CONCLUSION AND IMPLICATIONS

During the last decade the Spanish financial system has undergone a profound transformation since it has been influenced by different factors, such as increased competition, massive technological changes, greater accessibility to services by customers, higher levels of competition, reduced margins, and so on, bringing as a result that most

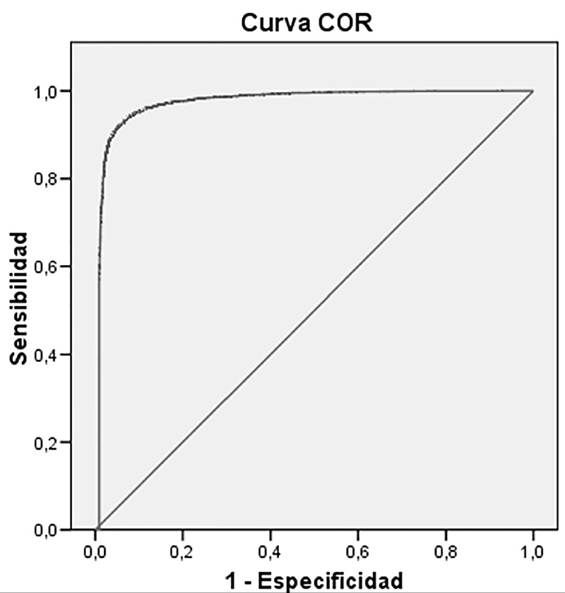

Figure 3.

ROC curve

organizations try to ensure customer loyalty by means of satisfaction and confidence. Our research comes to evidence that, apart from these two classical variables reviewed by scientific literature, it is necessary to analyze socio-demographic and economic factors of the clients themselves to determine the risk of dropping out.

While some authors have defined models of loyalty for a financial institution, the novelty of this research is the approach that has been given to e-Banking customers as well as the level of accessibility to the information that has been analyzed. The model we present has confirmed that there are factors that affect the probability of customer drop-out of a bank. Although it is an ad-hoc model for each bank, the methodology can be generalized to any savings and credit institution with the loyalty of its customers as one of its objectives, provided that, as specialized literature suggests, there exists a binding relationship between dropping out and satisfaction, trust and other socio-demographic and economic variables of customers. According to the results, satisfaction and confidence do not necessarily lead to bank loyalty. However, they are required conditions for this loyalty to happen, having achieved a correct classification rate close to 95%. The proposed model shows the probability for a customer to be disloyal and, therefore, abandon the bank, so that the latter can concentrate their efforts towards loyalty those with higher probabilities.

After a first evaluation of the proposed model and the analyzed variables, we can conclude that the assumptions cannot be rejected, thus accepting the statements of the same.

From the perspective of the financial institution management, customer loyalty will become a fundamental goal (Hypothesis 1 and 2). In particular, the products “credit card” and “debit cards” appear in our model as key variables in the financial relationship with the customer. In order to achieve this relationship, in the last decade the institutions implemented various management systems like CRM, which tries to increase customer loyalty with regular campaigns through the branch network. In addition, these campaigns are reinforced by general communication actions of the network, thus favouring up-selling and crossselling strategies while reducing low membership and improving its products.

Besides, the qualitative aspects in establishing business relationship with the customer, as revealed in Hypotheses 3 and 4 -such as clarity, agility, confidence, customer service and satisfaction-, strengthen the loyalty of customers to the entity, for which the implementation of a CRM strategy will be essential.

Loyalty will be, therefore, the most important aim of financial institutions in the next years because it will get more compensation due to a high linkage that keeps the e-banking customer with the bank. For that, considering the low cost of transfer when facilitating the dropping out in the banking sector, managers must focus their efforts on developing loyalty activities basically for handling customer complaints.

However, the institution should not wait until there are complaints and must take actions in order to increase customer satisfaction and the quality of the service offered, as there is the risk of losing a large number of customers before taking appropriate action.

REFERENCES

Arnould, E. J. (2004). Consumers (2nd ed.). New York: McGraw-Hill Companies, Inc.

Autor.

(2011). El efecto moderador de la experi- encia del usuario en la satisfaction con la banca electronica, trabajo de tesina. Departamento de Comercializacion e Investigacion de Mercados, Universidad de Granada.Barroso, C., & Armario, E. M. (2000). Desarrollo del marketing relacional en Espana. Revista Espanola de Direction y Economia de la Empresa, 9(3), 25-46.

Barrutia, J. M., & Echevarria, C. (2002). Banca de relaciones: De la declaracion de intenciones a la declaracion real. Boletin Economico de ICE, 2737, 27-49.

Bass, F. M. (1974). The theory of stochastic preference and brand switching. JMR, Journal of Marketing Research, 11, 1-20. doi:10.2307/3150989

Bensic, M., Sarlija, N., & Zekic-Susak, M. (2006). Modelling small-business credit scoring by using logistic regression, neural networks and decision trees. Intelligent Systems in Accounting. Financial Management, 13(3), 133-150.

Bettencourt, L. A. (1997). Customer voluntary performance: Customers as partners in service delivery. Journal of Retailing, 73(3), 383-406. doi:10.1016/S0022-4359(97)90024-5

Bhattacherjee, A. (2001). An empirical analysis of the antecedents of electronic commerce service continuance. Decision Support Systems, 32(2), 201-214. doi:10.1016/S0167-9236(01)00111-7

Bigne, E., & Blesa, A. (2003). Market orientation, trust and satisfaction in dyadic relationships: A manufacturer-retailer analysis. International Journal of Retail & Distribution Management, 31(11), 574-590. doi:10.1108/09590550310503302

Brandt, R. (2000). Loyalty really isn’t all that simple, restrictive. Marketing News, 34(17), 7.

Brown, G. H. (1952). Brand loyalty - Fact or fiction? Advertising Age, 23, 53-55.

Cameron, F., Cornish, C., & Nelson, W. (2006). A new methodology for segmenting consumers for financial services. Journal of Financial Services Marketing, 10(3), 260-271. doi:10.1057/palgrave. fsm.4770191

Chen, P., & Hitt, L. (2002). Measuring switching costs and the determinants of customer retention in internet-enabled businesses: A study of the online brokerage industry.

Information Systems Research, 13(3), 255-274. doi:10.1287/isre.13.3.255.78 Christopher, M., Payne, A., & Ballantyne, D. (1994). Marketing relacional: Integrando la cali- dad, el servicio al cliente y el marketing. Madrid: Diaz de Santos.Crie, D. (2003). Consumer’s complaint behavior: Taxonomy, typologyand determinants: Towards a unified ontology. Journal of Database Marketing & Customer Strategy Management, 11(1), 60-66. doi:10.1057/palgrave.dbm.3240206

Day, G. S. (1969). A two dimensional concept of brand loyalty. Journal of Advertising Research, 9, 29-36.

Dick, A. S., & Basu, K. (1994). Customer loyalty: Toward an integrated conceptual framework. Journal of the Academy of Marketing Science, 22(2), 99-113. doi:10.1177/0092070394222001

Diller, H. (2000). Customer loyalty: Fata morgan or realistic goal? Managing relationships with customers. In Relationship marketing: Gaining competitive advantage through customer satisfaction and customer retention. Berlin: Springer. doi:10.1007/978-3-662-09745-8_2

Dwyer, F. R., Schurr, P. H., & Oh, S. (1987). Developing buyer-seller relationships. Journal of Marketing, 51(2), 11-27. doi:10.2307/1251126

Eisenbeis, R. A. (1981). Credit-scoring applications. In Applications of classifications techniques in business, banking & finance. Greenwich, CT: JAI Press.

Fournier, S. (1998). Consumers and their brands: Developing relationship theory in consumer research. The Journal of Consumer Research, 24, 343-373. doi:10.1086/209515

Garcia, N., Sanzo, M. J., & Trespalacios, J. A. (2008). Can a good organizational climate compensate for a lack of top management commitment to new product development? Journal of Business Research, 61, 118-131. doi:10.1016/j. jbusres.2007.06.011

Garland, R. (2002). Estimating customer defection in personal retail banking. International Journal of Bank Marketing, 20(7), 317-324. doi:10.1108/02652320210451214

Gronroos, C. (2004). The relationship marketing process: communication, interaction, dialogue, value.

Journal ofBusiness and Industrial Marketing, 19(2), 99-113. doi:10.1108/08858620410523981Hallowell, R. (1996). The relationships of customer satisfaction, customer loyalty and profitability: An empirical study. International Journal of Service Industry Management, 7(4), 27-42. doi:10.1108/09564239610129931

Hernandez, J. (2010). Analisis y modelizacion del Comportamiento de uso de las herramientas travel 2.0. Universidad de Granada.

Howard, J. A. (1974). The structure of buyer behavior. In Consumer behavior: Theory and application (pp. 9-32). Boston: Allyn & Bacon.

Javalgi, R. G., & Moberg, C. R. (1997). Service loyalty: Implications for serviceproviders. Journal of Services Marketing, 11(3), 165-179. doi:10.1108/08876049710168663

Karjaluoto, H., Mattila, M., & Pento, T. (2002). Factors underlying attitude formation toward online banking in Finland. International Journal of Bank Marketing, 20(6), 261-272. doi:10.1108/02652320210446724

Kim, D. J., Ferrin, D. L., & Rao, H. R. (2009). Trust and satisfaction, the two wheels for successful e-commerce transactions: A longitudinal exploration. Information Systems Research, 20(2), 237-257. doi:10.1287/isre.1080.0188

Lawrence, E. C., & Arshadi, N. (1995). A multinomial logit analysis of problem loan resolution choices in banking. Journal of Money, Credit and Banking, 27(1), 202-216. doi:10.2307/2077859 Malhotra, N. K., Oly-Ndubisi, N., & Agarwal, J. (2008). Comportamiento de quej as publicas frente a privadas y desercion del cliente en Malasia: Val- oracion de los factores moderadores. EsicMarket, 131, 61-95.

Mayer, R. C., Davis, J. H., & Schoorman, F. D. (1995). An integrative model of organizational trust. Academy of Management Review, 20(3), 709-734.

Menard, S. W. (2009). Logistic regression: From introductory to advanced concepts and applications. Thousand Oaks, CA: SAGE.

Moliner, B. (2004). La formation de la sat- isfaccion/insatisfaccion del consumidor y del comportamiento de queja: Aplicacion al ambito de los restaurantes.

(Tesis Doctoral). Valencia, Spain: Departamento de Direccion de Empresas, Universidad de Valencia.Momparler, A. (2008). El desarrollo de la banca electronica en Espana: Un analisis comparativo entre entidades online y tradicionales en Espana y estados unidos. (TesisDoctoral). Valencia, Spain: Departamento de Organizacion de Empresas, Universidad Politecnica de Valencia.

Munoz-Leiva, F., Luque-Martinez, T., & Sanchez, J. (2010). How to improve trust toward electronic banking. Online Information Review, 34(6), 907-934. doi:10.1108/14684521011099405

Mures, M. J., Garcia, A., & Vallejo, M. E. (2005). Aplicacion del analisis discriminante y regresion logιstica en el estudio de la morosidad de las en- tidades financieras: Comparacion de resultados. Pecunia, 1, 175-199.

Oliver, R. L. (1980). A cognitive model of the antecedents and consequences of satisfaction decisions. JMR, Journal of Marketing Research, 17, 460-469. doi:10.2307/3150499

Oliver, R. L. (1981). Measurement and evaluation of satisfaction process in retail setting. Journal of Retailing, 57(3), 25-48.

Oliver, R. L. (1999). Whence consumer loyalty? Journal of Marketing, 63, 33-44. doi:10.2307/1252099

Ranawera, C., McDougall, G., & Bansal, H. (2005). A model of online customer behavior during the initial transaction: Moderating effects of customer characteristics. Marketing Theory, 5(1), 51-74. doi:10.1177/1470593105049601

Reichheld, F. F. (1996). The loyalty effect: The hidden force behind growth, profits, and lasting value. Boston, MA: Harvard Business School Press.

Rust, R., & Oliver, R. (1994). Service quality: Insights and managerial implications from the frontier. In R. T. Rust, & R. L. Oliver (Eds.), Service quality: New directions in theory and practice. Thousand Oaks, CA: Sage. doi:10.4135/9781452229102.n1

Santiago, J. M. (2008). Factores de proteccion y riesgo de infidelidad en la banca comercial. Cuadernos de Trabajo, 7, 1-15.

Segarra, P. (2007). Influencia de la heterogeneidad del mercado en la intention de comportamiento del consumidor: Respuestas a la actividad relational en la distribution de gran consumo. (Tesis Doctoral). Departamento de Gestion de Empresas, Universidad Rovira y Virgili.

Shankar, V., Urban, G., & Sultan, F. (2002). Online trust: A stakeholder perspective, concepts, implications, and future directions. The Journal of Strategic Information Systems, 11, 325-344. doi:10.1016/S0963-8687(02)00022-7

Sheth, J. N., Mittal, B., & Bruce, I. N. (1999).

Customer behavior: Consumer behavior & beyond. New York: The Dryden Press.

Stewart, K. (1998). An exploration of customer exit in retail banking. International Journal of Bank Marketing, 16(1), 6-14. doi:10.1108/02652329810197735

Yi, Y. (1990). A critical review of consumer satisfaction. In Review of Marketing. Academic Press.

KEY TERMS AND DEFINITIONS

Banking: Entities responsible for providing financial services credit and saving and other financial intermediation activities.

Confidence or Trust: The willingness of a consumer to be vulnerable to the actions of an online store based on the expectation that the online store will perform a particular action important to the consumer, irrespective of the ability to monitor or control the online store.

Drop-Out Risk: The risk exists that a customer cancels their contract with a financial institution and, subsequently, enter as a customer with another bank.

Logit: Parametric statistical technique of obtaining probability of occurrence of a particular event that is used to classify a set of subjects into two groups.

Loyalty: A customer's attitude toward the e-retailer that results in repeat buying behavior.

Receiver Operating Characteristic (ROC): A graphical plot which illustrates the performance of a binary classifier system as its discrimination threshold is varied.

Satisfaction: The result of comparison between a subjective experience and prior base reference.

ENDNOTES

Mayer et al. (1995).

Javalgi & Moberg (1997) in Segarra (2007) Caja Rural of Granada is a credit and savings bank that is part of Caja Rural group, including a structure of 203 offices (in the provinces of Granada, Malaga, Almeria and Madrid), a network of 234 ATMs, a staff of 832 employees and a positive balance of ˆ 20.1 million by the end of 2010.

This work was previously published in Electronic Payment Systems for Competitive Advantage in E-Commerce, edited by Francisco Liebana-Cabanillas, Francisco Munoz-Leiva, Juan Sanchez-Fernandez, and Myriam Martinez-Fiestas, pages 143-162, copyright 2014 by Business Science Reference (an imprint of IGI Global).

350

More on the topic CONCLUSION AND IMPLICATIONS:

- Cline W.. The Right Balance for Banks. Peterson Institute for International Economics,2017. — 281 p., 2017

- Hare C., Neo D. (eds.). Trade Finance: Technology, Innovation and Documentary Credit. Oxford University Press,2021. — 417 p., 2021

- Conclusion: A Christian Empire

- CONCLUSION

- CONCLUSION

- CONCLUSION AND FUTURE RESEARCH DIRECTIONS

- Conclusion

- Conclusion

- SUMMARY AND CONCLUSION

- CONCLUSION