008). A “macro” analysis of the use of XBRL. International Journal of Managerial and Financial Accounting, 1(2), 213-223. doi:10.1504/ IJMFA.2008.021243

Aguilar, M. K. (2008, July 1). Survey: Many unprepared for XBRL. Compliance Week. Retrieved from http://www.complianceweek.com

Ajzen, I. (1991). The theory of planned behavior. Organizational Behavior and Human Decision Processes, 50(2), 179-211. doi:10.1016/0749- 5978(91)90020-T

Alexander, D. (2011). Some personal thoughts on financial reporting. International Journal of Accounting and Information Management, 19(2), 198.

Alles, M., & Gray, G. L. (2012). A relative cost framework of demand for external assurance of XBRL filings. Journal of Information Systems, 26(1), 103-126. doi:10.2308/isys-10248

Alles, M., & Piechocki, M. (2010). Will XBRL improve corporate governance? A framework for enhancing governance decision making using interactive data. International Journal of Accounting Information Systems. doi: doi :10.1016/j. accinf.2010.09.008

Alles, M. G., Kogan, A., & Vasarhelyi, M. A. (2002). Feasibility and economics of continuous assurance. Auditing: A Journal of Practice & Theory, 21(1), 125-138.

Alles, M. G., Kogan, A., & Vasarhelyi, M. A. (2008). Exploiting comparative advantage: A paradigm for value added research in accounting information systems. International Journal of Accounting Information Systems, 9(4), 202-215. doi:10.1016/j.accinf.2008.06.001

Alley, C., & James, S. (2005). The use of financial reporting standards-based accounting for the preparation of tax returns. International Tax Journal, 31-48.

Apostolou, A. K., & Nanopoulos, K. A. (2009). Interactive financial reporting using XBRL: An overview of the global markets and Europe. International Journal of Disclosures and Governance, 6(3), 262-272. doi:10.1057/jdg.2009.3

Argyrou, A., & Andreev, A. (2011). A semisupervised tool for clustering accounting databases with applications to internal controls. Expert Systems with Applications, 38, 11176-11181. doi:10.1016/j.eswa.2011.02.163

Badua, F. (2008). Pedagogy and the PC: Trends in the AIS curriculum. Journal of Education for Business, 83(5), 259-264. doi:10.3200/ JOEB.83.5.259-264

Bagchi, K., & Kirs, P. (2009). The impact of Schwartz’s cultural value types on ICT use: A multi-national individual-level analysis. In Proceedings of International Conference on Information Systems, Phoenix, Arizona: 205. The Association for Information Systems.

Baldwin, A. A., Brown, C. E., & Trinkle, B. S. (2006). XBRL: An impacts framework and research challenge. Journal of Emerging Technologies in Accounting, 3(1), 97-116. doi:10.2308/ jeta.2006.3.1.97

Baldwin, A. A., & Trinkle, B. S. (2011). The impact of XBRL: A Delphi investigation. The International Journal of Digital Accounting Research, 11, 1-24. doi:10.4192/1577-8517-v11_1

Ball, C. (2007). Better information better management. The Journal of Government Fianncial Management, 56(2), 16-19.

Barnabe, R. (2003). Seeing the whole elephant: A proposed experiment on measuring the activities of multinational enterprises. Statistical Journal of the United Nations ECE, 20, 173-183.

Bartlett, R. P. (2010). Inefficiencies in the information thicket: A case study of derivative disclosures during the financial crisis. The Journal of Corporation Law, 36(1), 1-57.

Bartley, J., Chen, A. Y. S., & Taylor, E. Z. (2010). Avoiding common errors of XBRL implementation. Journal of Accountancy, 209(2), 46-51.

Bartley, J., Chen, A. Y. S., & Taylor, E. Z. (2011). A comparison of XBRL filings to corporate 10- Ks - evidence from the voluntary filing program. Accounting Horizon, 25(2), 227-245. doi:10.2308/ acch-10028

Bhagat, R. S., Kedia, B. L., Harveston, P., & Triandis, H. C. (2002). Cultural variations in the cross-border transfer of organizational knowledge: An integrative framework. Academy of Management Review, 27(2), 204-221.

Bizarro, P. A., & Garcia, A. (2010). XBRL - Beyond the basics. The CPA Journal, 80(5), 62-71.

Blankespoor, E., Miller, B. P., & White, H. D. (2012). Initial evidence on the market impact of the XBRL mandate. Working paper, University of Chicago.

Bonson, E. (2001). The role of XBRL in Europe. The International Journal of Digital Accounting Research, 1(2), 101-110.

Bonson, E., Cortijo, V., & Escobar, T. (2009). Towards the global adoption of XBRL using International Financial Reporting Standards (IFRS). International Journal of Accounting Information Systems, 10(1), 46-60. doi:10.1016/j. accinf.2008.10.002

Bonson, E., Cortijo, V., Escobar, T., & Flores,

F. (2010). Solvency II and XBRL: New ruls and technologies in insurance supervision. Journal of Financial Regulation and Compliance, 18(2), 144-157. doi:10.1108/13581981011034005

Boritz, J. E., & No, W. G. (2005). Security in XMLbased financial reporting services on the Internet. Journal of Accounting and Public Policy, 24(1), 11-35. doi:10.1016/j.jaccpubpol.2004.12.002

Boritz, J. E., & No, W. G. (2008). The SECs XBRL voluntary filing program on EDGAR: A case for quality assurance. Current Issues in Auditing, 2(2), A36-A50. doi:10.2308/ciia.2008.2.2.A36 Boritz, J. E., & No, W. G. (2009). Assurance on XBRL-related documents: The case of United Technologies Corporation. Journal ofInformation Systems, 23, 49-78. doi:10.2308/jis.2009.23.2.49

Bovee, M., Ettredge, M., Srivastava, R., & Vasar- helyi, M. (2002). Does the year 2000 XBRL taxonomy accommodate current business financial reporting practice? Journal ofInformation Systems, 16(2), 165-182. doi:10.2308/jis.2002.16.2.165

Bovee, M., Kogan, A., Nelson, K., Srivastava, R., & Vasarhelyi, M. (2005). Financial reporting and auditing agent with net knowledge (FRAANK) and Extensible Business Reporting Language (XBRL). Journal of Information Systems, 19(1), 19-41. doi:10.2308/jis.2005.19.1.19

Brands, K. (2011). Peer review: An internal control for the XBRL SEC tagging mandate. Strategic Finance, 93(1), 56-57.

Brown, F., & Willis, M. (2003). XBRL: Revolutionizing the corporate reporting supply chain. Financial Executive, 19(3), 70-71.

Callaghan, J., & Nehmer, R. (2009). Financial and governance characteristics of voluntary XBRL adopters in the United States. International Journal of Disclosure and Governance, 6(4), 321-335. doi:10.1057/jdg.2009.15

Capozzoli, E., & Farewell, S. (2010). SEC XBRL filing requirements: An instructional case on tagging financial statement disclosures. Issues in Accounting Education, 25(3), 489-511. doi:10.2308/ iace.2010.25.3.489

Chang, C., & Jarvenpaa, S. (2005). Pace of information systems standards development and implementation: The case of XBRL. Electronic Markets, 15(4),365-377. doi:10.1080/10196780500303029

Cheung, H. K., & Burn, J. (1994). Distributing global information systems resources in multinational companies. Journal of Global Information Management, 2(3), 14-27.

Chironna, J., & Zwikker, E. (2011). XBRL. Strategic Finance, 92(9), 56-57.

Choi, V., Grant, G. H., & Luzi, A. D. (2008). Insights from the SEC’s XBRL voluntary filing program. The CPA Journal, 78(2), 69-71.

Coffin, Z. (2001a). The advent of real-time accounting. The Practical Accountant, 34(8), 48-49.

Coffin, Z. (2001b). The top 10 effects of XBRL. Strategic Finance, 82(12), 64-67.

Cohen, E. E. (2009). XBRL’s global ledger framework: Exploring the standardized missing link to ERP integration. International Journal of Disclosures and Governance, 6(3), 188-206. doi:10.1057/jdg.2009.5

Cohen, E. E., Schiavina, T., & Olivier, S. (2005). XBRL: The standardized business language for 21st century reporting and governance. International Journal of Disclosure and Governance, 2(4), 368-394. doi: 10.1057∕palgrave.jdg.2040006

Cong, Y. (2008). Relationship between industry characteristics of firms and their financial statement presentation formats: An empirical study in the United States. International Journal of Management, 25(1), 69-76.

Cuneo, E. C. (2002). XBRL: Still a ways away from saving the day; but the standard is seen as an important part of restoring consumer and investor confidence in big business. Information Week, 77(December), 1.

Cunningham, C. S. (2005). XBRL: A multitalented tool. Journal of Accountancy, 199(4), 70-71.

Davis, F. D., Bagozzi, R. P., & Warshaw, P. R. (1989). User acceptance of computer technology: A comparison of two theoretical models. Management Science, 35(8), 982-1003. doi:10.1287/ mnsc.35.8.982

Debrecency, R. S., & Farewell, S. (2010a). Adios! Airways: An assignment on mapping financial statements to the U.S. GAAP XBRL taxonomy. Issues in Accounting Education, 25(3), 465-488. doi:10.2308/iace.2010.25.3.465

Debrecency, R. S., & Farewell, S. (2010b). XBRL in the accounting curriculum. Issues in Accounting Education, 25(3), 379-403. doi:10.2308/ iace.2010.25.3.379

Debrecency, R. S., Farewell, S., Piechocki, M., Felden, C., & Graning, A. (2010). Does it add up? Early evidence on the data quality of XBRL filings to the SEC. Journal of Accounting and Public Policy, 29, 296-306. doi:10.1016/j.jac- cpubpol.2010.04.001

Debreceny, R., Chandra, A., Cheh, J. J., Guithues- Amrhein, D. D., Hannon, N. J., & Hutchison, P. D. et al. (2005). Financial reporting in XBRL on the SECs EDGAR systems: A critique and evaluation. Journal of Information Systems, 19(2), 191. doi:10.2308/jis.2005.19.2.191

Debreceny, R. S., Farewell, S. M., Piechochi, M., Felden, C., Graning, A., & D’eri, A. (2011). Flex or break? Extensions in XBRL. Accounting Horizons, 25(4), 631-657. doi:10.2308/acch-50068

Debreceny, R. S., & Gray, G. L. (2001). The production and use of semantically rich accounting reports on the Internet: XML and XBRL. International Journal of Accounting Information Systems, 2, 47-74. doi:10.1016/S1467-0895(00)00012-9

Deshmukh, A. (2004). XBRL. Communications of the Association for Information Systems, 13, 196-219.

Doolin, B., & Troshani, I. (2007). Organization adoption of XBRL. Electronic Markets, 17(3), 199-209. doi:10.1080/10196780701503195

Downing, C. E., Gallaugher, J., & Segars, A. H. (2003). Information technology choices in dissimilar cultures: Enhancing empowerment. Journal of Global Information Management, 11 (1), 20-39. doi:10.4018/jgim.2003010102

Dye, R. (1985). Disclosure of nonproprietary information. Journal of Accounting Research, 23(1), 123-145. doi:10.2307/2490910

Dye, R. (2010). Disclosure “bunching.” Journal of Accounting Research, 48(3), 489-530. doi:10.1111/j.1475-679X.2010.00375.x

Elliott, R. K. (2002). Twenty-first century assurance. Auditing: A Journal of Practice & Theory, 21(1), 139-146.

Estebanez, R. P., Grande, E. U., & Colomina, C. M. (2010) Information technology implementation: evidence in Spanish SMEs. International Journal of Accounting and information Management, 18(1), 39-57.

Fahy, M., Feller, J., Finnegan, P., & Murphy, C. (2009). Co-operatively re-engineering a financial services information supply chain: A case study. Canadian Journal of Administrative Sciences, 26, 125-135. doi:10.1002/cjas.98

Filipek, R. (2007). XBRL comes of age. Internal Auditor, 64(5), 29-33.

Fishbein, M., & Ajzen, I. (1975). Belief, attitude, intention, and behavior: An introduction to theory and research. Reading, MA: Addison-Wesley.

Fisher, L. (2008). The XBRL engine builds speed. Internal Auditor, 65(4), 51-55.

Florescu, V., & Tudor, C. G. (2009). The optimization of the internal and external reporting in financial accounting: Adopting XBRL international standards. Annuales UniversitatisApulensis Series Oeconomica, 11(1), 126-139.

Garbellotto, G. (2009). How to make your data interactive. Strategic Finance, 90(9), 56.

Garthwaite, C. (2000). The language of risk: Why the future of risk reporting is spelled XBRL. Balance Sheet, 8(4), 18-20. doi:10.1108/ EUM0000000005373

Grabski, S. V., Stewart, A. L., & Schmidt, P. J. (2011). A review of ERP research: A future agenda for accounting information systems. Journal of Information Systems, 25(1), 37-78. doi:10.2308/ jis.2011.25.1.37

Gray, G. L., & Miller, D. W. (2009). XBRL: Solving real world problems. International Journal of Disclosure & Governance, 6(3), 207-223. doi:10.1057/jdg.2009.8

Gray, S. J., Meek, G. K., & Roberst, C. B. (1995). International capital market pressures and voluntary annual report disclosures by U.S. and U.K. multinationals. Journal of International Financial Management & Accounting, 6(1), 43-68. doi:10.1111/j.1467-646X.1995.tb00049.x

Graziano, C. (2002). XBRL. Financial Executive, 18(8), 52-54.

Gunn, J. (2007). XBRL: Opportunities and challenges in enhancing financial reporting and assurance processes. Current Issues in Auditing, 1, A36-A43. doi:10.2308/ciia.2007.1.1.A36

Han, S., Kang, T., Salter, S., & Yoo, Y. K. (2010). A cross-country study on the effects of national culture on earnings management. Journal of International Business Studies, 41, 123-141. doi:10.1057/jibs.2008.78

Hannon, N. (2002). XBRL enters a new phase. Strategic Finance, 83, 61-62.

Hannon, N. (2004). XBRL and Metcalfe’s rule of technological change. Strategic Finance, 85(7), 57-58.

Hannon, N. (2006). Does XBRL cost too much? Strategic Finance, 87(10), 59-60.

Haseqawa, M., Sakata, T., Sambuichi, N., & Hannon, N. (2004). Breathing new life into old systems. Strategic Finance, 85(9), 46-51.

Haveman, H. A. (1993). Follow the leader: Mimetic isomorphism and entry into new markets. Administrative Science Quarterly, 38(4), 593-627. doi:10.2307/2393338

Hitt, L., & Brynjolfsson, E. (1996). Productivity, business profitability, and consumer surplus: three different measures of information technological value. Management Information Systems Quarterly, 20(2), 121-142. doi:10.2307/249475

Hodge, F. D., Kennedy, J. J., & Maines, L. A. (2004). Does search-facilitating technology improve the transparency of financial reporting? Accounting Review, 79(3), 687-703. doi:10.2308/ accr.2004.79.3.687

Hodgson, A., Lhaopadchan, S., & Buakes,

S. (2011). How informative is the Thai corporate governance index? A financial approach. International Journal of Accounting and Information Management, 19(1), 53-79. doi:10.1108/18347641111105935

Hofstede, G., & Bond, M. H. (1988). The Confucius connection: From cultural roots to economic growth. Organizational Dynamics, 16(4), 4-21. doi:10.1016/0090-2616(88)90009-5

Hoitash, R., Kogan, A., & Vasarhelyi, M. A. (2006). Peer-based approach for analytical procedures. Auditing: A Journal of Practice and Theory, 25(2), 53-84.

Howell, J. (2012). What’s XBRL reporting got to do with bar codes? Financial Executive, 28(1), 52-54.

Hunton, J. E., & Mcewen, R. A. (1997). An assessment ofthe relation between analysts’ earnings forecast accuracy, motivational incentives and cognitive information search strategy. Accounting Review, 72, 497-515.

Hwang, Y. (2005). Investigating enterprise systems adoption: uncertainty avoidance, intrinsic motivation, and the technology acceptance model. European Journal of Information Systems, 14, 150-161. doi:10.1057/palgrave.ejis.3000532

Iacovou, C. L., Benbasat, I., & Dexter, A. S. (1995). Electronic data interchange and small organizations: Adoption and impact of technology. Management Information Systems Quarterly, 19(4), 465-485. doi:10.2307/249629

Im, K. S., Dow, K. E., & Grover, V. A. (2001). A reexamination of it investment and the market value of the firm - an event study methodology. Information Systems Research, 12(1), 103-117. doi:10.1287/isre.12.1.103.9718

Ionascu, I., Ionascu, M., Minu, M., & Sacarin, M. (2011). Local accounting culture facing globalization: The case of Romania’s patrimoniality principle. International Journal of Accounting and Information Management, 19(2), 205-206.

Ionescu, L. (2011). The financial crisis as a failure of internal audit. Economics, Management, and

Financial Markets, 6(2), 833-838.

Janvrin, D., Bierstaker, J., & Lowe, D. J. (2008). An examination of audit information technology use and perceived importance. Accounting Horizons, 22(1), 1-21. doi:10.2308/acch.2008.22.1.1

Janvrin, D., & Mascha, M. F. (2010). The process of creating XBRL instance documents: A research framework. Review of Business Information Systems, 14(2), 11-34.

Janvrin, D., & No, W. G. (2010). XBRL implementation: A field investigation. Working paper, Iowa State University and University of Waterloo.

Janvrin, D., & No, W. G. (2012). XBRL implementation: A field investigation to identify research opportunities. Journal of Information Systems, 26(1), 169-197. doi:10.2308/isys-10252

Jensen, R. E., & Xiao, J. Z. (2001). Customized financial reporting, networked databases, and distributed file sharing. Accounting Horizons, 15(3), 209-222. doi:10.2308/acch.2001.15.3.209

Jones, A., & Willis, M. (2003). The challenge of XBRL: Business reporting for the investor. Balance Sheet, 11(3), 29-37. doi:10.1108/09657960310491172

Karimi, J., & Konsynski, B. (1991). Globalization and information management strategies. Journal of MIS, 7(4), 7-26.

Katz, J., & Townsend, J. B. (2000). The role of information technology in the “fit” between culture, business strategy and organizational structure of global firms. Journal of Global Information Management, 8(2), 24-35. doi: 10.4018/ jgim.2000040102

Keeling, D., & Domingo, L. (2004, October 13). Debating XBRL. Accountancy Age. Retrieved from http://www.accountancyage.com/aa/fea- ture/1768129/xbrl-debate

Kim, J. W., Lim, J. H., & No, W. G. (2012). The effects of first wave mandatory XBRL reporting across the financial information environment. Journal of Information Systems, 26(1), 127-153. doi:10.2308/isys-10260

Kivijarvi, H., & Saarinen, T. (1995). Investment in information systems and the financial performance of the firm. Information & Management, 28(2), 143-163. doi:10.1016/0378-7206(95)94022-5

Kull, J. L., Miller, L. E., St Clair, J. A., & Savage, M. (2007)... The Journal of Government Financial Management, 56(2), 10-14.

Lang, M., & Lundholm, R. (1993). Cross-sectional determinants of analyst ratings of corporate disclosure. Journal of Accounting Research, 31(2), 306-360. doi:10.2307/2491273

Lester, W. F. (2007). XBRL: The new language of corporate financial reporting. Business Communication Quarterly, 70(2), 226-231. doi:10.1 177/10805699070700020603

Leuz, C., Nanda, D., & Wysocki, P. D. (2003). Earnings management and investor protection: An international comparison. Journal of Financial Economics, 69, 505-527. doi:10.1016/S0304- 405X(03)00121-1

Li, S., & Pinsker, R. (2005). Modeling RBRT adoption and its effects on cost of capital. International Journal of Accounting Information Systems, 6, 196-215. doi:10.1016/j.accinf.2005.05.001

Lim, K. H., Leung, K., Sia, C. L., & Lee, M. K. O. (2004). Is ecommerce boundary-less? Effects of individualism-collectivism and uncertainty avoidance on internet shopping. Journal of International Business Studies, 35(6), 545-559. doi:10.1057/palgrave.jibs.8400104

Liu, C. (2011). IFRS and US-GAAP comparability before release no. 33-8879: Some evidence from US-listed Chinese companies. International Journal of Accounting and Information Management, 19(1), 24-33. doi:10.1108/18347641111105917

Liu, C., Sia, C. L., & Wei, K. K. (2008). Adopting organizational virtualization in B2B firms: An empirical study in Singapore. Information & Management, 45, 429-437. doi:10.1016/j. im.2008.06.005

Liu, C., Sia, C. L., Yao, J. L., & Wei, K. K. (2011a). Effects of national culture on a new global paradigm for business financial reporting. Working paper. University of Winnipeg, City University of Hong Kong, Loyola University New Orleans, City University of Hong Kong.

Liu, C., Wang, T. W., & Yao, L. J. (in press). An empirical study of XBRL’s impact on analyst forecast behavior. Journal of Accounting and Public Policy.

Liu, C., & Yao, L. J. (2011). The impact of initial mandatory XBRL adoption on cost of capital. Working paper, University of Winnipeg and Loyola University New Orleans.

Liu, C., Yao, L. J., Hu, N., & Liu, L. (2011b). The impact of IFRS on accounting quality in a regulated market: An empirical study of China. Journal of Accounting, Auditing & Finance, 26(4), 659-676. doi:10.1177/0148558X11409164

Liu, C., Yao, L. J., Sia, C. L., & Wei, K. K. (2013). The impact of early XBRL adoption on analysts’ forecast accuracy: Empirical evidence from China. Electronic Markets.doi:10.1007/ s12525-013-0132-8

Locke, J., & Lowe, A. (2007). XBRL: An (open) source of enlightenment or disillusion? European Accounting Review, 16(3), 585-623. doi:10.1080/09638180701507163

Malhotra, R., & Garritt, F. (2004). Extensible business reporting language: The future of e-commerce driven accounting. International Journal of Business, 9(1), 59-82.

Malonza, L. (2011). XBRL-speak no easy task for filers, revenue recognition standard to be re-exposed. Financial Executive, 27(6), 14-15.

Mascha, M. F., Janvrin, D., Plouff, J., & Kruger,

B. (2009). For small-to-medium-sized firms. Strategic Finance, 90(7), 47-53.

Matherne, L., & Coffin, Z. (2001). XBRL: A technology standard to reduce time, cut costs, and enable better analysis for tax preparers. The Tax Executive, 53, 68-71.

McGuire, B. L., Okesson, S. J., & Watson, L. A. (2006). Second-wave benefits of XBRL. Strategic Finance, 88(6), 43-47.

Mejias, R. J., Shepherd, M. M., Vogel, D. R., & Lazaneo, L. (1996). Consensus and perceived satisfaction and consensus levels: A cross cultural comparison of GSS and Non-GSS outcomes within and between the US and Mexico. Journal of Management Information Systems, 13(3), 137-161.

Milberg, S. J., Burke, S. J., Smith, J. H., & Kallman, E. A. (1995). Rethinking copyright issues and ethics on the Net: Values, personal information privacy, and regulatory approaches. Communications of the ACM, 38(12), 65-73. doi:10.1145/219663.219683

Miller, G. S. (2002). Earnings performance and discretionary disclosure. Journal of Accounting Research, 40, 173-204. doi:10.1111/1475- 679X.00043

Montazemi, A. R., & Irani, Z. (2009). Forward: Special section on information technology in support of financial markets. Canadian Journal of Administrative Sciences, 26, 122-124. doi:10.1002/cjas.101

Monterio, B. J. (2011). XBRL and its impact on corporate tax departments. Strategic Finance, 92(8), 56-61.

Naumann, J. W. (2004). Tap into XBRL’s power the easy way. Journal of Accountancy, 197(5), 32-39.

Nicolaou, A. I. (2000). A contingency model of perceived effectiveness in accounting information systems: Organizational coordination and control effects. International Information of Accounting Information Systems, 1(2), 91-105. doi:10.1016/ S1467-0895(00)00006-3

Nicolaou, A. I., Lord, A. T., & Liu, L. (2003). Demand for data assurances in electronic commerce: An experimental examination of a Web-based data exchange using XML. In S. J. Roohani (Ed.), Trust and data assurances in capital markets: The role of technology solutions (pp. 32-42). Smithfield, RI: Bryant College and PricewaterhouseCoopers. O’Kelly, C. (2010, May 1). XBRL adoption update. Retrieved from http://www.slideshare. net/xbrlplanet/xbrl-world-wide-adoption-survey- april-2010

Oliveira, T., & Martins, M. F. (2011). Literature review of information technology adoption models at firm level. The Electronic Journal Information Systems Evaluation, 14(1), 110-121.

Otley, D. T. (1980). The contingency theory of management accounting: Achievement and prognosis. Accounting, Organizations and Society, 5, 413-428. doi:10.1016/0361-3682(80)90040-9

Peng, J., & Chang, C. J. (2010). Applying XBRL in an accounting information system design using the REA approach: An instructional case. Accounting Perspectives, 9(1), 55-78. doi:10.1111/j.1911- 3838.2010.00004.x

Phillips, M. E., Bahmanziari, T. E., & Colvard, R. G. (2008). Six steps to XBRL. Journal of Accountancy, 205(2), 34-37.

Piechocki, M., Felden, C., Graning, A., & Deb- receny, R. (2009). Design and standardization of XBRL solutions for governance and transparency. International Journal of Disclosure and Governance, 6(3), 224-240. doi:10.1057/jdg.2009.9

Pinsker, R. (2003). XBRL awareness in auditing: A sleeping giant? Managerial Auditing Journal, 18(9), 732-736.doi:10.1108/02686900310500497

Pinsker, R., & Li, S. (2008). Costs and benefits of XBRL adoption: Early evidence. Communications of the ACM, 51(3), 47-50. doi:10.1145/1325555.1325565

Pinsker, R., & Wheeler, P. (2009). Nonprofessional investors’ perceptions of the efficiency and effectiveness of XBRL-enabled financial statement analysis and of firms providing XBRL-formatted information. International Journal of Disclosure and Governance, 6(3), 241-261. doi:10.1057/ jdg.2009.6

Pitre, T. J. (2007). Reporting frequency and sample size: Effects on prediiton, confidence levels, and confidence intervals. Journal of Behavioral Finance, 8(3), 154-160. doi:10.1080/15427560701545622

Plumlee, R. D., & Plumlee, M. A. (2008). Assurance on XBRL for financial reporting. Accounting Horizons, 22(3), 353-368. doi:10.2308/ acch.2008.22.3.353

Ponte, E. B., Gallego, V. C., & Rodriguez, T. E. (2009). A Delphi investigation to explain the voluntary adoption of XBRL. The International Journal of Digital Accounting Research, 9(15), 193-205.

Premuros, R. F., & Bhattacharya, S. (2008). Do early and voluntary filers of financial information in XBRL format signal superior corporate governance and operating performance? International Journal of Accounting Information Systems, 9(1), 1-20. doi:10.1016/j.accinf.2008.01.002

Quaddus, M. A., & Tung, L. L. (2002). Explaining cultural differences in decision conferencing. Communications of the ACM, 45(8), 93-98. doi:10.1145/545151.545157

Quinlan, P. (2010). XBRL: Not just for public companies. The CPA Journal, 80(6), 14.

Rezaee, Z., Elam, R., & Sharbatoghlie, A. (2001). Continuous auditing: The audit of the future. Managerial Auditing Journal, 16(3), 150-158. doi:10.1108/02686900110385605

Rezaee, Z., Lambert, K. R., & Harmon, W. K. (2006). Electronic commerce education: Analysis of existing courses. Accounting Education: An International Journal, 15(1), 73-88. doi:10.1080/06939280600579370

Rezaee, Z., Sharbatoghlie, A., Elam, R., & Mc- mickle, P. L. (2002). Continuous auditing: Building automated auditing capability. Auditing: A Journal of Practice & Theory, 21(1), 147-163. Rezaee, Z., & Turner, J. L. (2005). XBRL-based financial reporting: Challenges and opportunities for government accountants. The Journal of Government Financial Management, 51(2), 16-22.

Richards, J., & Tower, G. (2004). Progress on XBRL from an Australian Perspective. Australian Accounting Review, 14(1), 81-88. doi:10.1111/j.1835-2561.2004.tb00286.x

Roohani, S., Furusho, Y., & Koizumi, M. (2009). XBRL: Improving transparency and monitoring functions of corporate governance. International Journal of Disclosure and Governance, 6(4), 355-369. doi:10.1057/jdg.2009.17

Said, H. A. (2011). Corporate financial reporting complexity: Recommendations for Improvement. Review of Business, 31(2), 69-87.

Seetharaman, A., Subramaniam, R., & Seow, Y. S. (2005). Internet financial reporting: Problems and prospects. Corporate Finance Review, 10(2), 23-34.

Sharma, R., & Yetton, P. (2003). The contingent effects of management support and task interdependence on successful information systems implementation. Management Information Systems Quarterly, 27(4), 533-555.

Sia, C. L., Lim, K. H., Leung, K., Lee, M. K. O., Huang, W. W., & Benbasat, I. (2011). Web strategies to promote Internet shopping: Is cultural- customization needed? Management Information Systems Quarterly, 33(3), 491-512.

Sinnett, W. M. (2011). Bringing XBRL in-house - a trend? Financial Executive, 27(9), 68.

Sircar, S., Turnbow, J. L., & Bordoloi, B. (2000). A framework for assessing the relationship between information technology investments and firm performance. Journal of Management Information Systems, 16(4), 69-97.

Sledgianowski, E., Fondeder, R., & Slavin, N. S. (2010). Implementing XBRL reporting. The CPA Journal, 80(8), 68-72.

Spies, M. (2010). An ontology modeling perspective on business reporting. Information Systems, 35(4), 404-416. doi:10.1016/j.is.2008.12.003

Srivastava, R. P., & Kogan, A. (2010). Assurance on XBRL instance document: A conceptual framework of assertions. International Journal of Accounting Information Systems, 11(3), 261-273. doi:10.1016/j.accinf.2010.07.019

Stantial, J. (2007). ROI on XBRL. Journal of Accountancy, (June): 32-35.

Strader, T. J. (2007). XBRL capabilities and limitations. The CPA Journal, 77(12), 68-71.

Tan, B. C. Y., Wei, K. K., Watson, R. T., Clapper, D. L., & Mclean, E. (1998). Computer-mediated communication and majority influence: Assessing the impact in an individualistic and a collectivist culture. Management Science, 44(9), 1263-1278. doi:10.1287/mnsc.44.9.1263

Taylor, E. Z., & Dzuranin, A. C. (2010). Interactive financial reporting: An introduction to Extensible Business Reporting Language (XBRL). Issues in Accounting Education, 25(1), 71-83. doi:10.2308/ iace.2010.25.1.71

Taylor, S., & Todd, P. (1995). Decomposition and crossover effects in the theory of planned behavior: A study of consumer adoption intentions. International Journal of Research in Marketing, 12(2), 137-155. doi:10.1016/0167-8116(94)00019-K

Teo, H. H., Oh, L. B., Liu, C., & Wei, K. K. (2003). An empirical study of the effects of interactivity on web user attitude. International Journal of HumanComputer Studies, 58, 281-305. doi:10.1016/ S1071-5819(03)00008-9

Teo, T. S. H., Ranganathan, C., & Dhaliwal,

J. (2006). Key dimensions of inhibitors for the deployment of web-based business-to-business electronic commerce. IEEE Transactions on Engineering Management, 53(3), 395-411. doi:10.1109/TEM.2006.878106

Thomson, J. C., & Iyer, U. (2011). XBRL and ERM: Increasing organizational effectiveness. Strategic Finance, 92(11), 64-69.

Topazio, N. (2008). Online reporting. Financial Management, 2008, 34-35.

Tribunella, T., & Tribunella, H. (2010). Using XBRL to analyze financial statements. The CPA Journal, 80(3), 69-72.

Troshani, I., & Doolin, B. (2007). Innovation diffusion: A stakeholder and social network view. European Journal of Innovation Management, 10(2), 176-200. doi:10.1108/14601060710745242

Troshani, I., & Lymer, A. (2010). Translation in XBRL standardization. Information Technology & People, 23(2), 136-164. doi:10.1108/09593841011052147

Troshani, I., & Rao, S. (2007). Drivers and inhibitors to XBRL adoption: A qualitative approach to build a theory in under-researched areas. International Journal of E-Business Research, 3(4), 98-111. doi:10.4018/jebr.2007100106

Vasarhelyi, M. A., Chan, D. Y., & Krahel, J. P. (2012). Consequences of XBRL standardization on financial statement data. Journal ofInformation Systems, 26(1), 155-167. doi:10.2308/isys-10258

Vasarhelyi, M. A., Teeter, R. A., & Krahel, J. P. (2010). Audit education and the real-time economy. Issues in Accounting Education, 25(3), 405-423. doi:10.2308/iace.2010.25.3.405

Verrecchia, R. E. (2001). Essays on disclosure. Journal of Accounting and Economics, 32(1-3), 97-180. doi:10.1016/S0165-4101(01)00025-8 Wallace, A. (2001). The new language of financial reporting. Balance Sheet, 9(2), 29-32. doi:10.1108/09657960110695637

Wang, E. T. G., & Chen, J. H. F. (2006). Effects of internal support and consultant quality on the consulting process and ERP system quality. Decision Support Systems, 42(2), 1029-1041. doi:10.1016/j.dss.2005.08.005

Warren, M. (2004). Farmers online: Drivers and impediments in adoption of Internet in UK agricultural businesses. Journal of Small Business and Enterprise Development, 11(3), 371-381. doi:10.1108/14626000410551627

Weber, R. A. (2003). XML, XBRL, and the future of business and business reporting in trust and data assurances in capital markets: The role of technology solution (S. T. Roohani, Ed.). Smithfield, RI: Bryant College.

Wells, B. L. (2009). The expansion of e-commerce: Addressing sales tax complexity with technology. Journal of State Taxation, 27(6), 33-36.

Wenger, M. R., Elam, R., & Williams, K. (2011). Global ledger: The next step for XBRL. The CPA Journal, 81(9), 64-71.

White, C. E. Jr. (2010a). Discussion of assurance on XBRL instance document: A conceptual framework of assertions - a discussion and extension. International Journal of Accounting Information Systems, 11,274-278. doi:10.1016/j. accinf.2010.07.020

White, C. E. Jr. (2010b). Jim’s sporting goods: The move to XBRL reporting. Issues in Accounting Education, 25(3), 425-463. doi:10.2308/ iace.2010.25.3.425

Williams, S. P., Scifleet, P. A., & Hardy, C. A. (2006). Online business reporting: An information management perspective. International Journal of Information Management, 26(2), 91-101. doi:10.1016/j.ijinfomgt.2005.11.004

Willis, M. (2005). XBRL and data standardization: Transforming the way CPAs work. Journal of Accountancy, 199(3), 80-81.

Willis, M., & Sinnet, W. M. (2008). XBRL not just for external reporting. Financial Executive, 24(4), 44-47.

Wright, A. M., Botosan, C. A., & Colson, R. H. (2008). Response to the progress report of the SEC advisory committee on improvements to financial reporting. Accounting Horizons, 22(4), 471-494. doi:10.2308/acch.2008.22.4.471