EBIT, EBITDA, AND TOTAL ENTERPRISE VALUE

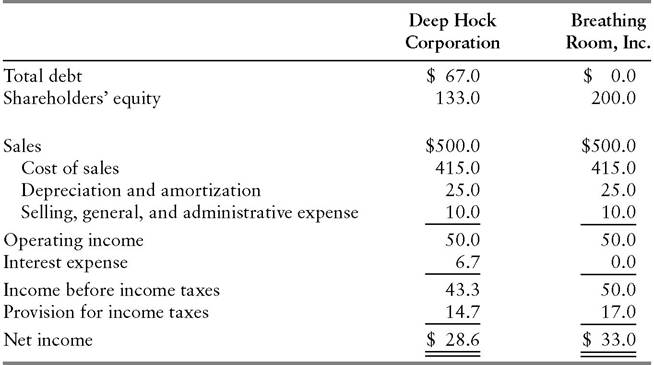

The fictitious case of Deep Hock and Breathing Room (Exhibit 8.1) illustrates the problems of relating net income to total enterprise value.

Both companies compete within the thingmabob industry. Their net profits for the latest year are $28.6 million and $33.0 million, respectively.When Breathing Room announces an agreement to be acquired by a multinational thingmabob producer for $666 million, Deep Hock’s founder and controlling shareholder, Philip Atlee, realizes that his company is a hot item in the mergers-and-acquisitions market. Trusting his own skills as a negotiator, he dispenses with M&A advisers and directly contacts an investor group that has previously approached him about buying Deep Hock. With thingmabob makers in strong demand, Atlee reasons, now is the time to sell.

Breathing Room’s selling price represented a multiple of 20 times its $33.0 million net income, in line with levels paid in other recent thingmabob acquisitions. On that basis, Atlee sets his sights on a price of 20 times Deep Hock’s $28.6 million of net income, or $572 million. He starts the negotiations at a higher level and, after some haggling, accepts a $572 million offer. After popping open the champagne, Atlee begins shopping for a yacht.

One month later, Atlee’s quiet retirement is rudely disturbed by news that the investors who bought Deep Hock have quickly resold it to a large industrial corporation for $666 million. The ex-CEO realizes, to his dismay,

EXHIBIT 8.1 Comparative Financial Data ($000 omitted) Year Ended December 31, 2001

that he apparently left $94 million on the table.

Dumbfounded by the turn of events, Atlee wonders why anyone would pay $666 million for Deep Hock. That is equivalent to the price paid for Breathing Room, a company with net income 15% higher. Surely, the investment group that paid $572 million for Deep Hock could not have boosted its profits materially in the space of a month. Neither have price-earnings ratios on thingmabob companies risen from 20 times in the interim.Determined to solve the mystery, Atlee seeks an explanation from his niece, Alana, an intern at an investment management firm. Drawing on her experience in analyzing financial statements, she obliges by pointing out that Deep Hock’s income from operations, at $50.0 million, is equivalent to Breathing Room’s. The difference at the bottom line arises because Breathing Room, with a debt-free balance sheet, has no interest expense.

“If I had bought your company, Uncle Phil,” Alana explains, “I would have immediately created pro forma financials showing what Deep Hock’s net income would be if all of its debt were paid off. Without the $6.7 million of interest expense, its income before income taxes would be $50.0 million, just like Breathing Room’s. At the company’s effective tax rate of 34%, the tax bill would be higher ($17.0 million versus $14.7 million), but net income would rise from $28.6 million to $33.0 million, the same as at Breathing Room. Then I would put the company up for sale at 20 times earnings, or $666 million. That’s probably what that group of investors did after they bought Deep Hock from you.”

Pausing for effect, Alana adds a detail concerning the transaction. “In order to raise Deep Hock’s earnings from $28.6 million to $33.0 million on an actual, as opposed to a pro forma basis, somebody has to retire the $67 million of debt. Assuming the investor group paid off the borrowings and sold the company debt-free, its net gain wasn’t $94 million, as you assumed, but only $27 million.

I mention that, just in case it’s any consolation to you. An alternative way to structure the deal would have been to make the $67 million debt assumption part of the $666 million purchase price. Either way, the net cash proceeds to the seller come to $599 million, for a quick profit of $27 million.”Still unhappy about failing to get top-dollar, but intrigued by his niece’s insights into financial statement analysis, Atlee asks a follow-up question. “I see now that applying a multiple to net income is not a good way to compare the total enterprise values of companies with dissimilar capital structures. This kind of situation must arise frequently. Is there a simple, direct valuation method that would have shown us what our company was truly worth, even if we weren’t clever enough to think of increasing the earnings by eliminating the debt?”

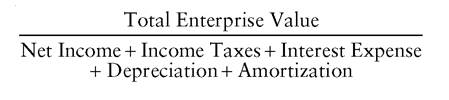

“Yes,” answers Alana. “Instead of calculating a multiple of net income on the comparable transaction, that is, the sale of Breathing Room, you should have calculated a multiple of EBIT. That stands for ‘earnings before interest and taxes.’ Add Breathing Room’s net income, income taxes, and interest expense to get the denominator. The numerator is the sale price:

![]()

“Let’s apply that same EBIT multiple of 13.32 to the comparable data from Deep Hock’s income statement,” Alana continues.

“So that’s how the pros ensure that valuation multiples will be consistent between companies with similar operating characteristics but different financial strategies?” asks the sadder but wiser ex-CEO of Deep Hock.

“Actually, Uncle Phil,” Alana replies, “there’s one more comparability issue that we need to address.

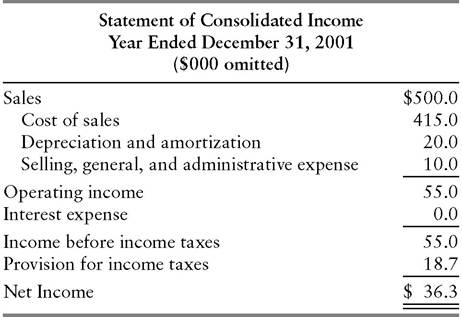

As you know, the accounting standards leave companies considerable discretion regarding the depreciable lives they assign to their property, plant, and equipment. The same applies to amortization schedules for intangible assets. Now, let’s imagine for a moment that Breathing Room’s managers had been writing off its assets not at a rate of $25 million a year, but only $20 million a year. That means that they would have been depreciating assets more slowly than you were, since the two companies’ rates of depreciation were identical. Here’s Breathing Room’s income statement, revised for this hypothetical change in depreciation rates (Exhibit 8.2).“Let’s calculate EBIT from this statement and apply the EBIT multiple that, according to our previous analysis, represents the value being assigned to thingmabob companies currently:

“It appears that simply by stretching out the depreciable lives of its assets, Breathing Room has boosted its value from $666 million to $732.6 million.

EXHIBIT 8.2 Breathing Room, Inc.

But that can’t be correct. Depreciation is an accrual, rather than a cash expense. Changing the depreciation rate for financial reporting purposes is therefore nothing but an alteration of a bookkeeping entry. It doesn’t increase or decrease the number of dollars actually flowing into the company. If management had changed the depreciation rate for tax reporting purposes, then the actual tax payments would decline. In that case, more dollars would flow into Breathing Room. But that’s another matter. What we’re concerned about is that Breathing Room might fetch a higher price than Deep Hock, merely because of a difference in accounting policy that represents no difference in economic value.

“To prevent this sort of distortion, we calculate a multiple on a base that’s even better than EBIT.

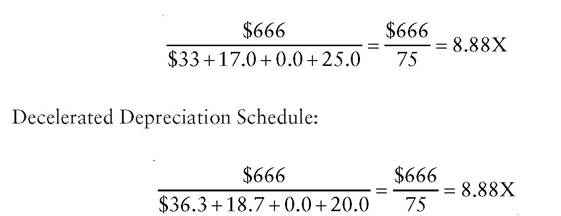

It’s called EBITDA. That stands for ‘earnings before interest, taxes, depreciation, and amortization.’ (Yes, I know that on the income statement, the correct order, moving from top to bottom, is EBDAIT. But the convention is to use the acronym EBITDA, pronounced “eebit-dah.”) Breathing Room’s EBITDA multiple is the same, whether it depreciates its assets at the rate of $25 million a year or $20 million a year:EBITDA Multiple =

Original Depreciation Schedule:

“If we calculate Deep Hock’s EBITDA and apply that same multiple of 8.88X, we get the correct total enterprise value of $666 million, meaning that we’ve achieved comparability with respect to both capital structure and depreciation policy:

“In summary, Uncle Phil, it’s much smarter to calculate total enterprise value as a multiple of EBITDA than to use net income. But the most important lesson is that if you decide to come out of retirement and start another company, be sure to hire me as your financial adviser.”

Atlee grins. “I guess you’re never too old to learn new and better approaches to financial statement analysis.”