INNOVATION IN FINANCIAL INDUSTRY

Providing sustainability has gained considerable importance in every field of global business as well as in the banking services (Karabay and Okay, 2012, 6). The Banking Sector is highly dynamic with its nature and considered as an influential engine of the economy.

On the other hand, the Insurance Sector plays an active role in the economy and is one of the most emerging industries in financial services. In industrialized economies, the elasticity of demand for insurance and significant shift of the fund to this sector has attracted attention to the financial industry. In the literature, it can be observed that researchers often use indicators of the R&D capability of countries and R&D expenditures of a company (see, Table 2).The management of risky R&D expenditures has become even more influential for the survival of a firm (Cassiman and Veugelers, 1999, 63). Research and development activities appear to be one of the most important activities required for innovation, especially technological innovation (Tsai, 2005, 796). Investing in R&D has many benefits like ;

1. R&D investments create a large number of innovative products and services (Korkmaz, 2010, 3322),

2. R&D investments provide business growth and support the competitive advantages (Korkmaz, 2010, 3320; ^alipinar and Baς, 2007, 446),

3. R&D expenditures are associated with the business outcomes of the innovation activities (Turkoglu and ^elikkaya, 2011; ^alipinar and Baς, 2007; Tuyluoglu and Saraς, 2012; Korkmaz, 2010), and

4. Information obtained from R&D activities is used in the development of a new product and the detection of a new market. This information contributes to development of a company by increasing its competitiveness (I§ik and Kilιnς, 2011, 17).

With the impact of globalization and liberalization, the restructuring of the markets fostered by the new entry of domestic and foreign banks and other financial institutions, concerns of the firms continue to increase regarding the protection of their market shares.

The firms that offer the fastest and best service to customers at the lowest cost anticipate and meet the needs of the evolving economic environment are likely to remain alive. At this point, the financial reform of innovation emerges as a defining element of the competitive process (Yagcilar, 2010, 84-85). While the attention to innovation in financial business remains so strong, the literature, on the other hand, presents various studies regarding innovation in financial services. The next section consists of a brief survey of the literature from a number of outstanding studies.Table 2. Global competitive index 2012-2013

| Capacity for Innovation | Company Spending on R&D | Innovation and Sophistication Scores | |||||

| Country | Value | Rank | Country | Value | Country | Rank | Score |

| Japan | 5.9 | 1 | Switzerland | 5.9 | Switzerland | 1 | 5.79 |

| Switzerland | 5.8 | 2 | Japan | 5.8 | Japan | 2 | 5.67 |

| Germany | 5.7 | 3 | Finland | 5.6 | Finland | 3 | 5.62 |

| Finland | 5.6 | 4 | Germany | 5.5 | Germany | 4 | 5.57 |

| Sweeden | 5.5 | 5 | Sweeden | 5.5 | Sweeden | 5 | 5.56 |

| Israel | 5.4 | 6 | Israel | 5.4 | Netherlands | 6 | 5.47 |

| United States | 5.2 | 7 | United States | 5.3 | United states | 7 | 5.42 |

| Netherlands | 5.1 | 8 | Singapore | 5.1 | United kingdom | 9 | 5.32 |

| Austria | 5.0 | 9 | Denmark | 4.9 | Austria | 10 | 5.30 |

| France | 5.0 | 10 | Taiwan,China | 4.9 | Singapore | 11 | 5.27 |

Source: Schwab, K.

2012. WEF, The Global Competitiveness Report, 2012-2013Literature Review

Benfratelo et al (2006) investigate the effect of local banking development on firms’ innovation activities, particularly for a large number of Italian banks during the 1990s. According to the findings, the probability of introducing a process or product innovation is significantly and positively related both to the firm size and the degree of banking development. They also present some evidence which indicates that banking development reduces the cash flow sensitivity of fixed investment spending, particularly for small firms, and that it increases the probability they will engage in R&D.

Uchupalanan (2000) examines the dynamic relationship between competitive strategy and information technology-based product and process innovation in financial services, particularly for the Thai banking industry in the late1960s. The results show the basic limitations of the Reverse Product Cycle approach and concludes with an alternative conceptual framework on a countryspecific innovation model.

Polatoglu and Ekin (2001) illustrate evidence on the consumer acceptance of the Internet banking (IB) services of a Turkish bank. They examine both consumer-related factors that may affect the adoption of an innovation or a product as well as organizational factors such as marketing effort. The results suggest that internet banking not only reduces operational cost to the bank but also leads to higher levels of customer satisfaction and retention.

Jayawardhena and Foley (2000) reveal that the Internet provides many opportunities for banks. An Internet bank can act as an online payment facilitator or as a provider of other services and shopping opportunity and therefore assist the growth of electronic commerce.

Another research was conducted by S antomero and Trester (1998) who state that the risky asset portfolio held by the banking sector unambiguously increases as a result of the innovations considered.

As a matter of fact, a reduction in illiquidity increases the banking sector’s willingness to provide risk capital for real sector investment.Tiwari et al (2007) investigate in their study the impact of Mobile Banking. They present five propositions about the role of innovative business solutions in the banking sectors.

When the insurance industry is considered, the number of studies are insufficient compared to the banking sector. The reason for this, in my opinion, is related to the dynamics of insurance sector. This is significantly observed in the related literature.

Pearson (1997) examines innovation in the British Insurance Sector between 1700 and 1914. In his study, the factors determining innovation were surveyed and comparisons were drawn with European Insurance. The findings suggest that insurance innovation ran broadly counter-cyclical to the innovation in the industry during this period, and was relatively undynamic.

Lado and Olivares (2001) reveal that there is a statistically significant and positive association between market orientation and business innovation performance in both the US and EU financial markets. According to them, more market oriented insurance firms are more innovative and have higher innovation success.

Barrett (1995) in his paper uses the case study method to explore how a Jamaican general insurance company responds to pressures by establishing a cross-cultural joint venture for IT development. The study focuses on visionary leadership which utilises the knowledge of the business along with double loop learning capabilities. According to the results, during the implementation of the innovation, leadership styles do not cope adequately with cultural characteristics.

Apart from the studies summarized above, there are various studies contributing to the innovation in the banking sector (Buzzacchi et al, 1995; Pennings and Harianto, 1992; Morgan et al, 1995) and the insurance sector (Storey and Christopher, 1996; Johne and Davies, 2000; Pon- tremoli, 2002; Lehmann and Zweifel, 2004).

In the following section, the phenomenon of innovation will be assessed within the context of banking and insurance sectors in Turkey.Innovation in the Turkish Banking Sector

The level of competition in the financial sector has a significant impact on the efficiency of the production of financial services, quality of financial products and degree of innovation in the sector (Claessens and Laeven 2004, 565; Karabay and Okay, 2012, 10). As the dynamics of the competition between the banks have begun to change after the restructuring program in the Turkish Banking Sector, measuring the competitive behavior of the banks has attracted a greater attention (Karabay and Okay, 2012, 3). Although innovation has been on the agenda since the early 1900s in the developed countries, the concept of innovation in Turkey began to take its place on the agenda in the mid 2000s (Elςi, 2008, 6). By virtue of the increasing pressure within the market and especially from the non-banking financial services sector, the banks now aim to move towards multi-channel banking services, provide innovative products and offer a wide range of choices with lower costs to customers. In addition, under the intense competition, a number of leading private Turkish Banks have been implementing programs and systems to provide better quality services (Yavas et al, 1997). They focus on innovating new products/ services (including offering multi-channel banking services) for their customers, in order to increase efficiency and customer satisfaction (Polatoglu and Ekin, 2001, 156).

The process of transition to the new economy affects the maturity of the Turkish Financial Sector. The Turkish Banking Sector can manage investments to increase the effectiveness of the marketing strategies more quickly than the banks in many countries around the world. For instance, transition to electronic commerce in the banking sector in Turkey has been much faster than in other sectors (Tolon, 2012, 1). Namely, a large number of customers in the sector consist of debit-card customers, depositors, lenders and credit card customers.

The Turkish Banking Sector, following the main developments in the last decade, has undergone a significant transformation since the 2001 crisis. In this period, several banks went bankruptcy because of their sunk costs. Later, the mergers and acquisitions, strategic investments, regulatory framework, risk management and market dynamics reshaped the global participation in the sector, as their relative shares changed.

The banking sector, a major locomotive of the financial system, is one of the fastest growing sectors in Turkey. As illustrated in Table 3, there are 49 banks as of 2012: 3 public deposit, 11 private deposit, 16 foreign deposit, 4 public investment, 5 private investment, 4 foreign investment, 4 participation banks and 2 banks under the supervision of the SDIF (Saving Deposit and Participation Funds) (TBB, 2012, ii-9).

Table 3. Structure of financial system in Turkey

| Banks | 49 |

| Factoring | 78 |

| Leasing | 31 |

| Financial Intermediaries | 13 |

| Asset Management | 9 |

| Intermediary Institutions | 73 |

| Portfolio Companies | 36 |

| Insurance Companies | 64 |

| Registered Institutions | 755 |

| Reinsurance Companies | 2 |

Source: BDDK, 2012,20. Data taken from the reports of BDDK, SPK, TSAKB. (November 2012 data are used.).

The banks operate in accordance with the provisions of the Banking Law No. 5411. As of 2010, 92, 6% of the assets of the sector belong to deposit banks; 4,3% of participation banks and 3,1% belong to development and investment banks (BDDK, 2010, iii-iv). Within the functional range, it can be seen that a large part of the sector’s total R&D expenditures are made by deposit banks. As illustrated in Table 4, the share of R&D expenditures of the commercial banks in 2010 was 96, 9%; the share of the investment and development banks stood at 2, 7% and 0, 4% of participation banks, respectively.

When we look at the Turkish Banking Sector, it can be seen that most of the merger and acquisition investments become from the growing consolidation among large banks and the foreign corporations’ willingness of affiliation with Turkish market. The largest deal of 2010 was the purchase of the Turkish Garanti Bank by Spanish banking giant “Banco Bilbao Vizcaya Argentaria SA (BBVA)” as BBVA purchased the 24.9% stake in the price of ˆ 4.2 billion. Lately, Turkish Economy Bank (TEB) and Fortis Bank merged under the name of Turkish Economy Bank (TEB) (KPMG, 2011, 26).

Technology is intensely used for the development of the Turkish Banking Sector and for the diversification of products and services, which has facilitated the increase on the demand of mobile and internet banking. Furthermore, by the process of harmonization within the financial sector, the growth of the volume of transactions within the mobile banking has also accelerated (BDDK, 2012, 21).

As mentioned before, R&D expenses are one of the most significant indicators of the development of a country as well as industries and corporations. R&D expenditures are of great importance not only for the development of new products and methods but also for the efficient use of existing or imported technology, adaptation or modification of activities at every stage of technological processes (Arican et al, 2011, 38). In the sector, large-scale banks are expected to take part more in R&D activities whereas small-scale banks have to invest more in R&D. It may be possible to enhance the financial capacity and that of financial innovations by increasing the investments on R&D activities (BDDK, 2010, vi).

The development of information technologies plays a central, though not exclusive, role in the innovation of many service activities. The implications of the rise of knowledge systems for the activities of service firms and, more specifically, for R&D innovation activities are complex and have to be analyzed at several levels. At the most immediate level, technology (in the commonsense usage of the word) is penetrating into the systems for processing and circulating information in a growing number of service firms. Some of them (banking and insurance in particular) have developed new technologies, for instance, expert systems and image processing techniques (Gadrey et al, 1994, 7).

Table 4. Research and development expenses: Concentration indicators

| R&D Expenses | 2005 | 2006 | 2007 | bgcolor=white>20082009 | 2010 | |

| Top 5 Banks | 91,4 | 91,6 | 93,4 | 97,1 | 95,3 | 94,5 |

| Top10 banks | 98,9 | 99,0 | 99,4 | 99,7 | 99,7 | 99,7 |

| Distribution by Scale | ||||||

| Large-Size Banks | 70,6 | 63,4 | 86,3 | 89,4 | 72,5 | 73,4 |

| Medium-Size Banks | 26,0 | 33,2 | 12,2 | 9,4 | 24,4 | 23,2 |

| Small-Size banks | 3,5 | 3,3 | 1,5 | 1,2 | 3,1 | 3,4 |

| Total | 100 | 100 | 100 | 100 | 100 | 100 |

| Functional Distribution | ||||||

| Deposit Banks | 99,9 | 99,8 | 98,7 | 98,9 | 97,1 | 96,9 |

| Development and Investment Banks | 0,1 | 0,0 | 1,3 | 1,0 | 2,1 | 2,7 |

| Participation Banks | 0,0 | 0,2 | 0,0 | 0,1 | 0,7 | 0,4 |

| Total | 100 | 100 | 100 | 100 | 100 | 100 |

Source: BDDK, 2010, p.82.

However, banks are structurally different from other sectors: that is to say, few resources are allocated to R&D and banks are fast in copying each other. In the Turkish Financial System the banks prefer to outsource the financing of an R&D activity and employ professionals for R&D divisions owing to the fact that outsourcing has today become a widely used funding method by enterprises. The information and specialization are intensively provided by consultancy firms or through R&D sector. When the expenses are considered, they are usually covered by general administrative or staff expenses. Regarding the banks, small-scale banks mainly may hesitate to outsource because they fear to lose direct control. The same is true for the insurance sector. Especially for the insurance services, the companies require significant market research (Yu, 2010, 17). Another contributing reason is that less resource is provided for organizational learning. Following the liberalization of the sector in the last decade, competition has greatly increased and banks have focused on innovation in order to remain competitive (Gopalakrishnan and Brierly, 2001, 126). This may have resulted from various reasons. First of all, although the basic functions of banks remain the same, financial intermediaries and banking services are under continuous structural change due to new technologies and liberalization. Secondly, lower cost or greater access to credit may affect product or process innovation playing an important role on the firm level inputs (fixed capital, etc.) (Benfratelo et al, 2006, 10). The change has also been encouraged by the development of storage and speed of data transfer (Joseph et al, 1999, 182).

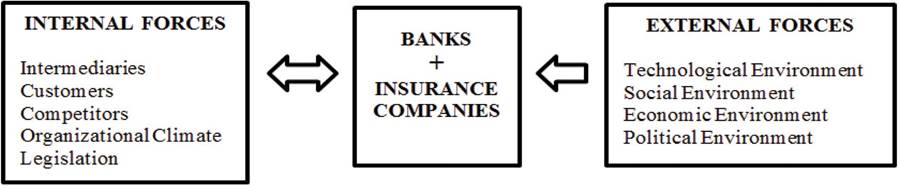

The properties of the environment in which businesses operate directly affect the performance of innovation, competitiveness through innovation, and the nature of the facilities (Elςi et al, 2008, 13). As illustrated in Figure 2, the banking sector is subject to both internal and external forces (Jayawardhena and Foley, 2000, 19).

The decision of implementing innovative strategies in banking is a managerial issue. Considering the innovation types explained in the previous sections, the introduction of process or product innovations is an inherently a riskier business than a mere expansion of the existing activities. Product innovation is so risky and uncollateraliz- able because it is related to expenditures on human c apital or entrants in the banking sector that provide substantial funding (Benfratelo et al, 2006, 8-9).

Banks, therefore, have to manage the innovation process accurately. The challenge that lies ahead for the banks is critical for several reasons. First, they need to satisfy customer needs that are complex and difficult to manage. Second, they need to face the increased competition from within the sector and from the new entrants coming into the financial services market. Third, they need to address the demands placed upon their intermediaries. Finally, they must continually invent new products and services in the light of the change described above (Jayawardhena and Foley, 2000, 29).

Figure 2. Dynamics of Turkish financial sector

The new strategic trend in the financial services is to consider the knowledge-based strategies as a competitive approach with the purpose of obtaining and maintaining a sustainable competitive power in the rising markets (Karabay, 2010, ii). The World Bank has adopted these strategies as a strategic breakthrough (Drew, 1999, 131). Similarly, on the global scene, all the positive developments in the Turkish Banking Sector encourage innovation in the sector (Arican et al, 2011, 147). There are various examples regarding innovation in the banks which mostly focus on the digital platform. For instance, Garantibank, a leading Turkish bank in the sector, has developed a service offered to customers, including a bank guarantee-warranty- for the new social media users, called “Ask Garanti.” By virtue of this campaign, the Bank’s Bonus Card holders will benefit from special campaigns and advantages of Garanti Link application through their facebook and twitter accounts. Banks also acquire a strong competitive advantage through creative products and distribution channels (Tolon, 2002, 3).

Innovation in the Turkish Insurance Sector

On account of the differences in structure, the innovation strategies have become a much more complex issue for the insurance services. This is because of the complex nature of the insurance services offered. Consumers sometimes find insurance services difficult to understand and evaluate. Therefore, they need additional services offered (i.e. branches, staff and other physical evidence) to judge the nature and quality of the insurance service. This is especially important for the financial services as the material benefits may be realized only in the long-term in the case of insurance services (Storey and Easingwood, 1994, 31).

Because of the rapidly rising share in the financial sector and increasing number of insurance companies, the insurance sector has become one of the locomotives in the Turkish Financial System. Today insurance is not only a must for all kinds of trade and industry but it is an important part of the social structure. Insurance, in conjunction with securement qualifications, is also an element of trust (Kιιsς∙ιι and Revanoglu, 2011, 131). Furthermore, fostered by the new regulations and law abidements, such as the private pension system, the number of investors and equity participation funds shows an increase compared to the previous years. However, the number of customers has remained relatively low in relation to the banking sector (BDDK, 2012, 20). By the end of 2012, 64 insurance and 2 reinsurance companies have been operating in the insurance sector. There are 53 private and 6 publicly-owned companies, of which 44 companies work with foreign partners (Retrived 18.04.2013 from http://www.tsrsb.org. tr/sayfa/turkiyede-sigortacilik).

Turkish Insurance Sector needs not only a more dynamic structure but also extra financial sources in order to accommodate the changing conditions in the market structure. Increasing competition in the insurance sector, facilitated by globalization, makes the mergers & acquisitions compulsory. This contributes to the enchancing premium production volumes, product and service variety, which makes foreign capital inflows more noteworthy. On the other hand, several obstacles which the sector faces (Ugur and Akdemir, 2011, 25) can be summarized as:

1. Gaps and deficiencies in the legislation,

2. Lower pricing as a result of intense competition,

3. Problems arising from the auditing and legal structure,

4. Problems emerging from imperfect competition, and

5. Lack of capital.

When the overall view of the sector is considered, the total premium production increased by 27,72% in the first quarter of 2013, compared to the same period last year and reached 2 billion 246 million euro. Part of the premium production of 2 billion 259 million euro came from non-life premium production while 386 million euro was obtained from life insurances. AXA was the top leading company with 289 million euro in the first quarter. This was followed by the production of 284 million euro by Anadolu Insurance and that of 203 million euro by Allianz (www.tsb.org.tr). In recent years, the premiums have declined in the developed countries, whereas in the developing countries the premium production has increased despite the crisis, as in the case of Turkey (Kuscu and Revanoglu, 2011, 141). However, new legal arrangements have been carried out in the Turkish Insurance Industry in recent years (Ba§turk, 2012, 1084). By 2002, the Turkish Insurance Market, for general insurance (broadly defined as non-life insurance), had become fiercely competitive. Local investors are not the only potential innovators in the insurance market. The rise of GDP/capital and the fall in inflation began to create huge growth for the insurance market in Turkey, becoming attractive for new entrants to the market (Deloitte, 2010, 13). New entrants within mergers and acquisitions to the market had fostered the development of attractive new insurance products. Asian investors are considerably interested in investing in Turkish Insurance sector. Sompo Japan Insurance, one of the insurance subsidiaries of NKSJ, bought the Fiba Insurance Co. in 2010 (KPMG, 2011, 26).

Furthermore, important changes especially the separation of life and pension companies in 2008 fostered the restructuring of the sector. Traditionally, the insurance companies in Turkey distribute their general products through corporations, agencies and brokers.

New forms of competition also continue to arise within the external market, such as banks, which have started offering general insurance products on a cross-selling basis called “bancassurance.” Both the requirements of the related laws, marketing and operational processes assert that the sector is under revision. Since Turkish Financial Industry has a banking-weighted structure and the rise in the share of “bank insurance” practices continues, technological infrastructure and data system have to be revised to obtain competitive advantage. In the sector, the insurance and individual retirement industries took part on the fourth line until the year 2007. Then it increased to the third line in the year 2008 and it maintained its place in the years 2009 and 2010 (Ba§turk, 2012, 1085). Technological developments are influential in the insurance sector. Insurance companies can follow their customers’ damage or loss practices through the websites. They are also able to perform online transactions like “Health Price Description,” “Claims Processing,” “Provisioning Operations on Pharmacy and Hospital,” “Market Operations on Damaged Cars,” “Portal Operations on Purchasing,” “Insurance Operations,” and “Policy & Receipt Imaging.” The technological developments and new innovative efforts have a positive effect in some branches. Intelligent building control systems, with its various functions in terms of insurance, have a significant impact on the insurance industry. One of them is the ability of protecting the buildings against fire as it will reduce the risk of personal harm. The early- warning of fire, by activating the anti-system or sprinkler system, allows people to evacuate the building quickly and safely. Secondly, it is important in terms of protection of the assets of households. Smart buildings can take control of the assets in case of floods and fires. This may help to reduce the cost to society. Finally, the third effect would be saving energy costs.

The importance of innovation strategies has been well recognized and the industry is growing by adopting technological and innovative requirements (Bayraktutan and §ahin, 2007, 96). Besides the innovation of products/services in the sector, the insurance industry also continue to invest in institutional developments. One of the significant developments in innovation is the TRAMER case. TRAMER was established to enable the database of the industry related to insurance and road traffic. TRAMER, co-operating with other databases of E-government, aims to provide reports, data and information for the users within the scope of the project.

Another similar development was in 2008, when the Insurance Information Centre (SBM) was established. SBM’s purpose of foundation was to collect all the information about life, health and traffic insurance at one center so that the branches of compulsory insurance and the insurance operations could be conducted within a more comprehensive and effective way (Ugur and Akdemir, 2011, 26).

Again one of the companies known as “Ray Insurance Co” has brought about new applications and innovations in the insurance sector. The company aims to expand in the foreign reinsurance market to promote the potential of insurance of the responsibilities of the stakeholders in order to be more competitive in the global reinsurance market so that they may obtain the best terms and prices (Retrieved 01.05.2013 from http://www. raysigorta.com.tr).

Another company, “Ergo Insurance” promotes another innovative campaign to attract new customers. The company has developed a new product called “Our Housing Policy” for individuals who want to insure their houses, household goods and belongings against the damages caused by home accidents. “Our housing policy” offers provision for the damages of the risks that the tenant, the landlord, and the neighbour can face (AkilliYa§am, 2012, 8). The companies offering general insurance products provide excellent examples of how chief executives of medium-sized companies react to the major changes in the competitive environment (Johne and Davies, 2000, 6). Companies that aim to have a significant economic part of the private pension market need to emerge with customer-focused and creative approaches to differ from their competitors. Similar to life and pension markets, these approaches will determine the winners and losers in the market considering the private pension market is relatively a new born branch in the sector (Bayraktutan and §ahin, 2007, 104).

However, the insurance market has several obstacles that prevent the sector from growing faster. The most significant one is the legal abidements that force one to one relationship with customers. For instance, in the individual pension system provision for pension intermediaries, licensed representatives can not perfom sales unless they have a wet signature. In addition to the services, pre-sales and post-innovation efforts for the implementation of alternative distribution channels in the sector appear to be essential (Bayraktutan and §ahin, 2007, 103).

Another impediment is related to R&D activities. R&D activities which are an important determinant of innovation capacity haven’t reached the expected levels in Turkey (Napier et al, 2004, 43). Moreover, decisions taken for the support of innovation in enterprises in Turkey still has severe problems, such as tax liabilities. Addtion- ally, special incentive mechanisms to support the formation and development of innovative companies are still insufficient (Calipinar and Bap, 2007, 447). Finally, it is essential to notify that the Turkish financial sector is quite susceptible to financial crises due to its fragile nature. 2008 has comprised significant affects of crisis and the sectoral mergers, take overs and acquisitions in the sector. This characteristic is assumed to be one of the critical factors preventing the sector to improve in terms of innovative capacity (Cagil and Karabay, 2011, 2-7).

Despite these obtacles acknowledged so far, the importance of the issue has been well recognized and the industry is growing by adapting technological and innovative requirements (Bayraktutan and §ahin, 2007, 96). In the recent years, the insurance industry has not only gained an increasing importance in the financial markets but has also begun to constitute a more dynamic structure. In this way, the insurance industry can realize the aims of generating profit, growth and preserving its existence while achieving the main objectives of sustaining the changing technology and the development of new services to customers (Yucememi§ et al, 2011, 54-55).